Polen Capital, and Please Feel Free Importance on Education

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

4607 Stores 11084 Millions Of

4,607 stores millions of 11,084 euros in sales countries with 74 sales presence 92,301 employees nnual A Report 2009 Global Reporting 6 Initiative Indicators Letter from the 14 Chairman Inditex business 16 model 18 53 54 163 IP Inditex Performance IC Inditex Commitment Summary of 2009 Customers, shareholders 20 financial year 56 and society Milestones Corporate Social 26 for the year 66 Responsibility Commercial Human 28 concepts 124 Resources International Environmental 46 presence 136 dimension 4 Inditex Annual Report 2009 164 309 LD Legal Documentation Economic and financial 167 report Corporate governance 233 report Activities Report 296 Audit and Control Committee Activities Report Nomination 303 And Remuneration Committee Verification of the audit of 308 GRI indicators 5 lobal G Reporting Initiative Indicators With transparency as the fundamental principle in its relationship with society, Inditex has followed the Global Reporting Initiative indicators since it published its first Sustainability Report in 2002. Using this guide, Inditex attempts to provide detailed, organised access to the infor- mation on its activity to all its stakeholders. Within the general indicators, specific indicators for the textile and footwear sector have been included, identified in the following way: Specific indicator for the sector Specific indicator comment for the sector 6 Inditex Annual Report 2009 Pages 1. STRATEGY AND ANALYSIS 14-15 1.1 Statement from the most senior decision-maker about the relevance of sustainability to the organisation and its strategy. 267-273, 1.2 Description of key impacts, risks, and opportunities. 20-25 Apparel and Footwear Sector Specific Commentary: Where applicable, this should include an assessment of supply chain performance. -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Annual Report 2014

We want to help people and businesses prosper Annual 2014 report Santander in 2014 Santander’s purpose is to help people and businesses prosper. We want to be the best retail and commercial bank that earns the lasting loyalty of our people, customers, shareholders and communities. Ana Botín Group executive chairman Employees Customers Shareholders Communities 12 million students and teachers benefit from cooperation agreements 185,405 117 3.2 between universities and employees million customers million shareholders the Bank Gender International network Agreements with universities 45% 55% 12,951 €0.479 1,175 branches EPS in 2014 cooperation agreements in 21 countries Customer loans (net) Positioning Contribution to higher education 97% 734,711 #1 146 employees received million euros largest market capitalisation million euros for training in 2014 in the euro zone universities Recognitions Geographic diversification Contribution to attributable profit (%) REST OF EUROPE 6% UNITED KINGDOM UNITED STATES 19% 10% GERMANY 5% POLAND 6% BRAZIL MEXICO 19% 8% PORTUGAL 2% REST OF LATIN AMERICA 1% SPAIN 14% CHILE ARGENTINA 6% 4% Main countries Other countries where Banco Santander has commercial and retail banking businesses: Peru, Puerto Rico, Uruguay, Colombia, Norway, Sweden, Finland, Denmark, Holland, Belgium, Austria, Switzerland and Italy. Financial indicators Total on-balance sheet assets CET1 fully loaded 1,266,296 9.7% Million euros Group attributable profit Balance sheet and results (Million euros) 2014 2013 Million euros Customer loans -

Amadeus IT Group, S.A

Amadeus IT GroupGroup,, S.A. Auditors’ Report Annual Accounts and Directors’ Report for the year ended December 31, 2013 Amadeus IT Group, S.A. Auditors’ Report for the year ended December 31, 2013 Amadeus IT Group, S.A. Annual Accounts for the year ended December 31, 2013 AMADEUS IT GROUP, S.A. BALANCE SHEET AT DECEMBER 31, 2013 AND 2012 (EXPRESSED IN THOUSANDS OF EUROS - KEUR) ASSETS Note 31/12/2013 31/12/2012 NON ---CURRENT ASSETS 3,634,4 919191 3,670,2 222333 Intangible fixed assets 6 2,154,239 2,245,771 Brands & trademarks 256,550 256,550 Goodwill 1,388,231 1,388,231 Software 7,348 4,151 Intangible rights 502,110 596,839 Tangible fixed assets 7 4,236 3,517 Furniture, office , equipment and other tangible assets 4,236 3,517 Long ---term investments in Group companies and joint ventures 18.2 1,1,1, 319,209 111,296,284 Equity instruments 8.3 899,589 869,144 Loans to companies 419,620 427,140 Long ---term financial investments 8.1 29,2 646464 31, 873 Equity instruments 7,451 6,300 Derivatives 10 876 5, 680 Other financial assets 20,937 19,893 Deferred tax assets 15 .1 113 ,,,287 92,778 Prepaid expenses long ---term 14,256 --- CURRENT ASSETS 808,596 708, 534 Trade debtors and other accounts receivable 318,033 223,27 333 Trade accounts receivable 9.1 179,156 129,648 Accounts receivable - Group companies and joint ventures 18 .2 115,784 70,255 Other accounts receivable 18,883 19,18 8 Employees receivable 385 305 Other accounts receivable from Public Administrations 15 .1 3,825 3,877 Short ---term investments in Group companies and joint -

Análisis De Datos Financieros: Amadeus

COLEGIO UNIVERSITARIO DE ESTUDIOS FINANCIEROS GRADO EN ADE BILINGÜE Trabajo de Fin de GRADO ANALÍSIS DE DATOS FINANCIEROS AMADEUS Autor: Cuesta García-Villamil, Álvaro Tutor: Gracia Díez, Mercedes Queralt Sánchez de las Matas, Ricardo Madrid, Abril 2020 INDEX 1. Abstract ........................................................................................................................ 3 2. Amadeus ...................................................................................................................... 3 2.1 General Company Description ................................................................................ 3 2.2 History and Geographic Location ........................................................................... 4 2.3 Business Structure ................................................................................................... 5 2.4 Share Capital ........................................................................................................... 7 2.5 Main Financial Events ............................................................................................ 7 3. Sector Analysis .......................................................................................................... 10 4. Financial Statements Analysis ................................................................................. 11 5. Statistical Descriptive Analysis ................................................................................ 15 5.1 Data Collection .................................................................................................... -

Common Stocks — 104.5%

Eaton Vance Tax-Advantaged Global Dividend Income Fund January 31, 2021 PORTFOLIO OF INVESTMENTS (Unaudited) Common Stocks — 104.5% Security Shares Value Aerospace & Defense — 0.8% Safran S.A.(1) 98,721 $ 12,409,977 $ 12,409,977 Banks — 6.7% Bank of New York Mellon Corp. (The) 518,654 $ 20,657,989 Citigroup, Inc. 301,884 17,506,253 HDFC Bank, Ltd.(1) 512,073 9,775,702 ING Groep NV(1) 1,676,061 14,902,461 Japan Post Bank Co., Ltd. 445,438 3,851,696 Mitsubishi UFJ Financial Group, Inc. 2,506,237 11,317,609 Mizuho Financial Group, Inc. 292,522 3,856,120 Sumitomo Mitsui Financial Group, Inc. 186,747 5,801,916 Wells Fargo & Co. 341,979 10,218,332 $ 97,888,078 Beverages — 1.0% Diageo PLC 378,117 $ 15,180,328 $ 15,180,328 Biotechnology — 1.2% CSL, Ltd. 82,845 $ 17,175,550 $ 17,175,550 Building Products — 0.9% Assa Abloy AB, Class B 509,607 $ 12,603,485 $ 12,603,485 Chemicals — 0.7% Sika AG 38,393 $ 10,447,185 $ 10,447,185 Construction & Engineering — 0.0% Abengoa S.A., Class A(1)(2) 311,491 $ 0 Abengoa S.A., Class B(1)(2) 3,220,895 0 $0 Construction Materials — 0.9% CRH PLC 332,889 $ 13,660,033 $ 13,660,033 Consumer Finance — 0.6% Capital One Financial Corp. 79,722 $ 8,311,816 $ 8,311,816 1 Security Shares Value Diversified Financial Services — 2.5% Berkshire Hathaway, Inc., Class B(1) 101,853 $ 23,209,243 ORIX Corp. -

EURO STOXX 50® Multi-Asset Indices

EURO STOXX 50® Multi-Asset Index Family January, 2017 1 1. EURO STOXX 50® - ICONIC BLUE-CHIP EUROZONE EQUITY INDEX 2 EURO STOXX 50 ® is Europe’s leading equity index EURO STOXX 50 ® » Launched 1998 » 50 blue-chip companies from 12 Eurozone countries » Representative and highly liquid » Underlying for financial products » Serves as benchmark 3 Outstanding methodology ensures well-balanced supersector representation Key facts Current index constituents » 50 largest companies from the Eurozone ADIDAS FRESENIUS AHOLD DELHAIZE GRP SOCIETE GENERALE AIR LIQUIDE IBERDROLA » Superior selection method for companies AIRBUS INDITEX ALLIANZ ING GRP » Captures about 60% of total free-float ANHEUSER-BUSCH INBEV INTESA SANPAOLO ASML HLDG L'OREAL supersector leaders AXA LVMH MOET HENNESSY BASF MUENCHENER RUECK » Quarterly adjustments to ensure timely BAYER NOKIA BCO BILBAO VIZCAYA ORANGE representation of markets ARGENTARIA PHILIPS BCO SANTANDER SAFRAN » Fully rules-based and transparent concept BMW SAINT GOBAIN BNP PARIBAS SANOFI without any subjectivity CRH SAP DAIMLER SCHNEIDER ELECTRIC » AUM in ETFs: EUR35.2 bn1) DANONE SIEMENS DEUTSCHE BANK TELEFONICA DEUTSCHE POST TOTAL » 73,010 Structured Products issued in 2016 DEUTSCHE TELEKOM UNIBAIL-RODAMCO YTD2) E.ON UNILEVER NV ENEL VINCI ENGIE VIVENDI ENI VOLKSWAGEN PREF ESSILOR INTERNATIONAL 1) Data as of Dec. 30, 2016 4 2) Data as of Oct. 30, 2016 2. EURO STOXX 50® CORPORATE BOND INDEX 5 The corporate bond index tracks the performance of EUR- denominated bonds issued by the EURO STOXX 50® companies Index methodology » Corporate bonds from companies1) that are constituents of EURO STOXX 50® index at the Underlying bond time of the rebalancing universe » Issuer Type: Corporate bonds, denominated in EUR Bond selection » Bond Type: Fixed and zero-coupon bonds criteria » Rating: Investment Grade (consolidated rating BBB or higher) » Time to maturity: At least 15 months measured from the respective re-balancing date » Amount outstanding: Minimum EUR 750 mn » Formulas acc. -

Cruz Roja Responde” Plan

Honeste vivere, alterum non laedete cuique suum tribuere OUR LAW OFFICES SUPPORT THE SPANISH RED CROSS “CRUZ ROJA RESPONDE” PLAN March 26, 2020 Spain is facing hard times in the health alert of the COVID-19 Coronavirus, which today raises the number of infected to more than 56,000 people and the number of deaths to more than 4,000 people. Our law offices in Malaga and Oporto wish to communicate to our clients and friends the following: 1. Despite the uncertainty and threat of recession hanging over the economy worldwide, it is gratifying the enormous solidarity effort and social commitment that some companies, charitable organizations and individuals are assuming to support and assist in the fight against the pandemic. Some of the large companies of the IBEX-35, such as Inditex, Iberdrola, Telefonica, Santander or BBVA, among others, companies like El Corte Inglés, Ikea, Mango, sports clubs like Real Madrid, and some foundations, businessmen, athletes and individuals are donating millions of euros or directly contributing providers of medical supplies and their logistical capacity to meet the urgent needs for equipment and protective accessories for healthcare professionals. 2. Spanish healthcare professionals are at the limit of their capabilities and need more respirators, personal protective equipment (self-filtering masks, protective gloves and clothing, eye and face protection material, etc), more ambulances for the mobilization of those affected and temporary hospital infrastructures, among other needs. 3. The Spanish Red Cross or Cruz Roja has been cooperating with the Spanish authorities and the Spanish health system since the beginning of the health crisis, with an unprecedented deployment of means and intense activity to attend to the most vulnerable people and the general population. -

FTSE Developed Europe

2 FTSE Russell Publications 19 August 2021 FTSE Developed Europe Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 1&1 AG 0.01 GERMANY Avast 0.03 UNITED Cnp Assurance 0.02 FRANCE 3i Group 0.14 UNITED KINGDOM Coca-Cola HBC AG 0.06 UNITED KINGDOM Aveva Group 0.05 UNITED KINGDOM A P Moller - Maersk A 0.1 DENMARK KINGDOM Coloplast B 0.19 DENMARK A P Moller - Maersk B 0.15 DENMARK Aviva 0.19 UNITED Colruyt 0.03 BELGIUM A2A 0.03 ITALY KINGDOM Commerzbank 0.07 GERMANY Aalberts NV 0.05 NETHERLANDS AXA 0.43 FRANCE Compagnie Financiere Richemont SA 0.55 SWITZERLAND ABB 0.51 SWITZERLAND B&M European Value Retail 0.06 UNITED Compass Group 0.33 UNITED KINGDOM ABN AMRO Bank NV 0.04 NETHERLANDS KINGDOM BAE Systems 0.21 UNITED Acciona S.A. 0.03 SPAIN Continental 0.14 GERMANY KINGDOM Accor 0.06 FRANCE ConvaTec Group 0.05 UNITED Baloise 0.06 SWITZERLAND Ackermans & Van Haaren 0.03 BELGIUM KINGDOM Banca Mediolanum 0.02 ITALY ACS Actividades Cons y Serv 0.06 SPAIN Covestro AG 0.1 GERMANY Banco Bilbao Vizcaya Argentaria 0.36 SPAIN Adecco Group AG 0.09 SWITZERLAND Covivio 0.04 FRANCE Banco Santander 0.58 SPAIN Adevinta 0.04 NORWAY Credit Agricole 0.14 FRANCE Bank Pekao 0.03 POLAND Adidas 0.63 GERMANY Credit Suisse Group 0.22 SWITZERLAND Bankinter 0.03 SPAIN Admiral Group 0.08 UNITED CRH 0.35 UNITED Banque Cantonale Vaudoise 0.02 SWITZERLAND KINGDOM KINGDOM Barclays 0.35 UNITED Adyen 0.62 NETHERLANDS Croda International 0.12 UNITED KINGDOM KINGDOM Aegon NV 0.06 NETHERLANDS Barratt Developments 0.09 UNITED Cts Eventim 0.03 GERMANY Aena SME SA 0.1 SPAIN KINGDOM Cyfrowy Polsat SA 0.02 POLAND Aeroports de Paris 0.03 FRANCE Barry Callebaut 0.07 SWITZERLAND Daimler AG 0.66 GERMANY Ageas 0.09 BELGIUM BASF 0.64 GERMANY Danone 0.37 FRANCE Ahold Delhaize 0.26 NETHERLANDS Bayer AG 0.53 GERMANY Danske Bank A/S 0.1 DENMARK AIB Group 0.02 IRELAND Bechtle 0.04 GERMANY Dassault Aviation S.A. -

Appendix D Updated.Xlsx

Block Threshold Minimum - Screen Tradeable LIS Pre-Trade Value - Block Only Strategy Threshold Minimum - Strategy Threshold Minimum - Basis Trade Threshold MIC PCC LCC Name ESMA ISIN Curr Lot Size Contracts Contracts Screen Tradeable Contracts Block Only Contracts Minimum Post-Trade LIS IFLO NWD NWA 21st Century Fox - Cash FLEX Fut Stock futures/forwards US90130A1016 USD 100 N/A 11 N/A 22 n/a 527 IFLO NWH NWA 21st Century Fox - Phys FLEX Fut Stock futures/forwards US90130A1016 USD 100 N/A 11 N/A 22 n/a 527 IFLO IIU III 3i Group plc - Amer Cash FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO IIQ III 3i Group plc - Amer Phys FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO 0U6 III 3i Group Plc - Cash DASF Stock dividend futures/forwardsGB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 60 IFLO IIY III 3i Group plc - Cash FLEX Fut Stock futures/forwards GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO IIJ III 3i Group plc - Euro Cash FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO IIX III 3i Group plc - Euro Phys FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO III III 3i Group Plc - STND OPT Stock options GB00B1YW4409 GBP 1000 250 3 500 6 n/a 168 IFLO PMR PMA 3M Co - Amer Phys Flex Opt Stock options US88579Y1010 USD 100 N/A 2 N/A 4 n/a 79 IFLO 3CP PMA 3M Co - Cash DASF Stock dividend futures/forwardsUS88579Y1010 USD 100 N/A 2 N/A 4 n/a 28 IFLO PMD PMA 3M Co - Cash FLEX Fut Stock futures/forwards US88579Y1010 USD 100 N/A 2 N/A 4 n/a 79 IFLO PML PMA 3M Co - Euro Cash Flex -

Esic Ranked 2 Business School in Spain for Its Talent

ESIC RANKED 2nd BUSINESS SCHOOL IN SPAIN FOR ITS TALENT IN ADDITION, ESIC HAS BEEN RANKED IN 47th POSITION AMONG THE 100 SPANISH COMPANIES WITH GREATEST CAPACITY FOR ATTRACTING AND RETAINING TALENT ACCORDING TO THE CORPORATE REPUTATION MONITOR, ESIC IS RANKED 4TH BEST COMPANY TO WORK FOR IN SPAIN (IN THE CATEGORY OF LESS THAN 800 EMPLOYEES) AFTER MICROSOFT, DKV AND IE BUSINESS SCHOOL According to the 11th Merco Talent Ranking, the monitor that determines the 100 best companies with most talent in Spain, ESIC is not only the second business school in the sector, ahead of EAE, IESE and ESADE, but it has been ranked 47th among the Spanish companies with greatest capacity to attract and retain talent. The monitor evaluates companies taking into consideration three key values: employment quality, employer brand and internal reputation. The monitoring of the methodology used for the elaboration of this ranking is subject to independent review by the consulting firm KPMG. Madrid, 7 November 2016 – The ranking is headed by Inditex, Repsol and BBVA. They are followed by Telefónica, Apple, Iberdrola, Santander, Google, Mercadona and Gas Natural in that order. This year, Merco Talent has carried out an analysis of workers’ commitment, both with the team with which they work regularly and with the organization as a whole, focusing on the culture of commitment. Merco Talent seeks to collect and analyze the different reputational dimensions linked to talent, including all those groups that determine the attractiveness of companies when it comes to capturing and retaining talent. Thus, the monitor has evaluated the opinion of more than 18,458 employees of the companies present in the ranking, 826 university graduates, 117 HR managers, 928 citizens, 748 alumni from business schools, 53 experts and head-hunters as well as a comparative analysis of the best management policies in the main ranked companies. -

Polen International Growth Portfolio Manager Commentary – June 2021

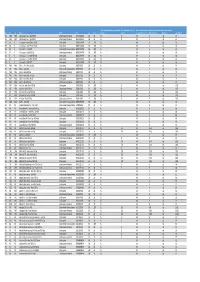

Polen International Growth Portfolio Manager Commentary – June 2021 Summary • During the second quarter of 2021, the Polen • The Portfolio performed largely in line with the Index. International Growth Composite Portfolio (the An uptick in regulatory action in China dampened the “Portfolio”) returned 5.57% gross of fees. The MSCI relative outperformance delivered by other positions All Country World Index (ex-US) (the “Index”) in the information technology and consumer returned 5.47%. discretionary sectors. • Pro-cyclical factors—which contrast the Portfolio’s • During the quarter, we initiated new positions in focus on secular, durable growth—drove market ASML, MercadoLibre, and Shopify. We added to our returns higher since November 2020 but seemed to investment in Adidas, and we trimmed our positions subside during the quarter. in Accenture, CSL, Walmart de Mexico, Bunzl, and Inditex. • Short-term differences in performance can work either for or against the strategy. That said, our focus • Ultimately, we seek to invest in companies that remains on positioning the Portfolio for superior long- contribute to consistent earnings growth across term earnings growth rather than shorter-term market cycles. This philosophy, in our view, results in a market preferences. Portfolio built to compound earnings growth faster than the Index. Seeks Growth & Capital Preservation (Performance (%) as of 06-30-2021) 1 Yr 3 Yr Inception 40 30 20 10 0 Qtr YTD 1 Yr 3 Yr 5 Yr Inception Polen International Growth (Gross) 5.57 4.36 20.66 11.19 - 15.87 Polen International Growth (Net) 5.46 4.16 20.14 10.40 - 15.00 MSCI ACWI (ex-USA) 5.47 9.16 35.71 9.38 - 11.04 The performance data quoted represents past performance and does not guarantee future results.