Ultra Low Emission Vans Study Final Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

New Renault TRAFIC

New Renault TRAFIC November 2019 A TRAFIC for every profession Instantly distinguishing New Renault TRAFIC is a more expressive front-end design, with full-LED headlights incorporated into the C-shaped lighting signature that represents the identity of the Renault line. A bolder grille, with details such as a new holder for the Renault logo and chrome finishing strip, plus a new ‘Urban Grey’ colour complete the revised styling. Your everyday activity is unique. New Renault TRAFIC has been reinvented in order to meet your specific needs. In its various versions, from the Panel Van to the Crew Van, you will find the one which will help you achieve the best performance. In addition to its remarkable loading capacities, it now has an updated design, a 2.0 l engine and an automatic gearbox which makes for an even smoother driving experience. A Strong personality New Renault TRAFIC re-asserts its style and stands out from the outset. The front-end panel, front grille with chrome and C-shape light signature with full LED lighting combine dynamism and robustness. More than a van, New Renault TRAFIC is designed to improve your comfort and safety. A ‘Mobile Office’ on wheels The New Renault TRAFIC has been specifically designed to meet your professional needs and provide you the ability to have a truly ‘Mobile Office’, packed with clever solutions. From tablet and smartphone cradles, to hidden laptop storage, to our integrated MediaNav system, we aim to keep you connected even when on the go. The cabin area is spacious and comfortable, creating optimal driving conditions with ergonomic seats with lumbar adjustment, adjustable steering wheel and climate control all available. -

Investment Decision Pack NGET A11.10 EV Fleet December 2019

Investment Decision Pack NGET A11.10 EV Fleet December 2019 As a part of the NGET Business Plan Submission Non-Operational Property Capex T2 Justification Paper Justification Paper Non-Operational Property Capex EV Fleet Justification Report Asset Family Fleet Vehicles Primary Investment Driver Environment Reference A11.10 Output Asset Types N/A Cost £47.49 Delivery Year(s) 2021-2026 Reporting Table D4.3a and D4.5 CAI Outputs included in T1 100% transition to EV fleet (where alternatives are available today, 2019) Business Plan T1 T2 T3 Spend Apportionment £59.30 £47.49 Unknown 1 Non-Operational Property Capex T2 Justification Paper Table of Contents Executive Summary ...................................................................................................................................... 3 Introduction ................................................................................................................................................... 3 Vehicles ........................................................................................................................................................ 4 Charging Infrastructure .................................................................................................................................. 4 Optioneering and Cost Benefit Analysis – Vehicles ....................................................................................... 5 Summary - Options considered:................................................................................................................ -

CATALOGUE of SEIZED VEHICLES SATURDAY 27Th OCTOBER 2018

31 Great Knollys Street, Reading RG1 7HU Telephone: 0118 950 8611 www.tsauction.co.uk CATALOGUE OF SEIZED VEHICLES th SATURDAY 27 OCTOBER 2018 Please note that a Buyers’ Premium of 20% (plus VAT) applies to every lot from 1701 - 1800 VAT will be added to all lots marked with a ‘v’ ALL VEHICLES ARE SOLD WITHOUT WARRANTY OR GUARANTEE AND WE STRONGLY ADVISE YOU TO READ THE SALE NOTES AND EXAMINE THE VEHICLES PRIOR TO BIDDING 1701 BMW 320 CD Sport coupe - SJ54 YYG Date of registration: 01.09.2004 1995cc, diesel, 6 speed manual, silver Odometer reading at last MOT: 95,282 miles MOT expiry date: 14.01.2019 No key, V5 available This vehicle has a broken window This vehicle was the subject of a Category D insurance loss 14.08.2008 and Category D insurance loss on 18.07.2009. 1702 Ford Mondeo GLX 5 door hatchback - T646 BUA Date of registration: 18.03.1999 1988cc, petrol, 5 speed manual, silver Odometer reading at last MOT: 99,516 miles MOT expiry date: 04.02.2018 No key, V5 available v1703 Vauxhall Combo 2000 CDTI 16V Car derived van - WR55 VTL Date of registration: 12.01.2006 1248cc, diesel, 5 speed manual, white Odometer reading at last MOT: 120,620 miles MOT expiry date: 10.01.2019 No key, V5 available 1704 Volkswagen Golf GT TDI 5 door hatchback - LS53 ENF Date of registration: 21.10.2003 1896cc, diesel, 5 speed manual, grey Odometer reading at last MOT: unknown MOT expiry date: 05.03.2019 No key, V5 available 1705 Renault Megane Privilege VVT Convertible - RF55 ZYB Date of registration: 10.11.2005 1598cc, petrol, 5 speed manual, gold Odometer -

Vehicle Registration Category and Body Type Examples

Vehicle Registration Category and Body Type Examples Registration Category Description Body Type Body Type Comments Ambulance Heavy Ambulance GVM over 4.5 tonnes Ambulance GVM up to and including 4.5 tonnes Bus GVM up to and including 4.5 tonnes Minibus GVM up to and including 4.5 tonnes Panel Van GVM up to and including 4.5 tonnes Wagon GVM up to and including 4.5 tonnes Articulated Truck Dual Purpose Truck GVM over 4.5 tonnes Prime Mover GVM over 4.5 tonnes Truck Cab'N'Chassis GVM over 4.5 tonnes Bus Minibus GVM from 4.01 tonnes up to & including 4.5 tonnes Stretch Limousine GVM from 4.01 tonnes up to & including 4.5 tonnes Wagon GVM from 4.01 tonnes up to & including 4.5 tonnes Articulated Bus GVM over 4.5 tonnes Bus GVM over 4.5 tonnes Truck Bus GVM over 4.5 tonnes Campervan/Motorhome Campervan GVM from 4.01 tonnes up to & including 4.5 tonnes Minibus GVM from 4.01 tonnes up to & including 4.5 tonnes Bus GVM over 4.5 tonnes Truk Based Motorhome GVM over 4.5 tonnes Conditional Registration Artc Water Trk E/D Restricted to 1-3 area zones Backhoe Loader Restricted to 1-3 area zones Bale Wagon Restricted to 1-3 area zones Bike Off Road Restricted to 1-3 area zones Break Pusher Restricted to 1-3 area zones Bunker Rake Restricted to 1-3 area zones Cane Plant Loader Restricted to 1-3 area zones Cane Planter Track Restricted to 1-3 area zones Chip Spreader Wheel Restricted to 1-3 area zones Compactor L/Fil Soil Restricted to 1-3 area zones Dozer Crawler/Loader Restricted to 1-3 area zones Drill\Driv Rig Track Restricted to 1-3 area zones -

Rotunda Times

Volume 2 No. 8 The Official Monthly Publication of the Ford and Mercury Restorer's Club of America. August 2013 Feature Vehicle: 1970 Mustang Fastback originallyowned by Tony Rainero My FInd I've always been fascinated with race cars. By 1972 I was bracket racing my 1966 Mustang, with some success. However, there never seemed to be enough time at the track to race which resulted in some street racing. After a couple of years I wanted to move up to stock or super stock. These were races Tony at the 1971 Summernationals classes that everyday guys could relate to and were not cost prohibitive. In the mid 70's I saw a pair of Mustang's racing out of Minot, ND at my home drag strip in Canada. One was a 1970 Fastback and the other, a 1969 Fastback. My first choice was the 1970 Fastback. But once I had made up my mind, the car had already been sold. My friend Bruce Bacon, said not to worry, because the 1969 was for sale. After making the deal on the 1969 Fastback and related spare parts, I was told the 1969 was really special because it had started life as a 1970, with $1 bill of sale from the Ford Motor Company. Upon further research I discovered this car was sponsored by Stark Hickey Ford of Royal Continued on Page 6 Jeff Gniewek parked at the Nankin Mills pavilion for the annual FMRCOA picnic and Hines Cruise Rotunda Times The Rotunda Times FMRCOA Published by: FORD AND MERCURY RESTORERS Ford and Mercury Restorers Club of America CLUB of AMERICA P.O. -

Vehicle Acquisition Report (01) 10/01/2020 to 08/31/2021 Monthly Report Vehicle Type Standard Item Quantity Percent Amount Percent

08/31/2021 03:05:31 Vehicle Acquisition Report (01) 10/01/2020 to 08/31/2021 Monthly Report Vehicle Type Standard Item Quantity Percent Amount Percent Sedans and Station Wagons 8,925 21.20% $187,809,030.73 13.31% 7 SEDAN, MINICOMPACT, 4 PASSENGER 19 0.21% $296,378.00 0.16% 7Z SEDAN, MINICOMPACT, 4 PASSENGER, 4 DOOR, EURO 59 0.66% $863,032.00 0.46% 8C SEDAN, SUBCOMPACT, 4 PASSENGER, 4 DOOR 2,601 29.14% $46,023,676.54 24.51% 8E SEDAN, SUBCOMPACT, 4 PASSENGER, ELECTRIC VEHICLE 83 0.93% $2,247,895.00 1.20% 8H SEDAN, SUBCOMPACT, 4 PASSENGER, HYBRID ELECTRIC VEHICLE 1,685 18.88% $33,599,039.00 17.89% 8P SEDAN, SUBCOMPACT, 4 PASSENGER, PLUG-IN HEV 50 0.56% $1,230,342.00 0.66% 8Z SEDAN, SUBCOMPACT, 4 PASSENGER, 4 DOOR, DIESEL, EURO 143 1.60% $2,511,187.00 1.34% 9C SEDAN, COMPACT, 5 PASSENGER, 4 DOOR, 4 CYL ENGINE 1,465 16.41% $29,544,249.19 15.73% 9H SEDAN, COMPACT, 5 PASSENGER, HYBRID ELECTRIC VEHICLE 1,308 14.66% $30,965,778.00 16.49% 9Z SEDAN, COMPACT, 5 PASSENGER, 4 DOOR, 4 CYL ENGINE, EURO 93 1.04% $2,053,640.00 1.09% 10B SEDAN, MIDSIZE, 5 PASSENGER, 4 DOOR 1,128 12.64% $33,003,769.00 17.57% 12A STATION WAGON, SUBCOMPACT, 4 PASSENGER, 4 DOOR 1 0.01% $18,240.00 0.01% 12Z STATION WAGON, SUBCOMPACT, 5 PASSENGER, 4 DOOR, EURO 253 2.83% $4,618,855.00 2.46% 13Z STATION WAGON, COMPACT, 5 PASSENGER, 4 DOOR, EURO 37 0.41% $832,950.00 0.44% Police Use Vehicles 1,781 4.23% $77,814,139.00 5.51% 17 SEDAN, POLICE USE, 4 DOOR 267 14.99% $9,981,598.00 12.83% 17H SEDAN, HYBRID ELECTRIC, POLICE USE, 4 DOOR 0 0.00% -$73,920.00 -0.09% 17Z SEDAN, LAW ENFORCEMENT -

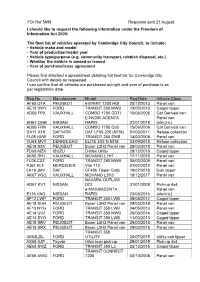

FOI Ref 5698 Response Sent 21 August I Should Like to Request The

FOI Ref 5698 Response sent 21 August I should like to request the following information under the Freedom of Information Act 2000: The fleet list of vehicles operated by Cambridge City Council, to include: • Vehicle make and model • Year of production/model year • Vehicle type/purpose (e.g. community transport, rubbish disposal, etc.) • Whether the vehicle is owned or leased • Year of purchase/lease agreement Please find attached a spreadsheet detailing full fleet list for Cambridge City Council with details as requested. I can confirm that all vehicles are purchased outright and year of purchase is as per registration date. Reg No Manufacturer Model Reg.Date Vehicle Class AF63 OTA PEUGEOT EXPERT 1200 HDI 20/12/2013 Panel van AE13 SWY FORD TRANSIT 350 MWB 13/03/2013 Caged tipper AD06 FPX VAUXHALL COMBO 1700 CDTI 15/06/2006 Car Derived van E-NV200 ACENTA Panel van EN67 OGB NISSAN RAPID 31/01/2018 (electric) AD06 FRN VAUXHALL COMBO 1700 Cdti 15/06/2006 Car Derived van DX11 ATK DAF/NTM DAF LF55.220 (NTM) 01/03/2011 Refuse collection FL08 HXW FORD TRANSIT 280 SWB 14/03/2008 Panel van VU68 MVY DENNIS EAG ELITE 4X2 N NTM 03/09/2018 Refuse collection AE18 SSV PEUGEOT Boxer L2H2 Panel van 29/03/2018 Panel van FD68 MZX ISUZU D-Max Utility 28/12/2018 Caged tipper AK66 SHJ VAUXHALL MOVANO L1H1 17/11/2016 Panel van FL08 CZZ FORD TRANSIT 260 MWB 05/03/2008 Panel van PJ61 KLF MERCEDES Vito 113 01/02/2012 Panel van LK18 JMV DAF CF400 Tipper Grab 18/07/2018 Bulk tipper AK67 VGO VAUXHALL MOVANO L3H3 18/12/2017 Panel van NAVARA OUTLAW AD57 KVT NISSAN DCI -

Caddy Panel Van

Caddy Panel Van Caddy Panel Van Specifications X = standard O = optional - = not available Caddy Panel Van Caddy Panel Van Caddy Panel Van Specification 1.6i 81kW 2.0 TDI 81kW SWB SWB Engine Cylinders 4 4 Capacity (cm3) 1598 1968 Output (kW @ r/min) 81 @ 5800 81 @ 4200 Torque (Nm @ r/min) 155 @ 3800-4000 250 @ 1500-2500 CO2 emissions (g/km)* 164 147 Transmission 5-speed manual X X 6-speed DSG® - - Performance Acceleration in seconds (0-100 km/h) 12,5 11,8 Top speed (km/h) 172 170 Fuel Consumption Urban cycle (litres/100 km)* 9,3 6,9 Extra-urban cycle (litres/100 km)* 6,1 5,0 Combined cycle (litres/100 km)* 7,3 5,7 Running Gear Standard suspension and shock absorption X X Brakes ABS (Anti-lock Braking System) X X MCB (Automatic Post-collision Braking System) X X ESP (Electronic Stability Programme) X X EDL (Electronic Differential Lock) X X TCS (Traction Control System) X X Hill-hold control - - Wheelrims/Tyres 15" steel wheels X X 16” steel wheels - - 16” ‘Fortaleza’ alloy wheels - - Tyres 195/65 R15 91T X X Tyres 205/55 R16 94T O O Full-sized spare wheel (steel) X X Full-sized spare wheel (alloy) - - Dimensions/Capacities Fuel tank (litres) 55 55 Length (mm) 4408 4408 Width excl. mirrors (mm) 1793 1793 Width incl. mirrors (mm) 2065 2065 Height excl. roof rails (mm) 1823 1823 Height incl. roof rails (mm) 1860 1860 Wheelbase (mm) 2682 2682 Caddy Panel Van Specifications X = standard O = optional - = not available Caddy Panel Van Caddy Panel Van Caddy Panel Van Specification 1.6i 81kW 2.0 TDI 81kW SWB SWB Dimension / Capacities (continued) Ramp angle (degrees) 14,0 14,0 Departure angle (degrees) 17,3 17,3 Turning circle (m) 11,1 11,1 Load compartment width, min./max. -

Series List Template

__________________________________________________________________ THE HOLDEN COLLECTION BRG 213 WOODVILLE PLANT Series 77 Series list _____________________________________________________________ When Holden Motor Body Builders outgrew their premises in King William Street South they looked beyond the city for a site suitable for a large factory, close to transport and with room for some expansion. In 1922 the Grenfell St works were closed, and in 1923 King William Street was expanded and a new factory at Woodville was opened. The Woodville factory became the sole production site Australian produced GM vehicles and the company’s expansion was on the back of this. By 1931 the depression was hitting HMBB hard and production levels had plummetd to unsustainable levels. The 1931 merge with GM resulting in the new company of General Motors –Holden’s saved the company, jobs and the Woodville factory. The Woodville factory continued to play an important role in Holden’s production despite the move of headquarters to Melbourne. As a large, advanced and efficient factory production levels remained high throughout the pre war, war and post war years, particularly with the introduction of the All Australian car the Holden 48-215 in 1948. With company restricturing and rationalisation in the late 1970s and 1980s GMH closed many smaller factories around the country. In South Australia the Woodville factory had expanded to its boundaries and capacity and was competing with the newer Elizabeth plant which did not have the disadvantage of being in a built up area with defined limits on expansion. Production levels were gradually reduced and activities and equipment transferred to the Elizabeth plant. -

The Crafter Panel Van Price List Build Find a Offers & Test Drive Conversions Your Own Tour Centre Finance Model Prices

The Crafter panel van Price list Build Find a Offers & Test drive Conversions your own Tour Centre Finance Model prices *Manufacturer’s on the road (OTR) package Model CR30 and CR35 CR50 Delivery to Van Centre £620.00 £620.00 Number plates £20.00 £20.00 VAT £128.00 £128.00 First registration fee £55.00 £55.00 Vehicle excise duty (VED) 1st year £275.00 £165.00 Basic OTR price (exc. VAT) £970.00 £860.00 Total OTR price (inc. VAT) £1,098.00 £988.00 Volkswagen Commercial Vehicles may change RRPs at any time (this includes where there are government changes in regulation and/or legislation). There may be a delay to any RRP displaying correctly on our materials. Always obtain prices from your chosen authorised Van Centre. Crafter panel van Crafter panel van Crafter panel van Crafter Panel van prices Business Pack options converter options •••• Build Find a Offers & Test drive Conversions your own Tour Centre Finance Panel van model prices Basic Total Total RRP inc. OTR* Total RRP inc. OTR* Trimline Engine/transmission/drive system exc. VAT inc. VAT exc. VAT inc. VAT Startline medium wheelbase with high roof CR30 2.0TDI 102PS FWD 6-speed manual £28,845.00 £34,614.00 £29,815.00 £35,712.00 CR35 2.0TDI 102PS FWD 6-speed manual £31,745.00 £38,094.00 £32,715.00 £39,192.00 2.0TDI 140PS FWD 6-speed manual £33,270.00 £39,924.00 £34,240.00 £41,022.00 2.0TDI 140PS 4MOTION 6-speed manual £39,350.00 £47,220.00 £40,320.00 £48,318.00 2.0TDI 140PS FWD 8-speed automatic £35,140.00 £42,168.00 £36,110.00 £43,266.00 2.0TDI 140PS RWD 6-speed manual £32,805.00 £39,366.00 -

FS-14 Trade-In Credit Limit Frequently Asked Questions

Illinois Department of Revenue Trade-In Credit Limit Frequently Asked Questions These FAQ’s are a supplement for Informational Bulletin FY 2020-1, Change to Credit Allowed for Traded-In First Division Motor Vehicles. What has changed with regard to the trade-in credit for Sales and Use Tax due on motor vehicles? Effective January 1, 2020, Public Act (P.A.) 101-0031 amended the Retailers’ Occupation Tax Act and the Use Tax Act to redefine the “selling price” subject to Sales and Use Taxes for sales and purchases of motor vehicles when a customer trades in a first division motor vehicle. Under this new definition, “selling price” includes the value of or credit given for traded-in first division motor vehicles exceeding $10,000. Beginning January 1, 2020, trade-in credit may not be taken for that portion of the value of or credit given for a traded-in first division motor vehicle of like kind and character as that being sold that exceeds $10,000. What this means for motor vehicle dealers is that $10,000 is the maximum credit the retailer may take on the applicable return (Form ST-556, Sales Tax Transaction Return, or Form ST-556-LSE, Transaction Return for Leases) to reduce the taxable selling price of a motor vehicle when that retailer accepts the trade in of a first division motor vehicle in the transaction, regardless of the value of or credit given for the trade in. This does not prohibit the retailer from reducing the price of the vehicle being sold by the value of or credit given for the traded-in motor vehicle. -

THE MAN TGE. Technical Data

THE MAN TGE. Technical data. Valid from 1 March 2019. DRIVELINE. Diesel engines 2,0 l 75 kW 2,0 l 90 kW 2,0 l 103 kW 2,0 l 130 kW Electric motor 100 kW Displacement [cm³] 1,968 1,968 1,968 1,968 Engine Permanent magnet Number of cylinders 4 4 4 4 synchronous machine max. power output max. power output [kW [kW (PS)] 75 (102) 90 (122) 103 (140) 130 (177) (PS)] 100 (136) at speed [rpm] 3,000 – 3,500 3,500 3,500 – 3,600 3,600 at speed [rpm] 3,300 – 11,700 max. torque [Nm] 300 300 340 410 max. torque [Nm] 290 at speed [rpm] 1,400 – 2,250 1,400 – 2,250 1,600 – 2,250 1,500 – 2,000 at speed [rpm] 0 – 3,300 Exhaust-gas category Euro 6 EURO VI Euro 6 Euro 6 / EURO VI Nominal capacity [kWh] 35.8 Fuel type Diesel as per DIN EN 590 Diesel as per DIN EN 590 Diesel as per DIN EN 590 Diesel as per DIN EN 590 Fuel type Electricity 6-speed manual gearbox 6-speed manual gearbox Gearbox variants 6-speed manual gearbox 6-speed manual gearbox 8-speed automatic gear- 8-speed automatic gear- Gearbox variant 1-speed gearbox box1 box Driveline Front-wheel drive Rear-wheel drive with Front-wheel drive Front-wheel drive max. range [km] 173 twin tyres All-wheel drive All-wheel drive Battery Lithium ion Rear-wheel drive with Rear-wheel drive with single tyres single tyres Charging Alternating current (AC)2 Rear-wheel drive with twin Direct current (DC)3 tyres 2.0 l (Euro 6) 2.0 l (EURO VI) 2.0 l (Euro 6) 2.0 l (Euro 6/EURO VI) 100 kW (electric motor) 140 140 140 140 140 130 kW 130 130 130 130 130 120 120 120 120 120 75 kW 110 90 kW 110 110 110 110 103 kW 103 kW 130