Stock Guide 20 Nov

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Significantly Regulated Organizations Added

Significantly Regulated Organizations Added ‐ September 2017 DUNS COUNTRY BUSINESS NAME TICKER SYMBOL EXCHANGE NAME NUMBER NAME 565406188 BRITISH AMERICAN TOBACCO ZIMBABWE ZIMBABWE BAT.ZW Zimbabwe Stock 565568949 MEDTECH HOLDINGS LTD ZIMBABWE MMDZ.ZW Zimbabwe Stock 565412350 NATIONAL FOODS LTD ZIMBABWE NTFD.ZW Zimbabwe Stock 565679081 STARAFRICA CORPORATION LTD ZIMBABWE SACL.ZW Zimbabwe Stock 555364141 CENTRAL PHARMACEUTICAL JOINT STOCK VIETNAM DP3 Hanoi Stock Exchange CHUONG DUONG BEVERAGE JOINT STOCK Ho Chi Minh Stock 555317798 COMPANY VIETNAM SCD Exchange 555297766 DANAMECO MEDICAL JOINT STOCK VIETNAM DNM Hanoi Stock Exchange DUC GIANG CHEMICALS AND DETERGENT 555345573 POWDER JOINT STOCK COMPANY VIETNAM DGC Hanoi Stock Exchange 555248250 Ha Long Canned Food Joint Stock Co. VIETNAM CAN Hanoi Stock Exchange 555530381 HA NOI INVESTMENT GENERAL VIETNAM SHN Hanoi Stock Exchange 555271543 HA TAY PHARMACEUTICAL JOINT STOCK VIETNAM DHT Hanoi Stock Exchange HOANG ANH GIA LAI JOINT STOCK Ho Chi Minh Stock 555335798 COMPANY VIETNAM HNG Exchange 555319636 HUNG HAU AGRICULTURAL CORPORATION VIETNAM SJ1 Hanoi Stock Exchange 555530218 HUNG VIET GREEN AGRICULTURE JOINT VIETNAM HVA Hanoi Stock Exchange KLF JOINT VENTURE GLOBAL INVESTMENT 555529792 JOINT STOCK COMPANY VIETNAM KLF Hanoi Stock Exchange 555340068 LAM DONG PHARMACEUTICAL JOINT STOCK VIETNAM LDP Hanoi Stock Exchange MECHANICS CONSTRUCTION AND 555303278 FOODSTUFF JOINT STOCK COMPANY VIETNAM MCF Hanoi Stock Exchange Ho Chi Minh Stock 555365190 NAFOODS GROUP JOINT STOCK COMPANY VIETNAM NAF Exchange NORTH PETROVIETNAM FERTILIZER & 555458287 CHEMICALS JOINT STOCK COMPANY VIETNAM PMB Hanoi Stock Exchange Ho Chi Minh Stock 555279715 S.P.M CORPORATION VIETNAM SPM Exchange SAIGON BEER ALCOHOL BEVERAGE Ho Chi Minh Stock 555254439 CORPORATION VIETNAM SAB Exchange 555341953 SAM CUONG ELECTRIC MATERIALS JS CO. -

THE NEGLECTED RISK Why Deforestation Risk Should Matter to Chinese Financial Institutions

DISCLOSURE INSIGHT ACTION THE NEGLECTED RISK Why deforestation risk should matter to Chinese financial institutions May 2019 CONTENTS 5 Key Findings 39 Asset owners and asset managers 6 Executive Summary 40 Chapter 4. Conclusions and recommendations 8 Chapter 1. Introduction 41 Conclusions 9 Global trends in ESG investment 42 Recommendations 10 An overlooked investment risk 45 Appendix I 12 Why should financial institutions address Research scope and methodology deforestation in their value chains? 45 Research scope 15 Chapter 2. Key findings 45 Company selection methodology 16 The current state of financial institutions’ environment management 46 Financial flow analysis methodology 18 The current state of corporates’ deforestation risk management 48 Methodology of estimating soy-related capital across sector 24 Financial institutions active in the soy sector 50 Research limitations 28 Institutional Investors 51 Appendix II Bond and share underwriters 30 Distribution of capital and exposure to deforestation risks across sectors 52 Appendix III Top 20 investors 32 Chapter 3. International policies, initiatives and good practice 53 Appendix IV Qualitative relationships 33 International policies and initiatives 54 Appendix V 34 Banks CDP responses 38 Institutional Investors Important Notice The contents of this report may be used by anyone providing acknowledgment is given to CDP Worldwide (CDP). This does not represent a license to repackage or resell any of the data reported to CDP or the contributing authors and presented in this report. If you intend to repackage or resell any of the contents of this report, you need to obtain express permission from CDP before doing so. CDP has prepared the data and analysis in this report based on responses to the CDP information request. -

China Food & Beverage Monthly

China / Hong Kong Monthly Chart Book China Food & Beverage Monthly Refer to important disclosures at the end of this report Page 1 DBS Group Research . Equity 11 Jan 2017 Diverging material trends Soft grain prices to keep feedstock costs low HSI: 22,745 Dairy prices could rise, but pork prices should retreat ANALYST Potential pressure from sugar and PET prices on beverage players Alice HUI, CFA +852 2971 1960 Grain prices remain favourable. Despite prior concerns on [email protected] impact from La Nina in 2016, production volume for grains (corn, Alison Fok +852 2971 1938 soybean) remained robust. According to USDA, global corn [email protected] production is expected to rise in FY17F. This, coupled with the cessation of the Chinese government’s corn reserve purchasing Mavis HUI+852 2863 8879; system since late 2016, would likely continue to put pressure on [email protected] corn prices. Corn prices in China have fallen by another 4.4% Eric YEE, CFA +86 21 6888 3360 m-o-m in January 2017, after dropping some 24% in 2016. As [email protected] corn makes up a large portion of meat and dairy upstream players’ raw material costs (est. 60-70% of total), lower corn F&B peer table prices should bode well for their margins. Meanwhile, prices of other grains such as soybean will also likely see limited upside as Price Target Upside Rec Mkt FY17 a result of a change in acreage planting in China (a shift from HK$ Price % Cap PE (x) lower-margin corn to other grains with better margins), as well HK$ (US$m) as stable global production volume growth, according to USDA. -

An Assessment of Environmental and Social Transparency of Food Related Companies Currently Listing in Hong Kong Stock Exchange

An assessment of Environmental and Social transparency of food related companies currently listing in Hong Kong Stock Exchange October 2017 Hong Kong 1 Executive Summary Oxfam Hong Kong seeks to better understand opportunities to engage with companies in Hong Kong. Oxfam Hong Kong commissioned CSR Asia to conduct a benchmarking exercise to assess the Environmental and Social transparency in the food, beverages, and agricultural products sectors in Hong Kong. The aims of this exercise were: To assess food companies’ Environment and Social transparency To summarise the Environment and Social transparency of selected companies. To assess what companies are doing to create more inclusive business models relating to both products and value chains, and to engage with issues associated with access to food products for poor people. To make recommendations on the business case for food companies to implement responsible business policies In total, 61 companies were benchmarked in this study. Data was compiled from publicly available information published in 2015 including corporate websites, annual reports and sustainability reports. Overall, the level of disclosure by the 61 companies is relatively low and indeed they were failed. Only 3 companies achieved over 30 points and 55 of the companies scoring below 20 points. This may seem disappointing at first but it should be recognized that the GRI indicators are very comprehensive and that most companies in Hong Kong are a long way from being able to report on them. Companies demonstrated weak performance in both categories in which the average score of social and environment are 12.5 and 8.7 respectively. -

China Consumer Staples

Deutsche Bank Markets Research Industry Date 14 November 2014 China Consumer Asia Staples Hong Kong Consumer Winnie Mak Research Analyst (+852) 2203 6178 [email protected] F.I.T.T. for investors The discretionary side of staples From 'needs' to 'wants' Noodles and drinks can be fashionable if consumers want it that way. Chinese consumers have had most of what they need, so we look into the discretionary side of consumer staples, i.e., what and how they want the beer and tea to be served. We think something new and/or chilled will help companies to put a stop on de-rating in 2015, and to prepare for the recovery ahead. ________________________________________________________________________________________________________________ Deutsche Bank AG/Hong Kong Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 148/04/2014. Deutsche Bank Markets Research Asia Industry Date Hong Kong 14 November 2014 Consumer China Consumer FITT Research Staples Winnie Mak Research Analyst The discretionary side of staples (+852) 2203 6178 [email protected] From 'needs' to 'wants' Companies Featured Noodles and drinks can be fashionable if consumers want it that way. Chinese consumers have had most of what they need, so we look into the discretionary Hengan Intl. (1044.HK),HKD82.00 Buy side of consumer staples, i.e., what and how they want the beer and tea to be 2013A 2014E 2015E served. -

Feeding Asia

ISSUES FOR RESPONSIBLE INVESTORS FEEDING ASIA APR 2011 Editors Benjamin McCarron Lucy Carmody Laura Dodge Researchers Gauri Nafrey Allison Prevatt COMMISSIONED BY Responsible Research is an independent provider of sectoral and thematic Asian environment, Responsible Research is the exclusive partner in Asia for RepRisk®, a web-based tool which social and governance (ESG) research, targeted at global institutional investors. Many of provides insights on environmental and social issues that present financial and reputational these fund managers and asset owners now find that traditional investment banking reports, risks to companies and investment portfolios. The tool enables commercial and investment financial models and public information sources can no longer be relied on to cover all risks bankers, asset managers, and supply chain managers to manage the corresponding risks and to earnings and deliver superior returns. Companies who do not monitor and report on this to implement effective screening procedures. ‘non-financial’ performance not only risk financial penalties for non-compliance with stricter regulatory environments but are also denied access to substantial pools of global capital which About the RepRisk® tool are managed according to sustainable principles. RepRisk® is a web-based tool that allows you to Our approach is based on analysis of material ESG factors, which change according to sector identify and assess the environmental and social and market. We provide our clients with local market knowledge of important regulatory issues which may present financial, reputational landscapes in Asia, along with a fresh perspective on local operational and sectoral issues. and ethical risks. It is used by investment We offer an annual subscription model for our monthly sectoral or thematic reports and give professionals, financial institutions, supply our clients access to the underlying data. -

Registration Period for Asia-Pacific & China Companies for the 2012 IR

Registration period for Asia-Pacific & China Companies for the 2012 IR Global Rankings Already Started! NEW YORK, June 11, 2012 /PRNewswire via COMTEX/ -- IR Global Rankings ("IRGR"), the most comprehensive technical ranking system for investor relations websites, corporate governance practices and financial disclosure procedures, is pleased to announce that the registration period for Asia-Pacific & China companies for the IR Global Rankings starts tomorrow, June 12, 2012, and will last until July 13, 2012. The 2011 IRGR, supported by of Arnold & Porter, KPMG, MZ and Sodali is a unique and independent external review of any company's communication process with the capital markets. TO REGISTER please click here or visit the website www.irglobalrankings.com . TOP 5 REASONS TO JOIN 1) Unique Ranking System: IRGR is the sole investor relations ranking system based on technical reviews (not opinion surveys or polls) and is supported by the input of audit and legal experts. IRGR is a unique way to have an external review and positioning of your investor relations and financial communications efforts among best practices among leading companies worldwide. 2) Individual Feedback: Participants that choose to acquire the individual feedback report will receive detailed suggestions for improvements where applicable. This report can be later discussed in a private conference call with the IRGR staff, upon request by the participating company. 3) Solid Benchmarking: By registering for IRGR, your company will be ranked among companies worldwide in all industries. Our extensive client base allows us to identify, rank and disclose the best IR communication programs in the world. Only positive examples are publicly disclosed. -

Download the 2010 IRGR Magazine, with the Winners and Best Practices, Please Go To

IR Global Rankings 2011 Best Ranked Companies in North America NEW YORK, Feb. 7, 2011 /PRNewswire/ - IR Global Rankings ("IRGR"), the most comprehensive technical ranking system for investor relations websites, corporate governance practices and financial disclosure procedures, jointly with its coordination group and supporting entities, Arnold & Porter, MZ, KPMG and Sodali, announced today at The IR Summit, an IR conference produced in association with Institutional Investor, the 2011 Best Ranked Companies in North America, as follows: Best Ranked IR Websites in North America: Life Technologies,PotashCorp,Intel, Cameco and Microsoft. Best Ranked Online Annual Report in North America: Nexen. Best Ranked Financial Disclosure Procedures in North America: URS Corporation, Fedex Corp., Ryder System, Cameco and BMO Financial Group. Best Ranked Corporate Governance Practices in North America: Nexen. We congratulate all the investor relations teams of the best ranked companies for their achievements and efforts. The Top 30 global results, as well as the industry results, will be available on our website http://www.irglobalrankings.com/ in December 2011. To learn more about the 2011 IRGR or download the 2010 IRGR magazine, with the winners and best practices, please go to: http://www.irglobalrankings.com/. More than 60 North American companies have registered for the 2011 IR Global Rankings, among them (in alphabetical order):AAAAmerican (LUX: AAA); Advent Software (NASDAQ: ADVS); Agnico-Eagle Mines (TSX, NYSE: AEM); Akamai Technologies (Nasdaq: AKAM); Alternet Systems (OTCBB: ALYI); Applied Materials, Inc. (NASDAQ: AMAT); Assurant (New York Stock Exchange: AIZ); AT&T (NYSE: T); AXA Equitable (CAC: CS FP); BAXTER (NYSE: BAX); Beckman Coulter, Inc. -

Updated April 2009

® ™ LexisNexis SmartIndexing Technology New Company Terms Updated April 2009 A-B........................................................................................................................1 C ...........................................................................................................................2 D-E........................................................................................................................4 F-G........................................................................................................................4 H-I.........................................................................................................................4 J-K ........................................................................................................................5 L-M........................................................................................................................5 N-O .......................................................................................................................6 P-Q-R....................................................................................................................7 S ...........................................................................................................................8 T-U........................................................................................................................9 V-W.......................................................................................................................9 -

China Modern Dairy Holdings Ltd. 中國現代牧業控股有限公司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 1117)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. China Modern Dairy Holdings Ltd. 中國現代牧業控股有限公司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 1117) APPOINTMENT OF DIRECTORS RESIGNATION OF INDEPENDENT NON-EXECUTIVE DIRECTOR AND CHANGE TO THE COMPOSITION OF THE AUDIT COMMITTEE, THE RENUMERATION COMMITTEE AND THE NOMINATION COMMITTEE APPOINTMENT OF CHAIRMAN The Board is pleased to announce that both Mr. Yu Xubo and Mr. Ding Sheng have been appointed as non-executive Directors, Mr. Liu Fuchun and Mr. Kang Yan have been appointed as independent non-executive Directors and Mr. Sun Yugang has been appointed as an executive Director, all of which are with effect from 28 June 2013. The Board further announces that Mr. Guo Lianheng tendered to the Board his resignation as an independent non-executive Director, a member of the Audit Committee, a member of the Remuneration Committee, and the chairman of the Nomination Committee of the Company on 28 June 2013. Mr. Guo’s resignation was considered and approved at the meeting of the Board on 28 June 2013 with immediate effect. The Board further announces that with effect from 28 June 2013, Mr. Yu Xubo, a non-executive Director, has been appointed as the Chairman of the Board in place of Mr. -

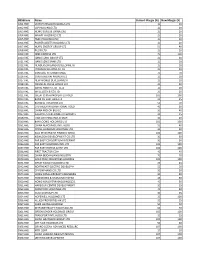

Copy of Default Margin List

IRESSCode Name Current Margin (%) New Margin (%) 0001.HKE CK HUTCHISON HOLDINGS LTD 10 10 0002.HKE CLP HOLDINGS LTD 10 10 0003.HKE HONG KONG & CHINA GAS 20 20 0004.HKE WHARF HOLDINGS LTD 20 20 0005.HKE HSBC HOLDINGS PLC 10 10 0006.HKE POWER ASSETS HOLDINGS LTD 10 10 0007.HKE HOIFU ENERGY GROUP LTD 50 40 0008.HKE PCCW LTD 20 20 0009.HKE NINE EXPRESS LTD 70 100 0010.HKE HANG LUNG GROUP LTD 20 20 0011.HKE HANG SENG BANK LTD 10 10 0012.HKE HENDERSON LAND DEVELOPMENT 10 10 0014.HKE HYSAN DEVELOPMENT CO 20 20 0015.HKE VANTAGE INTERNATIONAL 70 70 0016.HKE SUN HUNG KAI PROPERTIES 10 10 0017.HKE NEW WORLD DEVELOPMENT 10 10 0018.HKE ORIENTAL PRESS GROUP LTD 40 30 0019.HKE SWIRE PACIFIC LTD - CL A 10 10 0020.HKE WHEELOCK & CO LTD 20 20 0021.HKE GREAT CHINA PROPERTIES HOLDI 100 100 0023.HKE BANK OF EAST ASIA LTD 20 25 0024.HKE BURWILL HOLDINGS LTD 50 50 0025.HKE CHEVALIER INTERNATIONAL HOLD 40 30 0026.HKE CHINA MOTOR BUS CO 30 40 0027.HKE GALAXY ENTERTAINMENT GROUP L 20 15 0028.HKE TIAN AN CHINA INVESTMENT 30 20 0030.HKE BAN LOONG HOLDINGS LTD 100 100 0031.HKE CHINA AEROSPACE INTL HLDG 50 40 0032.HKE CROSS-HARBOUR HOLDINGS LTD 30 30 0033.HKE ASIA INVESTMENT FINANCE GROU 100 100 0034.HKE KOWLOON DEVELOPMENT CO LTD 30 30 0035.HKE FAR EAST CONSORTIUM INTERNAT 30 30 0036.HKE FAR EAST HOLDINGS INTL LTD 100 100 0037.HKE FAR EAST HOTELS & ENT LTD 100 100 0038.HKE FIRST TRACTOR CO-H 40 40 0039.HKE CHINA BEIDAHUANG INDUSTRY 70 70 0040.HKE GOLD PEAK INDUSTRIES HOLDING 100 100 0041.HKE GREAT EAGLE HOLDINGS LTD 25 25 0042.HKE NORTHEAST ELECTRIC DEVELOP-H 50 50 0043.HKE CP POKPHAND CO LTD 30 30 0044.HKE HONG KONG AIRCRAFT ENGINEERG 30 30 0045.HKE HONGKONG & SHANGHAI HOTELS 25 30 0050.HKE HONG KONG FERRY(HOLDINGS)CO. -

An Assessment of the Environmental and Social Transparency of Food Companies Currently Listed in the Hong Kong Stock Exchange

An assessment of the environmental and social transparency of food companies currently listed in the Hong Kong Stock Exchange Oct 2017 1. Foreword Oxfam, as an international poverty alleviation organisation, has been working to realise the United Nations Sustainable Development Goals (SDGs), particularly SDG 1 and 10: to end poverty, and tackle inequality and injustice. Oxfam believes that a just society should move towards a human economy. In other words, profit should not be the only goal; instead, the needs of people should be a priority in economic development. To build a just society, the basic needs of the underprivileged should be taken into account. Among the UN’s 17 SDGs1, Oxfam believes that by ending poverty (SDG 1), achieving gender equality (SDG 5), ensuring decent work and economic growth (SDG 8), and reducing inequality (SDG 10), the disparity between the rich and poor would be lessened, and our society would be better off and be more equal. To ensure people living in poverty can benefit from economic development, Oxfam has been promoting the integration of ‘Environmental, Social, and Governance’ (ESG) into corporate policies and business operations since 2004. Oxfam conducted three pioneering studies in 2008, 2009 and 2016 to study the corporate social responsibility (CSR) performance of the Hang Seng Index (HSI) constituents by looking at the implementation of their CSR initiatives. Oxfam hopes to influence companies to adopt international standards to formulate or improve their CSR policies ‒ especially in terms of committing to or reporting on areas such as the labour and supply chain, human rights, equal employment opportunities and the environment ‒ and set pro-poor policies.