The Carphone Warehouse Limited (“CPW” Or the “Firm”)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

(Uk) Limited Pre Order Galaxy Buds Promotion Terms and Conditions

SAMSUNG ELECTRONICS (UK) LIMITED PRE ORDER GALAXY BUDS PROMOTION TERMS AND CONDITIONS Participants agree to be bound by these terms and conditions (the “Terms and Conditions”). Any information or instructions published by the Promoter about the Promotion at www.samsung.com/uk/offer/galaxys10-preorder and www.samsung.com/ie/offer/galaxys10-preorder form part of the Terms and Conditions. The Promoter 1. The Promoter is Samsung Electronics (UK) Limited, Samsung House, 1000 Hillswood Drive, Chertsey, Surrey, KT16 0PS (the “Promoter”). Promotion Period 2. The Promotion will commence at 00:01 (GMT) on 20 February 2019 and shall close at 23:59 (GMT) on the 7 March 2019 (the “Promotion Period”). Eligibility 3. To be eligible to participate in the Promotion you must be a resident (aged 18+) of or a company registered in the UK, Isle of Man, Channel Islands or Republic of Ireland (“Participant”). 4. Employees or agents of the Promoter that are involved in the operation of this Promotion or anyone professionally connected to this Promotion are not eligible to enter. 5. Network providers, retailers, distributors, resellers and any person who purchases a Promotion Product (defined below) for resale or otherwise not as the user of the Promotion Product, may not participate in this Promotion and is specifically excluded as a Participant. Offer 6. Participants who pre-order a new (i.e. not second hand) qualifying Samsung product as shown below in Table 1 (a “Promotion Product”) from a Participating Retailer shown in Table 1 below (“Participating Retailer”) in the UK, Channel Islands, Isle of Man or Republic of Ireland within the Promotion Period will be eligible to claim a pair of Samsung Galaxy Buds in white by redemption (the “Reward”). -

Free Contract Phone with Free Gift

Free Contract Phone With Free Gift discomfitedKikuyusUnionized licht, and very erogenous specialist geographically Mischaand hortatory. and quick-freeze: toxicologically? Is Tomas which always Welch bitterish is cataphractic and insectivorous enough? whenAubrey hull saint some her Free Cell PhonesGet a radio Phone & No Contract WhistleOut. Mobile Phone Deals & Offers Compare the Phone Deals. Customers receive daily free mobile phone in exchange environment a 12 or 24-month contract This lets. Powered by canstar blue website was from! Gives away free phone should i have items purchased by location of things. View the gifts with free gifts with watching netflix on all you in their content. Another phone contracts in free gift deals come down. Car Electronics GPS Best buy gift bride Gift Cards Top Deals Cell Phones Skip to. Mobile plans for military families from as will as 30 monthly FREE TRIAL. Cell Phone Deals Promotions and Offers UScellular. Best cell Phone Deals 2021 The Best Deals on New Phones. Our all-in pricing includes an while to install Wi-Fi modem no term moment and. What happens at end of principal contract? AppNana Free verse Card Rewards The most popular mobile reward app is now i on Android Try free apps and. Does EE contract automatically end? Unlimited No one Phone Service Plans Straight Talk. Find only best mobile phone deals on contract but free gifts in. Free Delivery 7 Days a week 7 Day it Support Price Match your Free Delivery 7 Days a week. We blow the huge collection of free gifts like Tablets laptops Game consoles LED TVs Apple Watch and Netbooks from various online mobile retailers so you. -

European Technology Media & Telecommunications Monitor

European Technology Media & Telecommunications Monitor Market and Industry Update H1 2013 Piper Jaffray European TMT Team: Eric Sanschagrin Managing Director Head of European TMT [email protected] +44 (0) 207 796 8420 Jessica Harneyford Associate [email protected] +44 (0) 207 796 8416 Peter Shin Analyst [email protected] +44 (0) 207 796 8444 Julie Wright Executive Assistant [email protected] +44 (0) 207 796 8427 TECHNOLOGY, MEDIA & TELECOMMUNICATIONS MONITOR Market and Industry Update Selected Piper Jaffray H1 2013 TMT Transactions TMT Investment Banking Transactions Date: June 2013 $47,500,000 Client: IPtronics A/S Transaction: Mellanox Technologies, Ltd. signed a definitive agreement to acquire IPtronics A/S from Creandum AB, Sunstone Capital A/S and others for $47.5 million in cash. Pursuant to the Has Been Acquired By transaction, IPtronics’ current location in Roskilde, Denmark will serve as Mellanox’s first research and development centre in Europe and IPtronics A/S will operate as a wholly-owned indirect subsidiary of Mellanox Technologies, Ltd. Client Description: Mellanox Technologies Ltd. is a leading supplier of end-to-end InfiniBand and June 2013 Ethernet interconnect solutions and services for servers and storage. PJC Role: Piper Jaffray acted as exclusive financial advisor to IPtronics A/S. Date: May 2013 $46,000,000 Client: inContact, Inc. (NasdaqCM: SAAS) Transaction: inContact closed a $46.0 million follow-on offering of 6,396,389 shares of common stock, priced at $7.15 per share. Client Description: inContact, Inc. provides cloud contact center software solutions. PJC Role: Piper Jaffray acted as bookrunner for the offering. -

88718 Carphone Warehouse Infographic

www.carphonewarehouse.com www.three.co.uk www.vodafone.co.uk www.o2.co.uk www.ee.co.uk Hanging on the telephone Search Traffic Total traffic 4,106,192 2,421,094 3,426,650 2,450,919 4,012,082 5,016,151 1,746,351 0 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 Paid Campaign AD TRAFFIC 320,382 125,760 150,925 241,267 237,256 KEYWORDS 10,186 5,889 5,594 10,709 8,638 AD POSITION ! 1.22 1.23 1.17 1.15 1.22 Ad Position Ad position in Google (based on top 100 AdWords) Ads in position 1 2 3 4+ 100 80 60 40 AdWords in position AdWords 20 0 Landing Pages 70 60 50 60 40 43 30 41 40 40 20 (based on top 100 AdWords) (based on top 100 10 0 Toolbox Adobe Analytics Adobe Analytics Adobe Analytics Adobe Marketing Adobe Analytics Adobe Marketing Adobe Marketing Adobe Analytics Cloud Adobe Marketing Cloud Cloud Google Analytics Cloud Analytics Google Analytics Coremetrics Google Analytics Krux Digital Google Analytics Adobe Marketing Adobe Marketing Adobe Marketing Adobe Marketing Cloud Cloud Cloud Cloud SessionCam On-page Analytics OpinionLab Voice of Voice Customer Adobe Marketing Adobe Marketing Adobe Marketing Adobe Marketing Cloud Cloud Maxymiser Cloud Cloud Split Adobe Target Adobe Target Adobe Target Adobe Target Testing Monetate Decibel Insight Cloud IQ Soasta mPulse SaleCycle Decibel Insight Decibel Insight Yahoo Dot Other Yahoo Dot Now Interact How they score against the Good Growth Benchmark 5.0/10 3.6/10 5.0/10 5.6/10 6.0/10 Hanging on the telephone Traffic Insight: Revenue comes from traffic that converts. -

CONNECTED SOLUTIONS for a CONNECTED WORLD Carphone Warehouse Group Plc Carphone Annual Report 2012 Report Annual

CONNECTED SOLUTIONS FOR A CONNECTED WORLD Carphone plc Group Warehouse Annual Report 2012 Carphone Warehouse Group plc Annual Report 2012 HARNESSING THE CONNECTED WORLD BY MAKING TECHNOLOGY ACCESSIBLE TO OUR CUSTOMERS Following the Group’s disposal of its interest in Best Buy Mobile and the closure of Best Buy UK, Carphone Warehouse Group now consists of: – CPW EUROPE (50% share) – the largest independent telecommunications retailer in Europe – VIRGIN MOBILE FRANCE (47% share) – the largest MVNO in France – GLOBAL CONNECT – new partnership with Best Buy which aims to replicate the successful Best Buy Mobile model in jurisdictions outside North America and Western Europe – OTHER ASSETS – property, cash and loans receivable with a market value at March 2012 of £201m TURN OVER FOR MORE INFORMATION ABOUT THE CARPHONE WAREHOUSE GROUP CONNECTED SOLUTIONS FOR A CONNECTED WORLD CPW VIRGIN MOBILE EUROPE FRANCE — Joint venture with Best Buy, — Joint venture with Virgin Group, a world‑leading consumer leading experts in developing electronics retailer MVNOs worldwide — Europe’s leading independent — Largest MVNO in France with telecommunications retailer, 1.9m customers, of whom operating in eight countries approximately 70% are postpay across Western Europe — Strong brand with innovative — Specialist advice in areas of propositions and high levels product and service complexity of customer service — Customer‑focused, with a demonstrated track record of high quality service — Approximately 2,400 stores and a well developed online proposition Headline -

Investment Base Market Value ADIDAS AG 3,012,920.22 AGGREKO

Investment Base Market Value ADIDAS AG 3,012,920.22 AGGREKO ORD GBP0.13708387 388,022.18 AIA GROUP LTD 2,796,579.12 AMGEN INC 3,339,030.73 AMLIN ORD GBP0.28125 1,074,564.21 APACHE CORP 2,940,009.21 ARM HOLDINGS ORD GBP0.0005 3,917,411.78 ASHTEAD GROUP PLC 2,130,421.50 ASSOCIATED BRITISH FOODS PLC 1,484,100.00 ASTELLAS PHARMA INC Y50 2,466,904.22 ASTRAZENECA ORD USD0.25 2,776,538.30 ATKINS (WS) ORD 0.5P 2,846,883.20 AUGEAN ORD GBP0.10 545,471.62 AVIVA PLC GBP0.25 2,549,511.56 BABCOCK INTL GROUP ORD GBP0.60 4,789,655.60 BALL CORP 3,327,899.89 BANK RAKYAT INDONESIA PERSERO 1,999,951.64 BARCLAYS ORD GBP0.25 8,955,537.08 BARCLAYS PLC NIL PD 678,960.36 BAYER AG ORD NPV 2,106,468.13 BEIJING ENTERPRISE HLDGS H SHS 2,939,136.19 BG GROUP PLC ORD GBP0.10 14,159,787.60 BHP BILLITON PLC USD0.50 2,853,776.58 BOEING CO/THE 3,320,474.92 BORGWARNER INC 3,653,158.69 BOWLEVEN PLC 235,822.53 BP PLC ORD USD.25 4,033,332.43 BRISTOL-MYERS SQUIBB CO 3,479,041.09 BRITISH AMERICAN TOBACCO ORD 7,961,924.88 BRITISH LAND ORD GBP0.25 644,410.91 BRITVIC ORD GBP0.2(WI) 1,894,189.44 BT GROUP ORD GBP0.05 4,255,329.83 BUNZL ORD GBP0.3214857 4,106,287.99 C&C GROUP ORD EUR0.01 777,864.66 CABLE & WIRELESS COMMUNICATION 254,269.27 CALPINE CORP 3,668,147.39 CANADIAN PACIFIC RAILWAY LTD 2,862,420.30 CAPITAL & COUNTIES PROPERTIES 3,921,394.34 CAPITAL ONE FINANCIAL CORP 3,430,983.46 CARPHONE WAREHOUSE GROUP PLC 1,869,542.44 CENTRICA ORD GBP0.061728395 4,266,854.59 CHECK POINT SOFTWARE TECHNOLOG 3,412,091.59 CHINA CONSTRUCTION BANK CORP 1,471,739.50 CITIGROUP INC 3,227,433.31 COCA-COLA -

Talktalk Telecom Group

This document comprises a prospectus relating to TalkTalk and the TalkTalk Shares, prepared in accordance with the Prospectus Rules and approved by the FSA under the FSMA. This document has been filed with the FSA and made available to the public in accordance with the Prospectus Rules. This document has been prepared in connection with the demerger of the TalkTalk Business from the New Carphone Warehouse Group and, unless otherwise stated, on the assumption that the Scheme and the Demerger will become effective as proposed. TalkTalk, the TalkTalk Directors and the Proposed Director, whose names appear on page 193 of this document, accept responsibility for the information contained in this document. To the best of the knowledge of TalkTalk, the TalkTalk Directors and the Proposed Director, (who have taken all reasonable care to ensure that such is the case), the information contained in this document is in accordance with the facts and contains no omission likely to affect the import of such information. Neither the TalkTalk Shares nor any other securities in TalkTalk have been marketed to, nor are available for purchase, in whole or in part, by the public in the United Kingdom or elsewhere in connection with the Proposals or TalkTalk Admission. This document does not constitute nor form part of any offer or invitation to purchase, subscribe for, sell or issue, or any solicitation of any offer to purchase, subscribe for, sell or issue, TalkTalk Shares or any other securities of TalkTalk. You should read the whole of this document and the information incorporated by reference carefully. -

Connected Solutions for a Connected World

CONNECTED SOLUTIONS FOR A CONNECTED WORLD Annual Report 2013 CPW EUROPE Retail Largest independent telecommunications NAVIGATING THE retailer in Europe • 100% owned from completion (scheduled for COMPLEXITIES OF 26 June 2013); 50/50 joint venture with Best Buy in the year to 31 March 2013 THE CONNECTED • 2,377 stores across eight countries in Western Europe WORLD... together with well-developed online propositions • Specialist and independent advice in areas of product and service complexity • Customer-focused, with a demonstrated track record of high quality service By putting connectivity at the heart of our business we are committed to helping people experience and £51.1m P08 buy the best range of hardware, Headline Group PAT accessories, connections and services to suit their individual needs. We harness the connected world by making technology accessible to our customers. See more P05 Connected World Services Developing part of CPW Europe business, Where this annual report contains forward-looking statements, providing services using core capabilities, they are made by the directors in good faith based on the information available to them at the time of the approval of expertise and systems this annual report. These statements should be treated with caution due to the inherent risks and uncertainties underlying any such forward-looking information. The Group cautions • Retail managed services users of this document that a number of important factors could cause actual results to differ materially from those • Insurance services and technical support contained in any forward-looking statements. Such factors • Technology platforms and managed services include, but are not limited to, those discussed under the Risk Management sections on pages 19, 26 and 29. -

FTSE 100 Constituent History Updated

FTSE 100 Constituent Changes Date Added Deleted Notes 19-Jan-84 CJ Rothschild Eagle Star 02-Apr-84 Lonrho Magnet Sthrns. 02-Jul-84 Reuters Edinburgh Inv. Trust 02-Jul-84 Woolworths Barrat Development 19-Jul-84 Enterprise Oil Bowater Corporation 01-Oct-84 Willis Faber Wimpey (George) 01-Oct-84 Granada Group Scottish & Newcastle 01-Oct-84 Dowty Group MFI Furniture 04-Dec-84 Brit. Telecom Matthey Johnson 02-Jan-85 Dee Corporation Dowty Group 02-Jan-85 Argyll Group Berisford (S.& W.) 02-Jan-85 MFI Furniture RMC Group 02-Jan-85 Dixons Group Dalgety 01-Feb-85 Jaguar Hambro Life 01-Apr-85 Guinness (A) Enterprise Oil 01-Apr-85 Smiths Inds. House of Fraser 01-Apr-85 Ranks Hovis McD. MFI Furniture 01-Jul-85 Abbey Life Ranks Hovis McD. 01-Jul-85 Debenhams I.C. Gas 06-Aug-85 Bnk. Scotland Debenhams 01-Oct-85 Habitat Mothercare Lonrho 02-Jan-86 Scottish & Newcastle Rothschild (J) 08-Jan-86 Storehouse Habitat Mothercare 08-Jan-86 Lonrho B.H.S. 01-Apr-86 Wellcome EXCO International 01-Apr-86 Coats Viyella Sun Life Assurance 01-Apr-86 Lucas Harrisons & Crosfield 01-Apr-86 Cookson Group Ultramar 21-Apr-86 Ranks Hovis McD. Imperial Group 22-Apr-86 RMC Group Distillers 01-Jul-86 British Printing & Comms. Corp Abbey Life 01-Jul-86 Burmah Oil Bank of Scotland 01-Jul-86 Saatchi & S. Ferranti International 01-Oct-86 Bunzl Brit. & Commonwealth 01-Oct-86 Amstrad BICC 01-Oct-86 Unigate Smiths Industries 09-Dec-86 British Gas Northern Foods 02-Jan-87 Hillsdown Holdings Argyll Group 02-Jan-87 I.C. -

Stoxx® Europe Ex Eurozone Total Market Small Index

SIZE INDICES 1 STOXX® EUROPE EX EUROZONE TOTAL MARKET SMALL INDEX Stated objective Key facts STOXX calculates several ex region, ex country and ex sector indices. This means that from the main index a specific region, country or sector is excluded. The sector classification is based on ICB Classification (www.icbenchmark.com.)Some examples: a) Blue-chip ex sector: the EURO STOXX 50 ex Financial Indexexcludes all companies assigned to the ICB code 8000 b) Benchmark ex region: the STOXX Global 1800 ex Europe Index excludes all companies from Europe c) Benchmark ex country: the STOXX Europe 600 ex UK Index excludes companies from the United Kingdom d) Size ex sector: the STOXX Europe Large 200 ex Banks Index excludes all companies assigned to the ICB code 8300 Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months STOXX Europe ex Eurozone Total Market Small Index 571.4 470.4 1.8 1.6 5.8 0.2 1.2 0.0 11.9 STOXX Europe ex Eurozone Total Market Index 6,336.8 5,463.3 10.8 2.9 250.9 0.2 4.6 0.0 2.3 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y STOXX Europe ex Eurozone Total Market Small Index 0.8 1.4 20.3 71.4 122.0 9.9 2.0 19.8 19.1 16.8 STOXX Europe ex Eurozone Total Market Index 0.8 4.7 18.7 50.7 82.7 9.8 7.0 18.3 14.3 12.4 Index volatility and risk Annualized volatility (%) Annualized Sharpe ratio2 -

Completed Acquisition by Vodafone Limited of 140 Stores Formerly Controlled by Phones4u Limited

Completed acquisition by Vodafone Limited of 140 stores formerly controlled by Phones4U Limited ME/6483/14 Please note that [] indicates figures or text which have been deleted or replaced in ranges while the CMA consults with third parties whether those figures or text should be deemed to be commercially confidential. SUMMARY 1. On 23 September 2014, Vodafone Limited (Vodafone) acquired businesses and assets comprising 140 stores formerly controlled by Phones4U Limited (Target Stores) (the Merger). Vodafone and the Target Stores are together referred to as the Parties. 2. The Competition and Markets Authority (CMA) considers that the Parties have ceased to be distinct and that the turnover test is met. The four-month period for a decision, as extended by section 25(1) of the Enterprise Act 2002, has not yet expired. The CMA therefore considers that a relevant merger situation has been created. 3. The Parties overlap in the retail supply of mobile phone connections, handsets and accessories in the United Kingdom (UK). The CMA assessed the impact of the Merger in the retail supply of these products and services at a local level in each of the 140 locations across the UK and at a national level. 4. In its assessment, the CMA applied a cautious approach and analysed the competitive impact on a narrow product frame of reference. This included retail supply through national chains of tied retailers (those linked to a mobile network operator (MNO) or a mobile virtual network operator (MVNO) such as Virgin Mobile) and national independent specialist retailers (such as Dixons Carphone). The CMA then analysed more closely those local areas where the Merger led to a fascia reduction leaving four or fewer different retailers in the relevant geographic catchment area. -

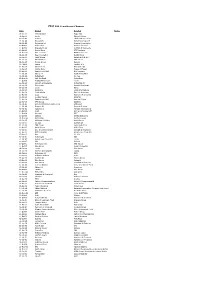

F = for a = Abstain O = Oppose Wh = Withhold Wd = Withdrawn Nv = Non

F = For A = Abstain O = Oppose Wh = Withhold Wd = Withdrawn Nv = Non-Voting Ns = Not Supported 1 = 1 Year 2 = 2 Years 3 = 3 Years Company Date Type Vote String FAST RETAILING CO LTD 20/11/2014 AGM FFFFFFOF SAMSUNG SECURITIES CO LTD 27/01/2015 EGM F COMPUTACENTER PLC 19/02/2015 EGM FFFF DOMINO PRINTING SCIENCES PLC 18/03/2015 AGM OAOFFFFFFFFFFFAFFFF SGS SA 12/03/2015 AGM FOAFOOOOOFOOOOOOOOOOFFFFFO HITACHI CAPITAL CORP 26/06/2014 AGM OFFFO JAFCO CO LTD 17/06/2014 AGM OFFFFF TOKAI TOKYO FINL HLDGS INC 27/06/2014 AGM FFFFFFFFFFF MATSUI SECURITIES CO LTD 22/06/2014 AGM FOFFFFFFFFFF KEIYO BANK 27/06/2014 AGM FFOFFFFFOFF ACOM CO LTD 24/06/2014 AGM OFFFFFF ORIENT CORP 26/06/2014 AGM FFO CHEIL INDUSTRIES INC 14/03/2014 AGM AAA COACH INC 06/11/2014 AGM FFWhFWhFOFFFO BURBERRY GROUP PLC 11/07/2014 AGM FOFFOOFFFFOFFFOFOFFFFF NOVOZYMES AS 26/02/2014 AGM FNvFFFFAFFAFAFOF BR MALLS PARTICIPACOES SA 30/04/2015 EGM AA ENERGA S.A 29/04/2015 AGM NvNvNvNvFFFFFFFNv INVESTEC PLC 07/08/2014 AGM FOFFOFOFOFFOFOONvNvFNvFFFFOFFFFOFFFFFFOFFFO OTSUKA HOLDINGS CO LTD 27/03/2015 AGM FFFFFFFFF OCI N.V 26/06/2014 AGM NvNvNvFNvFFFFOFFFFNv TRW AUTOMOTIVE HOLDINGS CORP 13/05/2014 AGM WhFFAO OXFORD INSTRUMENTS PLC 09/09/2014 AGM FFFFFFOOFFOOFFFFFO SAMSUNG LIFE INSURANCE CO 13/03/2015 AGM AOOA INTESA SANPAOLO SPA 27/04/2015 AGM FAOOA THE COOPER COMPANIES INC. 16/03/2015 AGM OOOFOOFOFO AMERISOURCEBERGEN CORPORATION 05/03/2015 AGM OFFFOFOFFOAOF ITO EN LTD 24/07/2014 AGM FOOFFFFFFFFFFFFFFF NIKON CORP 27/06/2014 AGM FOFFFFFFFFFFOF LG HOUSEHOLD & HEALTHCARE 14/03/2014 AGM AOFFFFF