Growing Connecting

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ambank and Digi Partner to Lower Barriers for Smes to Adopt Epayments

Media Release 6 August 2018 AmBank and Digi partner to lower barriers for SMEs to adopt e- payments Partnership aims to enable 10,000 terminals to accept Digi’s e-payment solution in the next 12 months AmBank (M) Berhad (AmBank) continues to step up its digital strategy by opening up its wide merchant network to accept Digi’s vcash QR code as an additional payment service. This ‘e-payment partnership’ with Digi Telecommunications Sdn Bhd (Digi) takes on a two-pronged approach. Firstly, AmBank’s merchant point-of- sale (POS) terminals will be enabled to accept vcash QR code transactions. What this means is that vcash users can pay for their transactions via Digi’s vcash mobile app. vcash users only need to scan the QR code to pay. Secondly, Digi will be signing up small and mid-sized enterprise (SME) merchants under the Master Merchant programme with AmBank. This will translate to more merchants accepting vcash payments, while growing AmBank’s merchant base. “This strategic tie-up with Digi complements our efforts in broadening our product offerings to existing merchants as well as new merchants, while staying relevant and competitive in the digital landscape. It is also part of our ongoing efforts to support Bank Negara Malaysia’s agenda to accelerate the country's migration to electronic payments (e-payments) as we move towards becoming a cashless society,” said Dato’ Sulaiman Mohd Tahir, Group Chief Executive Officer, AmBank Group. “In advancing eWallet payment technology, we are working on more strategic partnerships to offer wider acceptance to our customers. -

BERHAD (Company No

Serial No. 001 STRICTLY PRIVATE AND CONFIDENTIAL AMBANK (M) BERHAD (Company No. 8515-D) INFORMATION MEMORANDUM IN RELATION TO THE PROPOSED ISSUE OF, OFFER FOR SUBSCRIPTION OR PURCHASE OF, OR INVITATION TO SUBSCRIBE FOR OR PURCHASE OF UP TO RM 4.0 BILLION IN NOMINAL VALUE OF TIER 2 SUBORDINATED NOTES (“SUBORDINATED NOTES”) UNDER A SUBORDINATED NOTES PROGRAMME Principal Adviser/Lead Arranger/Lead Manager (Company No. 23742-V) This Information Memorandum is dated 16 December 2013 RESPONSIBILITY STATEMENT The directors of AmBank (M) Berhad (“AmBank”) have given approval for the issuance of an Information Memorandum (“IM”) relating to the issuance of tier 2 subordinated notes (the “Subordinated Notes”) pursuant to a Subordinated Notes programme of up to RM4.0 billion in nominal value (“Subordinated Notes Programme”). AmBank accepts full responsibility for the accuracy of the information contained in this IM. AmBank confirms that, to the best of its knowledge and belief: (a) this IM contains all information with respect to AmBank that is material in the context of the purpose for which this IM is issued; (b) the information and data contained in this IM are true, accurate and not misleading in all material respects; and (c) there is no material omission of any information and data from this IM. Enquiries have been made by AmBank to ascertain that all material facts have been disclosed and to verify the accuracy of all information and statements in this IM. ACKNOWLEDGEMENT AmBank hereby acknowledges that it has authorised AmInvestment Bank Berhad (“AmInvestment Bank” or “Lead Arranger/Lead Manager”) to circulate or distribute this IM on its behalf in respect of the issuance of Subordinated Notes pursuant to a Subordinated Notes Programme to prospective investors and that no further evidence of authorisation is required. -

Page 1 of 10 Delivery of Bank Confirmation Request: List of Contact Details for 26 Commercial Banks in Malaysia

Delivery of Bank Confirmation Request: List of Contact Details for 26 Commercial Banks in Malaysia (including their respective Islamic banking arms) Updated as at 18 February 2020 No Bank Contact Person 1. Affin Bank Berhad At domicile branch where account is maintained. For further enquiries, please contact: 1. Name: Fadhnita Binti Ariffin Designation: Executive, Loan Operation Telephone No: 03-27315269 Fax No: 03-20314984 Email Address: lad- [email protected] Name: Mok Soo Pon Designation: Acting Manager, Loan Operation Maintenance Section Telephone No: 03-2055 9172 Fax No: 03-20314984 Email Address: [email protected] Correspondence Address: Loan Administration and Documentation Department 9th Floor, Menara Affin 80 Jalan Raja Chulan 50200 Kuala Lumpur 2. Name: Ahmad Zahuri Idris Designation: Manager, Operations Telephone No: 03-20559646 Fax No: - Email Address: [email protected] Name: Anita Mahadi Designation: Team Leader, Admin Telephone No: 03-20559164 Fax No: - Email Address: [email protected] Correspondence Address: Special Asset Management 7th Floor, Menara Affin 80, Jalan Raja Chulan 50200 Kuala Lumpur Dewan Akauntan, Unit 33-01, Level 33, Tower A, The Vertical, Avenue 3 Bangsar South City, No.8, Jalan Kerinchi, 59200 Kuala Lumpur, Malaysia Page 1 of 10 Website: www.mia.org.my | Tel: + 603 2722 9000 | Fax: + 603 2722 9100 No Bank Contact Person 3. Name: Bramma Suriya A/P Ramaloo Designation: Unit Head, Customer Fullfilment Telephone No: 03-2055 9804 Fax No: - Email Address: [email protected] Name: Wan Mohd Faizal wan Yazdad Designation: Officer, Customer Fullfilment Telephone No: 03-20559100 Fax No: - Email Address: [email protected] Correspondence Address: Consumer Operations 8th Floor, Menara Affin 80, Jalan Raja Chulan 50200 Kuala Lumpur 2. -

Digi.Com Fact Sheet

DiGi.Com Fact Sheet Corporate Info DiGi.Com Berhad is listed on Bursa Malaysia Securities Berhad and is part of the global telecommunications provider, Telenor Group. Its mobile service operations are undertaken by its wholly-owned subsidiary, DiGi Telecommunications Sdn Bhd. DiGi commenced operations in May 1995 when it launched its fully digital GSM1800 services, the first digital mobile communications service in Malaysia. In the last five years, DiGi’s revenue has grown to RM6.7 billion from RM4.9 billion with a subscriber base of 11.0 million. DiGi focuses on making it easy, keeping it relevant and providing the best deals to ensure excellent customer experience in mobile and internet services. DiGi has now expanded its HSPA+ enabled 3G network to 83% population coverage and increased its own and jointly built fibre network to more than 4,400 kilometres nationwide, building the vital backhaul connectivity needed to support always-on, high-speed data experience. With the completion of modernized network in 2013, DiGi will continue its focus on delivering higher quality network experience, stronger internet usage and positive overall customer satisfaction. DiGi’s presence as a leader in prepaid services has spearheaded in a number of industry benchmarks for simplicity and innovation. In addition, DiGi has also revitalised its postpaid services under DiGi Postpaid and DiGi Business to deliver quality voice and mobile internet services to individuals and corporate customers. Through its corporate initiative, Deep Green, DiGi is committed -

Governance and Financial Report 2020 Eport 202 0 About This Report Integrated Reporting Approach

G O V E R NANCE AND FINANCIAL GOVERNANCE AND FINANCIAL REPORT 2020 R EPORT 202 0 ABOUT THIS REPORT INTEGRATED REPORTING APPROACH RATIONALE PGB has remained strong and robust since the liberalisation of the gas market in 2016. We have embraced the challenges presented by the new business landscape by adapting our strategies and operations accordingly. We are now well-prepared in shaping the path ahead of us. Our steadfastness and resilience are driven by our ongoing strategy – R2 Game Plan: 301Q99 Pushing Forward. We are focused on being the preferred solutions partner to our stakeholders. We became a leaner and more streamlined organisation. We also increased our efforts in digitalisation, while also reinforcing our systems and processes to drive growth and create long-term value for our stakeholders. Befitting our role as a Leading Gas Infrastructure and Centralised Utilities Company, we will continue Pushing Forward towards Shaping our New Norm as we progress responsibly to meet the nation’s needs. At PETRONAS Gas Berhad (PGB), we advocate transparency to stakeholders and we are honoured to present this report as the primary source of information on our Group’s financial and non-financial performance for 2020. It forms part of our reporting suite which comprises: OUR REPORTING SUITE INTEGRATED REPORT GOVERNANCE & FINANCIAL REPORT SUSTAINABILITY REPORT Our Integrated Report is the primary Our Governance and Financial Report provides Our Sustainability Report details our report to our stakeholders, showcasing our comprehensive approach towards efforts and commitment towards creating our value creation proposition and protection of value in our activities, together a sustainable business, positioned for delivery. -

Go V Ernance & a Udited Financial S T a Tement S 2 0 19

GOVERNANCE & AUDITED FINANCIAL STATEMENTS 2019 Governance & Compliance Information Governance & Audited Financial Statements 2019 Contents GOVERNANCE Group Corporate Structure 2 Profile of Directors 4 Board Remuneration 8 Directors’ Training List 2019 9 Profile of Group Senior Leadership Team 12 Profile of Operating Companies’ Management Team 18 Significant Milestones in 2019 20 Awards 21 Statement on Risk Management and Internal Control 26 Board Audit Committee Report 36 Strengthening Data Privacy and Cyber Security in 2019 38 Additional Compliance Information 40 AUDITED FINANCIAL STATEMENTS Directors’ Responsibility Statement 44 Audited Financial Statements for the financial year ended 31 December 2019 45 OTHER INFORMATION Shareholding Statistics 195 List of Top Ten Properties 198 Net Book Value of Land & Buildings 199 Glossary 200 Axiata’s Integrated Annual Report 2019 Suite is made up of the following: IAR Integrated Annual Report 2019 GAFS Governance & Audited SNCR Sustainability & National Financial Statements 2019 Contribution Report 2019 Governance Governance & Compliance Information Governance & Audited Financial Statements 2019 Group Corporate Structure* as at 31 March 2020 AXIATA GROUP BERHAD Celcom Axiata Berhad Axiata SPV1 Axiata Investments 1 (Malaysia) (Labuan) Limited (India) Limited (Labuan) (Mauritius) Celcom Resources Berhad Axiata SPV2 Axiata (Malaysia) Berhad Investments 2 (Malaysia) (India) Limited Celcom Networks Sdn Bhd (Mauritius) (Malaysia) Axiata Management Celcom Mobile Sdn Bhd Services Sdn Bhd (Malaysia) (Malaysia) -

True Visa Credit Card – Other Benefits

TRUE VISA MASTERCARD – FREQUENTLYTRUE VISA CREDIT ASKED CARD QUESTIONS – OTHER BENEFITS Get more out of life with your TRUE VISA Credit Card. Indulge in the finer things in life with our irresistible array of promotions, rewards and exclusive member privileges. Get to enjoy more lifestyle choices with us. Supplementary Card Share the pleasures and privileges of your card membership with your loved ones with the gift of a Supplementary Card. AmBank Spot Deals and Privileges Discover exciting deals and rewards with AmBank Spot. Enjoy special offers and privileges when you use your AmBank Credit Card at over 700 AmBank Spot merchant locations across the country. Indulge in dining privileges that will set your gastronomic senses alive, plus other fun-filled deals and promotions that let you shop, unwind and be entertained. Stay updated at ambankspot.com with the latest red hot AmBank Spot offers. Auto BILLPAY Pay your monthly bills on time, no rush and no long queue. Just enroll your bills with Auto BILLPAY, a free service for your convenience, and you can have your monthly bills automatically debited from your TRUE VISA Credit Card. Enjoy this hassle free utility bill payment for service providers such as Tenaga Nasional Berhad, Telekom Malaysia, Astro, Telco (Maxis, DiGi & Celcom), Allianz Insurance, MCIS Zurich and Zurich Insurance. 0% Easy Payment Plan (EPP) Stretch your money further at no additional cost with this interest free instalment plan. Enjoy up to 36 months of interest free instalment payments when you indulge yourself on big ticket items at over 1,000 participating merchant locations nationwide from mobile devices, electrical to home furnishings and personal wellness or beauty. -

LIST of LABUAN BANKS and INVESTMENT BANKS in LABUAN (Updated As at 10 May 2014) Printed on 6/12/2014

LIST OF LABUAN BANKS AND INVESTMENT BANKS IN LABUAN (Updated as at 10 May 2014) Printed on 6/12/2014 MARKETING OFFICE / CO-LOCATED OFFICE NAME OF BANKS TYPE OF LICENCE LABUAN OFFICE ADDRESS OFFICER IN-CHARGE ADDRESS 1 PUBLIC BANK (L) LTD. Labuan Bank Level 8 (A) & (B) N/A Mr. Alexander Wong Main Office Tower (Manager) Financial Park Complex Jalan Merdeka 87000 Labuan F.T. Tel : 087-411 898 Fax : 087-413 220 E-mail: [email protected] 2 MAYBANK INTERNATIONAL Labuan Bank Level 16(B), Main Office Tower Mr. Jubely bin Pa (L) LTD. Financial Park Complex (CEO) Jalan Merdeka 87000 Labuan F.T. N/A Tel : 087-414 406 / 414 566 Fax : 087-414 806 E-mail: [email protected] 3 STANDARD CHARTERED BANK Labuan Bank Level 10(F), Main Office Tower N/A Mr. John Han Yun Leong OFFSHORE LABUAN BRANCH Financial Park Complex (General Manager) Jalan Merdeka 87000 Labuan F.T. Tel : 087-417 200 / 417 201 Fax : 087-417 202 E-mail: [email protected] 4 THE HONGKONG AND Labuan Bank Level 11(B1), Main Office Tower 12th Floor, North Tower, Menara HSBC Ms. Foo Lee Choo SHANGHAI BANKING Financial Park Complex No.2, Leboh Ampang (Principal Officer) CORPORATION LIMITED Jalan Merdeka 50100 Kuala Lumpur OFFSHORE BANKING UNIT LABUAN 87000 Labuan F.T. Tel : 03-2075 3961 / 2075 3308 Tel : 087-599090 Fax : 03-2031 0840 Fax : 03-2179 6493 E-mail: [email protected] 5 RHB BANK (L) LTD. Labuan Bank Level 15(B), Main Office Tower Level 11 Tower 1, RHB Centre Ms. -

(TRUE SA/TRUE SA-I) Bonus Rate Campaign

Terms and Conditions TRUE Savers Account/TRUE Savers Account-i (TRUE SA/TRUE SA-i) Bonus Rate Campaign This Amended Terms and Conditions for AmBank (M) Berhad and AmBank Islamic Berhad: TRUE Savers Account/TRUE Savers Account-i (TRUE SA/TRUE SA-i) Bonus Rate Campaign will supersede the existing Terms and Conditions with effect from 12 July 2021. 1. Clause 4.4 (B) Spend (a) has been added in blue font to reflect the changes in Campaign Mechanics. 2. Clause 4.4 (B) Spend (d) has been added in blue font to reflect the changes in Campaign Mechanics REMINDER: The Eligible Customers (as defined below) are hereby reminded to read and understand the terms and conditions below which are available at www.ambank.com.my/TnC. If the Eligible Customers do not understand any of the terms and conditions and the updated terms and conditions (if any), the Eligible Customers are advised to discuss with any of the Bank’s staff, representative or agent. 1 Definition 1.1 For the purpose of these terms and conditions, the following words and expressions shall have the meanings assigned to them except where the context otherwise requires: “AmBank Group” refers to all the Related Corporations and Associate Corporations of the Bank whether incorporated within or outside of Malaysia, existing now or in the future and reference to ‘AmBank Group’ in these terms and conditions herein, shall include all or any entity within AmBank Group. “AmOnline” refers to the internet banking services offered by AmBank Group to its customers to perform banking transactions via the Internet in accordance with the terms and conditions stipulated at http://ambank.amonline.com.my “Bank” refers to both AmBank (M) Berhad (‘AmBank’) [Company No.: 196901000166 (8515-D)] and AmBank Islamic Berhad (‘AmBank Islamic’) [Company No.: 199401009897 (295576-U)], companies incorporated in Malaysia under the Companies Act 1965 (repealed by Companies Act 2016) and having their registered address at Level 22, Bangunan AmBank Group, No. -

Equities Listed Onbursa Malaysia Berhad

EQUITIES LISTED ONBURSA MALAYSIA BERHAD Bursa Malaysia Berhad As at 05 November 2020 International Securities Identification Number (ISIN) Issuer Name (Long) Issuer Name (Short) ISIN Issue Description Listing Date (yr/mth/d) Maturity Date (yr/mth/d) 7-ELEVEN MALAYSIA HOLDINGS BERHAD SEM MYL5250OO005 ORDINARY SHARE 20140530 A50CHIN-C62: CW ISHARES FTSE A50 CHINA ETF (MACQUARIE CAPITAL SECURITIES (MALAYSIA) SDN BHD) A50CHIN-C62 MYJ070362UC4 CALL WARRANT - FOREIGN 20200619 20201231 A50CHIN-C64: CW ISHARES FTSE A50 CHINA ETF (MACQUARIE CAPITAL SECURITIES (MALAYSIA) SDN BHD) A50CHIN-C64 MYJ070364V33 CALL WARRANT - FOREIGN 20200722 20210331 A50CHIN-C66: CW ISHARES FTSE A50 CHINA ETF (MACQUARIE CAPITAL SECURITIES (MALAYSIA) SDN BHD) A50CHIN-C66 MYJ070366V31 CALL WARRANT - FOREIGN 20200903 20210331 A50CHIN-H47: PW ISHARES FTSE A50 CHINA ETF (MACQUARIE CAPITAL SECURITIES (MALAYSIA) SDN BHD) A50CHIN-H47 MYJ070347UC5 PUT WARRANT-FOREIGN 20200619 20201231 A50CHIN-H49: PW ISHARES FTSE A50 CHINA ETF (MACQUARIE CAPITAL SECURITIES (MALAYSIA) SDN BHD) A50CHIN-H49 MYJ070349V33 PUT WARRANT-FOREIGN 20200722 20210331 A50CHIN-H51: PW ISHARES FTSE A50 CHINA ETF (MACQUARIE CAPITAL SECURITIES (MALAYSIA) SDN BHD) A50CHIN-H51 MYJ070351V38 PUT WARRANT-FOREIGN 20200903 20210331 ABF MALAYSIA BOND INDEX FUND ABFMY1 MYL0800EA002 ETF 20050718 ABLEGROUP BERHAD ABLEGRP MYL7086OO001 ORDINARY SHARE 20000327 ABM FUJIYA BERHAD AFUJIYA MYL5198OO006 ORDINARY SHARE 20130723 ABMB-C4: CW ALLIANCE BANK MALAYSIA BERHAD (AMBANK (M) BERHAD) ABMB-C4 MYL2488C4V32 CALL WARRANT - LOCAL -

List of Licensed Financial Institutions in Malaysia

LIST OF LICENSED FINANCIAL INSTITUTIONS IN MALAYSIA A) COMMERCIAL BANKS NO. NAME OF FINANCIAL INSTITUTIONS 1. Affin Bank Berhad 2. Alliance Bank Malaysia Berhad 3. AmBank (M) Berhad 4. BNP Paribas Malaysia Berhad 5. Bangkok Bank Berhad 6. Bank of America Malaysia Berhad 7. Bank of China (Malaysia) Berhad 8. CIMB Bank Berhad 9. China Construction Bank (Malaysia) Berhad 10. Citibank Berhad 11. Deutsche Bank (Malaysia) Berhad 12. HSBC Bank Malaysia Berhad 13. Hong Leong Bank Berhad 14. India International Bank (Malaysia) Berhad 15. Industrial and Commercial Bank of China (Malaysia) Berhad 16. J.P. Morgan Chase Bank Berhad 17. MUFG Bank (Malaysia) Berhad 18. Malayan Banking Berhad 19. Mizuho Bank (Malaysia) Berhad 20. National Bank of Abu Dhabi Malaysia Berhad 21. OCBC Bank (Malaysia) Berhad 22. Public Bank Berhad 23. RHB Bank Berhad 24. Standard Chartered Bank Malaysia Berhad 25. Sumitomo Mitsui Banking Corporation Malaysia Berhad 26. The Bank of Nova Scotia Berhad 27. United Overseas Bank (Malaysia) Bhd. B) ISLAMIC BANKS NO. NAME OF FINANCIAL INSTITUTIONS 1. Affin Islamic Bank Berhad 2. Al Rajhi Banking & Investment Corporation (Malaysia) Berhad 3. Alliance Islamic Bank Berhad 4. AmBank Islamic Berhad 5. Bank Islam Malaysia Berhad 6. Bank Muamalat Malaysia Berhad 7. CIMB Islamic Bank Berhad 8. HSBC Amanah Malaysia Berhad 9. Hong Leong Islamic Bank Berhad 10. Kuwait Finance House (Malaysia) Berhad 11. MBSB Bank Berhad 12. Maybank Islamic Berhad 13. OCBC Al-Amin Bank Berhad 14. Public Islamic Bank Berhad 15. RHB Islamic Bank Berhad 16. Standard Chartered SaadiqBerhad 1 C) INVESTMENT BANKS NO. NAME OF FINANCIAL INSTITUTIONS 1. -

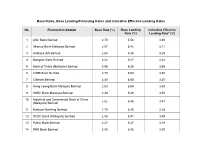

Base Rates, Base Lending/Financing Rates and Indicative Effective Lending Rates

Base Rates, Base Lending/Financing Rates and Indicative Effective Lending Rates No. Financial Institution Base Rate (%) Base Lending Indicative Effective Rate (%) Lending Rate* (%) 1 Affin Bank Berhad 2.70 5.56 3.30 2 Alliance Bank Malaysia Berhad 2.57 5.42 3.11 3 AmBank (M) Berhad 2.60 5.45 3.25 4 Bangkok Bank Berhad 3.22 5.87 4.42 5 Bank of China (Malaysia) Berhad 2.55 5.35 3.55 6 CIMB Bank Berhad 2.75 5.60 3.50 7 Citibank Berhad 2.40 5.55 3.20 8 Hong Leong Bank Malaysia Berhad 2.63 5.64 3.50 9 HSBC Bank Malaysia Berhad 2.39 5.49 3.50 10 Industrial and Commercial Bank of China 2.52 5.45 3.47 (Malaysia) Berhad 11 Malayan Banking Berhad 1.75 5.40 3.25 12 OCBC Bank (Malaysia) Berhad 2.58 5.51 3.45 13 Public Bank Berhad 2.27 5.47 3.10 14 RHB Bank Berhad 2.50 5.45 3.50 No. Financial Institution Base Rate (%) Base Lending Indicative Effective Rate (%) Lending Rate* (%) 15 Standard Chartered Bank Malaysia Berhad 2.27 5.45 3.50 16 United Overseas Bank (Malaysia) Bhd. 2.61 5.57 3.36 No. Islamic Financial Institution Base Rate (%) Base Financing Indicative Effective Rate (%) Lending Rate (%) 1 Affin Islamic Bank Berhad 2.70 5.56 3.30 2 Al Rajhi Banking & Investment Corporation 2.85 5.75 4.20 (Malaysia) Berhad 3 Alliance Islamic Bank Berhad 2.57 5.42 3.11 4 AmBank Islamic Berhad 2.60 5.45 3.25 5 Bank Islam Malaysia Berhad 2.52 5.47 3.25 6 Bank Muamalat Malaysia Berhad 2.56 5.56 3.56 7 CIMB Islamic Bank Berhad 2.75 5.60 3.50 8 Hong Leong Islamic Bank Berhad 2.63 5.64 3.35 9 HSBC Amanah Malaysia Berhad 2.39 5.49 3.50 10 Kuwait Finance House (Malaysia) Berhad 2.25 6.14 3.30 11 Maybank Islamic Berhad 1.75 5.40 3.25 No.