Indonesian Towers Philippine Fixed Broadband

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Daily Dispatch

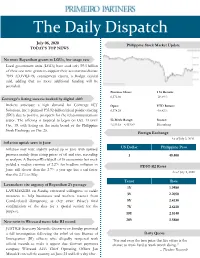

The Daily Dispatch July 06, 2020 Feb. 2, 2017 Philippine Stock Market Update TODAY’S TOP NEWS No more Bayanihan grants to LGUs, low usage rate Local government units (LGUs) have used only P5.5 billion of their one-time grants to support their coronavirus disease 2019 (COVID-19) containment efforts, a Budget official said, adding that no more additional funding will be provided. Previous Close: 1 Yr Return: 6,372.66 -20.58% Converge’s listing success backed by digital shift Brokers anticipate a high demand for Converge ICT Open: YTD Return: Solutions, Inc.’s planned P35.92-billion initial public offering 6,378.29 -18.82% (IPO) due to positive prospects for the telecommunications sector. The offering is targeted to begin on Oct. 13 until 52-Week Range: Source: Oct. 19, with listing on the main board of the Philippine 4,039.15 - 8,419.59 Bloomberg Stock Exchange on Oct. 26. Foreign Exchange As of July 3, 2020 Inflation uptick seen in June US Dollar Philippine Peso Inflation may have slightly picked up in June with upward pressure mainly from rising prices of oil and rice, according 1 49.400 to analysts. A BusinessWorld poll of 16 economists last week yielded a median estimate of 2.2% for headline inflation in PDST-R2 Rates June, still slower than the 2.7% a year ago but a tad faster As of July 3, 2020 than the 2.1% in May. Tenor Rate Lawmakers cite urgency of Bayanihan 2’s passage 1Y 1.9480 LAWMAKERS on Sunday reiterated willingness to tackle measures to help businesses and workers recover from 3Y 2.2050 Covid-related disruptions, as they await Palace’s final 5Y 2.4230 confirmation of the date for a special session for the 7Y 2.6410 purpose. -

TIP Openran: Toward Disaggregated Mobile Networking a Heavy Reading White Paper Produced for the Telecom Infra Project

Independent market research and competitive analysis of next-generation business and technology solutions for service providers and vendors TIP OpenRAN: Toward Disaggregated Mobile Networking A Heavy Reading white paper produced for the Telecom Infra Project AUTHOR: GABRIEL BROWN, PRINCIPAL ANALYST, HEAVY READING WHY OPEN, DISAGGREGATED RADIO ACCESS NETWORKS? Mobile networks serve more than 9 billion connections and generate almost $1 trillion in service revenue annually, according to research firm Omdia.* And with millions of cell sites deployed globally, this makes radio access networks (RANs) the most important distributed network infrastructure in the world. As operators enter the 5G era, the RAN is increasingly software-driven and based on open implementation and open interfaces. Some of the largest equipment vendors are migrating from integrated single-vendor systems to more modular, open platforms. In parallel, a new wave of challengers is adopting software-centric design principles to develop disaggregated, virtual RANs (vRANs) optimized for cloud deployment and operation. This paper profiles the work of the Telecom Infra Project (TIP) OpenRAN Project Group. TIP is an industry initiative focused on advancing open telecom networking through disaggregation, open interfaces, and the development of reference implementations. The TIP OpenRAN Project Group is one of the foremost open RAN initiatives in the industry. It is focused on collaborative working, reference implementations, interoperability, field trials, and developing pathways to commercial deployment of OpenRAN solutions. This paper identifies and explains the key achievements of the project group and looks ahead to the next phases of OpenRAN development. It places the work of the group in a wider industry context to illustrate how OpenRAN helps operators and the wider ecosystem advance their goals for low cost, high performance mobile connectivity. -

Barometer of Mobile Internet Connections in Indonesia Publication of March 14Th 2018

Barometer of mobile Internet connections in Indonesia Publication of March 14th 2018 Year 2017 nPerf is a trademark owned by nPerf SAS, 87 rue de Sèze 69006 LYON – France. Contents 1 Methodology ................................................................................................................................. 2 1.1 The panel ............................................................................................................................... 2 1.2 Speed and latency tests ....................................................................................................... 2 1.2.1 Objectives and operation of the speed and latency tests ............................................ 2 1.2.2 nPerf servers .................................................................................................................. 2 1.3 Tests Quality of Service (QoS) .............................................................................................. 2 1.3.1 The browsing test .......................................................................................................... 2 1.3.2 YouTube streaming test ................................................................................................ 3 1.4 Filtering of test results .......................................................................................................... 3 1.4.1 Filtering of devices ........................................................................................................ 3 2 Overall results 2G/3G/4G ............................................................................................................ -

(Access Network-Fiber) ADN Telecom Limited Bangladesh CTO ADN

Job Title Company Country Deputy General Manager (Access ADN Telecom Limited Bangladesh Network-Fiber) CTO ADN Telecom Limited Bangladesh Director of Customer Relations ASI Silica Machinery United States Engineering ManagerEngineering Manager Asian Vision Cable Philippines COO Asian Vision Cable Philippines Research and Testing Engineer Asian Vision Cable Holdings Inc Philippines IT/MIS Manager Asian Vision Cable Holdings Inc Philippines Network Engineer Asian Vision Cable Holdings Inc Philippines Business Development Representative AVSystem Poland Business Development Manager AVSystem Poland International Sales Director AVSystem Poland CEO AVSystem Poland President, Americas AVSystem United States Network Manager Batangas CATV Inc Philippines Engineer Binangonan Cable Tv Corp. Philippines Engineer Binangonan Cable Tv Corp. Philippines Sales Director APAC/LATAM BKtel Communications GmbH Germany BKtel Representative for South East Asia BKtel Communications GmbH Germany Assistant Manager - Network Operations Cable Link & Holdings Corp. Philippines & Engineering Vice President for Operations Cable Link & Holdings Corp. Philippines Manager - Network Operations & Cable Link & Holdings Corp. Philippines Engineering Head - Network Planning & Design Cable Link & Holdings Corp. Philippines Technical Engineer Cabletronics Cable Systems Inc Philippines Technical Engineer Cabletronics Cable Systems Inc Philippines AVP Solutions Engineering Calix United States Sales Manager Camozzi Technopolymers Srl Italy Chief Executive Officer Celcom Timur (Sabah) -

1Q2021 Financial Results Briefing Presentation

Meeting Reminders • Please mute your microphones during the presentation. • Questions will be entertained during the Q&A portion. You may send your questions through the Zoom Chat feature. Please introduce yourself along with your affiliated company/research house. • The session will be recorded. 2 Today’s Speakers Mr. Dennis Anthony H. Uy Ms. Grace Y. Uy CEO and Co-Founder President and Co-Founder Mr. Matthias Vukovich Mr. Jesus C. Romero Mr. Benjamin B. Azada Chief Financial Office Advisor Chief Operations Officer Chief Strategy Officer 1Q2021 Results Key Takeaways Maintained industry-leading trifecta in 1Q2021 (vs. 1Q2020) with ✓ 83.6% revenue growth, 55.0% EBITDA margin and 23.1% ROIC Continued strong EBITDA growth in 1Q2021 with 101.6% YoY growth ✓ (vs. 1Q2020) 500k new ports and 182k gross residential subscribers added in ✓ 1Q2021. Converge captured 48% of Fixed Broadband Net Adds Improved our residential blended ARPU from P1,284 in 1Q2020 to ✓ P1,390 during 1Q2021 Residential business delivered 110% YoY revenue growth in 1Q2021, ✓ driven by strong subscriber additions and slightly improved ARPU ✓ Enterprise business grew 2% YoY in 1Q2021 6 Added ~500k FTTH Ports during 1Q2021 Extensive and Fast-growing Network Homes Passed (MM) (1)(2)(3) 13% 25% 14% 28% 55% More than 7.1MM homes passed as of March 2021, almost 190 350 128 331 15.1 ✓ double from March 2020 ~2x 7.1 6.2 0.8 ~28% household coverage nationwide as of December 2020 3.2 0.8 3.6 ✓ (~50% in Luzon) 0.8 5.3 0.8 2.4 2.8 6.3 (6) 2019 2020 1Q2020 1Q2021 2021E 2025E Targeting 55% household coverage (~15MM homes passed) by FTTH Homes Passed HFC Homes Passed ✓ 2025 Monthly Addition Run-rate (‘000s) (4) Household Coverage (5) (for last month in the period) Number of Ports (MM) (1)(2) 100 177 66 165 ~4.0MM ports as of March 2021, 82% increase from March 7.5-8.0 ✓ 2020. -

Philippine Broadband Market Report

ICT MONITORING OVERVIEW This special report will give readers a view of the evolu&on of PHILIPPINE the broadband market in the Philippines -revenue, market share per provider, latest ini&a&ves, analyst outlook of the poten&al development and more about PH broadband BROADBAND market in the next few years. MARKET REPORT KEY PROVIDERS COVERED • Converge ICT • Eastern • Globe • PLDT • PT&T • Radius • RISE • Sky Cable • Source KEY INDICATORS COVERED Subscrip&ons (Historical quarterly figures covering the past 3 years + 5-year forecast): • Total broadband subscrip&ons • Total broadband subscrip"ons – market share by technology: xDSL, cable, FTTH/FTTB, fixed wireless access, mobile broadband, satellite) • Total broadband subscrip"ons – market share by provider • Total Business broadband subscrip&ons • Business broadband subscrip"ons – market share by technology: xDSL, cable, FTTH/FTTB, fixed wireless access, mobile broadband, satellite) • Business broadband subscrip"ons – market share by provider • Total Residen&al broadband subscrip&ons • Residen"al broadband subscrip"ons – market share by technology: xDSL, cable, FTTH/FTTB, fixed wireless access, mobile broadband, satellite) • Total Residen"al broadband subscrip"ons – market share by provider • Total broadband penetra&on rate (including breakdown by technology: xDSL, cable, FTTH/FTTB, fixed wireless access, mobile broadband, satellite) • Total broadband penetra"on rate – by provider • Business broadband penetra&on rate (including breakdown by technology: xDSL, cable, FTTH/FTTB, fixed wireless access, -

Analisis Kinerja Keuangan Berdasarkan Metode Eva Studi Pada Perusahaan Telekomunikasi Yang Tercatat Di Bursa Efek Indonesia (Bei) Tahun 2013

Vol. 3. No. 1, Juni 2015 Ekuitas – Jurnal Pendidikan Ekonomi ANALISIS KINERJA KEUANGAN BERDASARKAN METODE EVA STUDI PADA PERUSAHAAN TELEKOMUNIKASI YANG TERCATAT DI BURSA EFEK INDONESIA (BEI) TAHUN 2013 Ni Made Tatsani Widi Arini Jurusan Pendidikan Ekonomi Universitas Pendidikan Ganesha Singaraja, Indonesia e-mail: [email protected] ABSTRAK Penelitian ini bertujuan untuk mengetahui (1) nilai NOPAT pada Perusahaan Telekomunikasi yang telah tercatat di BEI tahun 2013, (2) nilai biaya modal pada perusahaan telekomunikasi yang telah tercatat di BEI tahun 2013, (3) kinerja keuangan perusahaan telekomunikasi yang telah tercatat di BEI tahun 2013 ditinjau dengan metode EVA. Jenis penelitian ini adalah deskriptif kuantitatif. Data dikumpulkan dengan metode dokumentasi dan analisis data yang digunakan yaitu analisis EVA. Hasil penelitian menunjukkan (1) nilai NOPAT PT Telekomunikasi Indonesia Tbk. adalah Rp 20.987.000.000.000,00, PT Indosat Tbk. sebesar Rp 841.838.000.000,00, PT Smartfren Tbk. sebesar Rp -1.784.682.909.136,00, PT XL Axiata Tbk. sebesar Rp 1.301.438.000.000,00, PT Bakrie Telecom sebesar Rp 27.320.180.033,00. (2) Biaya modal untuk PT Telekomunikasi Indonesia Tbk. sebesar Rp 10.284.848.546.016,00, PT Indosat Tbk. sebesar Rp 3.273.701.158.489,00, PT Smartfren Tbk. sebesar Rp 790.441.706.857,00, PT XL Axiata sebesar Tbk. Rp 1.670.800.564.235,00, dan biaya modal PT Bakrie Telecom sebesar Rp 196.585.006.260,00. (3) Hasil analisis EVA menunjukkan PT Telekomunikasi Indonesia Tbk. memililki nilai EVA>0, ini berarti kinerja keuangan perusahaan telah mampu menciptakan nilai tambah bagi perusahaan. -

Analysis and Testing of Data Transmission of Providers in Indonesia Using Gsm and Cdma Modem

(IJID) International Jurnal on Informatics for Development, Vol. 6, No. 1, 2017 ANALYSIS AND TESTING OF DATA TRANSMISSION OF PROVIDERS IN INDONESIA USING GSM AND CDMA MODEM Fanni Rakhman Hakim Bambang Sugiantoro Department of Informatics Department of Informatics Faculty of Sains and Technology Faculty of Sains and Technology State Islamic University Sunan Kalijaga State Islamic University Sunan Kalijaga Yogyakarta, Indonesia Yogyakarta, Indonesia [email protected] AbstractFThe technology of internet nowadays has Basically everyone who is connected to the Internet, become most important aspect and becomes they can exchange information and data between one primary need for certain group of peoples who person with others, either in the form of images, work in some field like sounds, video, text and more. With the it community, education,economy,health,etc. One of the biggest utilizing it in resolving the problem of the daily work problem which mostly brought by so many people that demands speed and accuracy. One of them is in is speed in data transfer. This paper emphasize in the speed of the data transfer. directly testing the quality of data transmission from each transmission technology. The equipment Mobile technology is also growing rapidly in line used by this paper is ZTE Join Air help, the with the needs of the community to get simcard provided by Telkomsel,XL, and indosat, communication service that is quick and easy. Some while CDMA technology used simcard provided by service providers mid-haul vying Indonesia good- smartfren and esia and modem provided by based Global System for Mobile Communication Smartfren which its series is EC176-2. -

NOW Corp Prospectus June 21, 2018

of of SUBJECT TO COMPLETION PRELIMINARY PROSPECTUS STRICTLY CONFIDENTIAL nary Prospectus constitute an offer to sell or the solicitation here such offer or sale is not permitted. is not oroffer sale such here notice. notice. The Offer Shares may not be sold nor may an offer to buy be NOW Corporation (A corporation duly incorporated under the laws of the Republic of the Philippines) Primary Offer of 5,000,000 Redeemable Convertible Cumulative Non-Participating Non-Voting Peso- denominated Preferred ―A‖ Shares with an Oversubscription Option of Subscriptions to 5,000,000 Preferred ―A‖ Shares, with 25,000,000 underlying Common Shares and an additional 25,000,000 Common Shares upon the exercise of the Oversubscription Option, which Common Shares shall be issued upon conversion of the Preferred ―A‖ Shares at a conversion price of ₱20.00 per share, or a conversion ratio of 5 Common Shares for every 1 Preferred ―A‖ Share, at an Initial Dividend Rate of [7.5544% to 8.3044%]1 per annum and an Offer Price of ₱100.00 per share to be listed and traded on the Main Board of the Philippine Stock Exchange, Inc. and 10,000,000 Detachable Subscription Warrants to be issued free of charge, with 10,000,000 underlying Common Shares, with an Oversubscription Option of Subscriptions to 10,000,000 Detachable Subscription Warrants and 10,000,000 underlying Common Shares to be listed and traded on the Main Board of the Philippine Stock Exchange, Inc. Unicapital, Inc. Issue Manager, Bookrunner and Underwriter The date of this Preliminary Prospectus is [June __, 2018]. -

Analisis Kualitas Jaringan 4G Menggunakan Parameter

ANALISIS KUALITAS JARINGAN 4G MENGGUNAKAN PARAMETER QUALITY OF SERVICE DI KOTA MAKASSAR Analysis Of 4G Network Quality Using Parameters Quality Of Service In The City Of Makassar Ayu Fitrah Alyah1, Dyah Darma Andayani 2, Syahrul3 Pendidikan Teknik Informatika dan Komputer, Jurusan Teknik Informatika dan Komputer Universitas Negeri Makassar [email protected] Abstrak - Perkembangan teknologi infomasi dan Teknologi dari layanan broadband sendiri telekomunikasi berkembang secara cepat dari generasi ke terus berkembang, dimulai dari generasi pertama atau generasi, perkembangan teknologi tersebut telah sampai biasa disebut dengan istilah 1G (Generasi Pertama), dimana pada generasi ini memiliki standar teknologi kegenerasi 4G. Perkembangan jaringan 4G memiliki Nordic Mobile Telephone (NMT) yang digunakan kemampuan transmisi yang besar terutama dalam hal berbasis analog, kemudian masuk ke generasi 2G kecepatan download dan upload, karena banyaknya teknologi sudah berbasis digital dilanjutkan ke generasi keinginan masyarakat akan kualitas jaringan dari provider 2.5G dengan peningkatan dalam kapasitas Bandwitdh yang dapat digunakan dengan lancar dan cepat, hal ini dari generasi sebelumnya sampai pada tahun 2000 an dimanfaatkan perusahaan telekomunikasi membangun perkembangan teknologi telekomnikasi di dunia Internet Service Provider (ISP) yang lebih cepat tersebut telah mencapai generasi 4G LTE bahkan 5G. Dengan berkembangnya jaringan seluler menggunakan jaringan 4G. Adanya perbedaan kualitas seperti hadirnya teknologi 4G LTE yang memiliki jaringan pada provider yang memicu untuk melakukan kemampuan transmisi yang besar terutama dalam hal pengujian kualitas jaringan 4G. Penelitian ini bertujuan kecepatan untuk download dan upload, serta banyaknya untuk menganalisis kualitas jaringan 4G dari berbagai keinginan masyarakat akan kualitas jaringan dari provider layanan telepon seluler di wilayah Kota Makassar, provider yang dapat digunakan untuk mengakses secara diwakili oleh Tiga provider. -

Depressed Valuations, Worth Their Uplift

Equity Research Telco Monday,24 May 2021 Telco OVERWEIGHT Depressed valuations, worth their uplift TLKM relative to JCI Index Our key thesis remains the buoyant data traffic enhanced by OTT and ecommerce solutions. Mobile competition could potentially ease off, and xxxx new competition levers will enhance outlook. Remain OVERWEIGHT. Telco M&A; short to medium term beneficiaries. 4,247 Towers divestment was performed at lightning speed by Indosat in the eyes of investors, and is able now to announce debt repayments. Their 1Q21 results renders a higher 2021 prospect to turn net profit and therefore Indosat becomes an attractive asset, unimaginable a few quarters back, – and offers a commanding lead in their M&A negotiation with Hutch3. Although M&A talks took extension implying stumbling issues in their way; but definitely will set the backdrop for the remainder of 2021. Last week telco stocks gained as catalysts reinforced one another; Indosat positive 1Q21 results and together with Smartfren aiming to post near zero net losses and become more attractive M&A targets, Telkomsel EXCL relative to JCI Index additional investment placing in Goto, and XL Axiata looking to benefit from xxxx slack in Indosat+Hutch3 combined future performance. Buoyant data traffic enhanced by OTT and ecommerce. XL 1Q21 numbers showed signs of market weakness XL posted results in 1Q21, with topline/EBITDA dragged by competition. 4Q20 and FY20 periods were heavily influenced by promotion of Unlimited data plans, smaller validity data plans to address weakening purchasing power, and from school data subsidies. These apply also in Indosat but it had better its capex resources and spectrum migration to 4G. -

Sec Form – I-Acgr Integrated Annual Corporate Governance Report

SEC FORM – I-ACGR INTEGRATED ANNUAL CORPORATE GOVERNANCE REPORT 1. For the fiscal year ended: December 31, 2020 2. SEC Identification Number: CS200716094 3. BIR Tax Identification No. 006-895-049 4. Exact name of issuer as specified in its charter CONVERGE ICT SOLUTIONS, INC. 5. Metro Manila, Philippines 6. (SEC Use Only) Province, Country or other jurisdiction of Industry Classification Code: incorporation or organization 7. New Street Bldg., Mc Arthur Highway, Balibago, Angeles City, Pampanga 2009 Address of principal office Postal Code 8. (02) 8667-0888 Issuer's telephone number, including area code 9. N/A Former name, former address, and former fiscal year, if changed since last report. INTEGRATED ANNUAL CORPORATE GOVERNANCE REPORT COMPLIANT/ ADDITIONAL INFORMATION EXPLANATION NON- COMPLIANT The Board’s Governance Responsibilities Principle 1: The company should be headed by a competent, working board to foster the long- term success of the corporation, and to sustain its competitiveness and profitability in a manner consistent with its corporate objectives and the long- term best interests of its shareholders and other stakeholders. Recommendation 1.1 1. Board is composed of directors with The Board of Directors is composed collective working knowledge, experience of highly skilled and capable or expertise that is relevant to the individuals, having expertise and company’s industry/sector. competencies in multiple industries 2. Board has an appropriate mix of that enable them to respond to the competence and expertise. needs of the organization and act for Compliant 3. Directors remain qualified for their positions the best interest of the company. individually and collectively to enable them to fulfill their roles and responsibilities References: and respond to the needs of the SEC Annual Report 17A Pages (56-57) organization.