What's in Our Food and on Our Mind

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Black Star Farms Food Service: Breakfast Chef PURPOSE: To

Black Star Farms Food Service: Breakfast Chef PURPOSE: To provide kitchen support, direction, and supervision for breakfast and hospitality at The Inn of Black Star Farms PAY RATE: $17-$20/hour, $1000 seasonal bonus CLASS: Hourly HOURS: Minimum 40 hours per week, may exceed 50 at peak times RESPONSIBILITY: Food service operations support REPORTING TO: Estate Chef & Director of Events and Culinary Operations REQUIREMENTS • Must be at least 18 years of age • Minimum Bachelor’s degree in associated industry or equivalent in experience and training • Be able to prepare and serve high quality, composed farm-to-table style breakfast and uphold white table cloth standards of food quality and service • Flexible schedule • Must be able to work weekends and holidays • Previous experience with commercial kitchen operations, experience with logistical coordination, problem resolution • ServSafe Certification, HAACP, or working towards • Some working knowledge of “farm-to-table” restaurant operations EXPECTATIONS • Coordinate and prepare daily Inn breakfast and hospitality hour (B&H) hors d'oeuvres • Supervise any kitchen personnel related to (B&H) and assist with coordinating assigned culinary activities • Ensure par stocks of breakfast food are maintained, ordered, and on hand for B&H services • Monitor and maintain white table cloth presentation and quality standards for all food served at B&H • Maintain recipe books and illustrations associated with all B&H functions • Track supply inventory weekly to ensure that all supplies are ordered, stocked, -

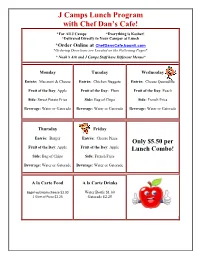

J Camps Lunch Program with Chef Dan's Cafe!

J Camps Lunch Program with Chef Dan’s Cafe! *For All J Camps *Everything is Kosher! *Delivered Directly to Your Camper at Lunch *Order Online at ChefDansCafe.boonli.com *Ordering Directions are Located on the Following Pages* * Noah's Ark and J Camps Staff have Different Menus* Monday Tuesday Wednesday Entrée: Macaroni & Cheese Entrée: Chicken Nuggets Entrée: Cheese Quesadilla Fruit of the Day: Apple Fruit of the Day: Plum Fruit of the Day: Peach Side: Sweet Potato Fries Side: Bag of Chips Side: French Fries Beverage: Water or Gatorade Beverage: Water or Gatorade Beverage: Water or Gatorade Thursday Friday Entrée: Burger Entrée: Cheese Pizza Only $5.50 per Fruit of the Day: Apple Fruit of the Day: Apple Lunch Combo! Side: Bag of Chips Side: French Fries Beverage: Water or Gatorade Beverage: Water or Gatorade A la Carte Food A la Carte Drinks Bagel w/cream cheese $2.00 Water Bottle $1.00 1 Slice of Pizza $2.25 Gatorade $2.25 This page is intentionally left blank Options 1, 2, 3 Chef Dan’s Cafe has partnered with BOONLI to provide a secure, fast, and easy-to-use online ordering system that allows our Owings Mills J Camps families to view our lunch menu, order, prepay and manage camper lunches from their smartphone, tablet, or computer. Registration and Ordering is Open! HOW TO GET STARTED! Go To ChefDansCafe.boonli.com (please bookmark this page) Click Create an Account: Password is: omjcc1 Enter information and click Submit CREATE YOUR USER PROFILES Every person who you will order for requires their own User Profile Enter First Name and -

Type of Meal

TYPE OF MEAL Breakfast: It is the first meal of the day served between 7 and 10.am. It offers all kinds of dishes that are suitable for the breakfast. Continental breakfast, English breakfast, American Breakfast and Indian breakfast menus are the commonly found menus. It may be in the form of table d’ hotel and a- la carte. Continental Breakfast: It is also termed as simple breakfast. It generally includes only bread and rolls with butter an preserves. Breakfast rolls include croissant, brioche, Vienna rolls. Etc . Preserves include Jam, marmalade and honey but honey is not placed on the table unless it is required. Term used in continental Breakfast Café complet- continental breakfast with coffee Café simple- only coffee with nothing to eat The complet- Continental breakfast with tea The Simple- Only tea, with nothing to eat. English Breakfast: It is heavy breakfast including the Fruit juices, stewed fruits, breakfast cereals , eggs, fish , meat, breads and beverages. Though the English breakfast is quite heavy traditionally, limited dishes are preferred by the guests. American Breakfast: American breakfast is neither too heavy nor light. It usually consist of eggs, juice, Bacon or sausage, toast or hash brown potatoes. It includes juice/ Fresh fruits, breakfast cereals, eggs to order, waffle/ pancake served with syrup and honey, choice of breads with butter and preserves. Coffee is the most preferred beverage. Chilled water is served before breakfast. Indian Breakfast: India is the land of varied culture, language and also of varied eating habits, Parathas, stuffed paratha, poori, masala etc are commonly served dishes in the North during breakfast along with bread and rolls, egg preparation. -

Breakfast Menu

Breakfast 6:00am-10:30am Omelets House Favorites Served with Breakfast Potatoes Egg Favorite Classic* 11.50 Denver Omelet 11.75 Two eggs, choice of ham, bacon or sausage Ham, peppers, onion, cheddar cheese with breakfast potatoes ~ GF Breakfast Burrito 10.50 Spanish Omelet 12.25 Scrambled eggs, bacon, sausage, cheddar cheese, Peppers, onion, black olives, peppers, house salsa, sour cream, and tortilla with pepper jack cheese, fresh salsa breakfast potatoes Grizzly Bear Omelet 13.25 Biscuits and Gravy 8.50 Bacon, sausage, ham, cheddar cheese Served with breakfast potatoes Angler Omelet 13.25 Corned Beef Hash* 10 Smoked trout, tomato, cream cheese Served with two cage free eggs, and breakfast potatoes ~ GF Morning Glory Omelet 12.25 Mountain Man Breakfast* 11 Egg whites, spinach, tomatoes and mushrooms Idaho trout with lemon butter, two cage free eggs and breakfast potatoes ~ GF Build Your Own 3 Egg Omelet 12.00 Choice of three: mushrooms, onions, peppers, bacon, Croissant Sandwich 10.50 ham, cheddar cheese, Swiss cheese Scrambled eggs, ham, cheddar cheese, Each Additional Item $0.75 and breakfast potatoes Pancakes Steel Cut Oatmeal 7 ~ Vegan Full Stack Buttermilk Pancakes 9.50 Cinnamon-Vanilla French Toast 9.50 Short Stack Buttermilk Pancakes 8 Choice of Bacon or Sausage I’m Your Huckleberry Pancakes 14 *Consuming raw or undercooked meats, poultry, seafood, or eggs may increase your risk of food-borne illness if you have certain medical conditions. Kindly address any dietary restrictions to your server. All dishes prepared using local and sustainable products as available. Parties of 8 or more will incur a 20% gratuity. -

Breakfast and Supper Menu

Breakfast and Supper Menu For more than 65 years, our menu has welcomed countless visitors with these simple words: “Thank you for your visit, we’re so glad you’re here.” Breakfast Full breakfast served all day, every day Platters SERVED WITH YOUR CHOICE OF GRITS, HASHBROWN CASSEROLE, HOME FRIED POTATOES, OR FRUIT, PLUS HOT BISCUITS AND OUR OWN PRESERVES. Famous Loveless Cafe Country Ham (7oz) 14.99 Country Fried Steak and Two Eggs* 13.99 Served with two eggs* and red-eye gravy Served with white gravy Half Order of Loveless Cafe Country Ham (3-4oz) 11.99 Breakfast Steak* and Two Eggs* – cooked to order 16.99 Served with two eggs* and red-eye gravy “City” Ham and Two Eggs* 13.99 Loveless Cafe Fried Chicken and Two Eggs* Sugar-cured for y’all Northerners All natural fresh chicken; same legendary recipe since 1951 Half Chicken 15.99 Music City Platter 15.29 Quarter Chicken | Dark Meat 12.99 • Light Meat 13.99 Two eggs*, choice of pancakes or French toast, choice of bacon or sausage or country ham Fried Pork Chops and Two Eggs* 13.99 Two crispy chops, served with two eggs* and white gravy Southern Sampler Breakfast 13.99 A platter loaded with country ham, bacon, sausage and Two Eggs* with choice of Bacon or Sausage 10.79 two eggs* Pit-cooked Pork Barbeque and Two Eggs* 13.99 Biscuit Sampler Platter 12.99 Breakfast Sandwich 10.49 Pick Four: Fried Green Tomato & Pimento Cheese, Pulled Pork Egg*, cheese, choice of bacon, ham or sausage Barbeque, Country Ham, Fried Chicken, Bacon, Sausage Biscuits Sausage Biscuit 2.75 Chicken Biscuit: Fried or Grilled 3.00 Add an egg* for 1.00 Add an egg* for 1.00 Bacon Biscuit 2.75 Pulled Pork Barbeque Biscuit 3.25 Add an egg* for 1.00 Add an egg* for 1.00 Country Ham Biscuit 2.75 Pimento Cheese n’ Fried Green Tomato Biscuit 3.00 Add an egg* for 1.00 Can’t Decide? Try our Biscuit Sampler Platter! Omelets ALL OMELETS ARE MADE WITH THREE EGGS AND SERVED WITH HOT BISCUITS AND OUR OWN PRESERVES; HONEY AND SORGHUM AVAILABLE ON REQUEST. -

Picos Restaruant

Breakfast Menu SERVED SATURDAY AND SUNDAY FROM 9AM TO 3PM Chilaquiles Omelets Chilaquiles Verdes o Rojos con Pollo 12 Chihuahua Omelet 12 Crispy homemade totopos tossed with chunks of pulled Filled with mushrooms, roasted poblano peppers, onions and chicken with your choice of tomatillo or ranchero sauce Chihuahua cheese topped with Chihuahua cheese and crema Mexicana Poblano Omelet 15 Chilaquiles Enmolados 12 Filled with roasted poblano peppers, squash blossoms, Crispy homemade totopos tossed with chunks of Pulled chuitlacoche and goat cheese chicken with your choice of mole poblano or mole negro Oaxaqueno, topped with Cotija cheese, crema Mexicana and Veggie & Cotija Cheese Omelet 12 chopped onions Filled with spinach, mushrooms, roasted poblano peppers, Add two fried eggs 3 onions and Cotija cheese. BREAKFAST OF CHAMPIONS All omelets are served with your choice of roasted potatoes or refried beans, house made tortillas and salsa ranchera. Menudo Bowl 10 Cup 6 Light breakfast Pozole (Potzolli) Bowl 10 Cup 6 Choice of chicken (verde) or traditional pork (rojo) Hot Cakes 7 Pancakes served with butter & maple syrup Huevos Fruit Plate 6 Seasonal fresh fruits Huevos en Rabo de Mestiza (drowned eggs) 12 Eggs poached in a tomato, roasted poblano pepper and onion Sides sauce, covered with melted Chihuahua cheese Chilaquiles Verdes o Rojos 5 Huevos Motuleños 12 Chorizo (Mexican Sausage) 4 Fried eggs served over slightly crisp corn tortillas topped with black beans and sliced ham, covered with fresh tomato chilpotle Tocino (Bacon) 5 salsa, Cotija -

Breakfast Meal Pattern Idaho School Nutrition Reference Guide

Breakfast Meal Pattern Idaho School Nutrition Reference Guide OVERVIEW The School Breakfast Program (SBP) is a Federally-funded, State administrated, nonprofit meal program operating in public and nonprofit private schools and residential child care institutions. The SBP provides nutritionally balanced, low-cost or free breakfasts to children each school day. First established by Congress as a pilot program in 1966, the SBP became a permanent program in 1975 and has continued to expand every year. The School Breakfast Program operates in the same manner as the National School Lunch Program. School districts and independent schools that choose to take part in the breakfast program receive reimbursement from the United States Department of Agriculture (USDA), through their State agency (SA), for each meal they serve. In return, participating School Food Authorities (SFAs) must serve breakfasts that meet Federal meal pattern requirements, and they must offer free or reduced price breakfasts to eligible children. The meal pattern and nutrition standards are based on the latest Dietary Guidelines for Americans, though decisions about specific food items to serve and how to prepare food are made by local SFAs. TERMS TO KNOW Food component (aka meal component) - One of the required food groups that comprise a USDA reimbursable meal; the three required breakfast food components are: fruit/vegetable; grain; and fluid milk. Schools must offer the specified food components in at least the minimum required quantities. Food item - A specific food offered within the food components required at breakfast. Depending on the planned menu, the student may need to select more than one food item to have the minimum quantity needed for a component to be credited. -

Dietary Variations Among Hispanics and Latinos with Diabetes Nilda Benmaor , M.S.,R.D.N., C.D.E

5/16/2018 “All Are Not The Same” Dietary Variations Among Hispanics and Latinos with Diabetes Nilda Benmaor , M.S.,R.D.N., C.D.E. ©Nilda Benmaor, RDN,CDE ‐2017 Learning Objectives After completing this course, nutrition professionals should be able to: . Select culturally appropriate foods for Hispanics and Latinos with diabetes. Identify the nutrient composition of traditional foods and the impact on post prandial blood sugar levels. Learn how to individualize a diabetic meal plan that includes patient’s preferred foods from country of origin. Apply diabetic dietary guidelines and carbohydrate counting to meal planning. Assess individual patient’s needs and beliefs in order to improve adherence to dietary recommendations and to achieve optimal glycemic control. CDR Learning Codes: 3000 Nutrition Assessment; 5000 Medical Nutrition Therapy; 5190 Diabetes Mellitus; 2020 Composition of Foods Nutrient Analysis ©Nilda Benmaor, RDN,CDE ‐2017 “It is easier to change a man’s religion than to change his diet.” Margaret Mead, Cultural Anthropologist ©Nilda Benmaor, RDN,CDE ‐2017 1 5/16/2018 Latin American Culture Place of Birth : The name of the province, territory or country in which the person was born. Ethnicity Mixed race ancestry: Colonization by Spain, Portugal and France. Immigration from Italy , Germany and Eastern Europe, Africa, China and Korea. Language Spanish, Portuguese ( Brazil), French ( Caribbean and French Guiana). Religion Primary is Roman Catholic. Also Protestant, Jewish, Evangelical, Buddhist, .Hindu ©Nilda Benmaor, RDN,CDE ‐2017 Definitions Hispanic* Refers to persons of Spanish–Speaking origin or ancestry from Latin Americans, but excludes Brazilians. Latino* Refers to persons of Latin American origin or ancestry ,including Brazilians, but excludes persons from Spain. -

Breakfast Lunch Lunch Lunch Breakfast Lunch Breakfast Lunch

Breakfast Breakfast Breakfast Breakfast Breakfast Cook at Home Cook at Home Reduced Sugar Fruit Loops Breaded Chicken Biscuit Reduced Sugar Frosted Flakes Sausage Biscuit Breakfast Pizza Breakfast Breakfast Graham Crackers Apple Juice Biscuit Apple Juice Orange Tangerine Juice French Toast Sticks * Reduced Sugar Cinnamon Toast Crunch Mandarin Oranges Mixed Fruit Juice Diced Apricot Red Delicious Apple Orange Tangerine Fruit Juice Syrup Graham Crackers Fresh Banana Fresh Gala Apple Mixed Fruit Juice Apple Juice Lunch Lunch Lunch Lunch Lunch Cheeseburger Diced Apricots Red Delicious Apple Chicken Chunks with Roll Roasted Wings Grilled Cheese * Beef Hot Dog Or or Cucumber and Tomato Salad Lunch Carrot Sticks (9) Or Chicken Strip Salad Lunch Ranch Dressing Fruit & Yogurt Plate V Celery Sticks (5) Mixed Cheese Chef Salad Breaded Beef * with Bun Chicken Tenders * Diced Apricots Pretzels Lettuce/Tomato/Pickels Coleslaw Coleslaw Roll Apple Juice Tossed Salad Diced Pears Whoel Kernel Corn VBlend Juice Baked Beans Summer Corn Salad Shortbread Cookies Roasted Carrots Mixed Berry Juice Ranch Dressing Cinnamon Applesauce Ranch Dressing Applesauce Mini Carrots/Ranch Assorted Juice Fruit Cocktail Fruit Punch Juice Applesauce Mixed Berry Juice Fruit Cocktail Fruit Punch Juice Mixed Berry Juice Meatless Monday Breakfast Breakfast Breakfast Breakfast Cook at Home Cook at Home Breakfast Turkey Sausage Biscuit Reduced Sugar Frosted Flakes Chicken Biscuit Pancake N Link Breakfast Breakfast Apple Juice Mixed Fruit Juice Reduced Sugar Fruit Loops Graham Gold -

New Zealand Culinary Tour 8 Days

New Zealand Culinary Tour 8 days Tour Description The stunning natural scenery and exciting food scene draw visitors to New Zealand each year. With a primarily agricultural economy, the country has become well-known for its fresh ingredient based cuisine. Locals and visitors alike savor seafood recipes and plentiful lamb, as well as a variety of vegetable dishes. The wines produced in the country are recognized as some of the best in the world. Sample New Zealand’s bounty while learning about the agricultural methods and preparation processes all while surrounded by attractive landscapes. Highlights Auckland City Tour Explore the Glowworm Grotto at the Waitomo Caves Five specialty lunches and five winery visits Visit a Maori village Experience a geothermal site in Rotorua Fruit orchard visit and tasting Art Deco city tour in Napier Olive grove visit with tasting Marlborough Sounds cruise with mussel farm visit Farewell dinner with behind the scenes visit to an award winning restaurant kitchen Sample Tour Itinerary Auckland – 1 night Day 1: Arrive Auckland At the Auckland airport you will be greeted and escorted to your private coach for a sightseeing tour of Auckland. Auckland is situated on the narrow isthmus between the Tasman Sea and the Pacific Ocean and is noted for its extensive parks and beautiful gardens. Unique to this city are a large number of extinct volcanic cones thrusting sharply upward out of a sea of houses. Your tour includes a visit to the Auckland War Memorial Museum for a visit to its unique Maori Court. After free time to grab a bite to eat and shop, you’ll be taken to a special wine tasting experience featuring the many wine regions of New Zealand. -

Breakfast Chef Job Brief

BREAKFAST CHEF JOB BRIEF BREAKFAST CHEF HIGHLY COMPETITIVE RENUMERATION ARE YOU A BREAKFAST CHEF WITH REAL AMBITION? • Outstanding remuneration depending on experience • Additional reward based on your performance • Excellent work-life balance through flexible hours • Free meals on shift and 30% discount at other times • Training and development to build your career • Real opportunity to progress within a young business • State of art kitchen and equipment (e.g. Rational oven, Induction plate) • Holiday and sick pay enhanced with service We need an ambitious BREAKFAST CHEF with previous experience to help us establish our remarkable new FRESH FOOD DESTINATION that reinterprets and redefines the hospitable essence of the original English COFFEE HOUSE where society of every sort felt welcome. THE FIND will produce an incredible selection of authentic, locally-sourced food, all attentively prepared in a state of the art kitchen - and served in wonderfully eclectic surrounding that give classic Regency elegance and comfort an entertaining modern twist. We will also serve the very finest artisan coffees and teas. To realise our extraordinary vision we are seeking an ambitious BREAKFAST CHEF who can help us build the business and ensure it will surprise and delight our audience of discerning customers – many of whom are eagerly anticipating our launch. We will consider both highly experienced candidates with well-proven sourcing, culinary and people skills, as well as less experienced candidates with the drive and potential to step up to this essential supportive role. If, having read the job description, you would like to apply for this position, please submit your details and CV via the recruitment page on our website. -

Breakfast Menu Served 8:00Am – 11:00Am

BREAKFAST MENU SERVED 8:00AM – 11:00AM THE “BIG BREAKFAST”* 12.99 DUTCHMAN BREAKFAST BURRITO 9.99 Three eggs any style, bacon and sausage, breakfast Large flour tortilla filled with scrambled eggs, potatoes, biscuit and gravy sausage, bacon, bell peppers, onions, cheddar cheese, homemade salsa, served with breakfast potatoes AMERICAN BREAKFAST* 9.99 MIGAS 9.99 Two eggs any style, your choice of bacon or sausage, Scrambled eggs, tortilla strips, pico de gallo, bacon, breakfast potatoes, toast or buttermilk biscuit bell peppers, cheddar cheese, ranchero salsa EGGS BENEDICT* 10.99 HUEVOS RANCHEROS* 9.99 Two poached eggs over Canadian bacon on an Two eggs sunny side up served on flour tortillas, English muffin with hollandaise sauce, served with bacon, cheddar cheese, ranchero salsa, served with breakfast potatoes breakfast potatoes OMELETS Served with Breakfast Potatoes and Toast or a Buttermilk Biscuit KEMAH 10.99 EL RANCHERO 10.99 Bacon, sausage, bell peppers, onions, tomatoes, Chorizo, bell peppers, onions, jack cheese, cheddar cheese pico de gallo, ranchero salsa CRAB AND SHRIMP 12.99 VEGGIE 9.99 Blackened lump crab, gulf shrimp, bell peppers, onions, Bell peppers, onions, mushrooms, tomatoes jack cheese FROM THE GRIDDLE OLD FASHIONED BELGIAN BISCUITS & GRAVY 8.99 PANCAKES (3) 8.99 WAFFLE 8.99 Two large buttermilk biscuits with our Served with whipped butter and hot Served with whipped butter, seasonal homemade sausage gravy maple syrup (add seasonal fruit $.99) fruit and hot maple syrup (add a side of sausage $1.99) SIDES STEEL CUT OATMEAL 5.99 BACON (3) 2.99 MIMOSA 6 (add fresh fruit .99) Sparkling champagne & fresh squeezed orange juice SEASONAL FRUIT SAUSAGE PATTIES (2) 1.99 Bowl 5.99 Cup 1.99 WHITE, WHEAT OR 1 EGG (ANY STYLE)* 1.49 BLOODY MARY 6 MULTIGRAIN TOAST 1.49 Vodka & zing zang bloody mary mix BUTTERMILK BISCUIT .99 BREAKFAST POTATOES 1.99 A suggested gratuity of 15% - 20% is customary.