Download File

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Redemption Outlets Visit Bit.Ly/Bluegc2018 for The

List of Redemption Outlets Location Address Owndays Ayala Center Cebu Level 1 Ayala Center Cebu, Cebu Business Park, Cebu City Owndays Ayala Malls Cloverleaf Level 1 Ayala Malls Cloverleaf, Quezon City Owndays Ayala Malls Vertis North Ground Floor Ayala Malls Vertis North, Quezon City Owndays Eastwood Mall Ground Floor Eastwood Mall Eastwood, Quezon City Owndays Estancia Level 1 Estancia Mall Meralco Ave. Pasig City Owndays Fairview Terraces Upper Ground Floor Fairview Terraces, Novaliches Quezon City Owndays Festival Mall UG Floor Festival Mall Expansion, Alabang, Muntinlupa City Owndays Gateway Mall Level 2 Gateway Mall Araneta Center Cubao Quezon City Owndays Glorietta 2 Ground Floor Glorietta 2 Mall, Ayala Center, Makati City Owndays MarQuee Mall Ground Floor MarQuee Mall Expansion, Angeles City Pampanga Owndays Robinsons Galleria 2nd Level Robinsons Galleria, Quezon City Owndays Robinsons Place Manila Level 1 Midtown Wing Robinsons Place Manila, Manila Owndays Shangri-La Plaza Level 1 Main Wing Shangri-La Plaza, Mandaluyong City Owndays SM City East Ortigas Ground Floor SM City East Ortigas Ortigas Ave. Pasig City Owndays SM City Fairview Upper Ground Level Main Building, SM City Fairview, Quezon City Owndays SM City Molino Ground Floor Mall Expansion SM City Molino, Bacoor Cavite Owndays SM Megamall 3rd Level SM Mega Fashion Hall SM Megamall, Mandaluyong Owndays Solenad 3 Ground Floor Building C Solenad 3, Santa Rosa Laguna Owndays U.P. Town Center Level 1 U.P. Town Center Katipunan, Quezon City Owndays Uptown Mall UG Floor Uptown Mall Uptown, Taguig City Visit bit.ly/BlueGC2018 for the redemption process and requirements.. -

Philippine Rating Services Corporation (Philratings)

PRESS RELEASE RATING NEWS December 16, 2019 The Pioneer Domestic Credit Rating Agency EastWest Bank Gets High Credit Rating East West Banking Corporation (EastWest Bank), the banking arm of the Filinvest Group, was assigned an issuer credit rating of PRS Aa plus (corp.) by Philippine Rating Services Corporation (PhilRatings). The rating has a Stable Outlook. An Issuer Credit Rating is a measure of the general creditworthiness of a company over a one year period. A company rated PRS Aa (corp.) differs from the highest rated corporates only to a small degree, and has a strong capacity to meet its financial commitments relative to that of other Philippine corporates. The plus further qualifies the assigned rating within the “Aa” rating level. A Stable Outlook, on the other hand, indicates that the rating is likely to be maintained or to remain unchanged in the next 12 months. The issuer credit rating takes into consideration EastWest Bank’s clearly-defined and well- executed growth strategy; its ability to compete in its chosen market; the favorable outlook for domestic consumer credit despite economic headwinds in 2018; and the bank’s strong shareholders and highly- experienced management. The issuer credit rating assigned by PhilRatings is based on available information and projections at the time that the rating review was performed. PhilRatings shall continuously monitor developments relating to EastWest Bank, and may change the rating at any time, should circumstances warrant a change. As a domestic universal bank (unibank), EastWest Bank provides a wide range of financial services to consumer and corporate clients. These services include deposit-taking, loan and trade finance, treasury, trust services, credit cards, cash management, custodial services, insurance services and leasing and finance. -

Participating Robinsons Supermarket Branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST

Participating Robinsons Supermarket branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST. NOAH'S ARC BLDG. BF HOMES PARANAQUE CITY ROBINSONS EASYMART ALIMA BAY ALIMA BAY RESIDENCES AND COMMERCIAL COMPLEX IN GEN. EVANGELISTA ST. BRGY. ALIMA BACOOR CAVITE ROBINSONS EASYMART ANTIPOLO ROBINSONS EASYMART ANTIPOLO RODRIGUEZ ROAD BARANGAY SITIO PARUGAN SAN JOSE ANTIPOLO CITY ROBINSONS EASYMART ARNAIZ ARNAIZ AVENUE, LIBERTAD PASAY CITY PASAY 1300 ROBINSONS EASYMART E RODRIGUEZ SR 340 E. RODRIGUEZ SR. AVE COR. CORDILLERA ST. BRGY. DON MANUEL, QC ROBINSONS EASYMART FILINVEST BATASAN FILINVEST II GATE B SAN MATEO ROAD-BATASAN HILLS QUEZON HILLS CITY ROBINSONS EASYMART GREENGATE IMUS PHASE 3 GREEN GATE SUBDV. MALAGASANG 2A IMUS CAVITE ROBINSONS EASYMART KAMUNING #89 K1ST BARANGAY KAMUNING QUEZON CITY ROBINSONS EASYMART LAGRO SUNBEST BLDG. ASCENSION AVENUE BRGY. GREATER LAGRO, QUEZON CITY ROBINSONS EASYMART LOYOLA HEIGHTS #88 ROSA ALVERO ST. LOYOLA HEIGHTS QUEZON CITY ROBINSONS EASYMART MARILAO GROUND FLOOR OF CINDY SQUARE IN MC ARTHUR HIGHWAY, ABANGAN,NORTE,MARILAO BULACAN ROBINSONS EASYMART MARIPOSA ARCADE G/F MARIPOSA ARCADE A. MABINI ST. KAPASIGAN PASIG CITY ROBINSONS EASYMART MOONWALK LP G/F SAVER'S BUILDUING ALABANG ZAPOTE ROAD TALON 1 MOONWALK LAS PINAS CITY ROBINSONS EASYMART PILILIA RIZAL J.P. RIZAL STREET, BRGY. IMATONG, PILILLA, RIZAL ROBINSONS EASYMART POBLACION 888 SAN IGNACIO ST., BRGY. POBLACION I, SAN JOSE DEL MONTE BULACAN 3023 PHILIPPINES ROBINSONS EASYMART PROJECT 6 #54 EMERALD COURT BLDG. ROAD 8, PROJECT 6, QUEZON CITY ROBINSONS EASYMART SAN AGUSTIN-TANZA SAN AGUSTIN COR SAN FRANCISCO ST POBLACION 2 TANZA CAVITE 4108 PHILIPPINES ROBINSONS EASYMART SAN MATEO KAMBAL ROAD BRGY.GITNANG BAYAN 1 SAN MATEO, RIZAL ROBINSONS EASYMART SAVERS ROOSEVELT 192 SAVERS APPLIANCE DEPOT ROOSEVELT AVE. -

Sec Form 20-Is

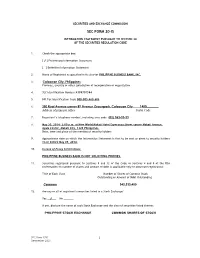

SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ √ ] Preliminary Information Statement [ ] Definitive Information Statement 2. Name of Registrant as specified in its charter PHILIPPINE BUSINESS BANK, INC. 3. Caloocan City, Philippines Province, country or other jurisdiction of incorporation or organization 4. SEC Identification Number A199701584 5. BIR Tax Identification Code 000-005-469-606 6. 350 Rizal Avenue corner 8th Avenue Gracepark, Caloocan City 1400________ Address of principal office Postal Code 7. Registrant’s telephone number, including area code (02) 363-33-33 8. May 30, 2014- 2:00 p.m. at New World Makati Hotel Esperanza Street corner Makati Avenue, Ayala Center, Makati City, 1228 Philippines. Date, time and place of the meeting of security holders 9. Approximate date on which the Information Statement is first to be sent or given to security holders on or before May 09, 2014. 10. In case of Proxy Solicitations: PHILIPPINE BUSINESS BANK IS NOT SOLICITING PROXIES. 11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding or Amount of Debt Outstanding Common 343,333,400 12. Are any or all of registrant's securities listed in a Stock Exchange? Yes __√___ No _______ If yes, disclose the name of such Stock Exchange and the class of securities listed therein: PHILIPPINE STOCK EXCHANGE COMMON SHARES OF STOCK SEC Form 17-IS 1 December 2003 PHILIPPINE BUSINESS BANK, INC. -

Filipino Fund, Inc. FFI

CR01980-2018 The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. Filipino Fund, Inc. FFI PSE Disclosure Form 17-12 - List of Top 100 Stockholders Reference: Section 17.12 of the Revised Disclosure Rules Type of Securities Common Preferred N/A Others N/A For the period ended Mar 31, 2018 Description of the Disclosure FFI report on Top 100 stockholders as of March 31, 2018. Filed on behalf by: Name Natividad Chua Designation Corporate Information Officer BPI STOCK TRANSFER OFFICE FILIPINO FUND, INC TOP 100 STOCKHOLDERS AS OF MARCH 31, 2018 RANK STOCKHOLDER NUMBER STOCKHOLDER NAME NATIONALITY CERTIFICATE CLASS OUTSTANDING SHARES PERCENTAGE TOTAL 1 16000457 PCD NOMINEE CORPORATION (FILIPINO) FIL A 43,885,935 87.4789% 43,885,935 G/F MAKATI STOCK EXCHANGE 2 16000458 PCD NOMINEE CORPORATION (NON-FILIPINO) NOF A 240,350 0.4790% 240,350 BLDG., AYALA AVENUE, MAK G/F MAKATI STOCK EXCHANGE 3 18000767 ALLEN C. ROXAS FIL A 94,667 0.1887% 94,667 BLDG., AYALA AVENUE, MAK 4/F STATE CENTRE BLDG., 4 15000217 ALBERT GO ONG FIL A 90,250 0.1798% 90,250 333 JUAN LUNA ST., BINONDO 33 DUHAT STREET, VALLE VERDE I, PASIG CITY 5 18000497 REYMONT INC. -

BUS Schedule, Stops And

BUS bus time schedule & line map Dbp Ave, Taguig City, Manila, Manila →Mmda BUS Navotos Bus Terminal, Circumferential Road 4, View In Website Mode Navotas City, Manila The BUS bus line (Dbp Ave, Taguig City, Manila, Manila →Mmda Navotos Bus Terminal, Circumferential Road 4, Navotas City, Manila) has 2 routes. For regular weekdays, their operation hours are: (1) Dbp Ave, Taguig City, Manila, Manila →Mmda Navotos Bus Terminal, Circumferential Road 4, Navotas City, Manila: 12:00 AM - 11:00 PM (2) Mmda Navotos Bus Terminal, Circumferential Road 4, Navotas City, Manila →Dbp Ave, Taguig City, Manila, Manila: 12:00 AM - 11:00 PM Use the Moovit App to ƒnd the closest BUS bus station near you and ƒnd out when is the next BUS bus arriving. Direction: Dbp Ave, Taguig City, Manila, BUS bus Time Schedule Manila →Mmda Navotos Bus Terminal, Dbp Ave, Taguig City, Manila, Manila →Mmda Circumferential Road 4, Navotas City, Manila Navotos Bus Terminal, Circumferential Road 4, 110 stops Navotas City, Manila Route Timetable: VIEW LINE SCHEDULE Sunday 12:00 AM - 10:00 PM Monday 12:00 AM - 11:00 PM Dbp Ave, Taguig City, Manila, Manila Tuesday 12:00 AM - 11:00 PM Dbp Ave, Taguig City, Manila, Manila East Service Road, Philippines Wednesday 12:00 AM - 11:00 PM Thursday 12:00 AM - 11:00 PM South Luzon Expressway, Taguig City, Manila C-5 Entrance ramp, Philippines Friday 12:00 AM - 11:00 PM South Luzon Expressway, Taguig City, Manila Saturday 12:00 AM - 10:00 PM South Luzon Expressway, Taguig City, Manila South Luzon Expressway, Taguig City, Manila Nichols Exit, -

2019 ANNUAL REPORT [email protected]

PHILIPPINE DEPOSIT INSURANCE CORPORATION TAKING THE HELM, Philippine Deposit Insurance Corporation SSS Bldg., 6782 Ayala Ave. cor. V.A. Rufino St. ONWARD TO A NEW HORIZON 1226 Makati City, Philippines 2019 ANNUAL REPORT www.pdic.gov.ph [email protected] 1 PHILIPPINE DEPOSIT INSURANCE CORPORATION TAKING THE HELM, Philippine Deposit Insurance Corporation SSS Bldg., 6782 Ayala Ave, cor. V.A. Rufino St. ONWARD TO A NEW HORIZON 1226 Makati City, Philippines 2019 ANNUAL REPORT www.pdic.gov.ph [email protected] CONTENTS 01 Corporate Profile 02 The Philippine Deposit Insurance System 03 Transmittal Letters 06 Chairman’s Message ABOUT THE COVER 08 President’s Report Titled “Taking the Helm, Onward to a New Horizon”, the 2019 15 Corporate Operating Environment Annual Report wraps up another trilogy of PDIC annual reports, from “Changing Horizons” in 2017 and “A New Horizon” in 18 Institutional Governance Framework 2018. The horizon, represented by the ever-evolving financial 22 Strengthening Depositor Protection landscape that PDIC navigates, is full of challenges, and the Corporation continues to face it head on. The PDIC is undeterred 36 Ensuring Good Governance by the currents and is committed to create ripples of positive 50 Promoting Financial Stability change in the service of its clients and stakeholders. 68 Financial Performance The organization’s readiness and earnest desire to serve 74 Corporate Direction for 2020 is communicated through this year’s cover design -- young professionals take determined strides towards the rising sun, 78 Board of Directors embodying confidence that the PDIC is in the right direction to 86 Executive Committee accomplish its Vision to be a leading institution in depositor 87 Group Heads protection recognized for its operational excellence that is responsive to the changing times. -

Trust Division, 3F Eastwest Corporate Center, 5Th

EASTWEST BANKING CORPORATION > Your dream Our focus < EASTWEST PESO MONEY MARKET FUND KEY INFORMATION AND INVESTMENT DISCLOSURE STATEMENT For the Quarter 30 June 2015 FUND FACTS Net Asset Value per Unit Classification: Peso Money Market P1,242.1114 (NAVPU): Launch Date: 1 March 2007 Total Fund NAV: P288.313 million Min. Initial Investment: P100,000.00 Dealing Day: Daily, up to 12 noon Next banking day from date Min. Additional Investment: P0.00 Redemption Settlement: of redemption Min. Holding Period: None Early Redemption Charge: Not Applicable Applicable Tax: 20% Final Tax Valuation: Marked-to-Market FEES Trustee Fee: Custodianship Fee: External Audit Fee: Other Fees: 0.2500% p.a. 0.0000%* 0.0000% 0.0000% EastWest Bank – Trust Division HSBC SGV *Ratio of expense to the quarter’s average daily net asset value. INVESTMENT OBJECTIVE AND STRATEGY The Fund aims to provide its participants with enhanced yields for their short-term liquidity needs by investing in a portfolio of bank deposits and BSP Special Deposit Accounts with maximum time to maturity of twelve months. It aims to outperform the 3-month Philippine Dealing System Treasury Interpolated Rate PM (PDSI-R2). CLIENT SUITABILITY A client profiling process should be performed prior to participating in the Fund to guide the prospective investor if the Fund is suited to his/her investment objectives and risk tolerance. Clients are advised to read the Declaration of Trust/Plan Rules of the Fund, which may be obtained from the Trustee, before deciding to invest. The Fund is suitable for investors who: Have a conservative risk appetite Are looking for current income over an investment time horizon of at least thirty days KEY RISKS AND RISK MANAGEMENT You should not invest in this Fund if you do not understand or are not comfortable with the accompanying risks. -

Province, City, Municipality Total and Barangay Population AURORA

2010 Census of Population and Housing Aurora Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population AURORA 201,233 BALER (Capital) 36,010 Barangay I (Pob.) 717 Barangay II (Pob.) 374 Barangay III (Pob.) 434 Barangay IV (Pob.) 389 Barangay V (Pob.) 1,662 Buhangin 5,057 Calabuanan 3,221 Obligacion 1,135 Pingit 4,989 Reserva 4,064 Sabang 4,829 Suclayin 5,923 Zabali 3,216 CASIGURAN 23,865 Barangay 1 (Pob.) 799 Barangay 2 (Pob.) 665 Barangay 3 (Pob.) 257 Barangay 4 (Pob.) 302 Barangay 5 (Pob.) 432 Barangay 6 (Pob.) 310 Barangay 7 (Pob.) 278 Barangay 8 (Pob.) 601 Calabgan 496 Calangcuasan 1,099 Calantas 1,799 Culat 630 Dibet 971 Esperanza 458 Lual 1,482 Marikit 609 Tabas 1,007 Tinib 765 National Statistics Office 1 2010 Census of Population and Housing Aurora Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population Bianuan 3,440 Cozo 1,618 Dibacong 2,374 Ditinagyan 587 Esteves 1,786 San Ildefonso 1,100 DILASAG 15,683 Diagyan 2,537 Dicabasan 677 Dilaguidi 1,015 Dimaseset 1,408 Diniog 2,331 Lawang 379 Maligaya (Pob.) 1,801 Manggitahan 1,760 Masagana (Pob.) 1,822 Ura 712 Esperanza 1,241 DINALUNGAN 10,988 Abuleg 1,190 Zone I (Pob.) 1,866 Zone II (Pob.) 1,653 Nipoo (Bulo) 896 Dibaraybay 1,283 Ditawini 686 Mapalad 812 Paleg 971 Simbahan 1,631 DINGALAN 23,554 Aplaya 1,619 Butas Na Bato 813 Cabog (Matawe) 3,090 Caragsacan 2,729 National Statistics Office 2 2010 Census of Population and -

DINING MERCHANT PARTICIPATING BRANCHE/S OFFER Wooden Horse Steakhouse G/F Molito Complex, Madrigal Ave., Cor Alabang Zapote Road

DINING MERCHANT PARTICIPATING BRANCHE/S OFFER G/F Molito Complex, Madrigal Ave., cor Alabang Zapote Road Wooden Horse Steakhouse 10% OFF on total bill Muntinlupa City SM Megamall - 2/F Mega Atruim, Julia Vargas Ave., Wack Wack 15% OFF on total bill Kichitora Mandaluyong BCG - 3/F BGC Central Sqaure, BGC Taguig City Greenbelt 3 - 3/F Greenbelt 3, Makati City 15% OFF on total bill Motorino BGC - G/F Netlima Bldg. BGC Taguig City Tappella Greenbelt 5 - G/4 Greenbelt 5 Ayala Center Makati City 10% OFF on total bill La Cabrera Glorieta Complex - 6750 Building Glorieta Complex Makati City 15% OFF on total bill Nikkei No. 111 Frabelle Bldg. Rada Street Legaspi Village Makati City 15% OFF on total bill Alimall – Araneta Centre Cubao Quezon City Alabang – Festival Mall Alabang Antipolo – Sumulong Hills Antipolo Antipolo – Robinsons Place Antipolo Baguio – SM City Baguio Cebu – SM City Cebu Congressional – Barrington Place, Congressional Ave. QC Katipunan – Katipunan Ave, Loyola Heights QC Manila – SM City Manila The Old Spaghetti House 10% OFF on total bill Market! Market! – Bonifacio Global City, Taguig Marikina – SM City Marikina – Midtown – Robinsons Place Ermita Midtown MOA – SM Mall of Asia Otis – Robinsons Place Otis Pioneer – Robinsons Place Forum SM The Block – SM City North Edsa The Block Sta Rosa – Solenad 3, Sta Rosa Laguna Valero – Paseo De Roxas Valero Street Makati Antipolo – Robinsons Place Antipolo MOA – SM City Mall of Asia Market! Market! – Bonifacio Global City, Taguig The Shrimp Shack 10% OFF on total bill Midtown – Robinsons Place Ermita Midtown SM The Block – SM North Edsa The Block Pioneer – Robinsons Place Forum Pioneer Greenhills San Juan Greenbelt 5 Diliman Torch Trinoma Mall 10% OFF on total bill BGC Alabang Olympia Venice Grand Canal Mall, McKinley Hill, Taguig Rice & Dough 10% OFF on total bill Eastwood Mall Ayala Fairview Terraces Gateway Mall Robinsons Galleria Rockwell SM City Marikina SM City North EDSA- The Block Burgoo SM Mall of Asia 10% OFF on total bill SM South Mall Solenad 3, Nuvali, Sta. -

Jcb Unique Dining Experience Merchants

JCB UNIQUE DINING EXPERIENCE MERCHANTS 7107 Culture + Cuisine Restaurant • G/F, Treston Bldg., BGC Alba Restaurante Espaǹol • Bel-Air, Makati City • Tomas Morato Quezon City • Westgate Center,Muntinlupa City • Prism Plaza, TwoEcom Center Building Mall of Asia Complex, Pasay City • Estancia Mall Capitol Commons, Pasig City Alchemy - Bistro • 4893 Durban St. Poblacion Makati Bari Uma Ramen • Ground Floor Serendra, Bonifacio High Street, BGC • Ayala Center Cebu Burgoo • The Block, North Edsa • SM City Marikina • The District Imus • Solenad 3, Nuvali • Robinsons Galleria • SM Mall of Asia • Gateway Mall • SM Southmall • Fairview Terraces • Vista Mall, Taguig Butamaru • West Gate Center, Alabang, Muntinlupa City • Technopoint Bldg, Pasig Chairman Wang's • Molito Lifestyle Bldg, Alabang Chotto Matte • Net Park, 5th Avenue, Bonifacio Global City, Taguig City Gumbo • SM Mall of Asia • Mega Atrium, Megamall • Robinsons Magnolia Hatsu Hana Tei • Herald Suites, Don Chino Roces Avenue, Makati City Ikomai & Tochi • ACI Group Building Makati City Izakaya Sensu • Net Park Building Bonifacio, Global City Kichitora • Bonifacio Highstreet Central, Bonifacio Global City • SM Megamall La Cabrera • Ayala Business Center, 6750 Ayala Avenue Mireio • 1 Raffles Drive Makati Avenue, Makati City Motto Motto • Ground Floor, Serendra, Bonifacio Global City, Taguig City Txanton • Alegria Alta Building,Makati City Wooden Horse Steakhouse • Molito Complex Alabang Yanagi • Midas Hotel Roxas Blvd, Pasay Yoshinoya • Glorietta Mall • SMCity Cebu North • Robinsons, Cybergate -

No. Company Star

Fair Trade Enforcement Bureau-DTI Business Licensing and Accreditation Division LIST OF ACCREDITED SERVICE AND REPAIR SHOPS As of November 30, 2019 No. Star- Expiry Company Classific Address City Contact Person Tel. No. E-mail Category Date ation 1 (FMEI) Fernando Medical Enterprises 1460-1462 E. Rodriguez Sr. Avenue, Quezon City Maria Victoria F. Gutierrez - Managing (02)727 1521; marivicgutierrez@f Medical/Dental 31-Dec-19 Inc. Immculate Concepcion, Quezon City Director (02)727 1532 ernandomedical.co m 2 08 Auto Services 1 Star 4 B. Serrano cor. William Shaw Street, Caloocan City Edson B. Cachuela - Proprietor (02)330 6907 Automotive (Excluding 31-Dec-19 Caloocan City Aircon Servicing) 3 1 Stop Battery Shop, Inc. 1 Star 214 Gen. Luis St., Novaliches, Quezon Quezon City Herminio DC. Castillo - President and (02)9360 2262 419 onestopbattery201 Automotive (Excluding 31-Dec-19 City General Manager 2859 [email protected] Aircon Servicing) 4 1-29 Car Aircon Service Center 1 Star B1 L1 Sheryll Mirra Street, Multinational Parañaque City Ma. Luz M. Reyes - Proprietress (02)821 1202 macuzreyes129@ Automotive (Including 31-Dec-19 Village, Parañaque City gmail.com Aircon Servicing) 5 1st Corinthean's Appliance Services 1 Star 515-B Quintas Street, CAA BF Int'l. Las Piñas City Felvicenso L. Arguelles - Owner (02)463 0229 vinzarguelles@yah Ref and Airconditioning 31-Dec-19 Village, Las Piñas City oo.com (Type A) 6 2539 Cycle Parts Enterprises 1 Star 2539 M-Roxas Street, Sta. Ana, Manila Manila Robert C. Quides - Owner (02)954 4704 iluvurobert@gmail. Automotive 31-Dec-19 com (Motorcycle/Small Engine Servicing) 7 3BMA Refrigeration & Airconditioning 1 Star 2 Don Pepe St., Sto.