Africa Re Annual Report & Accounts 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Le Re the African Reinsurer

June 2020 Volume 034 Volume 2020 June The African Reinsurer - June 2020 -June2020 Reinsurer The African NEWS FROM THE REGIONS THE FROM NEWS LE REASSUREUR AFRICAIN PUBLICATION DE LA SOCIETE AFRICAINE DE REASSURANCE MARKET PRESENTATION MARKET MANAGEMENT & FINANCE & MANAGEMENT INSURANCE & REINSURANCE & INSURANCE EDITORIAL EDITORIAL ASSURANCE ET REASSURANCE GESTION ET FINANCE PRESENTATION DE MARCHE A PUBLICATION OF THE AFRICAN REINSURANCE CORPORATION REINSURANCE AFRICAN THE OF PUBLICATION A THE AFRICAN REINSURER AFRICAN THE NOUVELLES DES REGIONS assureur Africain - Juin 2020 assureur Africain é Le R Juin 2020 Volume 034 THE AFRICAN REINSURER African Reinsurance Corporation Société Africaine de Réassurance A PUBLICATION OF THE AFRICAN REINSURANCE CORPORATION African Reinsurance Corporation Société Africaine de Réassurance Headquarters/Siège: Plot 1679, Karimu Kotun St., Victoria Island, P.M.B. 12765, Lagos, NIGERIA Tel: (234-1) 4616820-8, 2800924-5 Telefax: (234-1)2800074 E-mail: [email protected] - Web site: http://www.africa-re.com - Your Reinsurer - Votre Réassureur - An ally within your reach - Un Interlocuteur de proximité - A Partner you can trust - Un Partenaire de confiance - A Strong Security with A Rating - Un Réassureur fiable (A.M. Best) and A- (S & P)) Noté A (A.M. Best) et A- (S & P) - An African professional that - Un Professionnel africain à vos côtés stands by you Regional Offices Casablanca Nairobi Abidjan Lagos 33 Boulevard Moulay Youssef, Africa Re Centre, Hospital Road, Rue Mgr René Kouassi A45 - Cocody Plot 1679, Karimu Kotun St., B.P. 7556 Upper Hill, Nairobi. Ambassades Victoria Island, Casablanca, Maroc P.O. Box 62328 - 00200, Nairobi 20 B.P 1623 Abidjan 20 Côte d’Ivoire P.M.B. -

Fairfax 2016 Annual Report

30JAN201416052574 2016 Annual Report Contents Fairfax Corporate Performance ............. 1 Corporate Profile ...................... 2 Chairman’s Letter to Shareholders .......... 4 Management’s Responsibility for the Financial Statements and Management’s Report on Internal Control over Financial Reporting . 28 Independent Auditor’s Report to the Shareholders ........................ 29 Fairfax Consolidated Financial Statements ..... 32 Notes to Consolidated Financial Statements . 39 Management’s Discussion and Analysis of Financial Condition and Results of Operations 115 Appendix – Fairfax Guiding Principles ........ 187 Corporate Information .................. 188 30JAN201416052574 2016 Annual Report Fairfax Corporate Performance (in US$ millions, except as otherwise indicated)(1) Book Common Earnings value Closing Net share- Shares (loss) per share earnings Total Invest- Net holders’ out- per share price(1) Revenue (loss) assets ments debt equity standing share As at and for the years ended December 31(2) 1985 1.52 3.25(3) 12.2 (0.6) 30.4 23.9 – 7.6 5.0 (1.35) 1986 4.25 12.75 38.9 4.7 93.4 68.8 3.7 29.7 7.0 0.98 1987 6.30 12.37 86.9 12.3 139.8 93.5 4.9 46.0 7.3 1.72 1988 8.26 15.00 112.0 12.1 200.6 111.7 27.3 60.3 7.3 1.63 1989 10.50 18.75 108.6 14.4 209.5 113.1 21.9 76.7 7.3 1.87 1990 14.84 11.00 167.0 18.2 461.9 289.3 83.3 81.6 5.5 2.42 1991 18.38 21.25 217.4 19.6 447.0 295.3 58.0 101.1 5.5 3.34 1992 18.55 25.00 237.0 8.3 464.6 311.7 69.4 113.1 6.1 1.44 1993 26.39 61.25 266.7 25.8 906.6 641.1 118.7 211.1 8.0 4.19 1994 31.06 67.00 -

Africa Re Annual Report & Accounts 2020

Annual Report & Accounts 2020 Contents • Established in1976 • 41 African Member States ANNUAL REPORT & ACCOUNTS 2020 1 Annual Report & Accounts 2020 Contents About Us The African Reinsurance Corporation (Africa Re) was established by a multilateral Agreement as a pan-African intergovernmental reinsurance group on 24 February 1976 by 36 member States of the Organization of African Unity (now African Union) and the African Development Bank Group (AfDB). Mission • To foster the development of the insurance and reinsurance industry in Africa; • To promote the growth of national, regional and sub-regional underwriting and retention capacities; • To support African economic development. Value Proposition • We deploy our strengths and leverage our proximities for endless possibilities and client protection. • • We offer financial protection through reinsurance covers to life and non-life insurers in Africa and other selected markets in the Middle East, Asia and South America. Diversified Shareholding • 41 African States – 34.50%; • 114 Insurance and Reinsurance Companies – 34.00%; • African Development Bank – 8.40%; • Fairfax Financial Holdings – 7.35%; • AXA Africa Holdings – 7.35%; • Allianz SE – 8.40%. With a gross written premium of US$ 804.774 million in 2020, Africa Re is the leading and largest pan-African reinsurer in Africa and the Middle East (by net reinsurance written premium). Africa Re is ranked 36th by S&P in the Top 40 Global Reinsurance Groups by net reinsurance premiums written in 2019 and ranked 41st by AM Best in the Top 50 World’s Largest Reinsurance Groups by unaffiliated gross premium written in 2019. Our portfolio is about 95% Property & Casualty with the remainder covering Life & Health. -

2019 Annual Report GUIDING PRINCIPLES for FAIRFAX FINANCIAL HOLDINGS LIMITED

2019 Annual Report GUIDING PRINCIPLES FOR FAIRFAX FINANCIAL HOLDINGS LIMITED OBJECTIVES: 1) We expect to compound our mark-to-market book value per share over the long term by 15% annually by running Fairfax and its subsidiaries for the long term benefit of customers, employees, shareholders and the communities where we operate – at the expense of short term profits if necessary. 2) Our focus is long term growth in book value per share and not quarterly earnings. We plan to grow through internal means as well as through friendly acquisitions. 3) We always want to be soundly financed. 4) We provide complete disclosure annually to our shareholders. STRUCTURE: 1) Our companies are decentralized and run by the presidents except for performance evaluation, succession planning, acquisitions, financing and investments, which are done by or with Fairfax. Investing will always be conducted based on a long term value-oriented philosophy. Cooperation among companies is encouraged to the benefit of Fairfax in total. 2) Complete and open communication between Fairfax and subsidiaries is an essential requirement at Fairfax. 3) Share ownership and large incentives are encouraged across the Group. 4) Fairfax will always be a very small holding company and not an operating company. VALUES: 1) Honesty and integrity are essential in all our relationships and will never be compromised. 2) We are results oriented – not political. 3) We are team players – no ‘‘egos’’. A confrontational style is not appropriate. We value loyalty – to Fairfax and our colleagues. 4) We are hard working but not at the expense of our families. 5) We always look at opportunities but emphasize downside protection and look for ways to minimize loss of capital. -

Global Reinsurance Segment Review

Global Reinsurance BEST’S SPECIALOur R Insight,EPORT Your Advantage. Segment Review September 2, 2015 “It is Not Your Father’s Reinsurance Market Anymore” – The New Reality The reinsurance sector has always been a leader in terms of evolution, but over the past few Reinsurance years the pace of change has unquestionably been more rapid. Historically, changes within the risk functioning sector had been cyclical in nature, but now many observers believe the current evolution to be structural. The market is operating in a “new reality” of abundant capacity from traditional like a tradable and alternative sources, low interest rates and thinner reinsurance margins driven by intense asset class competition against shrinking demand for reinsurance cover. seems to be At this year’s annual shareholders’ meeting, Berkshire Hathaway Chairman and CEO Warren Buffett stated “It’s a business whose prospects have turned for the worse and there is not much the end game. we can do about it.” He added that the reinsurance industry in the next ten years “will not be as it has been in the last 30”. Historically, traditional reinsurance protection had been the primary source of capacity for cedents. That is clearly changing as primary companies are retaining more risk and are increasingly utilizing alternative markets for their risk management needs. At the same time, the old playbook of private equity starting a traditional reinsurance company and then exiting via an IPO is becoming less attractive. Investors would rather put capital to work for a relatively short period of time (typically 1 to 3 years) as opposed to creating new companies that require longer-term capital commitments with a less certain exit strategy. -

The African Reinsurer

Juin 2017 Volume 031 2017 Volume Juin Le R é assureur Africain - Juin 2017 assureur Africain NOUVELLES DES REGIONS DES NOUVELLES PRESENTATION DE MARCHE DE PRESENTATION ASSURANCE ET REASSURANCE ET ASSURANCE EDITORIAL THE AFRICAN REINSURER A PUBLICATION OF THE AFRICAN REINSURANCE CORPORATION PUBLICATION DE LA SOCIETE AFRICAINE DE REASSURANCE DE AFRICAINE SOCIETE LA DE PUBLICATION LE REASSUREUR AFRICAIN REASSUREUR LE EDITORIAL INSURANCE & REINSURANCE MARKET PRESENTATION NEWS FROM THE REGIONS The African Reinsurer - June 2017 Reinsurer The African June 2017 Volume 031 THE AFRICAN REINSURER African Reinsurance Corporation Société Africaine de Réassurance A PUBLICATION OF THE AFRICAN REINSURANCE CORPORATION African Reinsurance Corporation Société Africaine de Réassurance Headquarters/Siège: Plot 1679, Karimu Kotun St., Victoria Island, P.M.B. 12765, Lagos, NIGERIA Tel: (234-1) 4616820-8, 2800924-5 Telefax: (234-1)2800074 E-mail: [email protected] - Web site: http://www.africa-re.com - Your Reinsurer - Votre Réassureur - An ally within your reach - Un Interlocuteur de proximité - A Partner you can trust - Un Partenaire de confiance - A Strong Security With A- Rating - Un réassureur fiable (S & P and A.M. Best) Noté A- (S & P et A.M. Best) - An African professional that - Un Professionnel africain à vos côtés stands by you Regional Offices Casablanca Nairobi Abidjan West Africa Regional Office 33 Boulevard Moulay Youssef, Africa Re Centre, Hospital Road, Rue Viviane A24 - Cocody Plot 1679, Karimu Kotun St., B.P. 7556 Upper Hill, Nairobi. Ambassades Victoria Island, Casablanca, Maroc P.O. Box 62328 - 00200, Nairobi 20 B.P 1623 Abidjan 20. P.M.B. 12765 Tel: (212) 22 43 77 00 - 5 Tel: (254-20) 297-0000 Tel : (225) 22404480 / 75 Lagos - NIGERIA Fax: (212) 22 43 77 29 -30 Fax: (254-20) 297-0666, 297-0777 Fax: (225) 22404482 Tel: (234-1) 461 6820, 28 000 78 E.mail: [email protected] E.mail: [email protected] E.mail: [email protected] Fax: (234-1) 28 000 74 E.mail: [email protected] Cairo Mauritius 7, Elkhalily Str. -

20 Annual Report 20

2020 Annual Report GUIDING PRINCIPLES FOR FAIRFAX FINANCIAL HOLDINGS LIMITED OBJECTIVES: 1) We expect to compound our mark-to-market book value per share over the long term by 15% annually by running Fairfax and its subsidiaries for the long term benefit of customers, employees, shareholders and the communities where we operate – at the expense of short term profits if necessary. 2) Our focus is long term growth in book value per share and not quarterly earnings. We plan to grow through internal means as well as through friendly acquisitions. 3) We always want to be soundly financed. 4) We provide complete disclosure annually to our shareholders. STRUCTURE: 1) Our companies are decentralized and run by the presidents except for performance evaluation, succession planning, acquisitions, financing and investments, which are done by or with Fairfax. Investing will always be conducted based on a long term value-oriented philosophy. Cooperation among companies is encouraged to the benefit of Fairfax in total. 2) Complete and open communication between Fairfax and subsidiaries is an essential requirement at Fairfax. 3) Share ownership and large incentives are encouraged across the Group. 4) Fairfax will always be a very small holding company and not an operating company. VALUES: 1) Honesty and integrity are essential in all our relationships and will never be compromised. 2) We are results oriented – not political. 3) We are team players – no ‘‘egos’’. A confrontational style is not appropriate. We value loyalty – to Fairfax and our colleagues. 4) We are hard working but not at the expense of our families. 5) We always look at opportunities but emphasize downside protection and look for ways to minimize loss of capital. -

Africa Re Annual Report & Accounts 2019

Annual Report & Accounts 2019 Contents • Established in1976 • 41 African Member States ANNUAL REPORT & ACCOUNTS 2019 1 Annual Report & Accounts 2019 Annual Report & Accounts 2019 Contents Contents About Us The Corporation is the best rated pan-African reinsurer. The African Reinsurance Corporation (Africa Re) was established as a pan-African • A.M. Best Company: A (Excellent / Stable Outlook) since 2016 (A – since 2002) intergovernmental reinsurance group on 24 February 1976 by 36 member States of the • Standard & Poor’s: A – (Strong / Stable Outlook) since 2009. Organization of African Unity (now African Union) and the African Development Bank Group (AfDB). Africa Re manages the following continental and national Insurance Pools: Mission • AAIP: African Aviation Insurance Pool, which started in 1983 is promoted by the African • To foster the development of the insurance and reinsurance industry in Africa; Insurance Organization (AIO) for aviation business. • To promote the growth of national, regional and sub-regional underwriting and retention • AOEIP: African Oil & Energy Insurance Pool, which started in 1989 is promoted by the African capacities; Insurance Organization (AIO) for oil & energy business. • To support African economic development. • EAIPN: Energy & Allied Insurance Pool of Nigeria, which started in 2014 is promoted by the Nigerian Insurers Association (NIA) for oil & energy business. Value Proposition We also contribute to the wellbeing of our societies through the Africa Re Foundation registered • We deploy our strengths and leverage our proximities for endless possibilities and client in Mauritius. Up to two percent (2%) of our annual Net Profit is committed to Corporate Social protection. Responsibility (CSR) activities. The areas of focus of the Africa Re Foundation are: • We Offer financial protection through reinsurance covers to life and non-life insurers in Africa • Insurance education; and other selected markets in the Middle East, Asia and South America. -

The African Reinsurer

THE AFRICAN REINSURER A PUBLICATION OF THE AFRICAN REINSURANCE CORPORATION Headquarters/Siège: Plot 1679, Karimu Kotun St., Victoria Island, P.M.B. 12765, Lagos, NIGERIA Tel: (234-1) 2663323, 2626660-2, 618820 Telefax: (234-1) 2663282/2626664 E.mail: [email protected] - Web site: http://www.africa-re.com - Your Reinsurer - Votre Réassureur - An ally within your reach - Un Interlocuteur de Proximité - A Partner You can trust - Un Partenaire de confiance - A Strong Security - Une Sécurité renforcée with (S & P) BBB+ and A.M. Best A- Rating avec les cotes BBB+de S & P et A- de A.M. Best A- - An African Professional that stands by - Un Professionnel Africain à vos côtés you Regional Offices Bureaux Regionaux Nairobi Abidjan Casablanca Africa Re Centre, Hospital Road, Rue, Viviane A24 - Cocody Tour Atlas, Place Zallaqa Upper Hill, Nairobi. 20 BP 1623 Abidjan 20. BP 7556, Casablanca, Maroc P.O. Box 62328, Nairobi Tel : (225) 22404480 - 22404481 Tel: (212) 22 317174, 22 30 61 54 Tel: (254 -2) 2730608, 2730624 Fax : (225) 22404482. Fax: (212) 22 30 79 64 Fax:2724896 E.mail: [email protected] Tlx 28079 M E.mail: [email protected] E.mail: [email protected] Subsidiary Filiale Mauritius Cairo African Reinsurance Corp. (South One Cathedral Square, 12 Khan Younus Africa) Ltd Mezannine level, off Shehab Street rd 3 Floor (Noth Wing) Pope Henessy Street Mohandeseen, Geiza - Oakhurst Building 11-13, Andrew’s Port Louis Tel: (202 )3456611 3034880, Road, Parktown 2193, Houghton Mauritius Fax: (202)303480 2041, Johannesburg Tel: (230) 210-0795, -

The African Reinsurer

THE AFRICAN REINSURER A PUBLICATION OF THE AFRICAN REINSURANCE CORPORATION Volume 022, June 2008 The African Reinsurer AFRICAN REINSURANCE CORPORATION SOCIETE AFRICAINE DE REASSURANCE Headquarters/Siège: Plot 679, Karimu Kotun St., Victoria Island, P.M.B. 2765, Lagos, NIGERIA Tel: (234-) 2663323, 2626660-2, 68820 Telefax: (234-) 2663282/2626664 E-mail: [email protected] - Web site: http://www.africa-re.com - Your Reinsurer - Votre Réassureur - An ally within your reach - Un Interlocuteur de Proximité - A Partner You can trust - Un partenaire de confiance - A Strong Security - Une Sécurité renforcée with (S & P) BBB+ and A.M. Best A- Ratings avec les cotes BBB+ de S & P et A- de A.M. Best - An African Professional that stands by you - Un Professionnel Africain à vos côtés REGIONAL OFFICES Casablanca Nairobi Abidjan 33 Boulevard Moulay Youssef, Africa Re Centre, Hospital Road, Rue Viviane A24 - Cocody Ambassades Upper Hill, Nairobi. 20 BP 623 Abidjan 20. P. O. Box 7556 P.O. Box 62328 - 00200, Nairobi Tel : (225) 224 - 2240448 Casablanca, Morocco Tel: (254-20) 2730660 - 3 Fax : (225) 22404482 Tel: (22) 22 43 77 00 Fax: (254-20) 2724896, 2730608 E-mail: [email protected] Fax: (22) 22 43 77 29 E-mail: [email protected] E-mail: [email protected] SUBSIDIARY Mauritius Cairo African Reinsurance Corp. (South Africa) 38c Mansour Street Abdeen Downtown Ltd One Cathedral Square, Postal Code 46 Mezannine level, 2nd Floor (West Wing) Cairo, Egypt Pope Henessy Street Oakhurst Building -3, St Andrews Road, Tel: (20-2) 2792-4020 Port Louis Parktown 293, Houghton 204, Fax: (20-2) 2792-4030 Mauritius Johannesburg E-mail: [email protected] Tel: (230) 20-0795 Tel: (27-) 484-3764/970/606 Fax: (230) 20-2496 Fax: (27-) 484 - 00 E-mail: [email protected] E-mail: [email protected] 2 The African Reinsurer Volume 022, June 2008 CONTENTS 22nd Edition, June 2008 Established in 1987 Page 4 EDITORIAL THE AFRICAN 5 INSURANCE & REINSURANCE REINSURER 5 Takaful Concepts and Practice PUBLISHER By Zainal Abidin Mohd. -

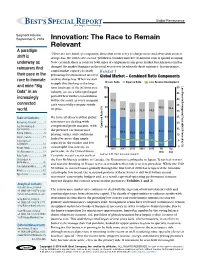

Global Reinsurance BEST’S Specialour R Insight,EPORT Your Advantage

Global Reinsurance BEST’S SPECIALOur R Insight,EPORT Your Advantage. Segment Review September 5, 2016 Innovation: The Race to Remain Relevant A paradigm “There are two kinds of companies, those that work to try to charge more and those that work to shift is charge less. We will be the second,” Jeff Bezos, founder and CEO of Amazon.com, is quoted as saying. underway as Now, certainly, there is room for both types of companies in any given market, but Amazon.com has reinsurers find changed the market dynamics in the retail sector over its relatively short existence. In reinsurance, capital market capacity is clearly Exhibit 1 their pace in the pressuring the reinsurance sector to Global Market – Combined Ratio Components race to innovate work to charge less. When we start to apply this thinking to the long- Loss Ratio Expense Ratio Loss Reserve Development and mine “Big term landscape of the (re)insurance 120 50 Favorable/(Unfavorable)Loss Reserve Development (%) Data” in an industry, we see a rather prolonged 45 period where further consolidation 100 increasingly 40 will be the result, as every company 31.5 connected can’t successfully compete strictly 35 80 32.2 on price. 31.6 32.6 world. 32.3 33.5 34.2 30 Table of Contents: We have all observed that global 60 25 Remaining Relevant ...........1 reinsurers are dealing with 20 compressed profit margins, with Top 50 Ranking & (%) Ratio Combined 40 77.3 Commentary ......................5 the pressure on reinsurance 15 60.2 63.3 61.3 Rating Outlook ...................9 56.5 56.2 56.2 pricing, terms, and conditions 10 20 Lloyd’s Trends ..................11 fueled by more than ample Convergence/ 5 ILS Market .......................13 capacity in the market and low catastrophe loss activity, in 0 0 Hedge Funds ...................19 2011 2012 2013 2014 2015 1H 5yr Life Reinsurance ..............22 particular, in the United States.