2019 ANNUAL REPORT [email protected]

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download File

C O V E R S H E E T for AUDITED FINANCIAL STATEMENTS SEC Registration Number 2 9 3 1 6 C O M P A N Y N A M E R O B I N S ON S BANK CORPORATI ON AND SUBSI D I ARY PRINCIPAL OFFICE ( No. / Street / Barangay / City / Town / Province ) 1 7 t h Fl o o r , G a l l e r i a Co r p o r a t e Ce n t e r , EDSA c o r n e r O r t i g a s A v e n u e , Qu e z o n Ci t y Form Type Department requiring the report Secondary License Type, If Applicable 1 7 - A C O M P A N Y I N F O R M A T I O N Company’s Email Address Company’s Telephone Number Mobile Number www.robinsonsbank.com.ph 702-9500 N/A No. of Stockholders Annual Meeting (Month / Day) Fiscal Year (Month / Day) 15 Last week of April December 31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number Ms. Irma D. Velasco [email protected] 702-9515 09988403139 CONTACT PERSON’s ADDRESS 17th Floor, Galleria Corporate Center, EDSA corner Ortigas Avenue, Quezon City NOTE 1 : In case of death, resignation or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. -

Sec Form 20-Is

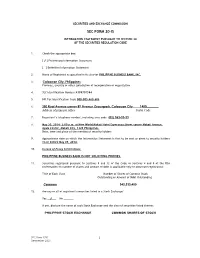

SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ √ ] Preliminary Information Statement [ ] Definitive Information Statement 2. Name of Registrant as specified in its charter PHILIPPINE BUSINESS BANK, INC. 3. Caloocan City, Philippines Province, country or other jurisdiction of incorporation or organization 4. SEC Identification Number A199701584 5. BIR Tax Identification Code 000-005-469-606 6. 350 Rizal Avenue corner 8th Avenue Gracepark, Caloocan City 1400________ Address of principal office Postal Code 7. Registrant’s telephone number, including area code (02) 363-33-33 8. May 30, 2014- 2:00 p.m. at New World Makati Hotel Esperanza Street corner Makati Avenue, Ayala Center, Makati City, 1228 Philippines. Date, time and place of the meeting of security holders 9. Approximate date on which the Information Statement is first to be sent or given to security holders on or before May 09, 2014. 10. In case of Proxy Solicitations: PHILIPPINE BUSINESS BANK IS NOT SOLICITING PROXIES. 11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding or Amount of Debt Outstanding Common 343,333,400 12. Are any or all of registrant's securities listed in a Stock Exchange? Yes __√___ No _______ If yes, disclose the name of such Stock Exchange and the class of securities listed therein: PHILIPPINE STOCK EXCHANGE COMMON SHARES OF STOCK SEC Form 17-IS 1 December 2003 PHILIPPINE BUSINESS BANK, INC. -

2018 Financial Statements

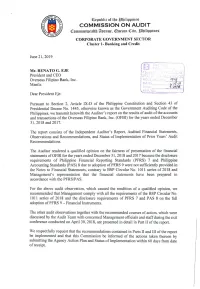

We acknowledge the support and cooperation that Management extended to the Audit Team, thus facilitating the completion of the report. Very truly yours, COMMISSION ON AUDIT Director IV Cluster Director Copy Furnished: The President of the Philippines The Chairperson - Appropriations Committee The Vice President The Secretary of the Department of Budget and Management The President of die Senate The Governance Commission of Government-Owned or Controlled Corporation The Speaker of the House of Representatives The National Library The Chairperson - Senate Finance Committee The UP Law Center Republic of the Philippines COMMISSION ON AUDIT Commonwealth Ave., Quezon City ANNUAL AUDIT REPORT on the OVERSEAS FILIPINO BANK, INC. (A Savings Bank of Landbank) For the years ended December 31, 2018 and 2017 EXECUTIVE SUMMARY INTRODUCTION Overseas Filipino Bank, Inc., A Savings Bank of LANDBANK, formerly known as Philippine Postal Savings Bank, Inc. (PPSBI) is a subsidiary of the Land Bank of the Philippines (LBP). On September 26, 2017, President Rodrigo Duterte issued Executive Order No. 44, which mandates the Philippine Postal Corporation and the Bureau of Treasury to transfer their PPSBI shares to Landbank at zero value. The EO further stated that Postbank will be converted into the Overseas Filipino Bank. On January 5, 2018, the PPSBI registered with the Securities and Exchange Commission the Amended Articles of Incorporation bearing the new corporate name. The Bangko Sentral ng Pilipinas through its Circular Letter No. CL-2018-007 dated January 18, 2018 approved the change of corporate name of the PPSBI to “Overseas Filipino Bank, Inc., a Savings Bank of LANDBANK”. As stated in its Vision, OFBI is a Digital Bank servicing Overseas Filipinos and their Beneficiaries through state-of-the-art Electronic Banking Channels such as Mobile Phone, ATM and Internet which are more convenient, faster (real-time), cheaper and secure, eliminating the need for over-the-counter services. -

Updated 2018 GLMS Compliance Status Data Presented Is Based from the Goccs’ Compliance As of 06 December 2019 Updated 2018 GLMS Compliance Status

Updated 2018 GLMS Compliance Status Data presented is based from the GOCCs’ Compliance as of 06 December 2019 Updated 2018 GLMS Compliance Status 30 GOCC SECTOR COMPLIANT NON-COMPLIANT Government Financial 25 2 25 Institutions Trade, Area Development 15 2 and Tourism 20 Education and Cultural 3 1 Gaming 1 1 Energy and Materials 8 1 15 Agriculture, Fisheries and 10 4 Food Utilities and No. of GOCCs of No. 14 4 10 Communications Healthcare Services 0 0 Holding Companies 5 0 5 Total Compliant GOCCs 81 0 Government Trade, Area Education and Gaming Sector Energy and Agriculture, Utilities and Healthcare Holding Financial Development Cultural Sector Materials Sector Fisheries and Communications Services Sector Companies Total Non-compliant GOCCs 15 Institutions Sector and Tourism Food Sector Sector Sector GOCC Sector COMPLIANT NON-COMPLIANT Data presented is based from the GOCCs’ Compliance as of 06 December 2019 Updated 2018 GLMS Compliance Status LIST OF COMPLIANT GOCCs 1. Al-Amanah Islamic Investment Bank of the Philippines 16. Philippine Deposit Insurance Corporation 2. Development Bank of the Philippines 17. Small Business Corporation 3. DBP Data Center, Inc. 18. Philippine Guarantee Corporation (formerly PHILEXIM) 4. Land Bank of the Philippines 19. Employees Compensation Commission 5. Land Bank Countryside Development Foundation, Inc. 20. Government Service Insurance System 6. LBP Resources and Development Corporation 21. Home Development Mutual Fund 7. Overseas Filipino Bank, Inc. 22. Philippine Health Insurance Corporation 8. Credit Information Corporation 23. Social Security System 9. DBP Leasing Corporation 24. Center for International Trade Expositions and Missions 10. LBP Insurance Brokerage, Inc. 25. Duty Free Philippines Corporation 11. -

Jennie $L Tl)F Frr:R»T«Rp

EIGHTEENTH CONGRESS OF THE ) REPUBLIC OF THE PHILIPPINES ) First Regular Session ) Jennie $l tl)f frr:r»t«rp SENATE •If OEC-9 A 9 flf P. S. RES. N 0234 RECEi (. D S'-'. Introduced by Senator JOEL VILLANUEVA RESOLUTION DIRECTING THE COMMITTEE ON LABOR, EMPLOYMENT AND HUMAN RESOURCES DEVELOPMENT, AND COMMITTEE ON BANKS, FINANCIAL INTERMEDIARIES, AND CURRENCIES, AND OTHER APPROPRIATE SENATE COMMITTEES TO INQUIRE AND REVIEW, IN AID OF LEGISLATION, THE EXTENSION OF CREDIT TO OVESEAS FILIPINOS AND OVERSEAS FILIPINO WORKERS, INCLUDING THE OPERATIONS OF THE OVERSEAS FILIPINO BANK WHEREAS, Section 35(c) of Republic Act No. 10801, otherwise known as the Overseas Workers Welfare Administration (OWWA) Act, mandates OWWA to provide low-interest loans to member-Overseas Filipino Workers; WHEREAS, Executive Order No. 44, series of 2017, acknowledges the need to establish a bank dedicated to provide financial products and services tailored to the requirements of Overseas Filipinos (OFs) and focused on delivering quality and efficient foreign remittance services. Correspondingly, Section 1 of Executive Order No. 44 directs the acquisition of the Philippines Postal Savings Bank (PPSB) by the Land Bank of the Philippines (LBP) and its conversion into an Overseas Filipino Bank, subject to the approval and/or clearance of the Bangko Sentral ng Pilipinas (BSP), Securities and Exchange Commission (SEC), Philippine Deposit Insurance Corporation (PDIC) and the Philippine Competition Commission (PCC); WHEREAS, The Overseas Filipino Bank is envisaged to be a fully “Digital Bank" servicing Overseas Filipino Workers through various electronic banking channels such as mobile phones. Automated Teller Machines (ATMs), and the internet, thereby removing the need for the establishment of physical branches and delivery of over-the-counter services.1 However, it appears that the Overseas Filipino ' “Vision and Mission." Overseas Filipino Bank. -

2016-Annual-Report.Pdf

ABOUT DOLE VISION “Every Filipino worker attains full, decent and productive employment” MISSION • To promote gainful employment opportunities; • To develop human resources; • To protect workers and promote their welfare; and • To maintain industrial peace. ORGANIZATION The DOLE has 10 agencies attached to it for program supervision and/or policy coordination, 6 Bureaus, 7 staff services, 16 regional offices, and 34 Philippine Overseas Labor Offices. It has a total manpower complement of 9,430. CLIENTS The DOLE serves 43.361 million1 workers comprising the Philippine labor force. Of this total, 40.998 million1 are employed while 2.363 million1 are unemployed. Outside the country, it serves 10.239 million2 Overseas Filipino Workers (OFWs) comprising both the temporary and irregular workers. Sources of data: 1 Current Labor Statistics (July 2017 Issue) Philippine Statistics Authority 2 Commission on Filipinos Overseas (as of December 2013 data) CONTENTS LETTER TO THE PRESIDENT SECRETARY’S MESSAGE PERFORMANCE REPORT Ensure compliance with labor laws and standards, particularly the right 01 to security of tenure Enhance workers employability and competitiveness of micro, small and 05 medium enterprises to address unemployment and underemployment 13 Strengthen protection and security of Overseas Filipino Workers 21 Strengthen social protection for vulnerable workers 25 Ensure just, simplified, and expeditious resolution of all labor disputes Achieve a sound, dynamic, and stable industrial peace with free and 27 democratic participation of workers and employers in policy and decision-making processes affecting them Streamline business processes and made frontline services responsive to 31 the people’s needs FINANCIAL REPORT DIRECTORY LETTER TO THE PRESIDENT RODRIGO ROA DUTERTE Republic of the Philippines Malacañang, Manila SIR, I am pleased to submit the Annual Report of the Department of Labor and Employment for 2016 pursuant to Section 43-46, Chapter 11, Book 1 of Executive Order No. -

Public Information and Consultation on LGU Credit Financing the Bureau of Local Government Finance

Public Information And Consultation On LGU Credit Financing The Bureau of Local Government Finance Attached agency of the DOF Supports the DOF in its mandate to “supervise the revenue operations of all local government units” • Central Office in Manila, with 15 Regional Offices • Mandated to “develop and promote plans and programs for the improvement of resource management systems, collection enforcement mechanisms and credit utilization schemes at the local levels” • Issues Certificate of Net Debt Service Ceiling (NDSC) and Borrowing Capacity (BC) to LGUs 2 Policy Thrust and Legal Framework Local Debt Policy Build capacity of local governments to borrow money to cover their expenditure responsibilities, devolved functions Prioritize financing capital infrastructure expenditure and tax flows and to foster political accountability out of these decisions National Government has to manage LGU debts to: ▪ Prevent a systemic LGU debt crisis that could force the National Government to bail out heavily indebted LGUs; ▪ Strengthen the implementation of the statutory limit on LGU debts; and ▪ Promote responsible and credible debt management among LGUs. 3 Policy Thrust and Legal Framework Legal Framework of Subnational Debts in the Philippines Sec. 296 of LGC, Art. 395 Sec. 324 of LGC LGC IRR Appropriations of 20% of the LGU’s regular income for debt LGUs may create indebtedness servicing and avail of credit facilities for local infra and socio-economic development projects with government or private banks and lending institutions Art. 403 LGC -

Securities and Exchange Commission Sec Form 17-A

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended: December 31, 2005 2. SEC Identification Number: 34001 3. BIR Tax Identification No. 000-708-174-000 4. Exact name of registrant as specified in its charter: BANCO DE ORO UNIVERSAL BANK 5. _______Manila_____________ 6. (SEC Use Only) Province, Country or other jurisdiction of incorporation or organization 7. 12 ADB Avenue, Ortigas Center, Mandaluyong City 1605 Address of principal office Postal Code 8. (632) 636-6060/ 631-7349 Registrant’s telephone number, including area code 9. Not Applicable Former name, former address, and former fiscal year, if changed since last report. 10. Securities registered pursuant to Section 4 and 8 of the SRC Title of Each Class Number of Shares Common Stock, Php10.00 par value 962,023,048 Preferred Stock, Php10.00 par value 25,000,000 11. Are any or all these securities listed on the Philippine Stock Exchange? Yes [ X ] No [ ] Philippines Stock Exchange, Common Shares 12. Check whether the registrant: a. has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11 (a)-1 and Sections 26 and 141 of the Corporation Code of the Philippines during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) Yes [ X ] No [ ] b. has been subject to such filing requirements for the past 90 days Yes [ X ] No [ ] 13. -

The Politics of Economic Reform in the Philippines the Case of Banking Sector Reform Between 1986 and 1995

The Politics of Economic Reform in the Philippines The Case of Banking Sector Reform between 1986 and 1995 A thesis submitted for the degree of PhD School of Oriental and African Studies (SOAS) University of London 2005 Shingo MIKAMO ProQuest Number: 10673052 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10673052 Published by ProQuest LLC(2017). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 2 Abstract This thesis is about the political economy of the Philippines in the process of recovery from the ruin of economic crisis in the early 1980s. It examines the dynamics of Philippine politics by focussing on banking sector reform between 1986 and 1995. After the economic turmoil of the early 1980s, the economy recovered between 1986 and 1996 under the Aquino and Ramos governments, although the country is still facing numerous economic challenges. After the "Asian currency crisis" of 1997, the economy inevitably decelerated again. However, the Philippines was seen as one of the economies least adversely affected by the rapid depreciation of its currency. The existing literature tends to stress the roles played by international financial structures, the policy preferences of the IMF, the World Bank and the US government and the interests of the dominant social force as decisive factors underlying economic and banking reform policy-making in the Philippines. -

2014 Audited Financial

A Government Savings Bank 2014 Audited Financial Statements Basis for Qualified Opinion Republic of the Philippines Loans and receivables amounting to P2.128 billion were carried at diminishing cost instead of amortized cost COMMISSION ON AUDIT using the effective interest method contrary to paragraph 9 of Philippine Accounting Standards (PAS) 39, Commonwealth Ave., Quezon City thereby affecting the fair presentation of the account in the financial statements. CORPORATE GOVERNMENT SECTOR CLUSTER 1—BANKING AND CREDIT Qualified Opinion INDEPENDENT AUDITOR’S REPORT In our opinion, except for the effects of the matters discussed in the Basis for Qualified Opinion paragraph, the financial statements present fairly, in all material respects, the financial position of Philippine Postal Savings Bank, Inc. as at December 31, 2014, and its financial performance and its cash flows for the year ended in accordance with Philippine Financial Reporting Standards. The Board of Directors Philippine Postal Savings Bank, Inc. Report on the Supplementary Information Required Under Revenue Regulations Liwasang Bonifacio, Manila 19-2011 and 15-2010 We have audited the accompanying financial statements of Philippine Postal Savings Bank, Inc., a subsidiary Our audits were conducted for the purpose of forming an opinion on the basis financial statements taken as of the Philippine Postal Corporation, which comprise the statement of financial position as at December 31, a whole. The supplementary information required under Revenue Regulations 19-2011 and 15-2010 in Note 2014, and the statement of comprehensive income, statement of changes in equity and statement of cash flows to the financial statements is presented for purposes of filing with the Bureau of Internal Revenue and is not for the year then ended, and a summary of significant accounting policies and other explanatory information. -

Strengthening Banking Regulation

Policy Brief SENATE ECONOMIC PLANNING OFFICE December 2011 PB-11-04 Strengthening Banking As the central monetary Regulation: Amending the BSP Charter authority of the country, the BSP is mandated to Introduction provide policy directions A country’s central bank serves as its foremost monetary authority. As in areas concerning such, it has three policy objectives, namely: 1) stable monetary policy; 2) money, banking and credit. strong macroeconomic fundamentals; and 3) sound financial supervision. As the Philippines’ central bank, the Bangko Sentral ng Pilipinas (BSP) With the increasing assumes the same aforementioned goals. In particular, its first and foremost liberalization of the objective is to maintain price stability conducive to a balanced and sustainable economic growth. Second, is to promote and preserve financial market, monetary stability and the convertibility of the national currency.1 conglomeration of financial institutions, With the liberalization of the financial market, conglomeration of and advancements in financial institutions, and advancements in technology, the BSP, as with 2 technology, the BSP, most central banks in the world, faces increased level of risks. Since its inception, the BSP has already hurdled two international financial crises as with most central banks (i.e., the 1997 Asian financial crisis and the 2008 global financial crisis). It in the world, also faced a number of domestic banking issues, the more recent of which faces increased level are the cases of Legacy, Banco Filipino and LBC Development Bank that of risks. drew attention to the BSP’s inadequate supervisory powers. Amid the changing financial landscape and the realization of the need to make the As such, there is a need to BSP stronger and more responsive, came the calls to amend the New Central Bank Act of 1993 (Republic Act No. -

Philhealth's Accredited Collecting Agents

No. 2018 - 0071 PHILHEALTH’S ACCREDITED COLLECTING AGENTS (Under DOF Circular 01-2017) The following are the authorized Accredited Collecting Agents of PhilHealth pursuant to the implementation of the DOF Circular 01-2017 on the use of transaction fee-based arrangement in the collection of premium contribution on October 1, 2018: Over-the-counter system 29. Saviour Rural Bank, Inc. 1. Asia United Bank 30. Bayad Center, Inc. 2. China Banking Corporation 31. SM Retail, Inc. 3. Development Bank of the Philippines 4. Land Bank of the Philippines Online system 5. Rizal Commercial Banking Corporation Bancnet Member Banks - e-Gov facility 6. United Coconut Planters Bank 1. Asia United Bank 7. Union Bank of the Philippines 2. Bank of Commerce 8. Bank of Commerce 3. BDO Unibank 9. Maybank Philippines 4. China Banking Corporation 10. Philippine Veterans Bank 5. CTBC Bank 11. Robinsons Bank Corporation 6. Development Bank of the Philippines 12. Bank One Savings & Trust Corporation 7. East West Bank 13. Century Savings Bank 8. Maybank Philippines 14. Citystate Savings Bank 9. Metropolitan Bank & Trust Company 15. Chinabank Savings, Inc. 10. MUFG Bank, Ltd. 16. Overseas Filipino Bank (Head Office only) 11. Philippine National Bank 17. Penbank, Inc. 12. RCBC Savings Bank 18. Philippine Business Bank 13. Rizal Commercial Banking Corporation 19. RCBC Savings Bank 14. Robinsons Bank Corporation 20. UCPB Savings Bank 15. United Coconut Planters Bank 21. Camalig Rural Bank 22. Century Rural Bank Other Online Payment facilities 23. East West Rural Bank, Inc. 1. Bank of the Philippine Islands - BizLink 24. Money Mall Rural Bank, Inc.