IMPORTANT NOTICE This Prospectus Is Being Displayed on the Website to Make the Prospectus Accessible to More Investors. the Phil

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download File

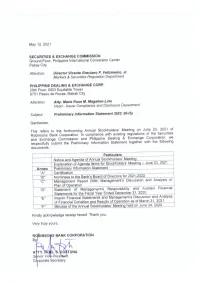

C O V E R S H E E T for AUDITED FINANCIAL STATEMENTS SEC Registration Number 2 9 3 1 6 C O M P A N Y N A M E R O B I N S ON S BANK CORPORATI ON AND SUBSI D I ARY PRINCIPAL OFFICE ( No. / Street / Barangay / City / Town / Province ) 1 7 t h Fl o o r , G a l l e r i a Co r p o r a t e Ce n t e r , EDSA c o r n e r O r t i g a s A v e n u e , Qu e z o n Ci t y Form Type Department requiring the report Secondary License Type, If Applicable 1 7 - A C O M P A N Y I N F O R M A T I O N Company’s Email Address Company’s Telephone Number Mobile Number www.robinsonsbank.com.ph 702-9500 N/A No. of Stockholders Annual Meeting (Month / Day) Fiscal Year (Month / Day) 15 Last week of April December 31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number Ms. Irma D. Velasco [email protected] 702-9515 09988403139 CONTACT PERSON’s ADDRESS 17th Floor, Galleria Corporate Center, EDSA corner Ortigas Avenue, Quezon City NOTE 1 : In case of death, resignation or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. -

Participating Robinsons Supermarket Branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST

Participating Robinsons Supermarket branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST. NOAH'S ARC BLDG. BF HOMES PARANAQUE CITY ROBINSONS EASYMART ALIMA BAY ALIMA BAY RESIDENCES AND COMMERCIAL COMPLEX IN GEN. EVANGELISTA ST. BRGY. ALIMA BACOOR CAVITE ROBINSONS EASYMART ANTIPOLO ROBINSONS EASYMART ANTIPOLO RODRIGUEZ ROAD BARANGAY SITIO PARUGAN SAN JOSE ANTIPOLO CITY ROBINSONS EASYMART ARNAIZ ARNAIZ AVENUE, LIBERTAD PASAY CITY PASAY 1300 ROBINSONS EASYMART E RODRIGUEZ SR 340 E. RODRIGUEZ SR. AVE COR. CORDILLERA ST. BRGY. DON MANUEL, QC ROBINSONS EASYMART FILINVEST BATASAN FILINVEST II GATE B SAN MATEO ROAD-BATASAN HILLS QUEZON HILLS CITY ROBINSONS EASYMART GREENGATE IMUS PHASE 3 GREEN GATE SUBDV. MALAGASANG 2A IMUS CAVITE ROBINSONS EASYMART KAMUNING #89 K1ST BARANGAY KAMUNING QUEZON CITY ROBINSONS EASYMART LAGRO SUNBEST BLDG. ASCENSION AVENUE BRGY. GREATER LAGRO, QUEZON CITY ROBINSONS EASYMART LOYOLA HEIGHTS #88 ROSA ALVERO ST. LOYOLA HEIGHTS QUEZON CITY ROBINSONS EASYMART MARILAO GROUND FLOOR OF CINDY SQUARE IN MC ARTHUR HIGHWAY, ABANGAN,NORTE,MARILAO BULACAN ROBINSONS EASYMART MARIPOSA ARCADE G/F MARIPOSA ARCADE A. MABINI ST. KAPASIGAN PASIG CITY ROBINSONS EASYMART MOONWALK LP G/F SAVER'S BUILDUING ALABANG ZAPOTE ROAD TALON 1 MOONWALK LAS PINAS CITY ROBINSONS EASYMART PILILIA RIZAL J.P. RIZAL STREET, BRGY. IMATONG, PILILLA, RIZAL ROBINSONS EASYMART POBLACION 888 SAN IGNACIO ST., BRGY. POBLACION I, SAN JOSE DEL MONTE BULACAN 3023 PHILIPPINES ROBINSONS EASYMART PROJECT 6 #54 EMERALD COURT BLDG. ROAD 8, PROJECT 6, QUEZON CITY ROBINSONS EASYMART SAN AGUSTIN-TANZA SAN AGUSTIN COR SAN FRANCISCO ST POBLACION 2 TANZA CAVITE 4108 PHILIPPINES ROBINSONS EASYMART SAN MATEO KAMBAL ROAD BRGY.GITNANG BAYAN 1 SAN MATEO, RIZAL ROBINSONS EASYMART SAVERS ROOSEVELT 192 SAVERS APPLIANCE DEPOT ROOSEVELT AVE. -

NEOPOLITAN CONDOMINIUMS TOWER 3 Residential Condominium the New Project from Sta

NEOPOLITAN CONDOMINIUMS TOWER 3 residential condominium The new project from Sta. Lucia Land, Inc. is an eight-storey residential development with a total of 138 units. NEOPOLITAN CONDOMINIUMS TOWER 3 PROJECT LOCATION Neopolitan Condominiums Tower 3 is located within Neopolitan Business Park, along Mindanao and Regalado Avenues in Fairview, Quezon City. With its own development plans of becoming a hub for residential and office condominiums, townhouses, business process outsourcing offices, restaurants, state-of-the art hospital facility, and other points of interest, NEOPOLITAN BUSINESS PARK is clearly set to be an exciting landmark for local and foreign investors alike. To further match this promising development comes the opening of the MRT-7 line that will pass very near the complex. Quezon Memorial Tandang Doña Mindanao Sacred San Jose Circle sora Batasan Carmen Ave Heart del Monte North University Don Manggahan Regalado Quirino Tala Ave Ave Antonio NEOPOLITAN TOWER 1 SGN TOWER 2 SITE DEVELOMENT PLAN NEOPOLITAN CONDOMINIUMS TOWER 3 NEOPOLITAN TOWER 3 *The content of this material does not form any part of an offer or contract, nor shall any contract be made based on the content WHY QUEZON CITY It's nearby UP-Ayala Land Techno The Commonwealth Hospital and Hub, 22 MINS AWAY Medical Center is only 5 MINS WAY – home to several multinational companies that can be accessed via Commonwealth Avenue. QC also houses the country's major broadcasting networks such as ABS- CBN and GMA Networks. Educational institutions such as UP-Diliman, and Ateneo de Manila University 30-40 MINS AWAY WHY FAIRVIEW, QUEZON CITY SAN JOSE DEL MONTE N VALENZUELA CITY RODRIGUEZ & CALOOCAN W E SAN MATEO MANILA MARIKINA & PASIG S SAN JUAN & MANDALUYONG WHYWHY FAIRVIEW,FAIRVIEW QUEZON CITY CLOSE TO NATURE Fairview is near the La Mesa Dam and Reservoir, a 27-kilometer earth dam and protected area that contains the last remaining rainforest in Metro Manila. -

ROBINSONS BANK CORPORATION List of Branches As of August 2020

ROBINSONS BANK CORPORATION List of Branches as of August 2020 NO. BRANCH NAME ADDRESS 1 ACACIA LANE - SHAW BLVD. G/F Padilla Bldg. 333 Shaw Boulevard, Brgy. Bagong Silang, Mandaluyong City 2 ADRIACTICO [PADRE RADA] G/F Robinsons Place Manila, Adriatico Street, Ermita, Manila City G/F Unit 4, El Molito Commercial Complex, Madrigal Avenue cor Alabang-Zapote Road, Alabang, 3 ALABANG Muntinlupa City 4 ANGELES Level 1 Robinsons Place Angeles, McArthur Highway, Balibago, Angeles City, Pampanga Unit 169-A, Robinsons Place Antipolo, Sumulong Highway/Circumference Avenue, Dela Paz, 5 ANTIPOLO Antipolo City 6 ANTIQUE Level 1-116, 117 & 118 Robinsons Place Antique, Brgy. Maybato, San Jose de Buenavista, Antique Unit 7A Commercial Space, The Beacon Makati, A. Arnaiz Avenue corner Chino Roces Ave, Makati 7 ARNAIZ AVE City G/F Don Norberto & Doña Salustiana Ty Building, #403 Asuncion Street corner San Nicolas Street, 8 ASUNCION BINONDO Binondo, Manila 9 AYALA 6780 G/F JAKA 1 Building, Ayala Avenue, Makati City 10 BACOLOD CAPITOL R. PERFORMANCE Building A 62-64 Narra Avenue, Capitol Shopping Center, Bacolod City Level 1 C2002, The Central Citywalk, Robinsons Place Bacolod, Lacson Street, Mandalagan, 11 BACOLOD CITY Bacolod City, Negros Occidental 12 BACOOR Units 1 & 2, Apollo Mart Building, #369 Gen. Aguinaldo Highway, Talaba 4, Bacoor, Cavite 13 BACOOR MOLINO BLVD. G/F Main Square Bacoor, Molino Boulevard, Bacoor City, Cavite 14 BAGUIO G/F, ECCO/EDGARDOMCO REALTY CORP. Bldg., #43 Assumption Road, Baguio City 15 BAIS Corner Quezon and Burgos Streets, Bais City, Negros Oriental 16 BALAGTAS G/F 103-1 Balagtas Town Center, McArthur Highway, Borol 1st, Balagtas, Bulacan 17 BALANGA G/F, R & R Building, Don Manuel Banzon Avenue, Doña Francisca, Balanga City, Bataan 18 BALAYAN G/F Stalls Numbers 2, 3 & 4 Balayan Public Market, Plaza Mabini Street, Balayan Batangas 19 BANAWE (FORMERLY PASAY) Store No. -

Bayadcentername Address Area Ebiz - Bangued Alzate Building Mckinley St

BAYADCENTERNAME ADDRESS AREA EBIZ - BANGUED ALZATE BUILDING MCKINLEY ST. BANGUED ABRA Abra RCPI BANGUED PASTORAL BLDG., RIZAL ST., BANGUED Abra EBIZ - BUTUAN LT & SONS BLDG. BESIDE CROWN THEATER MONTILLA RD. Agusan del Norte RCPI BUTUAN 2 JC AQUINO ESPINA BLDG. JC AQUINO AVE. BUTUAN CITY Agusan del Norte RCPI BUTUAN MONTILLA BLVD Montilla Blvd., Butuan City Agusan del Norte RCPI SAN FRANCISCO AGUSAN SUR BRGY. 2 CENTER ISLAND SAN FRANCISCO Agusan del Sur EBIZ - KALIBO 220 PASTRANA ST. KALIBO AKLAN Aklan RCPI AKLAN BORACAY Boat Station 3, Oro Compound, Boracay, Malay Aklan RCPI AKLAN KALIBO BURGOS ST. COR. GEN. LUNA ST. Aklan RCPI KALIBO 2 GAISANO ROXAS AVE. INFRONT OF GAISANO CITY KALIBO AKLAN Aklan EBIZ - ALBAY LEGASPI V & O BLDG. COR. QUEZON AVE. & LAPU LAPUST LEGASPI Albay EBIZ - ALBAY TABACO LOT 1 7651 A1 ALMINE BLDG. ZIGA AVE. TABACO Albay RCPI ALBAY DARAGA RIZAL ST. BRGY. ILAWAD DARAGA ALBAY Albay RCPI ALBAY LEGASPI CITY VELASCO BLDG. RIZAL ST. COR. IMPERIAL, LEGASPI BI Albay RCPI ALBAY LEGASPI PACIFIC MALL F. IMPERIAL ST. PACIFIC MALL. BLDG. LEGASPI CITY Albay RCPI ALBAY LIGAO Centro, Ligao Albay RCPI ALBAY POLANGUI BRGY. UBALIW POLANGUI ALBAY Albay RCPI ALBAY TABACO FIRAZA BLDG. ZIGA AV. DIVINO ROSTRO, TABACO Albay RCPI AURORA BALER QUEZON ST. COR. GOMEZ ST. BALER AURORA Aurora EBIZ - BALANGA BONIFACIO ST. BALANGA CITY BATAAN Bataan EBIZ - DINALUPIHAN STALL ARCADE DINALUPIHAN PUBLIC MKT. NAT. HWAY Bataan RCPI BALANGA Don Manuel Banzon, Balanga Bataan RCPI BATAAN BALANGA RECAR COMPLEX GRND. FLR. RECAR COMPLEX J.P. RIZAL & ZULUETA ST. Bataan BATANGAS RB FOR COOPERATIVES NEW PUBLIC MARKET, PASTOR AVE, CUTA, BATANGAS CTY Batangas BAY CITY MALL P. -

Sec Form 20-Is

COVER SHEET 0 0 0 0 0 2 9 3 1 6 S.E.C. Registration Number R O B I N S O N S B A N K C O R P O R A T I O N (Company’s Full Name) 1 7 T H F L R G A L L E R I A C O R P O R A T E C E N T E R E D S A C O R O R T I G A S Q C (Business Address: No. Street City/Town/Province) RHORY F. GO 8702-9500 Contact Person Company Telephone Number 1 2 3 1 20 - IS 0 6 Last Wednesday Month Day Form Type Month Day (Fiscal Year) (Annual Meeting) NONE Secondary License Type, If Applicable Corporate Finance Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 15 Total No. of Stockholders Domestic Foreign ----------------------------------------------------------------------------------------------------------------------------------- To be accomplished by SEC Personal concerned File Number LCU Document I.D. Cashier Stamp Remarks: Please use BLACK ink for scanning purpose EXPLANATION OF AGENDA ITEMS FOR STOCKHOLDERS’ MEETING – JUNE 23, 2021 1. Call to Order including the ratification of related party transactions, will be presented to the Mr. Lance Y. Gokongwei, the Chairman of stockholders for their approval and the Board, will be the one to call the ratification. meeting in order. 2. Proof of Due Notice of Meeting Atty. Roel S. Costuna, the Corporate Secretary, will certify the date when the 7. Election of the Board of Directors for the written notice with the corresponding Ensuing Term (2021-2022) statement were sent to the stockholders of record as of May 27, 2021. -

BAYAD CENTER NAME ADDRESS CITY/PROVINCE 168 NET TECHNOLOGIES - PUREGOLD Stall No

BAYAD CENTER NAME ADDRESS CITY/PROVINCE 168 NET TECHNOLOGIES - PUREGOLD Stall No. 10 Puregold Building, Ninoy Aquino Avenue, Parañaque City PARANAQUE CITY 2BZ CORPORATION Ground Floor, AD Center Square, A. Rodriguez St., Corner Evangelista St., Brgy. Santolan, Pasig City PASIG CITY 3 AJ BAYAD CENTER Prime Asiatique, Commercial Center, Barangay Mambog Buhay Na Tubig, Imus, Cavite CAVITE 55 E.C. BERNABE CO INC. Block 17, L17, Stall 1, Donna Aguirre Avenue, Pilar Village, Las Pinas LAS PINAS CITY 777 COLLECTION - SSS MAC SSS Main Office, Quezon City UPPER QUEZON CITY 777 COLLECTION ASSISTANCE CENTER 2 Galino St., Balinghasa, Quezon City UPPER QUEZON CITY ABS-CBN E-MONEY PLUS INC. G/F ELJ COMM. CNTR. ABS-CBN CMPD. MOTHER IGNACIA Quezon City ACN BAYAD CENTER 100 Unit 2 Malolos Avenue, Tagumpay St., Caloocan City CALOOCAN CITY ACN OFFICE MART - BAGONG BARRIO 367 EDSA Bagong Barrio, Caloocan City (infront of Honda Cars - Caloocan) UPPER QUEZON CITY ACN OFFICEMART - SSS CALOOCAN EDSA Corner Gen Malvar St., Caloocan City CALOOCAN CITY ADB EMPLOYEES' MULTI-PURPOSE COOPERATIVE No. 6 ADB Avenue, Ortigas Center, Mandaluyong City MANDALUYONG CITY ADELAIDE ENTERPRISES Cagayan Valley Road, San Juan, San Ildefonso, Bulacan BULACAN ALTERNATE REALTIES Ground Floor, Festival Mall, Alabang, Muntinlupa City MUNTINLUPA CITY AMZ BAYAD CENTER - SAN BARTOLOME 1E Ground Floor Nova Square Quirino Highway, San Bartolome, Novaliches Quezon City UPPER QUEZON CITY AMZ BAYAD CENTER - TALIPAPA Quirino Highway, Talipapa, Novaliches, Quezon City UPPER QUEZON CITY ARFAZ BUSINESS CENTER - STA QUITERIA 231 Tandang Sora Extension Brgy. 163, Sta. Quiteria, Caloocan City UPPER QUEZON CITY AVELINO PAYMENT CENTER No. 13A Brgy. -

Where to Buy Yazz

WHERE TO BUY YAZZ YAZZ STORE PARTNERS Bahayang Pag-Asa Market Ground Floor Bahayang Pag-asa Market, Imus, Cavite Autohide Autoload Panganiban Drive, Naga CIty Emall – Cloudfone Kiosk GF Emall Elias Angeles St. Penafrancia Ave. Naga City Kooky N Luscious G/F MCC Building Ayala Ave Makati CIty Pacific Mall Lucena Viewerss Mobile 2f (M.L Tagarao St.), Lucena City Viewers Mobile Gadgets Quezon Ave. Lucena City CD-R KING BRANCHES BRANCH NAME ADDRESS Alabang Town Center-under 3/f alabang town center brgy. ayala alabang renovation until May 31 muntinlupa city Upper Ground Floor Alimall, Araneta Center Alimall Cubao, Brgy. Socorro, Quezon City Anonas LRT City Center, Aurora Blvd., Brgy. Anonas LRT Bagumbuhay, Quezon City 3rd Floor Stall 312 , Ayala Center Cebu, Bus. Park, Ayala Cebu Cebu City (Capital), Cebu, 6000, Central Visayas Unit S10-12 Bluewave Strip Mall, marikina, Bluewave Strip Mall Sumulong Highway, Marikina City 2nd Floor Cash & Carry Mall, South Super Cash and Carry Highway cor. Filmore St. Palanan Makati City. 3rd Floor Centrio Mall CM Recto Avenue, Cagayan De Oro City (Capital), Misamis Centrio Mall CDO Oriental, 9000, Northern Mindanao Dela Rosa Carpark 1, Delarosa Street, Legaspi Dela Rosa Carpark 1 – Makati Village, Makati City 2/F EDSA Central Pavillion, Edsa cor Shaw Blvd. Edsa Central Brgy. Highway Hills,Mandaluyong City 3rd Floor Elizabeth Mall Corner N. Bacalso Leon Kilat Street, Cebu City (Capital), Cebu, 6000, E-mall Cebu Central Visayas Unit L2-212 Nagaland Elizabeth-Mall, Elias Angeles Street San Francisco, Naga City, E-Mall Nagaland Camarines Sur, 4400, Bicol Region SF 16 &17, 2nd Floor Centris Station, Quezon E-ton Centris-under renovation Ave.,Pinyahan Quezon City 2/F Ever Gotesco Commonwealth, Ever Commonwealth Commonwealth Ave., Batasan Hills, Quezon City Fairview Terraces Level 3 Fairview Terraces Quirino Highway Pasong Putik Novaliches Quezon City Ground Floor New Farmers Plaza, Araneta Farmers Center Cubao, Brgy. -

Branch Name Address Abreeza Davao Ground Floor, Abreeza Mall

Branch Name Address Abreeza Davao Ground Floor, Abreeza Mall J.P. Laurel Avenue Bajada, Davao City Alabang Town Center G/F Alabang Commercial Center Alabang Town Center, Muntinlupa City Ali Mall U/G Flr. Phase II Alimall Bldg. Cubao, Quezon City Antipolo Circum #6 Circumferential Road, cor., M.L. Quezon Brgy. Dalig, Antipolo City Antipolo Victory Park 1st & 2nd Flr. P. Oliveros cor ML Quezon St. Antipolo, Rizal Ayala Bacolod Grd. Flr. The District North Point, National Highway, Talisay City, Negros Occidental Ayala Cebu Level 2 Ayala Center Archibishop Reyes Ave., Cebu City G/F Ayala Fairview Terraces, Quirino Highway cor. Maligaya Drive Bgy. Pasong Putik Ayala Fairview Terraces Novaliches, Quezon City Grd. Flr. Ayala The District, Aguinaldo Highway corner Daang Hari Road, Brgy. Anabu Ayala Imus Imus, Cavite Ayala Legazpi Ground Flr. Units 138-143 Liberty City Center Legazpi City, Albay Ayala Solenad 3 Ground Floor, Building D, Solenad 3, Nuvali, Sta. Rosa, Laguna First Floor, Ayala Malls Serin, Aguinaldo Highway, Brgy. Maharlika East, Tagaytay Ayala Tagaytay City, Cavite Baguio Abanao G/F Abanao Square cor. Zandueta Abanao St., Baguio City Batac Washington St. Brgy. Ablan Batac, Ilocos Norte Batangas Bay City G/F Bay City Mall, D. Silang St. corner P. Burgos, Batangas City Bauan 2369 ABCC Bauan Kapitan Ponso St Poblacion Bauan Batangas Bohol UG/F, Level, Island City Mall, Dampas District, Tagbilaran City, Bohol C Raymundo UG/F Danny Floro Bldg. C. Raymundo Ave. Pag-asa, Pasig City Cabanatuan G/F N.E Pacific Mall Maharlika Highway, Cabanatuan City Cagayan De Oro Borja Grd. Flr. Bldg. -

3 – Growth Centers

ANNEX 3 GROWTH CENTERS CBD-KNOWLEDGE COMMUNITY DISTRICT CUBAO GROWTH DISTRICT BATASAN-NGC GROWTH CENTER NOVLIHES-LAGRO GROWTH CENTER BALINTAWAK-MUNOZ GROWTH CENTER Annex 3: Growth Centers 1. CBD-KNOWLEDGE COMMUNITY DISTRICT 1.1. Area Coverage and Population The proposed CBD-Knowledge Community District has total area of 1,862 hectares and covers 22 barangays in Districts I, III and IV. It embraces the North, East, South and West triangles, UP Campus including the UP-Ayala Techno Hub, Ateneo de Manila University, Miriam College, Balara Filtration Plant, the vicinity of SM North EDSA and Veteran’s Memorial Medical Center and the residential communities in UP Village, Teacher’s Village, Pinyahan, Krus na Ligas, Malaya and Xavierville areas. 1.2. District Boundary The study area is bounded by the following: North: Area lot deep northside of Nueva Vizcaya St. and Road 3 up to lot deep westside of Mindanao Avenue then northward up to lot deep northside of Road 10 then eastward up to lot deep Westside of Visayas Avenue then northward up to lot deep northside of Central Avenue then eastward towards Commonwealth Avenue extending up to lot deep eastside of Katipunan Avenue. East: Area lot deep eastside of Katipunan Avenue going towards lot deep northside of Mactan St. then eastward towards lot deep eastside of Balintawak St. then southward to QC-Marikina politicalBoundary then westward through periphery of MWSS Balara Homesite up to MWSSAqueduct then southward up to lot deepEastside of Katipunan Avenue then Southward towards Mangyan St. and Eastward along southern periphery of LaVista Subdivision up to QC-Marikina politicalBoundary then southward up to Aurora Boulevard. -

Participating Robinsons Supermarket Branches

Participating Robinsons Supermarket branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST. NOAH'S ARC BLDG. BF HOMES PARANAQUE CITY ROBINSONS EASYMART ALIMA BAY ALIMA BAY RESIDENCES AND COMMERCIAL COMPLEX IN GEN. EVANGELISTA ST. BRGY. ALIMA BACOOR CAVITE ROBINSONS EASYMART ANTIPOLO ROBINSONS EASYMART ANTIPOLO RODRIGUEZ ROAD BARANGAY SITIO PARUGAN SAN JOSE ANTIPOLO CITY ROBINSONS EASYMART ARNAIZ ARNAIZ AVENUE, LIBERTAD PASAY CITY PASAY 1300 ROBINSONS EASYMART E 340 E. RODRIGUEZ SR. AVE COR. CORDILLERA ST. BRGY. DON RODRIGUEZ SR MANUEL, QC ROBINSONS EASYMART FILINVEST FILINVEST II GATE B SAN MATEO ROAD-BATASAN HILLS BATASAN HILLS QUEZON CITY ROBINSONS EASYMART PHASE 3 GREEN GATE SUBDV. MALAGASANG 2A IMUS CAVITE GREENGATE IMUS ROBINSONS EASYMART #89 K1ST BARANGAY KAMUNING QUEZON CITY KAMUNING ROBINSONS EASYMART LAGRO SUNBEST BLDG. ASCENSION AVENUE BRGY. GREATER LAGRO, QUEZON CITY ROBINSONS EASYMART LOYOLA #88 ROSA ALVERO ST. LOYOLA HEIGHTS QUEZON CITY HEIGHTS ROBINSONS EASYMART MARILAO GROUND FLOOR OF CINDY SQUARE IN MC ARTHUR HIGHWAY, ABANGAN,NORTE,MARILAO BULACAN ROBINSONS EASYMART MARIPOSA G/F MARIPOSA ARCADE A. MABINI ST. KAPASIGAN PASIG CITY ARCADE ROBINSONS EASYMART G/F SAVER'S BUILDUING ALABANG ZAPOTE ROAD TALON 1 MOONWALK LP MOONWALK LAS PINAS CITY ROBINSONS EASYMART PILILIA J.P. RIZAL STREET, BRGY. IMATONG, PILILLA, RIZAL RIZAL ROBINSONS EASYMART 888 SAN IGNACIO ST., BRGY. POBLACION I, SAN JOSE DEL POBLACION MONTE BULACAN 3023 PHILIPPINES ROBINSONS EASYMART PROJECT 6 #54 EMERALD COURT BLDG. ROAD 8, PROJECT 6, QUEZON CITY ROBINSONS EASYMART SAN SAN AGUSTIN COR SAN FRANCISCO ST POBLACION 2 TANZA AGUSTIN-TANZA CAVITE 4108 PHILIPPINES ROBINSONS EASYMART SAN KAMBAL ROAD BRGY.GITNANG BAYAN 1 SAN MATEO, RIZAL MATEO ROBINSONS EASYMART SAVERS 192 SAVERS APPLIANCE DEPOT ROOSEVELT AVE. -

2019 Annual Report Contents

2019 ANNUAL REPORT CONTENTS COMPANY PROFILE Financial Highlights . 3 Project Location (Map) . 4 Directory . 5 MESSAGE TO STAKEHOLDERS . 6 A TRIBUTE TO JOHN L. GOKONGWEI, JR. 10 OUR BUSINESS UNITS Commercial Centers . 13 Residential . 15 Office Buildings . 18 Hotels & Resorts . 20 Industrial & Integrated Developments . 22 Chengdu Ban Bian Jie . 23 CORPORATE SOCIAL RESPONSIBILITY RLove Program . 25 Robinsons Mall Gift of Change . 28 Environment & Sustainability . 30 CORPORATE GOVERNANCE Our Commitment to Good Governance . 33 The Board of Directors - Responsibilities and Composition . 37 Enterprise Risk Management, Accountability, and Audit . 42 Other Matters . 45 BOARD OF DIRECTORS . 47 AUDITED FINANCIAL STATEMENTS . 49 Financial Highlights For the Years ended December 31 2019 2018 2017 2016 2015 2014 2013 (in million pesos) Gross Revenues 30,583.84 29,558.48 22,516.82 22,809.05 20,306.91 17,460.22 16,552.44 Net Income 8,692.61 8,223.96 5,884.44 5,755.32 5,952.94 4,773.87 4,318.49 Total Assets 189,651.21 174,158.16 148,126.55 124,432.16 111,711.51 88,421.50 76,808.45 Stockholders' Equity 100,077.67 93,919.72 67,372.62 62,855.31 58,444.74 53,968.36 50,425.83 8.69 8.22 29.56 30.58 5.95 5.88 22.81 5.76 20.31 22.52 2015 2016 2017 2018 2019 2015 2016 2017 2018 2019 Gross Revenues Net Income (in billion pesos) (in billion pesos) 100.08 189.65 93.92 174.16 148.13 67.37 62.86 124.43 58.44 111.71 2015 2016 2017 2018 2019 2015 2016 2017 2018 2019 Total Assets Stockholders' Equity (in billion pesos) (in billion pesos) 3 ROBINSONS LAND CORPORATION