Enabling the Value of Time Implications for the Interior Design of Autonomous Vehicles

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Asset Management

A Cordence Perspective Asset Management Our view on how to unlock the value for your organization A uniquely agile partnership of independent management consulting firms, working together and sharing global industry insights, thought-leadership, and expertise across our interna- tional alliance A system driven approach to Enterprise Asset Management Our approach recognizes that the Management of major assets requires collaboration between asset owners, contractors, and other players in the Asset Management system We see Asset Owners facing five major challenges. • How to unlock the value of my assets? • What current practices should we stop and new practices should we adopt ? • How do we eliminate waste from the asset management system ? • How should we incorporate sustainability goals? • How do we get an AM organization that ensures that ‘everything keeps running and is also prepared for the future’? We help to create and accelerate those alliances in or between organizations Organizing a good asset management Perform is about insight into the Perform is about insight into the system often takes a transition from a performance of the Asset Management performance of the Asset Management historically grown maintenance approach system and therefore also of the AM system and therefore also of the AM to a system that allows decision makers to organization. For example with the organization. For example with the balance performance, risks and costs. We realization of Dashboards / Management realization of Dashboards / Management help to make -

Chapter 11 ) LAKELAND TOURS, LLC, Et Al.,1 ) Case No

20-11647-jlg Doc 205 Filed 09/30/20 Entered 09/30/20 13:16:46 Main Document Pg 1 of 105 UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK ) In re: ) Chapter 11 ) LAKELAND TOURS, LLC, et al.,1 ) Case No. 20-11647 (JLG) ) Debtors. ) Jointly Administered ) AFFIDAVIT OF SERVICE I, Julian A. Del Toro, depose and say that I am employed by Stretto, the claims and noticing agent for the Debtors in the above-captioned case. On September 25, 2020, at my direction and under my supervision, employees of Stretto caused the following document to be served via first-class mail on the service list attached hereto as Exhibit A, via electronic mail on the service list attached hereto as Exhibit B, and on three (3) confidential parties not listed herein: Notice of Filing Third Amended Plan Supplement (Docket No. 200) Notice of (I) Entry of Order (I) Approving the Disclosure Statement for and Confirming the Joint Prepackaged Chapter 11 Plan of Reorganization of Lakeland Tours, LLC and Its Debtor Affiliates and (II) Occurrence of the Effective Date to All (Docket No. 201) [THIS SPACE INTENTIONALLY LEFT BLANK] ________________________________________ 1 A complete list of each of the Debtors in these chapter 11 cases may be obtained on the website of the Debtors’ proposed claims and noticing agent at https://cases.stretto.com/WorldStrides. The location of the Debtors’ service address in these chapter 11 cases is: 49 West 45th Street, New York, NY 10036. 20-11647-jlg Doc 205 Filed 09/30/20 Entered 09/30/20 13:16:46 Main Document Pg 2 of 105 20-11647-jlg Doc 205 Filed 09/30/20 Entered 09/30/20 13:16:46 Main Document Pg 3 of 105 Exhibit A 20-11647-jlg Doc 205 Filed 09/30/20 Entered 09/30/20 13:16:46 Main Document Pg 4 of 105 Exhibit A Served via First-Class Mail Name Attention Address 1 Address 2 Address 3 City State Zip Country Aaron Joseph Borenstein Trust Address Redacted Attn: Benjamin Mintz & Peta Gordon & Lucas B. -

The Digital Future of Government Services a Global Point of View from the Experts of the Cordence Worldwide Partnership

A Cordence Perspective The digital future of government services A global point of view from the experts of the Cordence Worldwide Partnership Frank Weise – Horváth & Partners, Zoltan Tanács – IFUA / Horváth & Partners, Andrew Pennycuick – North Highland, Craig Spence – North Highland, Mark Dunwell – North Highland, Ageeth Telleman – Twynstra Gudde 2 Contents 01 Chapter 1: The transparent citizen – data security, privacy and the future of government in the new era of “dataism” answers by Zoltan Tanács, IFUA / Horváth & Partners, Hungary ............................. 05 02 Chapter 2: Digital by default - what citizen journeys look like in the digital future answers by Andrew Pennycuick and Craig Spence, North Highland, UK ......................................................... 08 03 Chapter 3: Disruptive technologies – solving tomorrow’s public sector challenges answers by Mark Dunwell, North Highland, UK ................................................................................................11 04 Chapter 4: Change management - successful digitization requires more than technology answers by Ageeth Telleman, Twynstra Gudde Netherlands ............................................................................14 05 Our experts ....................................................................................................................................................15 3 Digitization is not only changing our business environment introducing completely new disruptive business models but is also offering completely new -

Coping with Success / Managing Overcrowding In

COPING WITH SUCCESS MANAGING OVERCROWDING IN TOURISM DESTINATIONS December 2017 Copyright © McKinsey & Company and World Travel & Tourism Council Cover image: © petekarici/Getty Images 2 COPING WITH SUCCESS MANAGING OVERCROWDING IN TOURISM DESTINATIONS FOREWORD The Travel & Tourism (T&T) sector is a cornerstone of our global economy—and thanks to a growing middle class, improved digital and physical connectivity, and generations of people with an insatiable appetite to explore the world, it is expanding rapidly. Of course, this growth is accompanied by challenges, many of which can be summed up with the term “overcrowding.” Overcrowding is by no means new—but it seems to be coming to a head in popular destinations across the globe. As we set out to study overcrowding in tourism destinations, we had no illusions about the challenges we faced, including the following: Overcrowding is a complex issue. The problems associated with overcrowding can vary, from alienated local residents to overloaded infrastructure. The issues can affect both established and emerging destinations of all kinds. Countries, regions, cities, and individual sites, such as parks, beaches, and museums, may all be affected. The challenge is sometimes one of time, driven by high levels of seasonality or day visitors. Some destinations struggle to absorb crowds of domestic visitors, others face an influx of international visitors, and still others experience both. In short, the symptoms of overcrowding vary from place to place. Diverse interests are involved. Stakeholders include governments, comprised of elected officials and national, regional, and local agencies; tourism management and promotion agencies; commercial organizations, ranging from multinational corporations to locally owned small businesses; those employed in the sector; local residents; nonprofit and social sector organizations; and, finally, tourists themselves. -

AMIR NIKRAVAN Born 1983 Los Angeles, CA Lives and Works in Los

VARIOUS SMALL FIRES 812 NORTH HIGHLAND AVENUE LOS ANGELES 90038 VSF [email protected] / 310.426.8040 AMIR NIKRAVAN Born 1983 Los Angeles, CA Lives and works in Los Angeles, CA Education 2011 MFA, Painting, University of California Irvine, Irvine, CA 2004 BFA, Painting and Drawing, San Francisco Art Institute, San Francisco, CA Solo and two-person Exhibitions 2018 (Forthcoming), Various Small Fires, Los Angeles, CA 2017 Rational Design, Nathalie Karg Gallery, New York, NY 2015 Amir Nikravan & Paul Pescador / 1:1, ASHES / ASHES, Los Angeles, CA Aggregate, Jonathan Viner Gallery, London, UK VSF Presents Amir Nikravan, The Armory Show, New York, NY Masks, Arndt Singapore, Singapore Reps/Sets Jonathan Viner Gallery, LISTE, Basel, Switzerland 2014 Merge Visible, Various Small Fires, Los Angeles, CA Amir Nikravan and Jigger Cruz, ARNDT Berlin, abc ART BERLIN, Berlin, Germany Amir Nikravan and Wes Noble, Luce Gallery, Turin, Italy 2012 Gemini, Pepin Moore, Los Angeles, CA 2011 Internal, Contemporary Arts Center, Irvine, CA Kelly Cline and Amir Nikravan, Workspace, Los Angeles CA 2010 Thresholds, Rosamund Felsen Gallery, Santa Monica, CA Group Exhibitions 2017 Shifting Landscapes, Sophia Contemporary, London, UK 2016 2016 Tomorrow Never Happens, SAMEK Museum, Lewisburg, PA Boys and Girls Can Still Draw, Nathalie Karg Gallery, New York, NY 2015 Surface of Color, curated by Paul Pescador, The Pit, Los Angeles, CA Bloody Red Sun of Fantastic L.A., PIASA, Paris, France I Know You Got Soul, Arndt Singapore, Singapore 2014 The Go Between, Museo di Capodimonte, -

831 N. Highland, Los Angeles, CA, 90038 +1.323.397.9225 Diane

Diane Rosenstein Fine Art 831 North Highland Avenue Los Angeles, CA 90038 T. +1.323.397.9225 www.dianerosenstein.com The Black Mirror January 19 – March 9, 2013 Gallery Hours: Tuesday – Saturday 10:00am – 6:00 pm Opening: Saturday, January 19, 2013, 7:00 – 9:00 pm Curators: James Welling and Diane Rosenstein Associate Curator: Farrah Karapetian Diane Rosenstein Fine Art is pleased to present The Black Mirror, a group show curated by James Welling and Diane Rosenstein. This will be primarily an all-black show, engaging the literal and associative properties of reflective black surface materials. The power and provocation of each work is in the proposal it makes for presence in the absence of a diversified palette. The Black Mirror, opening Saturday, January 19th, will inaugurate Rosenstein's new gallery at 831 N. Highland Avenue in Hollywood. The title of the show is inspired by Henri Matisse's painting Anemones au Miroir Noir (1918-19) and also the history of artistic engagement with Claude glass, convex mirrors used especially in the 18th and 19th century by painters. A layer of black tint was placed over the mirror's surface producing impure images. The convexity of the mirror and its shape were variable, but in general were designed to enhance perception at differing distances. The relations of this exhibition's individual works to the conceit of The Black Mirror are as complex as are their relations to one another. Each work alters the viewer's perception, as might a Claude glass, using, by turns, literal or figurative transformation of objects, space, and material to suggest differing relations between an artwork and a self. -

JESPER JUST Education the Royal Danish Academy of Fine Art

VARIOUS SMALL FIRES 812 NORTH HIGHLAND AVENUE LOS ANGELES 90038 VSF [email protected] / 310.426.8040 JESPER JUST Born 1974 Copenhagen, Denmark Lives and works in New York, NY Education 2003 The Royal Danish Academy of Fine Art, Copenhagen, Denmark Solo and Two-person Exhibitions 2015 Landscape for Living, Various Small Fires, Los Angeles, CA Servitudes, Palais de Tokyo, Paris, France 2014 Jesper Just: This Is a Landscape of Desire, De Moines Art Center, De Moines, Iowa This Is a Landscape of Desire, The National Museum of Modern and Contemporary Art (MMCA), South Korea Jesper Just, ARoS, Aarhus, Denmark Jesper Just, Portland Museum, Portland, Jesper Just, Galleri Nicolai Wallner, Copenhagen, Denmark 2013 Intercourses, Danish Pavilion, 55th Venice Biennale, Venice, Italy Jesper Just, Galerie Perrotin, Paris, France This is a Landscape of Desire, Herning Museum for Contemporary Art, Jutland, Denmark 2012 This Nameless Spectacle, James Cohan Gallery, New York, NY This Nameless Spectacle, University of Michigan Museum of Art, Ann Arbor, MI This Nameless Spectacle, Galleri Nicolai Wallner, Copenhagen, Denmark 2011 Jesper Just: Sirens of Chrome, University of California Riverside, Sweeney Art Gallery, Riverside, CA Jesper Just: This Unknown Spectacle, Musee d’Art Contemporain Du Val-de-Marne, Val-de-Marne, France A Vicious Undertow, Single-Chanel Series, Des Moines Art Center, Des Moines, IA John Curtin Gallery, Perth, Australia This Nameless Spectacle, BALTIC Centre for Contemporary Art, Gateshead, United Kingdom Chambers Fine Arts, Beijing, China -

Curated by Joshua Friedman Kohn Gallery

myselves CURATED BY JOSHUA FRIEDMAN KOHN GALLERY ARTISTS KATE BARBEE ROMARE BEARDEN AMOAKO BOAFO JARVIS BOYLAND WILLIAM BRICKEL CHELSEA CULPRIT BRUCE CONNER rafa esparza HAMISHI FARAH NASH GLYNN HEIDI HAHN NAOTAKA HIRO LOIE HOLLOWELL OSCAR YI HOU GERALD LOVELL JESSE MOCKRIN SOPHIA NARRETT JAGDEEP RAINA ERIN M. RILEY MOISES SALAZAR PAUL MPAGI SEPUYA EMILY MAE SMITH CHIFFON THOMAS WOLFGANG TILLMANS SALMAN TOOR XIUCHING TSAY SKYE VOLMAR Sophia Narrett, Heart, 2018, embroidery thread, acrylic, aluminum and fabric, 25 x 7 1/2 inches detail Kate Barbee, Rain, 2018-20, acrylic, oil paint, painted scraps, thread, oil pastel, cold wax on canvas, 72 x 72 inches detail Chiffon Thomas, I’ll See For You If You Speak For Me, 2020 Embroidery foss, fabric, thread, chalk, pastel and window screen mesh, 21 1/2 x 20 inches detail Chiffon Thomas, Too Soon, 2020 Embroidery foss, fabric, leather, rusted paper, thread, chalk, pastel and window screen mesh, 21 1/2 x 28 inches detail Chiffon Thomas, I’ll See For You If You Speak For Me, 2020 Embroidery foss, fabric, thread, chalk, pastel and window screen mesh, 21 1/2 x 20 inches Moises Salazar, Clean, 2020, yarn and glitter on satin, 29 x 29 inches detail Moises Salazar, In my feelings, 2020, yarn and glitter on satin, 29 x 29 inches rafa esparza, Guadalupe Macias Ybarra. ¿Qué?, 2018, adobe, wood, chain link fence and acrylic, 93 x 45 x 1 1/2 inches detail installation Gerald Lovell, Sham, 2020, oil on panel, 40 x 30 inches detail Amoako Boafo, Untitled, 2018, oil on canvas, 52 1/2 x 46 inches Oscar yi Hou, Mlle. -

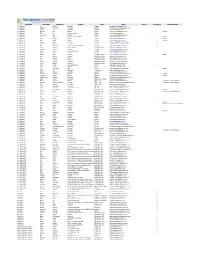

Firm Name First Name Last Name Position Office Email Phone Recruiter? Diversity Group A.T

Firm Name First Name Last Name Position Office Email Phone Recruiter? Diversity Group A.T. Kearney Joe Adamski Manager Atlanta [email protected] A.T. Kearney Matthew O'Connor Associate Atlanta [email protected] A.T. Kearney David Qu Manager Atlanta [email protected] A.T. Kearney Mui-Fong Goh Partner Beijing [email protected] Women A.T. Kearney Zhao Liu Business Analyst Beijing [email protected] A.T. Kearney Chee Wee Gan Principal Beijing chee [email protected] A.T. Kearney Amy Still Manager, Data Analytics Chicago [email protected] GALA A.T. Kearney Laura Gurski Partner Chicago [email protected] Women A.T. Kearney Beth Bovis Partner Chicago [email protected] Women A.T. Kearney Alissa Palko Recruiter Chicago [email protected] Y A.T. Kearney Christine Nicholas Recruiter Chicago [email protected] Y A.T. Kearney Erin Reichert Manager, HR & Recruitment Chicago [email protected] Y A.T. Kearney Andre Kimura Senior Associate Sao Paolo, Brazil [email protected] A.T. Kearney Zeshaun Ahmad Associate Chicago [email protected] A.T. Kearney Anna Kraft Sourcing Associate Chicago [email protected] A.T. Kearney Calvin Tam Associate Toronto [email protected] A.T. Kearney Braxton Sisco Manager Dallas/Fort Worth [email protected] GALA A.T. Kearney Juan Llanos Principal Dallas/Fort Worth [email protected] A.T. Kearney John Hubach Officer Dallas/Fort Worth [email protected] A.T. Kearney Alan Heckler Principal Dallas/Fort Worth [email protected] A.T. -

NYC's Nightlife Economy

NYC’s Nightlife Economy Impact, Assets, and Opportunities Commissioned by The Mayor’s Office of Media and Entertainment About the Mayor’s Office of Media and Entertainment The Mayor’s Office of Media and Entertainment encompasses the key economic and creative sectors of film, TV, theater, music, advertising, publishing, digital content and real estate as it relates to these industries. The office promotes New York City as a thriving center of creativity, issuing permits for productions filming on public property, and facilitating production throughout the five boroughs. In June 2017, Mayor Bill de Blasio announced that the Mayor’s Office of Media and Entertainment (MOME), led by Commissioner Julie Menin, would support NYC’s diverse nightlife community with a department dedicated to its management. The Office of Nightlife cements New York’s position as a leader in this growing global movement that recognizes nightlife’s value to cities, and represents the first time a NYC agency has been tasked with promoting an economically and culturally vibrant nightlife industry. About the Consulting Team The NYC Nightlife Economy report was conducted by a three-firm consulting team: The North Highland Company, Econsult Solutions, Inc. (ESI), and Urbane Development. The North Highland Company The North Highland Company is a global consulting organization serving multiple industries and functional areas. The Firm’s Consumer, Media and Entertainment, Public Sector and Strategy practices contributed to this study. Econsult Solutions, Inc. Econsult Solutions, Inc. (ESI) provides businesses and public policy makers with economic consulting services in urban economics, real estate economics, transportation, public infrastructure, development, public policy and finance, community and neighborhood development, planning, as well as litigation support. -

DIANE ROSENSTEIN GALLERY 831 North Highland Avenue, Los

DIANE ROSENSTEIN GALLERY ELEANOR ANTIN (USA, b. 1935) EDUCATION 1958 BA The City College of New York SOLO EXHIBITIONS 2019 Time’s Arrow, LACMA, Los Angeles (travels to The Art Institute of Chicago) 2017 Romans & Kings, Richard Saltoun, London, UK 100 Boots: The Lost Picture Show, Alden Projects, New York City, NY 2016 Eleanor Antin: What time is it?, Diane Rosenstein Gallery, Los Angeles, CA I wish I had a paper doll I could call my own…, Ronald Feldman Fine Arts, New York, NY 2014 Eleanor Antin: Passengers, Diane Rosenstein Gallery, Los Angeles, CA Multiple Occupancy: Eleanor Antin’s “Selves,” ICA, Boston, MA 2013 Multiple Occupancy: Eleanor Antin’s “Selves,” The Miriam and Ira D. Wallach Art Gallery, Columbia University, New York City, NY 2009 Classical Frieze, Galerie Erna Hecey, Brussels, Belgium 2008 Eleanor Antin: Historical Takes, San Diego Museum of Art, San Diego, CA Helen’s Odyssey, Ronald Feldman Fine Arts, New York City, NY 2007 The Empire of Signs, Galerie Erna Hecey, Brussels, Belgium 2006 100 Boots, Galerie Erna Hecey, Brussels, Belgium 2005 Roman Allegories, 2005 & 100 Boots, Marella Arte Contemporanea, Milan, Italy Roman Allegories, Ronald Feldman Fine Arts, New York City, NY 2004 The Last Days of Pompeii, Mandeville Art Gallery, San Diego, CA 2002 The Last Days of Pompeii, Marella Arte Contemporanea, Milan, Italy The Last Days of Pompeii, Craig Krull Gallery, Santa, Monica, CA Eleanor Antin, Galerie Hilger, Vienna, Austria The Last Days of Pompeii, Ronald Feldman, Fine Arts, New York City, NY 2001 Eleanor Antin: Real -

Panoramaseminary Vol

Pittsburgh Theological PANORAMASeminary Vol. XLVI No. 3 Spring 2007 ISBN 8755-0954 A Seminary of the Presbyterian Church (U.S.A.) ■ Founded 1794 All in the Family Lenten Journey to Russia College Chaplains’ Association Peace and Justice Fellowship PANORAMA CONTENTS All in the Family 3 is published in the spring, late summer, and winter seasons by Pittsburgh Theological Lilly Award to Dr. Creach 6 Seminary. It is intended to address timely issues related to the Seminary and to inform alumnae/i and other friends of the activities and programs of the school. It also commu- Peace and Justice Group 7 nicates information about alumnae/i news and recent location changes. Cunningham New Vice President 8 Zeitah Excavations 9 Editor: Lisa Dormire ’86 Meetings with Supreme Court Justices 11 Assistant Editor: Melissa Logan A Dinosaur for Mr. Rogers 12 Designer: Kathy Boykowycz Lecturer Links Evolution and Religion 15 Lenten Journey to Russia 16 Pittsburgh Theological Seminary Offi ce of Seminary Relations Chaplains’ Association Meets at PTS 20 616 North Highland Avenue Pittsburgh Faculty-Staff News 22 Pittsburgh, PA 15206-2596 Theological Alumnae/i News 23 412-362-5610 fax 412-363-3260 Seminary Driving Lessons 26 www.pts.edu Mourning, Past all tears now, But today, Mary sits very still In these dark woods Holy Like a rabbit Where preying wolves howl, Saturday Frozen Hope lies, In underbrush of cover, Like a faraway angelic dream Waiting for time, like danger, to pass Of Messianic ideals, Teresa L. Stricklen Over and around and through her Among shattered limbs In the hope Cut down by high and mighty winds, Th at by marking its fl ow, So that, frozen in time’s unnatural stream She can bathe in its mourning Babbling the obdurate eternity of love, Until all will somehow be safe Mary sits still, And cleansed into deliberate motion again.