Flying Efficiently 2014 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1.1.3 Helicopters

Information on the Company’s Activities / 1.1 Presentation of the Company 1.1.3 Helicopters Airbus Helicopters is a global leader in the civil and military The HIL programme, for which the Airbus Helicopters’ H160 rotorcraft market, offering one of the most complete and modern was selected in 2017, was initially scheduled for launch range of helicopters and related services. This product range in 2022 by the current military budget law. Launching the currently includes light single-engine, light twin-engine, medium programme earlier will enable delivery of the fi rst H160Ms to and medium-heavy rotorcraft, which are adaptable to all kinds of the French Armed Forces to be advanced to 2026. The H160 mission types based on customer needs. See “— 1.1.1 Overview” was designed to be a modular helicopter, enabling its military for an introduction to Airbus Helicopters. version, with a single platform, to perform missions ranging from commando infi ltration to air intercept, fi re support, and anti-ship warfare in order to meet the needs of the army, the Strategy navy and the air force through the HIL programme. The new fi ve-bladed H145 is on track for EASA and FAA Business Ambition certifi cation in 2020. To ensure these certifi cations, two fi ve- bladed prototypes have clocked more than 400 fl ight hours Airbus Helicopters continues to execute its ambition to lead the in extensive fl ight test campaigns in Germany, France, Spain, helicopter market, build end-to-end solutions and grow new Finland, and in South America. First deliveries of the new H145 VTOL businesses, while being fi nancially sound. -

OSB Representative Participant List by Industry

OSB Representative Participant List by Industry Aerospace • KAWASAKI • VOLVO • CATERPILLAR • ADVANCED COATING • KEDDEG COMPANY • XI'AN AIRCRAFT INDUSTRY • CHINA FAW GROUP TECHNOLOGIES GROUP • KOREAN AIRLINES • CHINA INTERNATIONAL Agriculture • AIRBUS MARINE CONTAINERS • L3 COMMUNICATIONS • AIRCELLE • AGRICOLA FORNACE • CHRYSLER • LOCKHEED MARTIN • ALLIANT TECHSYSTEMS • CARGILL • COMMERCIAL VEHICLE • M7 AEROSPACE GROUP • AVICHINA • E. RITTER & COMPANY • • MESSIER-BUGATTI- CONTINENTAL AIRLINES • BAE SYSTEMS • EXOPLAST DOWTY • CONTINENTAL • BE AEROSPACE • MITSUBISHI HEAVY • JOHN DEERE AUTOMOTIVE INDUSTRIES • • BELL HELICOPTER • MAUI PINEAPPLE CONTINENTAL • NASA COMPANY AUTOMOTIVE SYSTEMS • BOMBARDIER • • NGC INTEGRATED • USDA COOPER-STANDARD • CAE SYSTEMS AUTOMOTIVE Automotive • • CORNING • CESSNA AIRCRAFT NORTHROP GRUMMAN • AGCO • COMPANY • PRECISION CASTPARTS COSMA INDUSTRIAL DO • COBHAM CORP. • ALLIED SPECIALTY BRASIL • VEHICLES • CRP INDUSTRIES • COMAC RAYTHEON • AMSTED INDUSTRIES • • CUMMINS • DANAHER RAYTHEON E-SYSTEMS • ANHUI JIANGHUAI • • DAF TRUCKS • DASSAULT AVIATION RAYTHEON MISSLE AUTOMOBILE SYSTEMS COMPANY • • ARVINMERITOR DAIHATSU MOTOR • EATON • RAYTHEON NCS • • ASHOK LEYLAND DAIMLER • EMBRAER • RAYTHEON RMS • • ATC LOGISTICS & DALPHI METAL ESPANA • EUROPEAN AERONAUTIC • ROLLS-ROYCE DEFENCE AND SPACE ELECTRONICS • DANA HOLDING COMPANY • ROTORCRAFT • AUDI CORPORATION • FINMECCANICA ENTERPRISES • • AUTOZONE DANA INDÚSTRIAS • SAAB • FLIR SYSTEMS • • BAE SYSTEMS DELPHI • SMITH'S DETECTION • FUJI • • BECK/ARNLEY DENSO CORPORATION -

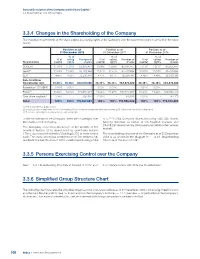

3.3.4 Changes in the Shareholding of the Company

General Description of the Company and its Share Capital / 3.3 Shareholdings and Voting Rights 3.3.4 Changes in the Shareholding of the Company The evolution in ownership of the share capital and voting rights of the Company over the past three years is set forth in the table below: Position as of Position as of Position as of 31 December 2018 31 December 2017 31 December 2016 % of % of % of % of voting Number of % of voting Number of % of voting Number of Shareholders capital rights shares capital rights shares capital rights shares SOGEPA 11.06% 11.06 % 85,835,477 11.08% 11.08% 85,835,477 11.11% 11.11% 85,835,477 GZBV(1) 11.04% 11.04 %85,709,82211.07% 11.07% 85,709,822 11.09% 11.09% 85,709,822 SEPI 4.16% 4.16 %32,330,381 4.17% 4.17% 32,330,381 4.18% 4.18% 32,330,381 Sub-total New Shareholder Agt. 26.26% 26.28% 203,875,680 26.32% 26.33% 203,875,680 26.38% 26.38% 203,875,680 Foundation “SOGEPA” 0.00% 0.00% 0 0.00% 0.00% - 0.00% 0.00% 0 Public(2) 73.66% 73.72% 571,855,277 73.66% 73.67% 570,550,857 73.60% 73.62% 568,853,019 Own share buyback(3) 0.08% - 636,924 0.02% - 129,525 0.02% - 184,170 Total 100% 100% 776,367,881 100% 100% 774,556,062 100% 100% 772,912,869 (1) KfW & other German public entities. -

Biodiversity and Ecosystem Services Scaling up Business Solutions

business solutions for a sustainable world Biodiversity and ecosystem services scaling up business solutions Company case studies that help achieve global biodiversity targets Contents Scale up, speed up and put the sound up ....... 2 15 PUMA – The Environmental Profi t & Loss Account..........................................................................................................................36 Business, biodiversity and ecosystem 16 Reliance Industries – Converting Wastelands to services in a nutshell ........................................................................... 3 Green Oases ..............................................................................................................40 17 Rio Tinto – Achieving the Goal of Net Positive Impact What are the Aichi Targets? .................................................... 4 on Biodiversity ........................................................................................................42 On the ground business actions ...................................... 6 18 Shell – Corrib Paves the Way – A Response that Bears Re-Peating ...................................................................................................................44 Case Studies ....................................................................................................... 8 19 Suncor Energy – Oil Sands Reclamation 1 ArcelorMittal – Mining in Liberia – Conserving Progress .........................................................................................................................46 -

Order 1 Purchase 2 Sale

Form to be sent to: ORDER 1 BNP Paribas Securities Services AIRBUS GROUP Securities Department Les Grands Moulins de Pantin 9, rue du Débarcadère 93761 PANTIN CEDEX - FRANCE 2 PURCHASE SALE Tel. : +33 1 57 43 35 00 Fax: +33 1 57 43 01 54 Confirmation of the order dated .… / … / ……. made by phone 3 DD/MM/YYYY I the undersigned, Mr. / Mrs. / Ms. Last name First name(s) (Strike out as appropriate) (For legal persons: name of signatory) (For legal persons: first name of signatory) Company name SIREN (For legal persons) Date and place of at Phone birth (DD/MM/YYYY) (Mandatory) Account number Residing at Town Post code Country Tax address (if different only) give instructions to BNP Paribas Securities Services to transmit the following order: Stock AIRBUS GROUP ISIN Code NL0000235190 Number of shares (In words) (In figures) i1 Type of order At market price Limit order at ________________________ EUR (Specify the maximum purchase price or minimum sale price) Validity of order (maximum end of month): __________________________ Account details to be credited by wire: Name of the account holder Bank’s name Bank address Country Account currency In France: Code Banque Code Guichet Numéro de compte Clé RIB In other countries4: BIC Code IBAN ABA Code BSB Code Bank Code Branch Code Bank account For payment to an account using an IBAN / BIC code, please specify the payment currency in which the account is held: ……………………………… Documents to be supplied for a sale order 5: a Bank Account identity (RIB), Postal Account identity (RIP), Savings Account identity (RICE) or IBAN number for payment by transfer of the proceeds of the sale of shares, after deduction of brokerage fees, taxes and commissions. -

Home at Airbus

Journal of Aircraft and Spacecraft Technology Original Research Paper Home at Airbus 1Relly Victoria Virgil Petrescu, 2Raffaella Aversa, 3Bilal Akash, 4Juan M. Corchado, 2Antonio Apicella and 1Florian Ion Tiberiu Petrescu 1ARoTMM-IFToMM, Bucharest Polytechnic University, Bucharest, (CE), Romania 2Advanced Material Lab, Department of Architecture and Industrial Design, Second University of Naples, 81031 Aversa (CE), Italy 3Dean of School of Graduate Studies and Research, American University of Ras Al Khaimah, UAE 4University of Salamanca, Spain Article history Abstract: Airbus Commerci al aircraft, known as Airbus, is a European Received: 16-04-2017 aeronautics manufacturer with headquarters in Blagnac, in the suburbs of Revised: 18-04-2017 Toulouse, France. The company, which is 100% -owned by the industrial Accepted: 04-07-2017 group of the same name, manufactures more than half of the airliners produced in the world and is Boeing's main competitor. Airbus was Corresponding Author: founded as a consortium by European manufacturers in the late 1960s. Florian Ion Tiberiu Petrescu Airbus Industry became a SAS (simplified joint-stock company) in 2001, a ARoTMM-IFToMM, Bucharest subsidiary of EADS renamed Airbus Group in 2014 and Airbus in 2017. Polytechnic University, Bucharest, (CE) Romania BAE Systems 20% of Airbus between 2001 and 2006. In 2010, 62,751 Email: [email protected] people are employed at 18 Airbus sites in France, Germany, the United Kingdom, Belgium (SABCA) and Spain. Even if parts of Airbus aircraft are essentially made in Europe some come from all over the world. But the final assembly lines are in Toulouse (France), Hamburg (Germany), Seville (Spain), Tianjin (China) and Mobile (United States). -

Important Notice the Depository Trust Company

Important Notice The Depository Trust Company B #: 12945-20 Date: February 10, 2020 To: All Participants Category: Dividends | International From: Global Tax Services Attention: Managing Partner/Officer, Cashier, Dividend Mgr., Tax Mgr. BNY Mellon | ADRs | Qualified Dividends for Tax Year 2019 Subject: Bank of New York Mellon Corporation (“BNYM”), as depositary for these issues listed below has reviewed and determined if they met the criteria for reduced U.S. tax rate as “qualified dividends” for tax year 2019. The Depository Trust Company received the attached correspondence containing Tax Information. If applicable, please consult your tax advisor to ensure proper treatment of these events. Non-Confidential DTCC Public (White) 2019 DIVIDEND CERTIFICATION CUSIP DR Name Country Exchange Qualified 000304105 AAC TECHNOLOGIES HLDGS INC CAYMAN ISLANDS OTC N 000380105 ABCAM PLC UNITED KINGDOM OTC Y 001201102 AGL ENERGY LTD AUSTRALIA OTC Y 001317205 AIA GROUP LTD HONG KONG OTC N 002482107 A2A SPA ITALY OTC Y 003381100 ABERTIS INFRAESTRUCTURAS S A SPAIN OTC Y 003725306 ABOITIZ EQUITY VENTURES INC PHILIPPINES OTC Y 003730108 ABOITIZ PWR CORP PHILIPPINES OTC Y 004563102 ACKERMANS & VAN HAAREN BELGIUM OTC Y 004845202 ACOM CO. JAPAN OTC Y 006754204 ADECCO GROUP AG SWITZERLAND OTC Y 007192107 ADMIRAL GROUP UNITED KINGDOM OTC Y 007627102 AEON CO LTD JAPAN OTC Y 008712200 AIDA ENGR LTD JAPAN OTC Y 009126202 AIR LIQUIDE FRANCE OTC Y 009279100 AIRBUS SE NETHERLANDS OTC Y 009707100 AJINOMOTO INC JAPAN OTC Y 015096209 ALEXANDRIA MINERAL - REG. S EGYPT None N 015393101 ALFA LAVAL AB SWEDEN SWEDEN OTC Y 021090204 ALPS ELEC LTD JAPAN OTC Y 021244207 ALSTOM FRANCE OTC Y 022205108 ALUMINA LTD AUSTRALIA OTC Y 022631204 AMADA HLDGS CO LTD JAPAN OTC Y 023511207 AMER GROUP HOLDING - REG. -

Investor Guide FY 2019

Airbus - Investor Guide FY 2019 A Global Leader Key Financials Contact . A global leader in aeronautics, space and related services 2018 2019 Head of Investor Relations and Financial Communication: . 86% civil revenues, 14% defence . Three reportable segments: Airbus, Helicopters, Defence and Space Revenues (€ bn) 63.7 70.5 Thorsten Fischer [email protected] +33 5 67 19 02 64 . Robust and diverse backlog EBIT adjusted (€ bn) 5.8 6.9 Institutionals and Analysts: . Global footprint with European industrial roots RoSbased on EBIT adjusted 9.2% 9.9% 2019 Consolidated Airbus 2019 Consolidated Airbus EBIT reported (€ bn) 5.0 1.3 Mohamed Denden [email protected] +33 5 82 05 30 53 External Revenue by Division Order Book in value by Region Net Income/ loss (€ bn) 3.1 -1.4 Philippe Gossard [email protected] +33 5 31 08 59 43 EPS reported (€) 3.94 -1.75 Pierre Lu [email protected] +65 82 92 08 00 Dividend (€) 1.65 1.80* Net Cash Position (€bn) 13.3 12.5 Individual Investors : [email protected] +33 800 01 2001 FCF before M&A and Customer Financing (€bn) 2.9 3.5 € 70.5 bn € 471 bn t/o defence € 38 bn Further information on https://www.airbus.com/investors.html t/o defence € 10.1 bn Click here for guidance . * Board proposal to be submitted to the AGM 2020, subject to AGM approval. Airbus 2019 External Revenue Split 2019 Deliveries by Programme (units) 2019 Orders & Deliveries Airbus 77% Asia Pacific 31% Middle East 9% Key Financials Helicopters 8% Europe 28% Latin America 6% 2018 2019 Defence and Space 15% North America 18% Other 8% . -

Airbus Corporate Jets Wins First Six ACJ Twotwenty Orders

Airbus Corporate Jets wins first six ACJ TwoTwenty orders #ACJTwoTwenty #ACJ #COMLUX Toulouse, 6 October 2020 - Airbus Corporate Jets has won its first orders for the ACJ TwoTwenty totalling six aircraft following its launch. While Comlux has revealed an order for two aircraft, four further jets were ordered by undisclosed customers. Entry into service of the first ACJ TwoTwenty by Comlux Aviation is targeted for early 2023. The new ACJ TwoTwenty will feature a high end VIP cabin interior, supported by a flexible cabin catalogue, from which Comlux has selected the business and guest lounge as well as a private entertainment space and a private suite, including a bathroom. The cabin, set to “Reimagine your place in the sky...” will be equipped with large full lie flat seats, a US-king size bed, a standing rainshower, a humidifying system for well-being on board and leading edge connectivity. “We are proud to be the launch customer of the Airbus’ newest family member, the ACJ TwoTwenty and the selected partner to outfit the cabin in our completion center in Indianapolis. We have worked jointly with ACJ and shared our long experience in operating and completing all types of aircraft, to allow the new Bizjet to offer more comfort and the latest cabin innovations available in the industry, “ said Richard Gaona, Executive Chairman & CEO Comlux. “Thanks to the unique combination of intercontinental range, comfort, extra space and second-to-none economics, we are convinced the aircraft will be a winner in the business aviation market.” “We are honoured to see our longstanding client Comlux becoming the launch customer of our new ACJ TwoTwenty as well as our cabin completion partner on the programme, “ said Benoit Defforge, President ACJ. -

PAR Capital Management Enters Into Binding Agreement to Subscribe to a 11.5% Stake in Icelandair Group

April-2019 PAR Capital Management Enters Into Binding Agreement To Subscribe To A 11.5% Stake In Icelandair Group Airbus Sells Its Shares In Alestis Aerospace Ethiopian Airlines Statement On The Preliminary Report Of The Accident On ET 302 Magnetic MRO Expands Camo Capabili- ties To Two New Wide-Bodies Contents Magnetic MRO Expands Camo Capabilities To Two New Wide-Bodies 1 Starlux Airlines Orders 17 A350 XWB Aircraft For Long-Haul Services 2 ATI Extends Long-Term Purchase Agreement With Rolls-Royce 3 Airbus Sells Its Shares In Alestis Aerospace 4 KBRA Assigns Final Ratings To Maps 2019-1 Limited 5 Vietnam Airlines Showcases Its Latest Airbus A350-900, Completing Its Fleet.. 6 UIA Adjusts Its Summer 2019 Schedule 8 Gulf Air Explores Growing The Airlines Network With Strategic Partners In Russia 9 PAR Capital Management Enters Into Binding Agreement To Subscribe To A 11.5%.. 10 Nordic Aviation Capital Has Successfully Completed The Largest Ever Senior.. 11 Airbus Shareholders Approve All AGM Resolutions, Guillaume Faury Appointed CEO 12 GA Telesis Appoints Kevin Geissler, Vice President Of Aviation Lease Solutions 14 Bombardier Signs Firm Purchase Agreement For Six Q400 Turboprops 15 Aerfin: Q1 Update 16 Ethiopian Airlines Statement On The Preliminary Report Of The Accident On ET 302 18 Airbus Launches “Skywise Health Monitoring” With Us Airline Allegiant Air.. 19 Tap Air Portugal Takes Delivery Of Its First A321LR 20 Skyworks Announces Q1 2019 Activities 22 ANA Receives New Boeing 787-10 For International Routes 23 Gulf Air And Etihad Airways Sign Codeshare Agreement, Strengthening.. 24 Magnetic MRO Expands Camo Capabilities To Two New Wide-Bodies Magnetic MRO, a global provider of Total that adds new wide-body aircraft to our portfolio Technical Care for aircraft operators and lessors, complements the company’s recent business has gained EASA’s approval to offer continuing acquisition. -

China Fully Committed to Debt Relief Plans Of

BUSINESS CHINA DAILY HONG KONG EDITION Friday, October 30, 2020 Airbus to China fully start A350 deliveries committed to from debt relief Tianjin By ZHU WENQIAN [email protected] European aircraft manufac- turer Airbus said on Thursday plans of G20 that it is expected to deliver widebody A350 aircraft from its completion and delivery center Measures to ease burden of poor nations in Tianjin from the first quarter of next year. and boost sustainable development An aerial view shows volunteers posing amid the decorations at the National Exhibition and Con- The Airbus Tianjin widebody vention Center in Shanghai, the venue for the 3rd CIIE. GAO ERQIANG / CHINA DAILY completion and delivery center, By CHEN JIA global fiscal stimulus packages may the company’s first widebody [email protected] have achieved $12 trillion, and the completion and delivery center average deficit ratio is projected to outside Europe, is gradually China is implementing the debt increase by 9 percentage points Livestreaming to enhance value of CIIE shifting its work, including cabin relief plans promoted by the Group from last year. installation and aircraft paint- of 20 to help ease the debt burden of G20 finance ministers and cen- ing, to A350XWB. poor countries and achieve sustain- tral bank governors agreed to By HE WEI in Shanghai taining to say,” he said. fray, amid an army of online influ- “At the beginning, the delivery able development during the novel extend the Debt Service Suspen- [email protected] Apart from introducing new encers. Spectators are also antici- rate of A350 from Tianjin won’t coronavirus epidemic, a senior gov- sion Initiative by six months at a brands and products to the Chi- pated to converse virtually with be too fast, and we plan to gradu- ernment official said. -

R&T Activities on Composite Structures

PUBLIC RELEASE R&T activities on composite structures for existing and future military A/C platforms at Airbus DS, Military Aircraft Mircea Calomfirescu, Rainer Neumaier, Thomas Körwien, Kay Dittrich Airbus Defence and Space GmbH Rechliner Str. 1 85077 Manching GERMANY [email protected] ABSTRACT This paper gives a short overview on the state of the art in composite aerostructures for civil and military aircraft. Major challenges are highlighted in this context and the requirements from military aircraft point of view are illustrated, derived from existing and future military aircraft perspectives. The main objective of the paper is to present the R&T activities in the aerostructure research program called FFS, advanced aerostructures. The activities range here from structural bonding, advanced radomes, new thermoplastic composite technologies and new materials and structures for low observability purposes. A brief insight is given to each of the topic highlighting the challenges and approaches, finishing with a summary of future trends and emerging technologies. 1.0 INTRODUCTION Composites offer several advantages over metallic aerostructures in civil as well as in military aircraft industry including reduced weight, less maintenance effort and costs due to “corrosion-free” composites and a superior fatigue behaviour compared to aluminium. The thermal expansion is much less and the material waste (“buy to fly ratio”) is more advantageous compared to aluminium structures. However, these advantages come along with higher material and manufacturing costs. For the prepreg technology for example the material has to be stored at -18°C, energy and investment intensive autoclaves are necessary and for quality assurance 100% non-destructive testing (NDT) is required in contrast to aluminium structures.