Sprott Gold Report June 22, 2018 Market Stress

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

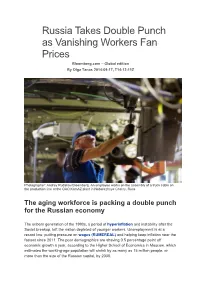

Russia Takes Double Punch As Vanishing Workers Fan Prices Bloomberg.Com – Global Edition by Olga Tanas 2014-09-17, T14:12:11Z

Russia Takes Double Punch as Vanishing Workers Fan Prices Bloomberg.com – Global edition By Olga Tanas 2014-09-17, T14:12:11Z Photographer: Andrey Rudakov/Bloomberg. An employee works on the assembly of a truck cabin on the production line at the OAO KamAZ plant in Naberezhnye Chelny, Russ The aging workforce is packing a double punch for the Russian economy The unborn generation of the 1990s, a period of hyperinflation and instability after the Soviet breakup, left the nation depleted of younger workers. Unemployment is at a record low, putting pressure on wages (RUMEREAL) and helping keep inflation near the fastest since 2011. The poor demographics are shaving 0.5 percentage point off economic growth a year, according to the Higher School of Economics in Moscow, which estimates the working-age population will shrink by as many as 15 million people, or more than the size of the Russian capital, by 2030. Aging populations are unsettling central bankers from Tokyo to Frankfurt in their struggle to prevent deflation as older workers tend to defer consumption in favor of savings. Russia faces the opposite threat: entrenched inflation that risks shackling monetary policy already lurching from one crisis to another since Crimea was annexed in March. “Taking into account low unemployment and tight supply on the labor market, wages will remain at a high level, affecting inflation,” said Natalia Orlova, chief economist at Alfa Bank in Moscow. With the central bank increasingly drawing attention to poor demographics, it’s “in effect saying it can do nothing for the economy, whose problems are structural in character.” Demographic Factor Russia is caught in a vise of elevated inflation and stalling economic growth. -

Russia's 2020 Strategic Economic Goals and the Role of International

Russia’s 2020 Strategic Economic Goals and the Role of International Integration 1800 K Street NW | Washington, DC 20006 Tel: (202) 887-0200 | Fax: (202) 775-3199 E-mail: [email protected] | Web: www.csis.org authors Andrew C. Kuchins Amy Beavin Anna Bryndza project codirectors Andrew C. Kuchins Thomas Gomart july 2008 europe, russia, and the united states ISBN 978-0-89206-547-9 finding a new balance Ë|xHSKITCy065479zv*:+:!:+:! CENTER FOR STRATEGIC & CSIS INTERNATIONAL STUDIES Russia’s 2020 Strategic Economic Goals and the Role of International Integration authors Andrew C. Kuchins Amy Beavin Anna Bryndza project codirectors Andrew C. Kuchins Thomas Gomart july 2008 About CSIS In an era of ever-changing global opportunities and challenges, the Center for Strategic and International Studies (CSIS) provides strategic insights and practical policy solutions to decisionmakers. CSIS conducts research and analysis and develops policy initiatives that look into the future and anticipate change. Founded by David M. Abshire and Admiral Arleigh Burke at the height of the Cold War, CSIS was dedicated to the simple but urgent goal of finding ways for America to survive as a nation and prosper as a people. Since 1962, CSIS has grown to become one of the world’s preeminent public policy institutions. Today, CSIS is a bipartisan, nonprofit organization headquartered in Washington, DC. More than 220 full- time staff and a large network of affiliated scholars focus their expertise on defense and security; on the world’s regions and the unique challenges inherent to them; and on the issues that know no boundary in an increasingly connected world. -

8-11 July 2021 Venice - Italy

3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING AND SIDE EVENTS 8-11 July 2021 Venice - Italy 1 CONTENTS 1 ABOUT THE G20 Pag. 3 2 ITALIAN G20 PRESIDENCY Pag. 4 3 2021 G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETINGS Pag. 4 4 3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING Pag. 6 Agenda Participants 5 MEDIA Pag. 13 Accreditation Media opportunities Media centre - Map - Operating hours - Facilities and services - Media liaison officers - Information technology - Interview rooms - Host broadcaster and photographer - Venue access Host city: Venice Reach and move in Venice - Airport - Trains - Public transports - Taxi Accomodation Climate & time zone Accessibility, special requirements and emergency phone numbers 6 COVID-19 PROCEDURE Pag. 26 7 CONTACTS Pag. 26 2 1 ABOUT THE G20 Population Economy Trade 60% of the world population 80 of global GDP 75% of global exports The G20 is the international forum How the G20 works that brings together the world’s major The G20 does not have a permanent economies. Its members account for more secretariat: its agenda and activities are than 80% of world GDP, 75% of global trade established by the rotating Presidencies, in and 60% of the population of the planet. cooperation with the membership. The forum has met every year since 1999 A “Troika”, represented by the country that and includes, since 2008, a yearly Summit, holds the Presidency, its predecessor and with the participation of the respective its successor, works to ensure continuity Heads of State and Government. within the G20. The Troika countries are currently Saudi Arabia, Italy and Indonesia. -

Russia's International Activity in Response to the Global Financial

BULLETIN No. 37 (37) June 25, 2009 © PISM Editors: Sławomir Dębski (Editor-in-Chief), Łukasz Adamski, Bartosz Cichocki, Mateusz Gniazdowski, Beata Górka-Winter, Leszek Jesień, Agnieszka Kondek (Executive Editor), Łukasz Kulesa, Ernest Wyciszkiewicz Russia’s International Activity in Response to the Global Financial Crisis by Jarosław Ćwiek-Karpowicz Russia has striven to exploit the global financial crisis to bolster its international position. The build- ing of an international coalition of developing states, which Russia wants to head, is a means to that end. Among other things, the Russian authorities have championed new regional powers’ increased participation in international financial institutions, at the expense of the U.S. and other Western state. These efforts of the Russian Federation are laden with the risk of failure, primarily because of the Russia’s weak economic potential and vastly diverse interests of the prospective coalition members. This June Russia launched a major push on the international forum. Representatives of global business, science and politics had an opportunity to exchange views during the St. Petersburg International Economic Forum (4–6 June) dubbed “a Russian Davos.” Several days later Moscow hosted a summit of the Collective Security Treaty Organization (CSTO) and a meeting of the Inter- state Council of the Euro-Asian Economic Community (EAEC)—two foremost (from Russia’s pers- pective) initiatives to reintegrate the post-Soviet area. From there, the leaders of China, Russia, India, Brazil, Pakistan, Afghanistan and the Central Asian states met in Yekaterinburg (16–17 June) at Shanghai Cooperation Organization (SCO) and Brazil–Russia–India–China (BRIC) summits. A majority of these meetings were attended by Russian President Dmitry Medvedev whose addresses were focused on international financial crisis issues and on the need to overhaul the international financial system. -

Domestic Gas Prices in Russia – Towards Export Netback?

Domestic Gas Prices in Russia – Towards Export Netback? James Henderson NG 57 November 2011 i The contents of this paper are the authors’ sole responsibility. They do not necessarily represent the views of the Oxford Institute for Energy Studies or any of its members. Copyright © 2011 Oxford Institute for Energy Studies (Registered Charity, No. 286084) This publication may be reproduced in part for educational or non‐profit purposes without special permission from the copyright holder, provided acknowledgment of the source is made. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the Oxford Institute for Energy Studies. ISBN 978‐1‐907555‐38‐1 ii Preface While most of the publicity and focus of Russian and CIS gas research is on exports to Europe and other potential markets, over the past few years OIES Gas Programme research has increasingly concentrated on domestic gas markets in these countries, especially the Russian Federation. With Russian gas demand in excess of 400 Bcm/year, the issue of how gas should be priced is of considerable importance, particularly given the start of much higher cost Gazprom production from Arctic fields in 2012. The announcement in 2006 that Russian domestic prices would be raised to European netback levels by 2011 caused much excitement both within and outside Russia. The reality has been less dramatic but as Jim Henderson ably demonstrates this is partly because of completely unforeseen developments in European gas pricing, largely driven by higher oil price levels than anybody believed possible five years ago. -

Miller - Russias Frozen Economy

DECEMBER 2014 RUSSIA’S FROZEN ECONOMY By Chris Miller Chris Miller, Associate Scholar of the Foreign Policy Research Institute, is a Ph.D. candidate at Yale. In 2012- 2014, he worked as a visiting researcher at the Carnegie Moscow Center while on an Alfa Fellowship and taught history at the New Economic School, a university in Moscow. He is currently completing a book manuscript on the collapse of the Soviet Union. December temperatures in Russia’s Siberian cities often reach 40 below zero, but the freeze that threatens Russia today has nothing to do with the winter cold. Russia’s economy is frozen. Western sanctions designed to punish Russia for invading Ukraine have deterred investment, while plummeting oil prices have substantially reduced Russia’s main source of export revenue. GDP growth will be basically flat this year, and will be no better in 2015. The rise in living standards, the foundation of Russian President Vladimir Putin’s popularity, has ground to a halt. At the trough of the 2008-2009 crisis, Russia’s economy performed worse, but it was clear that the financial crisis was caused by external factors. Today the opposite is true. Sanctions and a worsening business climate are direct consequences of Vladimir Putin’s policies. Even the shock created by declining oil export revenues, which is caused by global supply and demand factors, reflects poorly on Putin, because despite the advice of many economists he has declined to diversify Russia’s economy away from energy exports. That now looks foolish. The deep freeze gripping Russia is not simply an economic problem. -

The International Monetary and Financial

April 2016 The Bulletin Vol. 7 Ed. 4 Official monetary and financial institutions ▪ Asset management ▪ Global money and credit Lagarde’s lead Women in central banks Ezechiel Copic on gold’s boost from negative rates José Manuel González-Páramo on monetary policy Michael Kalavritinos on Latin American funds Christian Noyer on threat to London’s euro role Paul Tucker on geopolitics and the dollar You don’t thrive for 230 years by standing still. As one of the oldest, continuously operating financial institutions in the world, BNY Mellon has endured and prospered through every economic turn and market move since our founding over 230 years ago. Today, BNY Mellon remains strong and innovative, providing investment management and investment services that help our clients to invest, conduct business and transact with assurance in markets all over the world. bnymellon.com ©2016 The Bank of New York Mellon Corporation. All rights reserved. BNY Mellon is the corporate brand for The Bank of New York Mellon Corporation. The Bank of New York Mellon is supervised and regulated by the New York State Department of Financial Services and the Federal Reserve and authorised by the Prudential Regulation Authority. The Bank of New York Mellon London branch is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request. Products and services referred to herein are provided by The Bank of New York Mellon Corporation and its subsidiaries. Content is provided for informational purposes only and is not intended to provide authoritative financial, legal, regulatory or other professional advice. -

Russia's "Pivot" to Eurasia

RUSSIA’S “PIVOT” TO EURASIA edited by Kadri Liik ABOUT ECFR The European Council on Foreign Relations (ECFR) is the first pan-European think-tank. Launched in October 2007, its objective is to conduct research and promote informed debate across Europe on the development of coherent, effective and values-based European foreign policy. ECFR has developed a strategy with three distinctive elements that define its activities: • A pan-European Council. ECFR has brought together a distinguished Council of over two hundred Members – politicians, decision makers, thinkers and business people from the EU’s member states and candidate countries – which meets once a year as a full body. Through geographical and thematic task forces, members provide ECFR staff with advice and feedback on policy ideas and help with ECFR’s activities within their own countries. The Council is chaired by Martti Ahtisaari and Mabel van Oranje. • A physical presence in the main EU member states. ECFR, uniquely among European think-tanks, has offices in Berlin, London, Madrid, Paris, Rome, Sofia and Warsaw. Our offices are platforms for research, debate, advocacy and communications. • A distinctive research and policy development process. ECFR has brought together a team of distinguished researchers and practitioners from all over Europe to advance its objectives through innovative projects with a pan-European focus. ECFR’s activities include primary research, publication of policy reports, private meetings and public debates, ‘friends of ECFR’ gatherings in EU capitals and outreach to strategic media outlets. ECFR is a registered charity funded by the Open Society Foundations and other generous foundations, individuals and corporate entities. -

Russia Selective Capitalism and Kleptocracy

21st Century Authoritarians Freedom House Radio Free Europe/Radio Liberty Radio Free Asia JUNE 2009 FFH_UD7.inddH_UD7.indd iiiiii 55/22/09/22/09 111:221:22 AAMM RUSSIA SELECTIVE CAPITALISM AND KLEPTOCRACY Daniel Kimmage The Kremlin deploys the conceptual vocabulary of the new Russia—national renewal, anti-Western xenophobia, sovereign democracy—through a sophis- ticated domestic communications strategy that marshals both the traditional state resources and much-expanded control over virtually all mainstream mass media. This one-two punch, coming amid a period of rising prosperity, has had a signifi cant impact on popular opinion, and the Kremlin’s message has resonated with its intended recipients. introduction When Russian tanks halted their advance a few kilometers from Tbilisi in August 2008, with the Georgian army in full fl ight and Georgia’s allies in Europe and the United States reduced to fulmination, the global consensus on the meaning of the invasion was swift and bracing: Russia was back, a force to be reckoned with, and intent on reclaiming its lost share of import and infl uence among nations. This consensus is as wrongheaded and simplistic as the previous incarnations of con- ventional wisdom it has replaced: fi rst, that Russia was engaged in a rollicking, rollercoaster transition from communist torpor to liberal democracy and a free-market economy, and then, when that fi ne vision foundered in fi nancial crisis and sundry misadventures toward the end of the 1990s, that Russia had become mired in some intermediary phase of its supposed transition and might soon slink off history’s grand stage altogether. -

Global Finance's Central Banker Report Cards 2020

Global Finance’s Central Banker Report Cards 2020 NEW YORK, September 16, 2020 — Global Finance magazine has released the names of Central Bank Governors who earned ‘A’ or ‘A-’ grades as part of its Central Banker Report Cards 2020. The full Central Banker Report Cards 2020 report and grade list will appear in Global Finance’s October print and digital issues and online at GFMag.com. The Central Banker Report Cards, published annually by Global Finance since 1994, grade the central bank governors of more than 90 key countries as well as the European Union, the Eastern Caribbean Central Bank, the Bank of Central African States and the Central Bank of West African About Global Finance States. Global Finance, founded in 1987, has a circulation of Grades are based on an “A” to “F” scale for success in areas such as inflation control, economic 50,000 and readers in 191 growth goals, currency stability and interest rate management. (“A” represents an excellent countries. Global Finance’s performance down through “F” for outright failure.) Subjective criteria also apply. audience includes senior corporate and financial “Even in good times, central bankers face an array of challenges. Today, with a global health crisis officers responsible for making sweeping the world, they are squeezed between political and practical realities like they never investment and strategic have before,” said Global Finance publisher and editorial director Joseph Giarraputo. “Our annual decisions at multinational Central Banker Report Cards analyze which countries have sound leadership at the economic companies and financial helm, showcasing policy stances that work.” institutions. -

Emerging Countries in Global Financial Standard Setting: Explaining Relative Resilience and Its Implications

SPECIAL REPORT Emerging Countries in Global Financial Standard Setting: Explaining Relative Resilience and Its Implications Andrew Walter SPECIAL REPORT Emerging Countries in Global Financial Standard Setting: Explaining Relative Resilience and Its Implications Andrew Walter About CIGI Credits We are the Centre for International Governance Innovation: an independent, Director, Global Economy Robert Fay non-partisan think tank with an objective and uniquely global perspective. Our Program Manager Heather McNorgan research, opinions and public voice make a difference in today’s world by bringing clarity and innovative thinking to global policy making. By working Publisher Carol Bonnett across disciplines and in partnership with the best peers and experts, we are the Senior Publications Editor Jennifer Goyder benchmark for influential research and trusted analysis. Graphic Designer Brooklynn Schwartz Our research initiatives focus on governance of the global economy, global security and politics, and international law in collaboration with a range of strategic partners and have received support from the Government of Canada, the Government of Ontario, as well as founder Jim Balsillie. À propos du CIGI Au Centre pour l'innovation dans la gouvernance internationale (CIGI), nous formons un groupe de réflexion indépendant et non partisan doté d’un point de vue objectif et unique de portée mondiale. Nos recherches, nos avis et nos interventions publiques ont des effets réels sur le monde d'aujourd’hui car ils apportent de la clarté et une réflexion novatrice pour l’élaboration des politiques à l’échelle internationale. En raison des travaux accomplis en collaboration et en partenariat avec des pairs et des spécialistes interdisciplinaires des plus compétents, nous sommes devenus une référence grâce à l’influence de nos recherches et à la fiabilité de nos analyses. -

Appeared In: European Energy Review

Appeared in: European Energy Review http://www.europeanenergyreview.eu/site/pagina.php?id=3899 Putin increases control over Russian energy By Alexander Gusev Russian President Vladimir Putin has recently created a new Energy Commission by which he is seeking to wrest control over the energy sector from the government of Prime Minister Dmitry Medvedev. This move will lead to a further strengthening of the role of the State in the Russian oil and gas industry. It is bad news for those who are hoping for a more transparent investment climate, argues Alexander Gusev, Research Fellow at the German Institute for International and Security Affairs (SWP). On May 7, 2012, Vladimir Putin returned as President of Russia, swapping roles with his predecessor, Dmitry Medvedev, who took over as Prime Minister. There have been many speculations about the distribution of powers between the two. Since political power in Russia is to a large extent determined by control over energy resources, any institutional changes in this sphere create a new balance of powers. At the annual congress of United Russia, the dominant political party, in September last year, Medvedev put forward Putin as the Presidential candidate, emphasizing that it was “a deeply thought-out decision” discussed “as early as when our union was being formed.” In turn Putin expressed his confidence that Medvedev would form a “new, effective, young and energetic” cabinet and “continue his work on modernizing all aspects of our lives.” Despite the close personal ties between the two politicians, they do represent different camps in the Russian power structure and it is pertinent to ask who makes the decisions in the Russian energy field, keeping in mind that how the decision-making process is organized formally is different from how it works in practice.