Presented by Elliot Turner of RGA Investment Advisors Disclaimers and Disclosures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Thursday 15 October 11:00 an Introduction to Cinerama and Widescreen Cinema 18:00 Opening Night Delegate Reception (Kodak Gallery) 19:00 Oklahoma!

Thursday 15 October 11:00 An Introduction to Cinerama and Widescreen Cinema 18:00 Opening Night Delegate Reception (Kodak Gallery) 19:00 Oklahoma! Please allow 10 minutes for introductions Friday 16 October before all films during Widescreen Weekend. 09.45 Interstellar: Visual Effects for 70mm Filmmaking + Interstellar Intermissions are approximately 15 minutes. 14.45 BKSTS Widescreen Student Film of The Year IMAX SCREENINGS: See Picturehouse 17.00 Holiday In Spain (aka Scent of Mystery) listings for films and screening times in 19.45 Fiddler On The Roof the Museum’s newly refurbished digital IMAX cinema. Saturday 17 October 09.50 A Bridge Too Far 14:30 Screen Talk: Leslie Caron + Gigi 19:30 How The West Was Won Sunday 18 October 09.30 The Best of Cinerama 12.30 Widescreen Aesthetics And New Wave Cinema 14:50 Cineramacana and Todd-AO National Media Museum Pictureville, Bradford, West Yorkshire. BD1 1NQ 18.00 Keynote Speech: Douglas Trumbull – The State of Cinema www.nationalmediamuseum.org.uk/widescreen-weekend 20.00 2001: A Space Odyssey Picturehouse Box Office 0871 902 5756 (calls charged at 13p per minute + your provider’s access charge) 20.00 The Making of The Magnificent Seven with Brian Hannan plus book signing and The Magnificent Seven (Cubby Broccoli) Facebook: widescreenweekend Twitter: @widescreenwknd All screenings and events in Pictureville Cinema unless otherwise stated Widescreen Weekend Since its inception, cinema has been exploring, challenging and Tickets expanding technological boundaries in its continuous quest to provide Tickets for individual screenings and events the most immersive, engaging and entertaining spectacle possible. can be purchased from the Picturehouse box office at the National Media Museum or by We are privileged to have an unrivalled collection of ground-breaking phoning 0871 902 5756. -

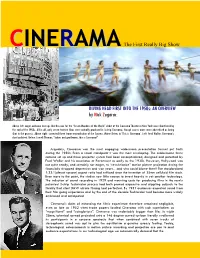

CINERAMA: the First Really Big Show

CCINEN RRAMAM : The First Really Big Show DIVING HEAD FIRST INTO THE 1950s:: AN OVERVIEW by Nick Zegarac Above left: eager audience line ups like this one for the “Seven Wonders of the World” debut at the Cinerama Theater in New York were short lived by the end of the 1950s. All in all, only seven feature films were actually produced in 3-strip Cinerama, though scores more were advertised as being shot in the process. Above right: corrected three frame reproduction of the Cypress Water Skiers in ‘This is Cinerama’. Left: Fred Waller, Cinerama’s chief architect. Below: Lowell Thomas; “ladies and gentlemen, this is Cinerama!” Arguably, Cinerama was the most engaging widescreen presentation format put forth during the 1950s. From a visual standpoint it was the most enveloping. The cumbersome three camera set up and three projector system had been conceptualized, designed and patented by Fred Waller and his associates at Paramount as early as the 1930s. However, Hollywood was not quite ready, and certainly not eager, to “revolutionize” motion picture projection during the financially strapped depression and war years…and who could blame them? The standardized 1:33:1(almost square) aspect ratio had sufficed since the invention of 35mm celluloid film stock. Even more to the point, the studios saw little reason to invest heavily in yet another technology. The induction of sound recording in 1929 and mounting costs for producing films in the newly patented 3-strip Technicolor process had both proved expensive and crippling adjuncts to the fluidity that silent B&W nitrate filming had perfected. -

History of Widescreen Aspect Ratios

HISTORY OF WIDESCREEN ASPECT RATIOS ACADEMY FRAME In 1889 Thomas Edison developed an early type of projector called a Kinetograph, which used 35mm film with four perforations on each side. The frame area was an inch wide and three quarters of an inch high, producing a ratio of 1.37:1. 1932 the Academy of Motion Picture Arts and Sciences made the Academy Ratio the standard Ratio, and was used in cinemas until 1953 when Paramount Pictures released Shane, produced with a Ratio of 1.66:1 on 35mm film. TELEVISION FRAME The standard analogue television screen ratio today is 1.33:1. The Aspect Ratio is the relationship between the width and height. A Ratio of 1.33:1 or 4:3 means that for every 4 units wide it is 3 units high (4 / 3 = 1.33). In the 1950s, Hollywood's attempt to lure people away from their television sets and back into cinemas led to a battle of screen sizes. Fred CINERAMA Waller of Paramount's Special Effects Department developed a large screen system called Cinerama, which utilised three cameras to record a single image. Three electronically synchronised projectors were used to project an image on a huge screen curved at an angle of 165 degrees, producing an aspect ratio of 2.8:1. This Is Cinerama was the first Cinerama film released in 1952 and was a thrilling travelogue which featured a roller-coaster ride. See Film Formats. In 1956 Metro Goldwyn Mayer was planning a CAMERA 65 ULTRA PANAVISION massive remake of their 1926 silent classic Ben Hur. -

ASPECT RATIO Aspect Ratios Are One of the More Confusing Parts of Video

ASPECT RATIO Aspect ratios are one of the more confusing parts of video, although they used to be simple. That's because television and movie content was all about the same size, 4:3 (also known as 1.33:1, meaning that the picture is 1.33 times as long as it is high). The Academy Standard before 1952 was 1.37:1, so there was virtually no problem showing movies on TV. However, as TV began to cut into Hollywood's take at the theater, the quest was on to differentiate theater offerings in ways that could not be seen on TV. Thus, innovations such as widescreen film, Technicolor, and even 3-D were born. Widescreen film was one of the innovations that survived and has since dominated the cinema. Today, you tend to find films in one of two widescreen aspect ratios: 1. Academy Standard (or "Flat"), which has an aspect ratio of 1.85:1 2. Anamorphic Scope (or "Scope"), which has an aspect ratio of 2.35:1. Scope is also called Panavision or CinemaScope. HDTV is specified at a 16:9, or 1.78:1, aspect ratio.If your television isn't widescreen and you want to watch a widescreen film, you have a problem. The most common approach in the past has been what's called Pan and Scan. For each frame o a film, a decision is made as to what constitutes the action area. That part of the film frame is retained, and the rest is lost.. This can often leave out the best parts of a picture. -

MARK FREEMAN Encyclopedia of Science, Technology and Society Ooks&Sidtext=0816031231&Leftid=0

MARK FREEMAN Encyclopedia of Science, Technology and Society http://www.factsonfile.com/newfacts/FactsDetail.asp?PageValue=B ooks&SIDText=0816031231&LeftID=0 WIDESCREEN The scale of motion picture projection depends upon the inter- relationship of several factors: the size and aspect ratio of the screen; the gauge of the film; the type of lenses used for filming and projection; and the number of synchronized projectors used. These choices are in turn determined by engineering, marketing and aesthetic considerations. Aspect ratio is the width of the screen divided by the height. The classic standard aspect ratio was expressed as 1.33:1. Today most movies are screened as 1.85:1 or 2.35:1 (widescreen). Films shot in these ratios are cropped for television, which retains the classic ratio of 1.33:1. This cropping is accomplished either by removing a third of the image at the sides of the frame, or by "panning and scanning." In this process a technician determines which portion of a given frame should be included. "Letterboxing" creates a band of black above and below the televised film image. This allows the composition as originally photographed to be screened in video. The larger the film negative, the more resolution. Large film gauges allow greater resolution over a given size of projected image. In the 1890's film sizes varied from 12mm to as many as 80mm, before accepting Edison's 35mm standard. Today films continue to be screened in a variety of guages including Super 8mm, 16mm and Super 16mm, 35mm, 70mm and IMAX. Cinema and the fairground share a common history in the search for technologically based spectacles and attractions. -

Film Essay for "This Is Cinerama"

This Is Cinerama By Kyle Westphal “The pictures you are now going to see have no plot. They have no stars. This is not a stage play, nor is it a feature picture not a travelogue nor a symphonic concert or an opera—but it is a combination of all of them.” So intones Lowell Thomas before introduc- ing America to a ‘major event in the history of entertainment’ in the eponymous “This Is Cinerama.” Let’s be clear: this is a hyperbol- ic film, striving for the awe and majesty of a baseball game, a fireworks show, and the virgin birth all rolled into one, delivered with Cinerama gave audiences the feeling they were riding the roller coaster the insistent hectoring of a hypnotically ef- at Rockaway’s Playland. Courtesy Library of Congress Collection. fective multilevel marketing pitch. rama productions for a year or two. Retrofitting existing “This Is Cinerama” possesses more bluster than a politi- theaters with Cinerama equipment was an enormously cian on the stump, but the Cinerama system was a genu- expensive proposition—and the costs didn’t end with in- inely groundbreaking development in the history of motion stallation. With very high fixed labor costs (the Broadway picture exhibition. Developed by inventor Fred Waller from employed no less than seventeen union projectionists), an his earlier Vitarama, a multi-projector system used primari- unusually large portion of a Cinerama theater’s weekly ly for artillery training during World War II, Cinerama gross went back into the venue’s operating costs, leaving sought to scrap most of the uniform projection standards precious little for the producers. -

Widescreen Weekend 2010 Brochure (PDF)

52 widescreen weekend widescreen weekend 53 2001: A SPACE ODYSSEY (70MM) REMASTERING A WIDESCREEN CLASSIC: Saturday 27 March, Pictureville Cinema WINDJAMMER GETS A MAJOR FACELIFT Dir. Stanley Kubrick GB/USA 1968 149 mins plus intermission (U) Saturday 27 March, Pictureville Cinema WIDESCREEN Keir Dullea, Gary Lockwood, William Sylvester, Leonard Rossiter, Ed Presented by David Strohmaier and Randy Gitsch Bishop and Douglas Rain as Hal The producer and director team behind Cinerama Adventure offer WEEKEND During the stone age, a mysterious black monolith of alien origination a fascinating behind-the-scenes look at how the Cinemiracle epic, influences the birth of intelligence amongst mankind. Thousands Now in its 17th year, the Widescreen Weekend Windjammer, was restored for High Definition. Several new and of years later scientists discover the monolith hidden on the moon continues to welcome all those fans of large format and innovative software restoration techniques were employed and the re- which subsequently lures them on a dangerous mission to Mars... widescreen films – CinemaScope, VistaVision, 70mm, mastering and preservation process has been documented in HD video. Regarded as one of the milestones in science-fiction filmmaking, Cinerama and IMAX – and presents an array of past A brief question and answer session will follow this event. Stanley Kubrick’s 2001: A Space Odyssey not only fascinated audiences classics from the vaults of the National Media Museum. This event is enerously sponsored by Cinerama, Inc., all around the world but also left many puzzled during its initial A weekend to wallow in the nostalgic best of cinema. release. More than four decades later it has lost none of its impact. -

(19) United States Pillarbox

US 20120013798A1 (19) United States (12) Patent Application Publication (10) Pub. No.: US 2012/0013798 A1 Arora et al. (43) Pub. Date: Jan. 19, 2012 (54) METHOD AND SYSTEM FOR ACHIEVING (52) US. Cl. ............................... .. 348/445; 348/E07.003 BETTER PICTURE QUALITY IN VARIOUS ZOOM MODES (57) ABSTRACT (76) Inventors: Gaurav Arora, Northborough, MA (US); Adil Jagmag, Hollis, NH A method and system are provided in Which a video image may be scaled from a ?rst to a second video format. The (Us) scaling may be a non-uniform scaling such as an anamorphic (21) Appl. No.: 13/013,307 scaling. When panning associated With the scaled video image is detected, one or more end portions of a current frame (22) Filed: Jan. 25, 2011 of the scaled video image may be adjusted, the adjustment being based on one or more frames of the scaled video image Related US. Application Data that are previous to the current frame. The adjustment may result from combining information from the corresponding (60) Provisional application No. 61/364,628, ?led on Jul. end portion of previous frames With the information of the 15, 2010. current frame. One or more end portions that are opposite to the ones adjusted may also be adjusted based on one or more Publication Classi?cation frames of the scaled video image that are subsequent to the (51) Int. Cl. current frame. The panning detected may be horizontal, ver H04N 7/01 (2006.01) tical, or a combination thereof. pillarbox 4:3 530a / 520 53Gb pillarbox Patent Application Publication Jan. -

Information on DW-TV 16:9 Widescreen Broadcasting

Information on DW-TV 16:9 widescreen broadcasting Why is transmission being changed to 16:9 widescreen format? What is anamorphic distortion of a television picture? Why are anamorphically distorted television pictures broadcast? What does letterboxing mean? What does Pan & Scan mean? How is the screen format identified when transmitted via satellite? What does WSS stand for? How is the screen format identified when using a SCART connector? FAQs How do I set my appliance to enable automatic screen size adjustment? Viewer’s Information - TV with 4:3 screen format The program is broadcast in 16:9 format; the picture on my 4:3 screen is vertically distorted. How can I solve the problem? My television has a 4:3 screen format; when the program is broadcast in 16:9 format some picture content is cut off on both sides. How can I solve the problem? My television has a 4:3 screen format; I would like to watch 16:9 screen broadcasts in letterbox format. How can I solve the problem? Viewer’s information - TV with 16:9 screen format The program is broadcast in 16:9 widescreen format; even though I have a 16:9 flat screen television, my picture is vertically distorted and has black bars on both sides. How can I solve the problem? A program broadcast in 4:3 format is horizontally distorted on my 16:9 flat screen television. How can I solve the problem? My television has a 16:9 widescreen format; if the program is broadcast in 4:3 format, some picture content is cut off at the top and bottom? How can I solve the problem? I receive DW programs via satellite or via cable; even though I have a 16:9 flat screen television, the broadcast in 16:9 format has black bars surrounding the picture. -

Digital Cinerama

Widescreen Weekend DDigitaligital CineramaCinerama - D150D150 CCinemaScopeinemaScope 5555 - Ultra-Ultra- PPanavisionanavision aandnd muchmuch muchmuch moremore MMarkark TTrompetelerrompeteler aatt thethe BradfordBradford WWidescreenidescreen WWeekendeekend The 14th. Annual Widescreen Weekend One of the most important and memorable was held from 19th. – 23rd. March at the moments in the history of film projection is National Museum of Media, in Bradford. “the Cinerama reveal” at the beginning of One hundred and five delegates travelled this film, when the curtains pull back from from all over the world to the Pictureville the small standard academy aspect ratio Cinema, based in the museum, for this black and white screen image to slowly annual event that celebrates and showcases reveal the giant colour widescreen aspect all aspects of widescreen cinema. Attendees ratio of the Cinerama image and also herald had travelled from as far away as Australia its fabulous accompanying magnetic track and New Zealand, China, America and sound. Even after all these years seeing this Canada, as well as from many countries at Bradford for the first, or a repeated time, both in Eastern and Western Europe, the is still a thrilling moment. (pictures below). Scandinavian countries and of course many parts of the UK and Ireland. The Dave Strohmaier and Randy Gitsch annual event has for many years been co- from Los Angeles (right) are amongst the programmed by Bill Lawrence and Thomas world’s leading experts, chroniclers and Hauerslev. This year the contribution documentary film makers on Cinerama of Duncan McGregor, the museum’s and its place in cinema history. They Projection Team Manager to the weekend’s attended this year for the fourth time. -

WIDE SCREEN MOVIES CORRECTIONS - Rev

WIDE SCREEN MOVIES CORRECTIONS - Rev. 2.0 - Revised December, 2004. © Copyright 1994-2004, Daniel J. Sherlock. All Rights Reserved. This document may not be published in whole or in part or included in another copyrighted work without the express written permission of the author. Permission is hereby given to freely copy and distribute this document electronically via computer media, computer bulletin boards and on-line services provided the content is not altered other than changes in formatting or data compression. Any comments or corrections individuals wish to make to this document should be made as a separate document rather than by altering this document. All trademarks belong to their respective companies. ========== COMMENTS FOR VERSION 1.0 (PUBLISHED APRIL, 1994): The following is a list of corrections and addenda to the book Wide Screen Movies by Robert E. Carr and R.M. Hayes, published in 1988 by McFarland & Company, Inc., Jefferson, NC and London; ISBN 0-89950-242-3. This document may be more understandable if you reference the book, but it is written so that you can read it by itself and get the general idea. This document was written at the request of several individuals to document the problems I found in the book. I am not in the habit of marking up books like I had done with this particular book, but the number of errors I found was overwhelming. The corrections are referenced with the appropriate page number and paragraph in the book. I have primarily limited my comments to the state of the art as it was when the book was published in 1988. -

Guide to Widescreen Notebook Displays

Guide to Widescreen Notebook Displays The earliest instance of the widescreen display being installed inside a notebook computer can be traced back to the Sony C1 which displayed a resolution of just 800 x 480. Widescreens made their official entrance in PC notebooks in 2003, although Apple preceded this by offering the 15” widescreen Power Mac. In 2005, the popularity of widescreen notebooks reached a new high with the unveiling of the Thinkpad widescreen Z60 series notebooks. Sony’s pioneering widescreen VAIO C1 notebook The question is: Is the widescreen format for everybody? A big part of the answer will depend on what a widescreen notebook or monitor is used to do. Here are some considerations that might help with your decision: 1. Widescreen Notebooks The length and width of a widescreen notebook’s screen set it apart from the standard notebook. The average notebook uses an aspect ratio of 4:3 and a resolution of 1024 x 768 pixels. The widescreen notebook breaks with tradition and increases screen size 25% lengthwise for proportions equal to that of the cinema screen or a widescreen LCD TV. Widescreen Acer Ferrari 4000 2. Widescreen Display Sizes The Sony C1 may have started it all, but it is by now considered only as a small-sized widescreen notebook, which is anything below 12.1”. Currently on offer are 8.9”, 10.6”, 11.1”, 12.1”, 13.3”, 14”, 15.4”, and 17” display sizes, with 19” products reportedly in the pipeline. 3. Widescreen Resolutions and their Corresponding Aspect Ratios Here are the common resolutions found in widescreen displays: 800 x 480 Representing an aspect ratio of 10:6, it was seen first in the Sony C1 notebook computer.