Metro Vancouver, BC Office Market Report (Year-End 2019)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1503 Kingsway Vancouver, BC

FOR SALE > 1.5 ACRE MIXED-USE DEVELOPMENT OPPORTUNITY 1503 Kingsway VANCOUVER, BC KINGSWAY KNIGHT STREET KNIGHT KING EDWARD VILLAGE Development Highlights > Mixed-use development site with rezoning potential > Substantial frontages along Kingsway (223 ft) and Dumfries Street (352 ft) providing outstanding exposure, accessibility and large lot size (66,318 square feet) > Potential for phenomenal views overlooking Downtown and the North Shore Mountains > Centrally located, making the area attractive to residents and businesses alike (12 minutes to Downtown Vancouver) > Community and municipal support for development in the area is demonstrated by the multitude of recent developments along Kingsway > Holding income that will alleviate time pressure SIMON LIM* SHELDON SCOTT* RANDY HEED* OLIVER OMI Executive Vice President Senior Vice President Senior Vice President Associate 604 661 0882 604 662 2660 604 661 0831 604 692 1465 [email protected] [email protected] [email protected] [email protected] 1503 Kingsway, Vancouver, BC Legal Address: That Part of Block 6 Lying to the West of the West Boundary of Plan 1257, Except Portions in Reference Plans 610, 2394 and 4580, District Lot 352 Plan 219 PID: 004-718-461 LOT 1, Except Part in Reference Plan 2394, of Lots 1 to 3 Block 6 District Lot 352 Plan 2497 PID: 004-719-247 Location: The Property occupies the northeast corner of Kingsway and Dumfries Street - located along one of the busiest arterials in Metro Vancouver. Site Area: The site is 66,318 SF with approximately 223 feet of frontage along Kingsway and 352 feet of frontage on Dumfries Street. -

7919-0048-00 to Permit the Development of a Mixed-Use High-Ris

City of Surrey PLANNING & DEVELOPMENT REPORT Application No.: 7919-0048-00 Planning Report Date: June 15, 2020 PROPOSAL: • OCP Amendment of Figure 16: Central Business District Densities from "3.5 FAR" to "7.5 FAR" • City Centre Plan Amendment from "Mixed Use 3.5 FAR" to "Mixed Use 7.5 FAR" • Rezoning from C-8, C-15 and CHI to CD • Development Permit to permit the development of a mixed-use high-rise building. LOCATION: 10732 - 135A Street 10731 - King George Boulevard 10751 - King George Boulevard ZONING: C-8, C-15 and CHI OCP DESIGNATION: Town Centre CITY CENTRE PLAN Mixed Use 3.5 FAR DESIGNATION: Staff Report to Council Planning & Development Report Application No.: 7919-0048-00 Page 2 RECOMMENDATION SUMMARY • By-law Introduction and set date for Public Hearing for: • OCP Amendment; and • Rezoning. • Approval to draft Development Permit for Form and Character. DEVIATION FROM PLANS, POLICIES OR REGULATIONS • Proposing an amendment to the Official Community Plan (Figure 16) to permit a higher density for the site. • Proposing an amendment to the City Centre Plan from Mixed Use 3.5 FAR to Mixed-Use 7.5 FAR. RATIONALE OF RECOMMENDATION • The proposed density and building form are appropriate for this part of Surrey City Centre, and forms part of an emerging high-density mixed-use hub that will be complementary to the City of Surrey Civic Centre to the south. • The proposed development conforms to the goal of achieving high-rise, high density, and mixed-use development around the three City Centre SkyTrain Stations. The Gateway SkyTrain Station is located within a walking distance of 400 metres of the subject site. -

Monthly BL Report

CITY OF NORTH VANCOUVER BUSINESS LICENCES ISSUED (Non-Resident) BUSINESS NAME CNV ADDRESS TEL. NO. DESCRIPTION IPS CODE EATON'S HEATING LTD 2466 FRISKIE AVEPORT COQUITLAM BC V3B 7P9 (604)535-8434 Gas Contractor 2383 PARAGON REMEDIATION GROUP LTD 8815 HARVIE RDSURREY BC V4N 4B9 (604)513-1324 Hazardous Materials Abatement 5621 (EASI) ENTRANCE AUTOMATION SYSTEMS 1 - 13015 84TH AVESURREY BC V3W 1B3 6045945127 Installation and Service of Pedestrian Automatic 2389 Doors 07048237 BC LTD 20363 62ND AVE LANGLEY BC V3A 5E6 (604)534-5555 HVAC/Gas Contractor 2383 0880441 BC LTD O/A EVENTPOWER 104-8838 HEATHER STVANCOUVER BC V6P 3S8 (604)524-1967 Electrical Contractor : Temporary Power for Events 2382 0986001 BC LTD 8563 GOVERNMENT STBURNABY BC V3N 4S9 (604)688-3157 Athletic Instructor - Sports Programs for Children 6116 0987762 BC LTD 338-3381 CAMBIE STVANCOUVER BC V5Z 4R3 (604)561-3366 Demolition & Excavating 2389 1024753 BC LTD 15075 59 AVESURREY BC V3S 3T2 (604)771-9703 Contractor 2361 1025689 BC LTD 108 - 8331 EASTLAKE DRIVEBURNABY BC V5A (604)444-2242 Contractor - Painting 2389 4W2 1049936 BC LTD 260 E 4TH AVEVANCOUVER BC V5T 1G5 (604)628-8752 Low Voltage Contractor 2382 1103735 BC LTD 5337 ST CATHERINES STVANCOUVER, BC V5W (250)886-6002 Electrical Contractor 2382 3G2 11466884 BC LTD 14485 88A AVENUESURREY BC V3R 1A2 (604)782-1971 Building Contractor- Framing 2389 1243035 BC LTD 208-3900 HASTINGS STBURNABY BC V5C 6C1 (403)880-9939 NEW HOME BUILDER- RESIDENTIAL 2361 1339022 ONTARIO LTD 75 INDUSTRIAL RDTOTTENHAM ON L0G 1W0 (905)936-5888 Sign -

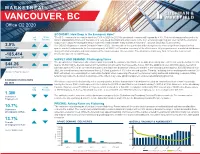

MARKET NAME Office QX 20XX

M A R K E T B E AT VANCOUVER, BC Office Q2 2020 ECONOMY: How Deep is the Economic Hole? YoY 12-Mo. "The B.C. economy is forecast to shrink by 7.8% in 2020. In 2021 the provincial economy will expand by 4.8%. This is a strong growth number by Chg Forecast historic standards but comes in the wake of a very steep downturn and only results in the B.C. economy regaining just over half of the economic output lost in 2020. Restoring the labour market to health will take many months if not years”. (Source: Business Council of BC). 3.9% The COVID-19 pandemic struck Canada in March 2020. This was late in the quarter but with enough time to have a significant impact on first Vacancy Rate quarter market fundamentals. In the second quarter of 2020, the Canadian economy felt its effects more fully as government mandated shutdowns along with shelter-in-place ordinances pushed the country deeper into recession. The situation remains very fluid. Access the most recent -185,414 information specific to COVID here. Net Absorption,SF SUPPLY AND DEMAND: Challenging Times The pre-pandemic Vancouver office market was strong and the vacancy rate had been steadily decreasing since 2015. It is very likely that the first $44.26 quarter of 2020 will be the last quarter with record low vacancies for the foreseeable future. With the addition of over 400,000 square feet (sf) of Asking Rent, PSF sublease space (45% of all current vacant space) arriving in the downtown Vancouver market in the second quarter (approx. -

BC's $25 Billion Opportunity a Transformation Agenda

BC's $25 Billion Opportunity A Transformation Agenda UPDATED MARCH 2020 2 BC TECH Policy Recommendations 11 Key Policy Recommendations SCALE TALENT OUTCOME: OUTCOME: ScaleUp BC's Tech Companies and increase Increase the tech talent pool to fulfill BC’s Technology Adoption in every industry. enormous economic growth potential. RECOMMENDATIONS RECOMMENDATIONS 1. 1. Partner with the federal government to Fund an additional 2,000 tech-relevant public invest a total of $50M over 5 years in ScaleUp post-secondary graduates to meet industry BC, a partnership to drive economic growth demand. and competitiveness across BC. 2. 2. Make the federal Global Talent Stream (GTS) per- Create a BC Transformation Fund of $1B over ten manent and extend the up-front BC foreign buyers’ years to accelerate BC's transition to the economy housing tax exemption to GTS nominees to ensure of the future. fairness. Extend the BC Provincial Nominee Program (PNP) Tech Pilot and increase the allocation of PNP 3. places for BC to unlock additional talent supply. Strengthen and extend DataBC’s mandate to stra- tegically manage BC’s public data to accelerate plat- 3. form growth and improve access to data. Establish a labour credit of 10% of the starting salary of a returning Canadian worker (resident for 3 years) re- 4. fundable against the payroll tax liabilities of BC-head- Update refundable SR&ED and Industrial Research quartered tech companies to bring Canadians working Assistance Program (IRAP) ceiling and employee lim- abroad home. its to increase these programs' scaling power. 4. 5. Double the New Ventures BC Innovator Skills Initiative Introduce a superdeduction for 150% of qualifying co-op places, increase the program employee cap from tech commercialization costs for BC-headquartered 100 to 300, and expand the program to include workers tech companies to promote market success and transitioning to tech to increase work-integrated learn- scale-up. -

Strategy Games Big Huge Games • Bruce C

04 3677_CH03 6/3/03 12:30 PM Page 67 Chapter 3 THE EXPERTS • Sid Meier, Firaxis General Game Design: • Bill Roper, Blizzard North • Brian Reynolds, Strategy Games Big Huge Games • Bruce C. Shelley, Ensemble Studios • Peter Molyneux, Do you like to use some brains along with (or instead of) brawn Lionhead Studios when gaming? This chapter is for you—how to create breathtaking • Alex Garden, strategy games. And do we have a roundtable of celebrities for you! Relic Entertainment Sid Meier, Firaxis • Louis Castle, There’s a very good reason why Sid Meier is one of the most Electronic Arts/ accomplished and respected game designers in the business. He Westwood Studios pioneered the industry with a number of unprecedented instant • Chris Sawyer, Freelance classics, such as the very first combat flight simulator, F-15 Strike Eagle; then Pirates, Railroad Tycoon, and of course, a game often • Rick Goodman, voted the number one game of all time, Civilization. Meier has con- Stainless Steel Studios tributed to a number of chapters in this book, but here he offers a • Phil Steinmeyer, few words on game inspiration. PopTop Software “Find something you as a designer are excited about,” begins • Ed Del Castillo, Meier. “If not, it will likely show through your work.” Meier also Liquid Entertainment reminds designers that this is a project that they’ll be working on for about two years, and designers have to ask themselves whether this is something they want to work on every day for that length of time. From a practical point of view, Meier says, “You probably don’t want to get into a genre that’s overly exhausted.” For me, working on SimGolf is a fine example, and Gettysburg is another—something I’ve been fascinated with all my life, and it wasn’t mainstream, but was a lot of fun to write—a fun game to put together. -

The Fastest 50 the Vancouver Sun Wed 31 Oct 2007 Page: F2 Section: Special Section Source: Vancouver Sun

The Fastest 50 The Vancouver Sun Wed 31 Oct 2007 Page: F2 Section: Special Section Source: Vancouver Sun British Columbia's fastest-growing publicly traded companies These lists detail two pillars of B.C.'s economy: Those companies with the fastest growth and those companies with the strongest fundamentals, hence the Fastest 50 and the Strongest 50 combine to form The Vancouver Sun's Top 100. The Fastest list is all about balanced growth, not just success in one category of financial performance. Where other ranking efforts look solely at revenue change, BusinessBC's sophisticated analysis is based on formulas developed by James Brander of the Sauder School of Business at the University of British Columbia. It takes into account employee growth, revenues, stock performance, and earnings. The Strongest 50 concentrates on total assets, market capitalization and how the company performs based on those fundamentals (more below.) Twenty-five companies, such as Teck Cominco, have both strong fundamentals and continue to grow, so they qualify for both lists. BusinessBC's other project partner, Ernst & Young LLP, began by looking at all publicly-traded companies with headquarters in B.C. and/or a significant proportion of business activities located in the province. Most but not all companies are traded on the Toronto Stock Exchange or the TSX Venture Exchange. Detailed financial information was drawn from annual reports and other sources. Employee numbers were volunteered by the companies and compiled by staff at The Vancouver Sun. Some 500 to 600 corporations were reviewed to arrive at this selection. James Brander's formula was applied to Ernst & Young's findings and the result was further refined to ensure that companies with balanced growth across the categories received due recognition. -

Debates of the House of Commons

43rd PARLIAMENT, 2nd SESSION House of Commons Debates Official Report (Hansard) Volume 150 No. 086 Thursday, April 22, 2021 Speaker: The Honourable Anthony Rota CONTENTS (Table of Contents appears at back of this issue.) 5997 HOUSE OF COMMONS Thursday, April 22, 2021 The House met at 10 a.m. government's position on it, diplomatic representations it has made with respect to that issue, as well as the government's intention with respect to raising the genocide investigation specifically. Prayer The response that was tabled to that question makes no mention of any genocide investigation. In fact, it does not address the ques‐ tion at all. It refers broadly to Sri Lanka, but it makes no mention of ROUTINE PROCEEDINGS the substance of the question. I know that it is practice for the Speaker not to be asked to evalu‐ ● (1005) ate the particulars of the quality of the response. However, in this [English] case, given that the alleged response does not in any way acknowl‐ COMMISSIONER OF THE ENVIRONMENT AND edge or respond to the question, I would submit that this makes a SUSTAINABLE DEVELOPMENT total mockery of the expectation in the Standing Orders for the gov‐ The Speaker: It is my duty to lay upon the table, pursuant to ernment to table a response. subsection 23(5) of the Auditor General Act, the spring 2021 re‐ There have to be some constraints on the response the govern‐ ports of the Commissioner of the Environment and Sustainable De‐ ment presents. After all, if the government were to present a re‐ velopment to the House of Commons. -

KING GEORGE BOULEVARD 10070 SURREY, BC Partnership

FOR LEASE KING GEORGE BOULEVARD 10070 SURREY, BC Partnership. Performance. OFFICE SPACE FOR LEASE Opportunity to lease in the heart of central Surrey with direct exposure along King George Boulevard. Josh Sookero*, Principal Nicolas Bilodeau, Senior Associate 604.647.5091 604.647.1336 [email protected] [email protected] * Personal Real Estate Corporation Jordan Gill, Associate 604.647.5097 [email protected] KING GEORGE BLVD BARNET HWY E HASTINGS ST RENFREW ST HASTINGS ST SURREY, BC ST JOHNS ST 10070 W 4 AVE CLARKE RD W BROADWAY KINGSWAY NANAIMO ST E BROADWAY W 16 AVE RUPERT ST GAGLARDI WAY SW MARINE DR W KING EDWARD AVE KNIGHT ST LOUGHEED HWY W 41 AVE W 41 AVE KINGSWAY W 49 AVE KNIGHT ST Subject Property GROSVENOR RD BRIDGEPORT RD 10070 King George Blvd104 AVE KING GEORGE BLVD 104 AVE 120 ST 152 ST 156 ST GOLDEN EARS WAY 96 AVE 96 AVE 96 AVE 96 AVE 208 ST SOUTH FRASER PERIMETER ROAD 200 ST WESTMINSTER HWY WESTMINSTER HWY FRASER HIGHWAY 88 AVE 88 AVE 88 AVE 88 AVE TRANS-CANADA HIGHWAY 88 AVE 200 ST 168 ST BLUNDELL RD NORDEL WAY 156 ST TRANS-CANADA HIGHWAY SCOTT ROAD SCOTT 128 ST 132 ST 140 ST 144 ST HARVIE RD NO 1 RD NO 2 RD NO 3 RD NO 4 RD NO 6 RD TRANS-CANADA HIGHWAY 208 ST 152 ST 184 ST RIVER RD KING GEORGE BLVD FRASER HIGHWAY STEVESTON HWY 72 AVE 72 AVE 72 AVE 264 ST 168 ST 200 ST 64 AVE 64 AVE 64 AVE 64 AVE 64 AVE 184 ST 128 ST 132 ST 120 ST 144 ST 104 ST 232 ST 216 ST 56 AVE LANGLEY BYPASS 56 AVE 152 ST 248 ST TRANS-CANADA HIGHWAY FRASER HIGHWAY LADNER TRUNK RD 200 ST 208 ST 168 ST 184 ST 216 ST 192 ST Location ARTHUR DR 152 ST th nd TRANS-CANADA HIGHWAY 232 ST Town Square is located mid-block between 100 Avenue and 102 Avenue on 36 AVE 224 ST 240 ST 248 ST DELTAPORT WAY 32 AVE 32 AVE 144 ST FRASER HIGHWAY 216 ST the east side of King George Boulevard in central Surrey. -

Expiring Contracts January 1, 2021 — December 31, 2021 Contract Company Union Expiry

Volume 53, Issue 1, Feb/Mar 2021 EXPIRING CONTRACTS JANUARY 1, 2021 — DECEMBER 31, 2021 CONTRACT COMPANY UNION EXPIRY PRIVATE SECTOR United Food & Commercial Workers Rossdown Farms and Natural Foods 2021-01-24 Union AJ Forsyth (Russell Metals) United Steelworkers 2021-01-31 Coast Coal Harbour Hotel Unifor 2021-01-31 Ideal Gear and Machine Works United Steelworkers 2021-01-31 Mitchell Press Unifor (MediaUnion) 2021-01-31 Ringball Corporation and Vanguard United Steelworkers 2021-01-31 Steel Ltd. British Columbia Government & Servomation/Centerplate Inc. 2021-01-31 Service Employees' Union The Hudson's Bay Company United Steelworkers 2021-01-31 British Columbia Government & Union Bay Credit Union 2021-01-31 Service Employees' Union British Columbia Government & Canadian Diabetes Association 2021-02-17 Service Employees' Union British Columbia Government & Freshwater Fisheries Society 2021-02-17 Service Employees' Union Marine Workers and Boilermakers Allied Shipbuilders Limited Industrial Union Local 1, Pipe Fitters 2021-02-28 UA, Local 170, IBEW Local 213 Interior Savings Credit Union British Columbia Government & 2021-02-28 (Thompson) Service Employees' Union International Union of Operating Lafarge Asphalt Technologies 2021-02-28 Engineers International Brotherhood of Seaspan Victoria Shipyards Co Ltd. 2021-02-28 Boilermakers Sprott Shaw Language (formerly KGIC Education and Training Employees' 2021-02-28 Language College) Association Cascade Aerospace Unifor 2021-03-30 IATSE 891, Teamsters 155, BC and Yukon Council of Film Unions International -

The State of Broadband 2019 Broadband As a Foundation for Sustainable Development

International The State of Broadband: Telecommunication Union Broadband as a Foundation Place des Nations CH-1211 Geneva 20 Switzerland for Sustainable Development September 2019 ISBN 978-92-61-28971-3 9 7 8 9 2 6 1 2 8 9 7 1 3 Published in Switzerland broadbandcommission.org Geneva, 2019 THE STATE OF BROADBAND 2019 Broadband as a Foundation for Sustainable Development ITU/UNESCO Broadband Commission for Sustainable Development © International Telecommunication Union and United Nations Educational, Scientific and Cultural Organization, 2019 Some rights reserved. This work is available under the Creative Commons Attribution-NonCommercial- ShareAlike 3.0 IGO licence (CC BY-NC-SA 3.0 IGO; https:// creativecommons .org/ licenses/by -nc -sa/ 3 .0/ igo).). Under the terms of this licence, you may copy, redistribute and adapt the work for non-commercial purposes, provided the work is appropriately cited, as indicated below. In any use of this work, there should be no suggestion that ITU or UNESCO endorses any specific organization, products or services. The unauthorized use of the ITU or UNESCO names or logos is not permitted. If you adapt the work, then you must license your work under the same or equivalent Creative Commons licence. If you create a translation of this work, you should add the following disclaimer along with the suggested citation: “This translation was not created by the International Telecommunication Union (ITU) or the United Nations Educational, Scientific and Cultural Organization (UNESCO). Neither ITU nor UNESCO are responsible for the content or accuracy of this translation. The original English edition shall be the binding and authentic edition”. -

843 Granville Street Vancouver, BC

FOR SALE 843 GRANVILLE STREET VANCOUVER, BC Contact Us ROBERT DOWN MATT SAUNDERS ASSOCIATE ASSOCIATE VICE PRESIDENT +1 604 692 1486 +1 604 661 0802 [email protected] [email protected] FORR SALE SALE > 843> 843 GR ANVILLEGRANVILLE STREET STREET Opportunity 1A Site Description 843 Granville Street presents the rare opportunity to acquire The subject parcel is approximately 3,000 SF (25’ x 120’) and a 100% freehold interest in a retail property on the desirable is rectangular in shape. The property has 25 feet of frontage 800 block of Granville Street, with short term re-positioning along the west side of Granville Street and is also accessible potential. by way of the rear lane. Location Zoning S t a 843 Granville Street is strategically located just south of DD – Downtown District; Section K1. This zoning permits a n l e y P Robson Street, in the heart of Downtown Vancouver’s maximum Floor Space Ratio (FSR) of 3.50, or up to 10,500 a r k S D entertainment and shopping district. t buildable SF, as well as, a maximum height of 90-feet. r a n le S y t a Beaver P n a l Lake r e k y D The subjectP property’s central location providesr easy access a P Gross Taxes r i k p C e l by way of public transit servicesi (skytrain and bus routes) a u n s e $53,447.08 (2014) e Stanley w R and enjoysa one of the highest daytimed pedestrian counts in Park y Avison W the city.