Auditor General of Pakistan Table of Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Details Is As Under

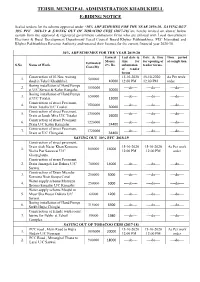

TEHSIL MUNICIPAL ADMINISTRATION KHADUKHELL E-BIDING NOTICE Sealed tenders for the scheme approved under “30% ADP SCHEMES FOR THE YEAR 2019-20, SAVING OUT 30% PFC 2018-19 & SAVING OUT OF TOBACOO CESS (2017-18)”are hereby invited on above/ below system from the approved & registered government contractors/ firms who are enlisted with Local Government Elections & Rural Development Department/ Local Council Board Khyber Pakhtunkhwa, PEC Islamabad and Khyber Pakhtunkhwa Revenue Authority and renewed their licenses for the current financial year 2020-10. 30% ADP SCHEMES FOR THE YEAR 2019-20 Earnest Last date & Date & time Time period Money time for for opening of of completion. Estimated S.No Name of Work. 2% Rs. submission tender forms. Cost.(M) of tender forms Construction of 03 Nos. waiting 15-10-2020 15-10-2020 As Per work 1. 500000 shed in Tehsil Khadukhel. 10000 12:00 PM 12:00 PM order Boring installation of Hand Pumps 2. 1500000 ----do---- ----do---- ----do---- at U/C Sarwai & Kalan Kangalai. 30000 Boring installation of Hand Pumps 3. 650000 ----do---- ----do---- ----do---- at U/C Totalai. 13000 Construction of street Pavement, 4. 1500000 ----do---- ----do---- ----do---- Drain Totalia U/C Totalai. 30000 Construction of street Pavement, 5. 1300000 ----do---- ----do---- ----do---- Drain at Janak Mira U/C Totalai 26000 Construction of street Pavement, 6. 1220000 ----do---- ----do---- ----do---- Drain U/C Kalan Kamgalai 24400 Construction of street Pavement, 7. 1720000 ----do---- ----do---- ----do---- Drain at U/C Chingalai. 34400 SAVING OUT 30% PFC 2018-19 Construction of street pavement, Drain shah Nazar Khan Koroona 15-10-2020 15-10-2020 As Per work 1. -

Khyber Pakhtunkhwa Current Rain Spell (31082020 to 04092020 at 11:00 Pm)

PDMA PROVINCIAL DISASTER MANAGEMENT AUTHORITY Provincial Emergency Operation Center Civil Secretariat, Peshawar, Khyber Pakhtunkhwa Phone: (091) 9212059, 9213845, Fax: (091) 9214025 www.pdma.gov.pk No. PDMA/PEOC/SR/2020/SepM125 Date: 04/09/2020 KHYBER PAKHTUNKHWA CURRENT RAIN SPELL (31082020 TO 04092020 AT 11:00 PM) INFRA/ HUMAN INCIDENTS NATURE OF CAUSE OF CATTLE DISTRICT HUMAN LOSSES/ INJURIES INFRASTRUCTURE DAMAGES INCIDENT INCIDENT PERISHED DEATH INJURED HOUSES SCHOOLS OTHERS Male Female Child Total Male Female Child Total Fully Partially Total Fully Partially Total Fully Partially Total House Collapse/Room Mardan Heavy Rain 0 0 0 0 4 4 1 9 0 0 6 6 0 0 0 0 0 0 Collapse Boundry Wall Collapse/Cattle Swabi Heavy Rain Shed/House 0 1 4 5 4 1 3 8 1 1 9 10 0 0 0 0 0 0 Collapse/Room Burnt/Room Collapse House Collapse/Room Charsadda Heavy Rain 0 0 0 0 0 0 1 1 0 0 2 2 0 0 0 0 0 0 Collapse Nowshera Heavy Rain House Collapse 0 0 0 0 0 0 0 0 0 0 11 11 0 0 0 0 0 0 Boundry Wall Collapse/Cattle Shed/House Buner Heavy Rain 0 2 3 5 0 1 2 3 5 6 121 127 0 0 0 0 0 0 Collapse/Roof Collapse/Room Collapse House Collapse/Room UpperChitral Heavy Rain 0 0 0 0 0 0 0 0 0 2 0 2 0 0 0 0 5 5 Collapse Malakand Heavy Rain House Collapse 0 0 0 0 0 0 0 0 0 0 14 14 0 0 0 0 0 0 Lower Dir Heavy Rain House Collapse 0 0 0 0 0 0 0 0 0 0 8 8 0 0 0 0 0 0 Boundry Wall Collapse/House Shangla Heavy Rain Collapse/Roof 1 0 3 4 0 4 2 6 12 2 40 42 0 0 0 0 2 2 Collapse/Room Collapse Boundry Wall Collapse/Flash Heavy Rain/Land Flood/Heavy Swat 7 2 2 11 5 0 4 9 0 3 27 30 0 0 -

Audit Report on the Accounts of District Government Buner

AUDIT REPORT ON THE ACCOUNTS OF DISTRICT GOVERNMENT BUNER AUDIT YEAR 2016-17 AUDITOR GENERAL OF PAKISTAN TABLE OF CONTENTS ABREVIATIONS AND ACRONYMS ii Preface………………………………………………………………………….iii EXECUTIVE SUMMARY ivv SUMMARY TABLES & CHARTS vii Table 1: Audit Work Statistics vii Table 2: Audit observations Classified by Categories……………………….. viii Table 3: Outcome Statistics………………………………………………….. viiii Table 4: Table of Irregularities pointed out…………………………………… ix Table 5: Cost Benefit Ratio ix CHAPTER-1 1 1.1District Government Buner 1 1.1.1 Introduction…………………………………………………………... 1 1.1.2 Comments on Budget and Accounts (Variance Analysis)………. 1 1.1.3 Comments on the status of compliance with ZAC / PAC Directives……….2 1.2 AUDIT PARAS 3 1.2.1 Non production of Record 3 1.2.2 Irregularities and Non Compliance 4 1.2.3 Internal Control Weaknesses 19 ANNEXURE 32 i ABBREVIATIONS AND ACRONYMS AP Advance Para AG Accountant General SDO Sub Divisional Officer BHUs Basic Health Units C&W Communication & Works CPWA Code Central Public Works Account Code CPWD Code Central Public Works Department Code DAC Departmental Accounts Committee DCO District Coordination Officer DHQ District Headquarter DO District Officer EMIS Education Management Information System EDO Executive District Officer GGPS Government Girl Primary School GFR General Financial Rules IPSAS International Public Sector Accounting Standards LGA Local Government Act MFDAC Memorandum for Departmental Accounts Committee PAC Public Accounts Committee PAO Principal Accounting Officer PHE Public Health Engineering XEN Executive Engineer ZAC Zilla Accounts Committee ii Preface Articles 169 &170 of the Constitution of the Islamic Republic of Pakistan, 1973 read with Sections-8 and 12 of the Auditor General’s (Functions, Powers and Terms and Conditions of Service) Ordinance, 2001 and Section-37 of Khyber Pakhtunkhwa Local Government Act 2013 require the Auditor General of Pakistan to conduct audit of the receipts and expenditure of District Fund and Public Account of District Governments. -

Contesting Candidates NA-1 Peshawar-I

Form-V: List of Contesting Candidates NA-1 Peshawar-I Serial No Name of contestng candidate in Address of contesting candidate Symbol Urdu Alphbeticl order Allotted 1 Sahibzada PO Ashrafia Colony, Mohala Afghan Cow Colony, Peshawar Akram Khan 2 H # 3/2, Mohala Raza Shah Shaheed Road, Lantern Bilour House, Peshawar Alhaj Ghulam Ahmad Bilour 3 Shangar PO Bara, Tehsil Bara, Khyber Agency, Kite Presented at Moh. Gul Abad, Bazid Khel, PO Bashir Ahmad Afridi Badh Ber, Distt Peshawar 4 Shaheen Muslim Town, Peshawar Suitcase Pir Abdur Rehman 5 Karim Pura, H # 282-B/20, St 2, Sheikhabad 2, Chiragh Peshawar (Lamp) Jan Alam Khan Paracha 6 H # 1960, Mohala Usman Street Warsak Road, Book Peshawar Haji Shah Nawaz 7 Fazal Haq Baba Yakatoot, PO Chowk Yadgar, H Ladder !"#$%&'() # 1413, Peshawar Hazrat Muhammad alias Babo Maavia 8 Outside Lahore Gate PO Karim Pura, Peshawar BUS *!+,.-/01!234 Khalid Tanveer Rohela Advocate 9 Inside Yakatoot, PO Chowk Yadgar, H # 1371, Key 5 67'8 Peshawar Syed Muhammad Sibtain Taj Agha 10 H # 070, Mohala Afghan Colony, Peshawar Scale 9 Shabir Ahmad Khan 11 Chamkani, Gulbahar Colony 2, Peshawar Umbrella :;< Tariq Saeed 12 Rehman Housing Society, Warsak Road, Fist 8= Kababiyan, Peshawar Amir Syed Monday, April 22, 2013 6:00:18 PM Contesting candidates Page 1 of 176 13 Outside Lahori Gate, Gulbahar Road, H # 245, Tap >?@A= Mohala Sheikh Abad 1, Peshawar Aamir Shehzad Hashmi 14 2 Zaman Park Zaman, Lahore Bat B Imran Khan 15 Shadman Colony # 3, Panal House, PO Warsad Tiger CDE' Road, Peshawar Muhammad Afzal Khan Panyala 16 House # 70/B, Street 2,Gulbahar#1,PO Arrow FGH!I' Gulbahar, Peshawar Muhammad Zulfiqar Afghani 17 Inside Asiya Gate, Moh. -

District Buner Adp 2020-21

Project Description Budget BD15D00166-check 10 BD15D00370-Pipe Water Channel UC Gulbandi 330,000 BD15D00371-WSS at UC Gulbandai 635,358 BD15D00389-Pressure Pump/Hand pump Nawagai-1 Hujra 111Akazai 213,032 BD15D00390-Pressure Pump/Hand pump Nawagai-2Bolagat 118,078 BD15D00391-Pressure Pump/Hand pump Nawagai-2 RahmatSaid 284,885 BD15D00392-Pressure Pump/Hand pump Nawagai-1 380,724 BD15D00393-Pressure Pump/Hand pump Makhranai Dandmaira Nasib 215,937 BD15D00394-Pressure Pump/Hand pump sora 257,749 BD15D00407-RAHIM PATAY ROAD 0 BD15D00409-"PRESSURE PUMP/HAND PUMP,WASH ROOM &REPAIR OF ROAD IN DISPENSORY AT CHANGLAI" 0 BD15D00430-WSS AT SOLAI CHUM & SANITATION AT KANDAWMASJED & RAHMAT KOROONA VC ELAI-1 173,000 BD15D00436-REPAIR OF BHU GAGRA 0 BD15D00469-CONSTRUCTION OF BOUNDRY WALL AT TOTYANOKALAY JANAZGAH 100,000 BD15D00472-INTEZARGAH AT NOREZE (AZMAT BIBI) 670,000 BD15D00474-INSTALLATION OF SOLAR ENRGY SYSTEM ANDHAND PUMP AT GMS SHARGHASHI BATAI 163,227 BD15D00475-INSTALLATION OF SOLAR ENRGY SYSTEM ANDHAND PUMP AT GHS BATAI 0 BD15D00477-REPAIR AND MAINTENANCE OF TEHSIL HEADQUARTER HOSPITAL 1,710,928 BD15D00486-INSTALLATION OF SOLAR SYSTEM IN GHSSAWARAI 0 BD15D00496-PCC PATHWAY ROAD GHS INZAR MIRA 140,712 BD15D00505-"HAND PUMPS AT MOHALLA SARGANTAL,MUGHALBARKHAN & MOMIN USTAD WARD TORWARSAK" 49,596 BD15D00513-REPAIR AND MAINTANANCE/ SOLAR SYSTEMGGmS GADEZI 894,157 BD15D00520-Pressure Pump at GHS Khanano Dherai 127,636 BD15D00521-Hand Pump at GHS Jangai & GGHS Kadal 500,000 BD15D00541-Protection Wall Khananu Dherai Wand UCMakhranai 330,000 BD16D00030-WSS -

Auditor General of Pakistan

AUDIT REPORT ON THE ACCOUNTS OF LOCAL GOVERNMENTS DISTRICT BUNER AUDIT YEAR 2018-19 AUDITOR GENERAL OF PAKISTAN TABLE OF CONTENTS ABBREVIATIONS AND ACRONYMS ................................................................................................................................................ I PREFACE ............................................................................................................................................................................................. II EXECUTIVE SUMMARY ................................................................................................................................................................... III SUMMARY TABLES & CHARTS .................................................................................................................................................... VII I: AUDIT WORK STATISTICS ......................................................................................................................................................... VII II: AUDIT OBSERVATIONS CLASSIFIED BY CATEGORIES ..................................................................................................... VII III: OUTCOME STATISTICS ........................................................................................................................................................... VIII IV: TABLE OF IRREGULARITIES POINTED OUT ........................................................................................................................ IX V: COST -

Puma Energy Pakistan (Private) Limited

11 Puma Energy Pakistan (Private) Limited Pumps Retail Prices of HSD and PMG Effective from 01st August, 2021 Pump Price Rs / Liter S.No Customer Name Address City HSD PMG 1 A. K. MANN PETROLEUM Chak # 112/7R, T. T. Singh-Burewala Road Toba Taik Singh 117.58 120.80 2 A.A ENTERPRISES SHAHPUR JAHANIAN TEHSIL MORO DISTRICT Daulatpur 117.05 120.29 3 A.Q MALIKANI PETROLEUM SERVICES Survey No.32 Deh Sattar Dino Shah,Tapo Mullan Dist Thatta 117.75 120.96 4 A.S PETROLEUM SERVICE Mouza Naroki Majaha, Pattoki-Changa Manga Road Pattoki 117.48 120.70 At Aray Wala Mouza Pakki (Near Qasba Shah Sadar Din)KM 26/27 From Dera Gazi Khan, Tunsaroad Indus 5 AADIL PETROLEUM SERVICES Dera Ghazi Khan 117.05 120.29 N-55 6 ABBAS FILLING STATION Block # 165/3 & 4, Sub #3A-3B-4A & 4B, Deh 86Nasrat Main Sanghar Road Nawabshah 117.05 120.29 7 ABBAS PETROLEUM STATION Kharian Dinga Road Noonan Wali Distt GujratNoonan Wali Noonan Wali - Gujrat 117.05 120.29 8 Abbasi Trucking Station Moro Servery No. 475, Situated in Deh Moro & Taluka Mo Moro 117.05 120.29 9 ABBASIA FILLING STATION Taluka Gularchi Plot No.A3 Khi Road, Shaheed Fazil Badin 117.93 121.12 10 ABDUL RAFAY PETROLEUM Mouza Kotla Qasim Khan Dinga Road, Tehsil Lala Mou Gujrat 117.05 120.29 11 ABDUL SATTAR PETROLEUM SERVICE Mouza Manga Ottar, (Near Honda Factory), on Nationon National Highway (N-5) (South Bond) Lahore 117.24 120.48 12 ABDULLAH PETROLEUM Chak Beli Khan / Rawalpindi Road, Tehsil & Distt Rawalpindi Rawal Pindi 117.05 120.29 13 ABDULLAH PETROLEUM STATION- GUJRAT Mouza Ganja B/W KM 8/9 From Lala Mopuza On NoonwalOn Noonwali-Ganja-Lala Mouza Road Gujrat 117.05 120.29 14 ABDULLAH PETROLEUM SERVICE Petrol Pump Baloch AJK, Baloch Sadhnoti AJK 117.48 120.70 15 ABID CNG STATION & PETROLEUM SERVICES On Jalal Pur Pirwala Road At Mouza KhaipurOpposite Al-Shamas At Shujanad Multan 117.16 120.40 16 ADIL FILLING STATION Survey No. -

Khyber Pakhtunkhwa FATA Punjab a JK Islamabad FA NA Disputed Area

Pakistan: Deployment of mobile and static clinics in Khyber Pakhtunkhwa Province as on august 4, 2010 Services of mobile clinics deployed on the KPK province Comp. PHC Referral Provision of Basic Basic Comp Nutrition Kalam Organisation Name District Tehsil Union Council ANC PNC IMNCI Services Services Medicines Lab EmONC EmONC Surveillance FANA A Bahrain Yes Yes Yes Yes Yes Yes N Care International Sw at Bahrain Tirat Yes Yes Yes Yes Yes Yes Disputed Area l Bahrain a FATA Khyber Pakhtunkhwa A Amazai Yes Yes Yes Yes Yes Yes ky an F B M Kaw ga Yes Yes Yes Yes Yes Yes ah r Punjab ain Makhranai Yes Yes Yes Yes Yes Yes Naw agai Yes Yes Yes Yes Yes Yes Gowalairaj Balochistan Ellai Yes Yes Yes Yes Yes Yes Tirat Buner Chamla Tehsil Krapa Yes Yes Yes Yes Yes Yes Bar Thana Sind Bahrain Mankyal Yes Yes Yes Yes Yes Khwazakhela Matta Sebujni Bar Thana Yes Yes Yes Yes Yes Yes Matta Khararai Shin Gow alairaj Yes Yes Yes Yes Yes Yes Swat Kotanai Dherai Yes Yes Shahpur IDEA Sw at Matta Sebujni Malik Khel Yes Yes Jano/chamtalai Concern Worldw ide Kohat Kohat Tehsil Sher Kot Yes Yes Yes Yes Yes Khawazakhela rai Buner Daggar Tehsil Daggar Kabal Charbagh Dhe Dhoda Malik Khel Kohat Kohat Tehsil Urban-4 Shangla Jano/chamtalai Babuzai Khaw azakhela Kotanai Yes Barikot Sori Chagharzai Sw at Khw azakhela Shin Gul Bandai Jarma Yes Yes Yes Yes Yes Yes Yes r a Handicap International Kohat Kohat Tehsil Lachi Rural Yes Yes Yes Yes Yes Yes Yes g g a Batara Batara Yes Yes Yes Yes Yes Yes D ai Ell Gul Bandai Yes Yes Yes Yes Yes Yes Buner Merlin Buner Chagharzai Tehsil -

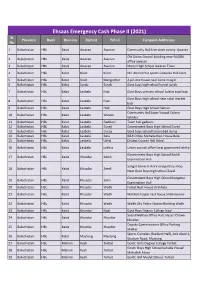

UPDATED CAMPSITES LIST for EECP PHASE-2.Xlsx

Ehsaas Emergency Cash Phase II (2021) Sr. Province Bank Division Distrcit Tehsil Campsite Addresses No. 1 Balochistan HBL Kalat Awaran Awaran Community Hall Live stock colony Awaran Old Union Council building near NADRA 2 Balochistan HBL Kalat Awaran Awaran office awaran 3 Balochistan HBL Kalat Awaran Awaran Model High School Awaran Town 4 Balochistan HBL Kalat Kalat Kalat Mir Ahmed Yar sports Complex Hall kalat 5 Balochistan HBL Kalat Kalat Mangochar A private house near Jame masjid 6 Balochistan HBL Kalat Surab Surab Govt boys high school hostel surab 7 Balochistan HBL Kalat Lasbela Hub Govt Boys primary school Adalat road hub Govt Boys high school near sabzi market 8 Balochistan HBL Kalat Lasbela Hub hub 9 Balochistan HBL Kalat Lasbela Hub Govt Boys High School Sakran Community Hall Jaam Yousuf Colony 10 Balochistan HBL Kalat Lasbela Winder Winder 11 Balochistan HBL Kalat Lasbela Gaddani Town hall gaddani 12 Balochistan HBL Kalat Lasbela Dureji Government Boys High School Dureji 13 Balochistan HBL Kalat Lasbela Dureji Govt boys school hasanabad dureji 14 Balochistan HBL Kalat Lasbela Bela B&R Office Mohalla Rest House Bela 15 Balochistan HBL Kalat Lasbela Uthal District Council Hall Uthal 16 Balochistan HBL Kalat Lasbela Lakhra Union council office local goverment lakhra Government Boys High School Karkh 17 Balochistan HBL Kalat Khuzdar Karkh Examination Hall Sangat General store and poltary shop 18 Balochistan HBL Kalat Khuzdar Zeedi Near Govt Boys high school Zeedi Government Boys High School Norgama 19 Balochistan HBL Kalat Khuzdar Zehri Examination Hall 20 Balochistan HBL Kalat Khuzdar Wadh Forest Rest House Drakhala 21 Balochistan HBL Kalat Khuzdar Wadh Mohbat Faqeer rest house Shahnoorani 22 Balochistan HBL Kalat Khuzdar Wadh Wadh City Police Station Building Wadh 23 Balochistan HBL Kalat Khuzdar Naal Govt Boys Degree College Naal Social Welfare Office Hall, Hazari Chowk 24 Balochistan HBL Kalat Khuzdar Khuzdar khuzdar. -

Ehsaas Emergency Cash Payments

Consolidated List of Campsites and Bank Branches for Ehsaas Emergency Cash Payments Campsites Ehsaas Emergency Cash List of campsites for biometrically enabled payments in all 4 provinces including GB, AJK and Islamabad AZAD JAMMU & KASHMIR SR# District Name Tehsil Campsite 1 Bagh Bagh Boys High School Bagh 2 Bagh Bagh Boys High School Bagh 3 Bagh Bagh Boys inter college Rera Dhulli Bagh 4 Bagh Harighal BISP Tehsil Office Harigal 5 Bagh Dhirkot Boys Degree College Dhirkot 6 Bagh Dhirkot Boys Degree College Dhirkot 7 Hattain Hattian Girls Degree Collage Hattain 8 Hattain Hattian Boys High School Chakothi 9 Hattain Chakar Boys Middle School Chakar 10 Hattain Leepa Girls Degree Collage Leepa (Nakot) 11 Haveli Kahuta Boys Degree Collage Kahutta 12 Haveli Kahuta Boys Degree Collage Kahutta 13 Haveli Khurshidabad Boys Inter Collage Khurshidabad 14 Kotli Kotli Govt. Boys Post Graduate College Kotli 15 Kotli Kotli Inter Science College Gulhar 16 Kotli Kotli Govt. Girls High School No. 02 Kotli 17 Kotli Kotli Boys Pilot High School Kotli 18 Kotli Kotli Govt. Boys Middle School Tatta Pani 19 Kotli Sehnsa Govt. Girls High School Sehnsa 20 Kotli Sehnsa Govt. Boys High School Sehnsa 21 Kotli Fatehpur Thakyala Govt. Boys Degree College Fatehpur Thakyala 22 Kotli Fatehpur Thakyala Local Govt. Office 23 Kotli Charhoi Govt. Boys High School Charhoi 24 Kotli Charhoi Govt. Boys Middle School Gulpur 25 Kotli Charhoi Govt. Boys Higher Secondary School Rajdhani 26 Kotli Charhoi Govt. Boys High School Naar 27 Kotli Khuiratta Govt. Boys High School Khuiratta 28 Kotli Khuiratta Govt. Girls High School Khuiratta 29 Bhimber Bhimber Govt. -

BD15D00305-Hands Pumps/Pressure Pumps At

DISTRICT Project Description BE 2018-19 BUNER BD15D00305-Hands Pumps/Pressure Pumps at wardShalbandi 6,000,000 BUNER BD15D00315-Protection wall at Ward Norizai 329,800 BUNER BD15D00345-Protection wall at Sarvai 330,000 BUNER BD15D00369-WSS at UC Gulbandai 97,892 BUNER BD15D00370-Water Tank for rain water storage 330,000 BUNER BD15D00371-WSS at UC Gulbandai 1,574,000 BUNER BD15D00373-"Rehabilitation of WSS in UC Abakhel,Soray & Petaw bazargay." 149,085 BUNER BD15D00377-Pressure Pumps Malak Pur Mera Mosque 300,000 BUNER BD15D00379-Pressure Pumps & Hand Pumps at Gagra 148,570 BUNER BD15D00384-Pressure Pump/Hand Pumps (3 Nos:) at UCRega 185,233 BUNER BD15D00386-Pressure Pump/Hand Pumps at Ward 27 UCKarapa 82,766 BUNER BD15D00401-PCC ROAD GMS MANDAW 1,320,000 BUNER BD15D00407-RAHIM PATAY ROAD 500,000 BUNER BD15D00409-"PRESSURE PUMP/HAND PUMP,WASH ROOM &REPAIR OF ROAD IN 660,000 DISPENSORY AT CHANGLAI" BUNER BD15D00413-REPAIR OF BHU BAGRA 660,000 BUNER BD15D00430-WSS AT SOLAI CHUM & SANITATION AT KANDAWMASJED & RAHMAT 659,000 KOROONA VC ELAI-1 BUNER BD15D00436-REPAIR OF BHU GAGRA 1,160,000 BUNER BD15D00448-"CONSTRUCTION OF KACHA ROAD TO GMS ,GPSAND GHS GUMBAT " - BUNER BD15D00465-WATER TANK & PIPE SCHEME AT GERARAI 333,000 BUNER BD15D00469-CONSTRUCTION OF BOUNDRY WALL AT TOTYANOKALAY JANAZGAH 100,000 BUNER BD15D00471-INSTALLATION OF HAND PUMP IN GGHS CHEENA 149,000 BUNER BD15D00472-INTEZARGAH AT NOREZE (AZMAT BIBI) 670,000 BUNER BD15D00474-INSTALLATION OF SOLAR ENRGY SYSTEM ANDHAND PUMP AT GMS 550,000 SHARGHASHI BATAI BUNER BD15D00475-INSTALLATION -

NOTICE INVITING E-BIDDING PHE Division Buner Government Of

OFFICE OF THE EXECUTIVE ENGINEER PUBLIC HEALTH ENGINEERING DIVISION BUNER Tele/Fax # 0939-510017 NOTICE INVITING E-BIDDING PHE Division Buner Government of Khyber Pakhtunkhwa invites Electronic Bids from the Eligible Firms/Contractors having specialization code CE-09 in light of rule 6 (2)(a) “Single Stage, One Envelop” procedures of Khyber Pakhtunkhwa Public Procurement Regulatory Authority (KPPRA) rules 2014, registered with income/sales tax, reflected on active taxpayer list of FBR, for the following works. Earnest Money Estimated Cost S No. Name of Work with Stamp (Rs. in Million) Duty (Rs.) “CONSTRUCTION OF WATER SUPPLY & SANITATION SCHEMES AT UCs MALAKPUR, PACHA KALAY, BATAI, ABAKHEL, MALIKHEL, GADEZAI, DAGGAR, GOKAN, ELAI ANGHAPOR & TORWARSAK DISTRICT BUNER” ADP # 280/200235 (2020-21) 01. Water Supply Scheme Landay PK-20, District Buner. 7.647 (M) 0.172 (M) 02. Water Supply Scheme Ashizo Maira 6.409 (M) 0.147 (M) 03. Water Supply Scheme Char Kalay 7.018 (M) 0.160 (M) 04. Water Supply Scheme Zaga UC Daggar 1.300 (M) 0.033 (M) 05. Water Supply Scheme Khwara UC Gadezi 3.609 (M) 0.0785 (M) 06. Water Supply Scheme Shodara UC Gokand 2.500 (M) 0.0563 (M) 07. Water Supply Scheme Sakhko Kass UC Abakhel 4.600 (M) 0.0983 (M) 08. Water Supply Scheme Qadarnagar Dara & Surrounding 0.900 (M) 0.0193 (M) 09. Water Supply Scheme Khail UC Daggar 1.200 (M) 0.0303 (M) 10. Water Supply Scheme Chor Banda UC Abakhel 1.500 (M) 0.0363 (M) 11. Water Supply Scheme Jower 5.523 (M) 0.1293 (M) 12.