Making Cross-Border Banking Easier

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

18 February 2019 Solvency and Diversification in Insurance Remain Key Strengths Despite Change in Structure

FINANCIAL INSTITUTIONS ISSUER IN-DEPTH Lloyds Banking Group plc 18 February 2019 Solvency and diversification in insurance remain key strengths despite change in structure Summary RATINGS In 2018, Lloyds Banking Group plc (LBG) altered its structure to comply with the UK's ring- Lloyds Banking Group plc Baseline Credit a3 fencing legislation, which requires large banks to separate their retail and SME operations, Assessment (BCA) and deposit taking in the European Economic Area (EEA) from their other activities, including Senior unsecured A3 Stable the riskier capital markets and trading business. As part of the change, LBG designated Lloyds Bank plc as the“ring-fenced” entity housing its retail, SME and corporate banking operations. Lloyds Bank plc It also assumed direct ownership of insurer Scottish Widows Limited, previously a subsidiary Baseline Credit A3 Assessment (BCA) of Lloyds Bank. The changes had little impact on the creditworthiness of LBG and Lloyds Adjusted BCA A3 Bank, leading us to affirm the deposit and senior unsecured ratings of both entities. Scottish Deposits Aa3 Stable/Prime-1 Widows' ratings were unaffected. Senior unsecured Aa3 Stable » LBG's reorganisation was less complex than that of most UK peers. The Lloyds Lloyds Bank Corporate Markets plc Banking Group is predominantly focused on retail and corporate banking, and the Baseline Credit baa3 required structural changes were therefore relatively minor. The group created a small Assessment (BCA) separate legal entity, Lloyds Bank Corporate Markets plc (LBCM), to manage its limited Adjusted BCA baa1 Deposits A1 Stable/Prime-1 capital markets and trading operations, and it transferred its offshore subsidiary, Lloyds Issuer rating A1 Stable Bank International Limited (LBIL), to LBCM from Lloyds Bank. -

Natwest Markets N.V. Annual Report and Accounts 2020 Financial Review

NatWest Markets N.V. Annual Report and Accounts 2020 Financial Review Page Description of business Financial review NWM N.V., a licensed bank, operates as an investment banking firm serving corporates and financial institutions in the European Economic Presentation of information 2 Area (‘EEA’). NWM N.V. offers financing and risk solutions which 2 Description of business includes debt capital markets and risk management, as well as trading 2 Performance overview and flow sales that provides liquidity and risk management in rates, Impact of COVID-19 3 currencies, credit, and securitised products. NWM N.V. is based in Chairman's statement 4 Amsterdam with branches authorised in London, Dublin, Frankfurt, Summary consolidated income statement 5 Madrid, Milan, Paris and Stockholm. Consolidated balance sheet 6 On 1 January 2017, due to the balance sheet reduction, RBSH 7 Top and emerging risks Group’s regulation in the Netherlands, and supervision responsibilities, Climate-related disclosures 8 transferred from the European Central Bank (ECB), under the Single Risk and capital management 11 Supervisory Mechanism. The joint Supervisory Team comprising ECB Corporate governance 43 and De Nederlandsche Bank (DNB) conducted the day-to-day Financial statements prudential supervision oversight, back to DNB. The Netherlands Authority for the Financial Markets, Autoriteit Financiële Markten Consolidated income statement 52 (AFM), is responsible for the conduct supervision. Consolidated statement of comprehensive income 52 Consolidated balance sheet 53 UK ring-fencing legislation Consolidated statement of changes in equity 54 The UK ring-fencing legislation required the separation of essential Consolidated cash flow statement 55 banking services from investment banking services from 1 January Accounting policies 56 2019. -

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Standard Chartered Bank, Impacts of E-Banking and the Customer Perception on E-Banking

Strategic Information Management Nowshad M Shawon Abstract Bank is one the most important financial sectors. Internet has made the banking function easier and changed the traditional banking system. The aim of this report is to compare the historical performance of Barclays and Standard chartered bank, impacts of E-banking and the customer perception on E-banking. To make the report uneatable, the author included brief history of the banks. In the first section of the analysis, the author discussed the historical performance of Barclays and Standard chartered through the use of MS-Excel. In the second section, the author discussed the positive and negative impacts of E-banking and finally at the end of this report, the customer perception on E-banking has been discussed through primary data collected by a questionnaire from the customers of Barclays and Standard chartered. NMS Page 1 Table of Contents 1 Introduction .................................................................................................................................... 4 1.1 Background of the Banks ........................................................................................................ 4 1.1.1 Barclays Plc ...................................................................................................................... 4 1.1.2 Standard Chartered Plc ................................................................................................... 5 2 Comparative analysis of Historical performances of Barclays Plc & Standard Chartered Plc -

Natwest, Lloyds Bank and Barclays Pilot UK's First Business Banking Hubs

NatWest, Lloyds Bank and Barclays pilot UK’s first business banking hubs NatWest, Lloyds Bank and Barclays have announced that they will pilot the UK’s first shared business banking hubs. The first hub will open its door in Perry Barr, Birmingham today. The pilot will also see five other shared hubs open across the UK in the coming weeks The hubs have been specifically designed to enable businesses that manage cash and cheque transactions to pay in large volumes of coins, notes and cheques and complete cash exchange transactions. They will be available on a trial basis to pre-selected business clients in each local area and will offer extended opening times (8am to 8pm) 7 days a week, providing business and corporate customers more flexibility to manage their day-to-day finances. The hubs will be branded Business Banking Hub and they have been designed to enable business customers from Natwest, Lloyds Bank and Barclays to conduct transactions through a shared facility. Commenting on the launch of the pilot, Deputy CEO of NatWest Holdings and CEO of NatWest Commercial and Private Banking Alison Rose said: “We have listened to what our business customers really want from our cash services. It is now more important than ever that we continue to offer innovative services, and we are creating an infrastructure that allows small business owners and entrepreneurs to do what they do best - run their business. I look forward to continued working with fellow banks to ensure the UK's businesses are getting the support they deserve." Commenting on the support this will provide businesses, Paul Gordon, Managing Director of SME and Mid Corporates at Lloyds Bank Commercial Banking said: “SMEs are the lifeblood of the UK economy. -

Meet the Exco

Meet the Exco 18th March 2021 Alison Rose Chief Executive Officer 2 Strategic priorities will drive sustainable returns NatWest Group is a relationship bank for a digital world. Simplifying our business to improve customer experience, increase efficiency and reduce costs Supporting Powering our strategy through customers at Powered by Simple to Sharpened every stage partnerships deal with capital innovation, partnership and of their lives & innovation allocation digital transformation. Our Targets Lending c.4% Cost Deploying our capital effectively growth Reduction above market rate per annum through to 20231 through to 20232 CET1 ratio ROTE Building Financial of 13-14% of 9-10% capability by 2023 by 2023 1. Comprises customer loans in our UK and RBS International retail and commercial businesses 2. Total expenses excluding litigation and conduct costs, strategic costs, operating lease depreciation and the impact of the phased 3 withdrawal from the Republic of Ireland Strategic priorities will drive sustainable returns Strengthened Exco team in place Alison Rose k ‘ k’ CEO to deliver for our stakeholders Today, introducing members of the Executive team who will be hosting a deep dive later in the year: David Lindberg 20th May: Commercial Banking Katie Murray Peter Flavel Paul Thwaite CFO CEO, Retail Banking NatWest Markets CEO, Private Banking CEO, Commercial Banking 29th June: Retail Banking Private Banking Robert Begbie Simon McNamara Jen Tippin CEO, NatWest Markets CAO CTO 4 Meet the Exco 5 Retail Banking Strategic Priorities David -

Banco Santander: Extending Financial Se Vices to Low-Income Communities in B Azil

CASE STUDY Banco Santander: Extending financial se vices to low-income communities in B azil Initi ti e Descriptio In September 2013, Santander Microcrédito joined the Business Call to Action with a commitment to serve 124,799 low-income consumers with microfinance services and to disburse up to US$490 million in microcredit loans by 2015. The goals of Santander Microcrédito are to: • Disburse R$540 million (US$230 million) in microcredit operations by the end of 2014; and R$600 million (US$260 million) in 2015; and • Attain 126,000 active microcredit clients by the end of 2014 and 131,000 additional clients Business Model Santander Microcredit is an example of how Banco in 2015. In Brazil, 52 million people and Santander Brasil contributes to approximately 25 million informal reducing social inequalities in entrepreneurs lack access to the for- the country. When we started mal banking system. Santander Brasil thinking about how to launch Microcredit, a company affiliated with the microcredit programme, we Banco Santander Brasil, was founded decided that it should be a in 2002 to offer microcredit operations model in which all involved to support business entrepreneurs parties could benefit. that could not access formal banking services. To this end, Santander Brasil Microcredit offers loans that con- tribute to employment and income generation for low-income people. Currently, Santander Microcredit The average monthly income in Brazil operates in more than 600 municipali- is US$6801 and 21 percent of the pop- ties (in 10 Brazilian states), and has 25 ulation live below the poverty line2. branch offices. -

Frequently Asked Questions

This document is provided for informational purposes only. It does not constitute a solicitation to buy/sell any product or security issued by the KBC Group or its subsidiaries. The information provided in this document is condensed and/or simplified and therefore incomplete. The document may contain forward- looking statements with respect to the strategy, earnings and capital trends of KBC, involving numerous assumptions and uncertainties. The risk exists that these statements may not be fulfilled and that future developments differ materially. Moreover, KBC does not undertake any obligation to update this document in line with new developments. The document may also contain non-IFRS information. By reading this document, each person is deemed to represent that he/she possesses sufficient expertise to understand the risks involved. KBC Group and its subsidiaries cannot be held liable for any damage resulting from the use of the information. KBC Group – who’s who in the Executive Committee, situation at 01 May 2014 Johan Thijs Group Chief Executive Officer °1965 Belgian Master’s Degree in Science (Applied Mathematics) and Actuarial Sciences (KU Leuven) Joined KBC Group or its pre-merger entities in 1988 Career o 1988 Various actuary functions in life and non-life insurance, ABB Insurance o 1995 Head of non-life department, Limburg regional office, ABB Insurance o 1998 Provincial manager Limburg and Eastern Belgium, KBC Insurance o 2001 Senior General Manager non-life insurance, KBC Insurance o 2006 Member of the Management Committee -

Web Updation FAQ's Version 3

FAQ’S for Barclaycard customers 1. Customer: How do I know when my Standard Chartered Bank Credit Card will become active? There is an Instructions letter with your new card that instructs the date on which your new Standard Chartered Bank Credit Card will become active and your Barclaycard will become inactive. A sms will also be sent to you before the activation of your new Standard Chartered Bank Credit Card. 2. Customer: I not received any card from Standard Chartered Bank after I received the Welcome Letter at the end of February 2012? We are dispatching cards in batches. You will receive an SMS from Standard Chartered Bank when your card is dispatched to you. The SMS will contain details of the Airway Bill No. of the courier which you can use to track your card. In case, you do not receive this SMS or your card by the 1st week of June, please write to Customer Care at [email protected] or call Standard Chartered Bank phone banking at the following numbers http://www.standardchartered.co.in/personal/ways-to-bank/en/phone-banking12.html 3. Customer: Do I need to give details about my account again or will it be transferred automatically? You do not need to do anything as all the information that is currently with Barclays bank will be transferred to Standard Chartered Bank in order to have your new card account set up. However if you have set up ECS/SI instructions on your current Barclaycard, then once you have received the new Standard Chartered Bank Credit Card please call the number at the back of your new Standard Chartered Bank Credit Card to provide ECS/SI instructions. -

Nordea Group Annual Report 2018

Annual Report 2018 CEO Letter Casper von Koskull, President and Group CEO, and Torsten Hagen Jrgensen, Group COO and Deputy CEO. Page 4 4 Best and most accessible advisory, with an 21 easy daily banking experience, delivered at scale. Page 13 Wholesale Banking No.1 relationship Asset & Wealth bank in the Nordics Management with operational Personal Banking 13 excellence. Page 21 Commercial & Business Banking Our vision is to become the lead- ing Asset & Wealth Manager in the 25 Nordic market by 2020. Page 25 Best-in-class advisory and digital experience, 17 ef ciency and scale with future capabilities in a disruptive market. Page 17 Annual Report 2018 Contents 4 CEO letter 6 Leading platform 10 Nordea investment case – strategic priorities 12 Business Areas 35 Our people Board of Directors’ report 37 The Nordea share and ratings 40 Financial Review 2018 46 Business area results 49 Risk, liquidity and capital management 67 Corporate Governance Statement 2018 76 Non-Financial Statement 78 Conflict of interest policy 79 Remuneration 83 Proposed distribution of earnings Financial statements 84 Financial Statements, Nordea Group 96 Notes to Group fi nancial statements 184 Financial statements Parent company 193 Notes to Parent company fi nancial statements 255 Signing of the Annual Report 256 Auditor’s report Capital adequacy 262 Capital adequacy for the Nordea Group 274 Capital adequacy for the Nordea Parent company Organisation 286 Board of Directors 288 Group Executive Management 290 Main legal structure & Group organisation 292 Annual General Meeting & Financial calendar This Annual Report contains forward-looking statements macro economic development, (ii) change in the competitive that reflect management’s current views with respect to climate, (iii) change in the regulatory environment and other certain future events and potential fi nancial performance. -

Analisis De La Responsabilidad Social Corporativa Del Sector Bancario

Facultad de Ciencias Económicas y Empresariales ANÁLISIS DE LA RESPONSABILIDAD SOCIAL CORPORATIVA EN EL SECTOR BANCARIO ESPAÑOL Autor: María Sánchez Barbero Director: Laura Gismera Tierno MADRID | Abril 2020 RESUMEN/ABSTRACT Resumen La Responsabilidad Social Corporativa es una práctica en auge desde finales de los años 90 y su función principal es satisfacer a los grupos de interés –stakeholders- de las empresas que la aplican. La RSC busca cumplir con los intereses internos de las compañías y de la sociedad, mejorando así la imagen corporativa de la empresa. El sector bancario español lleva casi 20 años aplicando esta corriente empresarial hasta el punto que, las distintas entidades bancarias que conforman el sector, desarrollan modelos de RSC prácticamente idénticos. Este trabajo tiene como principal objetivo analizar la Responsabilidad Social Corporativa en el sector bancario español. En primer lugar, se expondrá una aproximación al concepto de Responsabilidad Social Corporativa, así como su evolución, las principales teorías sobre la materia y ciertos aspectos diferenciales y normativos con los que se identifica la RSC. Así mismo, se realizará un análisis de la evolución del sector bancario en los últimos años junto con las oportunidades y amenazas a las que se enfrenta el mismo. Finalmente, se analizará el modelo de RSC de cinco de las entidades bancarias más importantes a nivel nacional: Santander, BBVA, CaixaBank, Bankinter y Banco Sabadell. Palabras clave: Responsabilidad Social Corporativa (RSC), economía, entidades bancarias, stakeholders, interés, sostenibilidad, acción social. Abstract Corporate Social Responsibility has been a growing practice since the late 1990s and its main function is to satisfy the stakeholders of the companies that apply it. -

2021 VIB Belg BT Infomemo 04-08-2021.Pdf

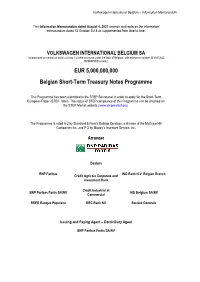

Volkswagen International Belgium – Information Memorandum This Information Memorandum dated August 4, 2021 amends and replaces the information memorandum dated 18 October 2018 as supplemented from time to time. VOLKSWAGEN INTERNATIONAL BELGIUM SA (incorporated as naamloze vennootschap / société anonyme under the laws of Belgium, with enterprise number 443.615.642 (RPM/RPR Brussels)). EUR 5,000,000,000 Belgian Short-Term Treasury Notes Programme This Programme has been submitted to the STEP Secretariat in order to apply for the Short-Term European Paper (STEP- label). The status of STEP compliance of this Programme can be checked on the STEP Market website (www.stepmarket.org). The Programme is rated A-2 by Standard & Poor’s Ratings Services, a division of the McGraw-Hill Companies Inc. and P-2 by Moody’s Investors Service, Inc. Arranger Dealers BNP Paribas ING Bank N.V. Belgian Branch Crédit Agricole Corporate and Investment Bank Crédit Industriel et BNP Paribas Fortis SA/NV ING Belgium SA/NV Commercial BRED Banque Populaire KBC Bank NV Société Générale Issuing and Paying Agent – Domiciliary Agent BNP Paribas Fortis SA/NV Volkswagen International Belgium – Information Memorandum Potential investors are invited to read this Information Memorandum, the Conditions and the selling restrictions, prior to investing. Each holder of Treasury Notes from time to time represents through its acquisition of a Treasury Note that it is and, as long as it holds any Treasury Notes, shall remain an Eligible Holder. Nevertheless, a decision to invest in