Maxell Holdings (6810, JP) 12/15/2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Suppliers for the Fairphone 2 Understanding Our List of Suppliers

List of Suppliers for the Fairphone 2 Consumer electronics supply chains include layers of our supply chain. In addition to our several complex, often opaque tiers of first-tier assembly manufacturer, we have suppliers, ranging from first-tier assembly mapped all second-tier suppliers, and are manufacturers (direct suppliers) to second, progressively including third and fourth-tier third and sometimes even fourth-tier suppliers in our research. By uncovering all component manufacturers. Many electronics of the different players and manufacturing manufacturers only have insight into their locations in our smartphone supply chain, we direct suppliers and perhaps some second-tier can start engaging with suppliers, establishing component manufacturers. relationships and initiating programs for improvement. At Fairphone, we are working to gain an in-depth understanding of the complicated Understanding our List of Suppliers The list below includes all of the first, second Locations: Whenever possible, we have listed and third-tier suppliers that we know of to the (approximate) manufacturing location. If this date, and it is accurate to the best of our information was not available, we have provided the location of the company headquarters. knowledge at the time of publication. We will periodically update the information in this Categories: Suppliers are grouped by the type of document as we learn more. components they produce. Some suppliers may be mentioned more than once because they produce Here is a bit more information about how the different kinds of components, sometimes with list is arranged: different manufacturing locations. Tiers: Supplier tiers are calculated from the point of the final assembly. -

Phoenix Unit Trust Managers Manager's Interim Report Putm Bothwell Japan Tracker Fund

PHOENIX UNIT TRUST MANAGERS MANAGER’S INTERIM REPORT For the half year: 1 February 2016 to 31 July 2016 PUTM BOTHWELL JAPAN TRACKER FUND Contents Investment review 2-3 Portfolio of investments 4-51 Top ten purchases and sales 52 Statistical information 53-56 Statements of total return & change in net assets attributable to unitholders 57 Balance sheet 58 Distribution table 59 Corporate information 60-61 1 Investment review Dear Investor Performance Review Welcome to the PUTM Bothwell Japan Tracker Fund Over the review period, the PUTM Bothwell Japan interim report for the six months to 31 July 2016. Tracker Fund returned 17.59% (Source: HSBC, Gross of AMC, GBP, based upon the movement in the Cancellation Price for the six months to 31/07/16). This compares with its benchmark index return of 17.94% (Source: Datastream, FTSE World Japan Index until 04/03/14 and thereafter the Topix Index, Total Return in GBP terms for six months to 31/07/16). In the table below, you can see how the Fund performed against its benchmark index over the last five discrete one-year periods. Standardised Past Performance Jul 15-16 Jul 14-15 Jul 13-14 Jul 12-13 Jul 11-12 % growth % growth % growth % growth % growth PUTM Bothwell Japan Tracker Fund 15.15 17.3 -0.6 29.8 -8.2 Benchmark Index 15.66 17.7 -0.4 30.2 -8.1 Source: Fund performance is HSBC, Gross of AMC, GBP, based upon the movement in the Cancellation Price to 31 July for each year. Benchmark Index performance is Datastream, FTSE World Japan Index until 04/03/14 and thereafter the Topix Index, Total Return in GBP terms to 31 July for each year. -

DEV-Informationdisplay

0 I Chapter News • (See also Page 13} Information JAPAN CHAPTER wins the Editor's Prize this month for B. A second meeting chaired by Chuji Sujuki, SID content and humor. On July 23 this chapter had two Chapter Committeeman was attended by 14 SID meetings at the Sharp Corporation offices in Tokyo as members and 15 non-members. This meeting was follows: primarily for yo ung engineers and research scientists. A. Meeting chaired by lwao Ohishi, Chai rman of SID Topics discussed included: Display Japan Chapter and Masao Sugimoto, Vice-Chairman, BCEE Group, IEEE Tokyo Chapter, attended by 29 SID * Topics i n author interviews at the 1981 SID members and 29 non-members. The program was as symposium j The Official Journal of t he Society For Information D isplay NOVEM BER, 1981 follows: * Sinclair's f lat CRTs * Application of POPs v * Cost down of Flat Panel Displays 1. Report on the 1981 SID International Symposium * Kanji Displays and Human Fa ctors General Review Koh-ichi Miyaji, * Penetration CRTs Shibaura Institute of Technology 1 .2 Session VII Human Factors * Eurodisplay '81 and Japan Display '83 Hideo Kusaka, NHK Broadcasting Science Research Labs., Tokyo 1.3 Session X Color CATs Humor: Ryuichi Kaneko, Japan Chapter Secretary, sent CATs your Editor a package of material which arrived just too Osamu Takeuchi, Sony Corp., Tokyo 1.4 Session IX Passive Displays I late for our September/ October issue. But don't ever let Noboru Kaneko, Daini Seikosha anyone tell you that our Japanese friends lack a sense of Co., Ltd., Tokyo humor. -

2020 Integrated Report

Integrated Report 2020 Year ended March 31, 2020 Basic Commitment of the Toshiba Group Committed to People, Committed to the Future. At Toshiba, we commit to raising the quality of life for people around The Essence of Toshiba the world, ensuring progress that is in harmony with our planet. Our Purpose The Essence of Toshiba is the basis for the We are Toshiba. We have an unwavering drive to make and do things that lead to a better world. sustainable growth of the Toshiba Group and A planet that’s safer and cleaner. the foundation of all corporate activities. A society that’s both sustainable and dynamic. A life as comfortable as it is exciting That’s the future we believe in. We see its possibilities, and work every day to deliver answers that will bring on a brilliant new day. By combining the power of invention with our expertise and desire for a better world, we imagine things that have never been – and make them a reality. That is our potential. Working together, we inspire a belief in each other and our customers that no challenge is too great, and there’s no promise we can’t fulfill. We turn on the promise of a new day. Our Values Do the right thing We act with integrity, honesty and The Essence of Toshiba comprises three openness, doing what’s right— not what’s easy. elements: Basic Commitment of the Toshiba Group, Our Purpose, and Our Values. Look for a better way We continually s trive to f ind new and better ways, embracing change With Toshiba’s Basic Commitment kept close to as a means for progress. -

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

Presentation Slides for 2Q-FY 2019

Second Quarter of FY 2019 (July 1 to September 30, 2019) Consolidate Financial Results Japan Display Inc. November 13, 2019 2Q-FY2019 Summary Sales: 2Q-FY19 sales increased QoQ and YoY due to the launch of major new products and advanced shipments of some other products. For the 1H sales were up 11%. Op. income: QoQ: Higher sales, write down effects and the effects of the Hakusan Plant production suspension reduced the operating loss to about ¥19bn. YoY: Contribution of an inventory increase in the 1H of last year to operating profit is absent this year. Major costs: Non-operating costs: Equity method investment loss of ¥2.1bn, Typhoon No. 15-related costs of ¥600mn Extraordinary losses: Business restructuring expenses of ¥12.1bn. (Billion yen) Net Operating Ordinary Net Dep. & R&D FX rate sales income income income Amort. expense (\/US$) 2Q-FY19 147.3 (8.1) (12.2) (25.4) 4.3 2.6 107.4 1Q-FY19 90.4 (27.5) (31.6) (83.3) 7.5 2.8 109.9 2Q-FY18 111.0 (4.7) (6.3) (7.8) 11.0 2.8 110.3 1H-FY19 237.8 (35.6) (43.8) (108.7) 11.8 5.5 108.6 Copyright © 2019 Japan Display Inc. All Rights Reserved. 2 Quarterly Sales by Region & Business Category Quarterly Sales Trends 2Q-FY19 Sales by Category (Billion yen) US/Euro China Mobile ■ Mobile category 251.1 Other regisons • Sales almost doubled QoQ due to the Non-mobile launch of new products and advanced Automotive shipments of some other products. -

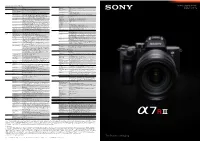

Interchangeable-Lens Digital Camera Viewfinder (Cont.) Field Coverage 100% Lens Mount E-Mount Magnification Aapprox

Main specifications of Interchangeable-lens General Camera Type Interchangeable-lens digital camera Viewfinder (Cont.) Field Coverage 100% Lens mount E-mount Magnification Aapprox. 0.78 x (with 50mm lens at infinity, -1m-1) digital camera Image sensor Type 35mm full frame (35.9×24.0mm), Exmor R CMOS sensor Dioptre Adjustment -4.0 to +3.0m-1 Number of Pixels Approx. 42.4 megapixels (effective), Approx. 43.6 (Total) Eye Point Approx. 23mm from the eyepiece lens, 18.5mm from the eyepiece frame at -1m-1 (CIPA Image sensor Aspect Ratio 3:2 standard) Anti-Dust System Charge protection coating on optical filter and image sensor shift mechanism Finder Frame Rate Selection NTSC mode: STD 60fps / HI 120fps Recording System Recording Format JPEG (DCF Ver. 2.0, Exif Ver.2.31, MPF Baseline compliant), RAW (Sony ARW 2.3 format) PAL mode: STD 50fps / HI 100fps (still image) Image Size (pixels) [3:2] [35mm full frame] L: 7952 x 5304 (42M), M: 5168 x 3448 (18M), S: 3984 x 2656 (11M) Display Content Graphic Display, Display All Info., No Disp. Info., Digital Level Gauge, Histogram [APS-C] L: 5168 x 3448 (18M), M: 3984 x 2656 (11M), S: 2592 x 1728 (4.5M) LCD Screen Type 7.5cm (3.0-type) type TFT Image Size (pixels) [16:9] [35mm full frame] L: 7952 x 4472 (36M), M: 5168 x 2912 (15M), S: 3984 x 2240 (8.9M) Number of Dots 1,440,000 dots [APS-C] L: 5168 x 2912 (15M), M: 3984 x 2240 (8.9M), S: 2592 x 1456 (3.8M) Touch Panel Yes Image Quality modes RAW, RAW & JPEG (Extra fine, Fine, Standard), JPEG (Extra fine, Fine, Standard) Brightness Control Manual (5 steps between -2 and +2), Sunny Weather mode Picture Effect 8 types: Posterization (Color), Posterization (B/W), Pop Color, Retro Photo, Partial Color (R/ Adjustable Angle Up by approx. -

Printmgr File

PROSPECTUS Sony Corporation (incorporated with limited liability under the laws of Japan) ¥150,000,000,000 Zero Coupon Convertible Bonds due 2017 OFFER PRICE: 102.5 PER CENT. The ¥150,000,000,000 Zero Coupon Convertible Bonds due 2017 (bonds with stock acquisition rights, tenkanshasaigata shinkabu yoyakuken-tsuki shasai) (the “Bonds”, which term shall, unless the context requires otherwise, include the stock acquisition rights (shinkabu yoyakuken) (the “Stock Acquisition Rights”) incorporated in the Bonds) of Sony Corporation (herein, the “Company”) will be issued in registered form in the denomination of ¥20,000,000 each with a Stock Acquisition Right exercisable on or after December 14, 2012 up to, and including, November 16, 2017 (unless previously redeemed or purchased and cancelled, or become due and repayable) into fully-paid and non-assessable shares of common stock of the Company (the “Shares”) at an initial Conversion Price (as defined in the terms and conditions of the Bonds, the “Conditions”), subject to adjustment in certain events as set out herein, of ¥957 per Share. The Closing Price (as defined in the Conditions) of the Shares as reported on the Tokyo Stock Exchange, Inc. (the “Tokyo Stock Exchange”) on November 14, 2012 was ¥870 per Share. Unless previously redeemed or purchased and cancelled, the Bonds will be redeemed at 100 per cent. of their principal amount on November 30, 2017. On or after November 30, 2015, the Bonds may be redeemed in whole but not in part at their principal amount at the option of the Company as set out herein, provided that no redemption may be made unless the Closing Price of the Shares for each of the 20 consecutive Trading Days (as defined in the Conditions), the last of which occurs not more than 30 days prior to the day upon which the notice of redemption is first given, is at least 130 per cent. -

IBIS Open Forum Minutes

IBIS Open Forum Minutes Meeting Date: November 8, 2019 Meeting Location: Tokyo, Japan VOTING MEMBERS AND 2019 PARTICIPANTS ANSYS Curtis Clark, Marko Marin, Miyo Kawata* Toru Watanabe, Akira Ohta, Bailing Zhang, Xi Wu Xin Sun, Jack Wu, Gregory Liao, Frances Peng Joan Chen, Ruby Wu Applied Simulation Technology (Fred Balistreri) Broadcom (Yunong Gan) Cadence Design Systems [Brad Brim], Ambrish Varma, Ken Willis Yingxin Sun, Zhen Mu, Jinsong Hu, Skipper Liang Zuli Qin, Haisan Wang, Hui Wang, Yaofei Wang Yitong Wen, Binyue (Kathy) Yang, Zhangmin Zhong George Zhu, Eric Lu, Frank Pai, Jessica Yeh Sylvia Kao, Nemo Hsu, Tric Chiang, Morihiro Nakazato* Cisco Systems Hannah Bian, Guobing (Robin) Han, Wei Li Zongyuan Liu, Sijie Mao, Jun (Gene) Zhang Dassault Systemes (CST) Stefan Paret, Longfei Bai Ericsson Anders Ekholm*, Anders Vennergrund, Felix Mbairi Hui Zhou, Inmyung Song, Mattias Lundqvist Wenyan Xie, Zilwan Mahmod, Nan Hou, Amy Zhang GLOBALFOUNDRIES Steve Parker Google Zhiping Yang, Songping Wu Huawei Technologies Antonio Ciccomancini, Haiping Cao, Peng Huang Hongxing Jiang, Chunhai Li, Shengli (Victory) Wang Zhengrong Xu, Hang (Paul) Yan, Chen (Jeff) Yu Zhengyi Zhu, Tianqi Fang Futurewei Technologies Albert Baek IBM Michael Cohen, Greg Edlund Infineon Technologies AG Anke Sauerbrey, Pietro Brenner, Francesco Settino Instituto de Telecomunicações (Abdelgader Abdalla) Intel Corporation Hsinho Wu, Michael Mirmak, Nhan Phan Kinger Cai, Eddie Frie, Wendem Beyene Yuanhong Zhao, Bruce Qin, Kai Yuan, Denis Chen Neo Hsiao Keysight Technologies Radek Biernacki, Hee-Soo Lee, Stephen Slater Jian Yang, Ming Yan, Pegah Alavi, Jiarui Wu Jiajie Zhao, Nash Tu, Toshinori Kaeura* Satoshi Nakamizo* ©2018 IBIS Open Forum 1 Maxim Integrated Joe Engert, Yan Liang, Charles Ganal Mentor, A Siemens Business Arpad Muranyi, Raj Raghuram, Weston Beal Vladimir Dmitriev-Zdorov, Mikael Stahlberg Todd Westerhoff, Ed Bartlett, Nitin Bhagwath Kunimoto Mashino* Micron Technology Randy Wolff*, Justin Butterfield, Jingwei Cheng Zack Yang, Cheng Zhang Micron Memory Japan, G.K. -

INCJ, Hitachi, Sony and Toshiba Sign Definitive Agreements Regarding Integration of Small- and Medium-Sized Display Businesses

FOR IMMEDIATE RELEASE INCJ, Hitachi, Sony and Toshiba Sign Definitive Agreements Regarding Integration of Small- and Medium-Sized Display Businesses Tokyo, November 15, 2011 --- Innovation Network Corporation of Japan (“INCJ”), Hitachi, Ltd. (“Hitachi”), Sony Corporation (“Sony”) and Toshiba Corporation (“Toshiba”) announced today that they have signed definitive agreements to integrate their small- and medium-sized display businesses in a new company to be established and operated by INCJ as attached. About Hitachi, Ltd. Hitachi, Ltd., (NYSE: HIT / TSE: 6501), headquartered in Tokyo, Japan, is a leading global electronics company with approximately 360,000 employees worldwide. Fiscal 2010 (ended March 31, 2011) consolidated revenues totaled 9,315 billion yen ($112.2 billion). Hitachi will focus more than ever on the Social Innovation Business, which includes information and telecommunication systems, power systems, environmental, industrial and transportation systems, and social and urban systems, as well as the sophisticated materials and key devices that support them. For more information on Hitachi, please visit the company's website at http://www.hitachi.com. # # # Attached NEWS RELEASE Innovation Network Corporation of Japan Hitachi, Ltd. Sony Corporation Toshiba Corporation INCJ, Hitachi, Sony and Toshiba Sign Definitive Agreements Regarding Integration of Small- and Medium-Sized Display Businesses TOKYO, November 15, 2011 – Innovation Network Corporation of Japan (“INCJ”), Hitachi, Ltd. (“Hitachi”), Sony Corporation (“Sony”) and -

FTSE Developed Asia Pacific All Cap

FTSE PUBLICATIONS 19 November 2016 FTSE Developed Asia Pacific All Cap Indicative Index Weight Data as at Closing on 30 September 2016 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 13 Holdings <0.005 HONG KONG Anest Iwata 0.01 JAPAN AWE <0.005 AUSTRALIA 360 Capital Industrial Fund 0.01 AUSTRALIA Anicom Holdings 0.01 JAPAN Axial Retailing 0.01 JAPAN 3S Korea <0.005 KOREA Anritsu 0.01 JAPAN Azbil Corp. 0.04 JAPAN 77 Bank 0.02 JAPAN Ansell 0.04 AUSTRALIA Bandai Namco Holdings 0.1 JAPAN a2 Milk 0.02 NEW Anton Oilfield Services <0.005 HONG KONG Bando Chem Inds 0.01 JAPAN ZEALAND AOI Electronics <0.005 JAPAN Bank of East Asia 0.08 HONG KONG AAC Technologies Holdings 0.12 HONG KONG Aoki Holdings 0.01 JAPAN Bank of Iwate 0.01 JAPAN Abacus Property Group 0.01 AUSTRALIA Aomori Bank 0.01 JAPAN Bank of Kyoto 0.04 JAPAN ABC-Mart 0.03 JAPAN Aoyama Trading 0.03 JAPAN Bank of Nagoya 0.01 JAPAN Able C&C <0.005 KOREA Aozora Bank 0.07 JAPAN Bank of Okinawa 0.01 JAPAN Accordia Golf 0.01 JAPAN APA Group 0.12 AUSTRALIA Bank of Queensland Ltd. 0.05 AUSTRALIA Accordia Golf Trust 0.01 SINGAPORE Aplus Financial <0.005 JAPAN Bank of Ryukyus 0.01 JAPAN Achilles <0.005 JAPAN APN News & Media 0.01 AUSTRALIA Bank of Saga 0.01 JAPAN Acom 0.03 JAPAN APN Outdoor Group 0.01 AUSTRALIA Bapcor 0.02 AUSTRALIA Aconex 0.01 AUSTRALIA Apt Satellite <0.005 HONG KONG Beach Energy 0.01 AUSTRALIA Acrux <0.005 AUSTRALIA ARA Asset Management 0.01 SINGAPORE Beadell Resources 0.01 AUSTRALIA Adastria Holdings 0.01 JAPAN Arakawa -

List of Suppliers for the Fairphone 2 Understanding Our List of Suppliers

List of Suppliers for the Fairphone 2 Consumer electronics supply chains include layers of our supply chain. In addition to our several complex, often opaque tiers of first-tier assembly manufacturer, we have suppliers, ranging from first-tier assembly mapped all second-tier suppliers, and are manufacturers (direct suppliers) to second, progressively including third and fourth-tier third and sometimes even fourth-tier suppliers in our research. By uncovering all component manufacturers. Many electronics of the different players and manufacturing manufacturers only have insight into their locations in our smartphone supply chain, we direct suppliers and perhaps some second-tier can start engaging with suppliers, establishing component manufacturers. relationships and initiating programs for improvement. At Fairphone, we are working to gain an in-depth understanding of the complicated Understanding our List of Suppliers The list below includes all of the first, second Locations: Whenever possible, we have listed and third-tier suppliers that we know of to the (approximate) manufacturing location. If this date, and it is accurate to the best of our information was not available, we have provided the location of the company headquarters. knowledge at the time of publication. We will periodically update the information in this Categories: Suppliers are grouped by the type of document as we learn more. components they produce. Some suppliers may be mentioned more than once because they produce Here is a bit more information about how the different kinds of components, sometimes with list is arranged: different manufacturing locations. Tiers: Supplier tiers are calculated from the point of the final assembly.