Wipro (WPRO IN)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

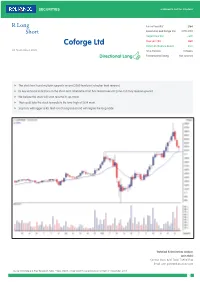

Coforge Ltd Potential Absolute Return 29% 03 November 2020 Time Horizon 9 Weeks Directional Long Fundamental Rating Not Covered

R Long Future Price (Rs)* 2164 Short Recommended Range (Rs) 2170-2150 Target Price (Rs) 2800 Stop Loss (Rs) 1880 Coforge Ltd Potential Absolute Return 29% 03 November 2020 Time Horizon 9 Weeks Directional Long Fundamental Rating Not covered f The stock has found multiple supports around 2080 level post a higher level reversal. f Its key technical indicators on the short-term timeframe chart has tested oversold zone and may reverse upward. f We believe the stock will soon resume its up-move. f That could take the stock towards its life-time-high of 2814 mark. f Stop loss will trigger at Rs 1880 (on closing basis) and will negate the long trade Technical & Derivatives Analyst: Jatin Gohil Contact: (022) 4215 7024/ 7498411546 Email: [email protected] Source: Bloomberg & RSec Research; Note: * Near Month- Single Stock Future price as on 12:15pm 3rd November, 2020 1 Recommendation Summary R Long Short Sr. Reco. Date Time Call Closure Recommendation Company Name Reco. Target Stop Call Status Current Return No Horizon date Price* Loss Price (%) Open Position 1 09-Sep-20 9 Weeks Short Bajaj Finance 3,413 2,550 3,770 Open 3456 -1.3% 2 20-Oct-20 10 Weeks Long Dabur 528 630 484 Open 516 -2.1% 3 21-Oct-20 6 Weeks Long M&M Financial 129 152 119 Open 126 -2.3% 4 30-Oct-20 6 Weeks Short JSW Steel 311 265 345 Open 314 0.9% 5 02-Nov-20 10 Weeks Long MFSL 615 800 545 Open 614 -0.1% Closed Positions 1 09-Oct-20 6 Weeks 28-Oct-20 Long Larsen & Toubro 900 1,065 842 Profit Booked 978 8.7% 2 15-Oct-20 6 Weeks 27-Oct-20 Long Kotak Bank 1,349 1,550 1,235 -

Mahindra & Mahindra

Mahindra & Mahindra (MAHMAH) CMP: | 866 Target: | 1,000 (16%) Target Period: 12 months BUY February 7, 2021 Further strength up ahead… Mahindra & Mahindra (M&M) reported a healthy operational performance in Q3FY21. Standalone net sales were at | 14,216 crore (up 15.2% YoY) – with Particulars automotive and tractor ASPs at | 6.92 lakh/unit (down 1.6% QoQ) and | 5.19 Particular Amount lakh/unit (flat QoQ), respectively. Standalone EBITDA margins at 16% dipped 12 bps QoQ, as operating leverage benefits cancelled out 150 bps Market Capitalization (₹ crore) 1,07,661.1 ₹ contraction in gross margins. Automotive EBIT margins rose ~210 bps QoQ Total Debt (FY20, crore) 3,068.0 Cash and Inv (FY20, ₹ crore) 6,426.1 to 6.3% while tractor margins were down ~100 bps QoQ to 23.4%. EV (FY20, ₹ crore) 1,04,303.1 Standalone PAT for the quarter came in at | 31 crore, impacted by a large 52 week H/L (₹) 893 / 246 Result Update Result impairment hit of | 1,692 crore in relation to long term investments. Equity capital (₹ crore) (FY20) 596.5 Strong volume headroom up ahead once supply concerns ease Face value (₹) ₹ 5 Price Performance M&M’s automotive and tractor performance continues to be on divergent 1000 20,000 paths – total automotive volumes are down 35% YoY in 9MFY21, thus far 750 15,000 (comprises~25% UV decline & ~26% drop in <3.5T LCVs i.e. pickups) while 500 10,000 tractors are up ~11% YoY. Auto performance has been hampered by slow 250 5,000 ramp up due to manufacturing presence in Maharashtra (among the worst hit by the pandemic) and fresh semiconductor shortage. -

OTC TCS 2005.Pdf

1 Annual Report 2004-05 Contents Board of Directors ............................................................................................................................................................................................................................... 3 Management Team ............................................................................................................................................................................................................................. 4 Message from the CEO...................................................................................................................................................................................................................... 6 Notice........................................................................................................................................................................................................................................................ 8 Directors' Report ............................................................................................................................................................................................................................... 15 Management Discussion and Analysis ................................................................................................................................................................................... 30 Corporate Governance Report................................................................................................................................................................................................... -

Franklin India Fund LU0231204701 31 August 2021

Franklin Templeton Investment Funds India Equity Franklin India Fund LU0231204701 31 August 2021 Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund USD Performance over 5 Years in Share Class Currency (%) Total Net Assets (USD) 1.44 billion Franklin India Fund I (acc) USD MSCI India Index-NR Fund Inception Date 25.10.2005 200 Number of Issuers 45 180 Benchmark MSCI India Index-NR 160 Investment Style Blend Morningstar Category™ India Equity 140 Summary of Investment Objective 120 The Fund aims to achieve long-term capital appreciation by 100 principally investing in equity securities of companies of any size located or performing business predominately in India. 80 Fund Management 60 08/16 02/17 08/17 02/18 08/18 02/19 08/19 02/20 08/20 02/21 08/21 Sukumar Rajah: Singapore Discrete Annual Performance in Share Class Currency (%) Ratings - I (acc) USD 08/20 08/19 08/18 08/17 08/16 08/21 08/20 08/19 08/18 08/17 Overall Morningstar Rating™: I (acc) USD 53.68 3.31 -9.75 -0.35 12.92 Asset Allocation Benchmark in USD 53.15 3.00 -7.64 7.12 17.46 Performance in Share Class Currency (%) Cumulative Since 1 Mth 3 Mths 6 Mths YTD 1 Yr 3 Yrs 5 Yrs Incept I (acc) USD 8.00 10.33 21.17 24.53 53.68 43.28 61.24 518.48 % Benchmark in USD 10.94 11.12 22.35 25.75 53.15 45.68 83.30 371.80 Equity 103.05 Category Average 7.59 10.63 20.10 25.82 52.53 37.90 66.00 355.61 Cash & Cash Equivalents -3.05 Calendar Year Performance in Share Class Currency (%) 2020 2019 2018 2017 2016 I (acc) USD 13.92 8.35 -14.74 39.23 2.82 Benchmark in USD 15.55 7.58 -7.31 38.76 -1.43 Past performance is not an indicator or a guarantee of future performance. -

Coforge Ltd (NIITEC)

Coforge Ltd (NIITEC) CMP: | 2456 Target: | 2690 ( 10%) Target Period: 12 months HOLD October 23, 2020 Robust operating performance… Coforge Ltd (Coforge) registered healthy revenue growth, up 8.1% QoQ in constant currency terms, above our estimate of 7.0% QoQ growth. The revenue growth was broad based across verticals mainly led by insurance (up 13.5% QoQ) and BFS (up 10.2% QoQ). Digital revenues (including IP) also increased 18.7% QoQ. Further, Coforge has guided for revenue growth Particulars of 6% YoY organic growth in FY21E and 17.8% EBITDA margin in FY21E Particular Amount before Esop cost. Market Capi (| Crore) 15,116.7 Healthy deal pipeline, digital to drive growth Total Debt (| Crore) 4.8 Update Result Cash & Invests (| Crore) 917.1 Coforge is witnessing healthy traction in cloud, data and artificial intelligence EV (| Crore) 14,204.4 (AI). This has led to healthy growth in digital revenues. The company is driving this growth via partnerships with large players in cloud like Microsoft 52 week H/L 2813 / 739 Azure, Google cloud and AWS and partnering with product start-ups that Equity capital 62.5 can help it to drive new age technology growth. Hence, we expect the Face value 10.0 company to benefit from improved traction in digital technology, going forward. Further, we expect Coforge to witness healthy traction in the BFS Key Highlights and insurance vertical led by large deal wins and wallet share gain in travel segment. In addition, the company expects strong revenue growth in Dollar revenue to improve in coming quarters based on large deal won and healthcare vertical (as seen in this quarter). -

India Meets Britain Tracker 2020 17 © 2021 Grant Thornton UK LLP

India meets Britain Tracker The latest trends in Indian investment in the UK 2021 About our research Our Tracker, developed in collaboration with the Confederation of Indian Industry, identifies the top fastest-growing Indian companies in the UK as measured by percentage revenue growth year-on-year. The Tracker includes Indian-owned corporates with operations headquartered or with a significant base in the UK, with turnover of more than £5 million, year-on-year revenue growth of at least 10% and a minimum two-year track record in the UK, based on the latest published accounts filed as at 31 March 2021, where available. Turnover figures have been annualised where periods of less or more than 12 months have been reported1. In the UK, to reflect the pandemic challenges, companies were granted a three-month extension to the usual filing period. Indian companies that took advantage of this option may therefore not appear in this year’s research. Our report also highlights the top Indian employers – those companies that employ more than 1,000 people in the UK2. To compile the India meets Britain Tracker 2021, Grant Thornton analysed data from 850 UK- incorporated limited companies that are owned directly or indirectly, or controlled, by either an Indian-incorporated parent or an Indian citizen resident outside the UK3. 1 As our research relies on published and filed accounts, there is inevitably a time lag between the recording of the performance of the companies and the publication of this report. 2 Employment numbers may include employees -

Franklin India Fund LU1212701376 31 August 2021

Franklin Templeton Investment Funds India Equity Franklin India Fund LU1212701376 31 August 2021 Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund USD Performance over 5 Years in Share Class Currency (%) Total Net Assets (USD) 1,44 billion Franklin India Fund A (acc) EUR-H1 MSCI India Index-NR in USD Fund Inception Date 25.10.2005 190 Number of Issuers 45 170 Benchmark MSCI India Index-NR 150 Morningstar Category™ Other Equity 130 Summary of Investment Objective The Fund aims to achieve long-term capital appreciation by 110 principally investing in equity securities of companies of any size located or performing business predominately in India. 90 Fund Management 70 Sukumar Rajah: Singapore 50 08/16 02/17 08/17 02/18 08/18 02/19 08/19 02/20 08/20 02/21 08/21 Asset Allocation Discrete Annual Performance in Share Class Currency (%) 08/20 08/19 08/18 08/17 08/16 08/21 08/20 08/19 08/18 08/17 A (acc) EUR-H1 50,51 -1,01 -13,58 -3,55 9,44 Benchmark in USD 53,15 3,00 -7,64 7,12 17,46 % Performance in Share Class Currency (%) Equity 103,05 Cumulative Annualised Cash & Cash Equivalents -3,05 Since Since 1 Mth 3 Mths 6 Mths 1 Yr 3 Yrs 5 Yrs Incept 3 Yrs 5 Yrs Incept A (acc) EUR-H1 7,78 9,87 19,92 50,51 28,75 35,90 46,91 8,79 6,33 6,24 Benchmark in USD 10,94 11,12 22,35 53,15 45,68 83,30 84,41 13,36 12,89 10,11 Calendar Year Performance in Share Class Currency (%) 2020 2019 2018 2017 2016 A (acc) EUR-H1 9,54 4,01 -17,74 34,53 0,74 Benchmark in USD 15,55 7,58 -7,31 38,76 -1,43 Past performance is not an indicator or a guarantee of future performance. -

ICICI Securities – Retail Equity Research Result Update Marico

Marico (MARLIM) CMP: | 546 Target: | 630 (15%) Target Period: 12 months BUY August 1, 2021 Saffola growth momentum continues… About the stock: Marico is one of the major FMCG companies present in hair oil, edible oil, foods & personal care segment. Major brands include Parachute, Saffola, Nihar, Hair & Care, Set Wet, Livon and Beardo. Particulars The company has an overall distribution network of more than 5 million Particulars (| crore) Amount outlets and direct reach of ~1 million outlets. Through its stockist network, Market Capitalization 70,503.0 it reaches 58000 villages Total Debt (FY21) 340.0 Cash and Investments (FY21) 1,572.0 Update Result With the high gross margins of ~47%, Marico is able to spend 10% of its EV 69,271.0 sales for advertisements to support new categories & products 52 week H/L (|) 552 / 333 Equity capital 129.0 Face value (|) 1.0 Q1FY22 Results: Marico reported robust revenue growth in Q1FY22 results. Shareholding pattern Sales were up 31.2% YoY with strong volume recovery and price hikes (in %) Sep-20 Dec-20 Mar-21 Jun-21 EBITDA was at | 481 crore, up 3.1% YoY, with margins at 19% Promoter 59.6 59.6 59.6 59.6 FII 23.7 24.2 24.0 25.0 Consequent PAT was at | 365 crore (down 5.3% YoY) DII 10.4 10.2 10.2 9.7 Others 6.3 6.0 6.2 5.7 What should investors do? Marico’s share price has given 84% return in the last five years (from | 297 in July 2016 to | 547 in July 2021). -

John Hancock Emerging Markets Fund

John Hancock Emerging Markets Fund Quarterly portfolio holdings 5/31/2021 Fund’s investments As of 5-31-21 (unaudited) Shares Value Common stocks 98.2% $200,999,813 (Cost $136,665,998) Australia 0.0% 68,087 MMG, Ltd. (A) 112,000 68,087 Belgium 0.0% 39,744 Titan Cement International SA (A) 1,861 39,744 Brazil 4.2% 8,517,702 AES Brasil Energia SA 14,898 40,592 Aliansce Sonae Shopping Centers SA 3,800 21,896 Alliar Medicos A Frente SA (A) 3,900 8,553 Alupar Investimento SA 7,050 36,713 Ambev SA, ADR 62,009 214,551 Arezzo Industria e Comercio SA 1,094 18,688 Atacadao SA 7,500 31,530 B2W Cia Digital (A) 1,700 19,535 B3 SA - Brasil Bolsa Balcao 90,234 302,644 Banco Bradesco SA 18,310 80,311 Banco BTG Pactual SA 3,588 84,638 Banco do Brasil SA 15,837 101,919 Banco Inter SA 3,300 14,088 Banco Santander Brasil SA 3,800 29,748 BB Seguridade Participacoes SA 8,229 36,932 BR Malls Participacoes SA (A) 28,804 62,453 BR Properties SA 8,524 15,489 BrasilAgro - Company Brasileira de Propriedades Agricolas 2,247 13,581 Braskem SA, ADR (A) 4,563 90,667 BRF SA (A) 18,790 92,838 Camil Alimentos SA 11,340 21,541 CCR SA 34,669 92,199 Centrais Eletricas Brasileiras SA 5,600 46,343 Cia Brasileira de Distribuicao 8,517 63,718 Cia de Locacao das Americas 18,348 93,294 Cia de Saneamento Basico do Estado de Sao Paulo 8,299 63,631 Cia de Saneamento de Minas Gerais-COPASA 4,505 14,816 Cia de Saneamento do Parana 3,000 2,337 Cia de Saneamento do Parana, Unit 8,545 33,283 Cia Energetica de Minas Gerais 8,594 27,209 Cia Hering 4,235 27,141 Cia Paranaense de Energia 3,200 -

Invesco India Equity Fund a (HKD)-Acc Shares 31 August 2021

Invesco India Equity Fund A (HKD)-Acc Shares 31 August 2021 This marketing communication is for investors in Switzerland only. Investors should read the legal documents prior to investing. Fund Strategy Summary of fund objective The fund aims to achieve long-term capital growth by investing principally in equity or similar The Fund is actively managed. instruments of Indian companies. We believe India is a high growth market with wealth of The objective of the Fund is to achieve investment opportunities, and that by focusing on stock fundamentals, we can identify long-term capital growth by investing “Quality Growth” companies with strong business models, industry leadership, competitive principally in equity or similar instruments advantages, strong management and what the believe to be reasonable valuations. We of Indian companies. For the full objectives adhere to a purely bottom-up investment process with a conviction-based approach and and investment policy please consult the preference for private enterprises. While the fund does not have any binding investment current prospectus. restrictions based on ESG, we believe ESG characteristics can positively impact financial performance and conduct in-depth proprietary research to assign ESG risk ratings. Key facts Indexed performance* Fund Benchmark 200 180 160 Shekhar 140 Sambhshivan 120 Hong Kong 100 Managed fund since May 2006 80 60 Share class launch 40 07 July 2011 08/16 08/17 08/18 08/19 08/20 08/21 Original fund launch 1 02 December 1994 The performance period shown here starts on the last day of the first indicated month and ends on the last day of the last indicated month. -

Ambuja Cements ( AMBCEM)

Ambuja Cements ( AMBCEM) CMP: | 407 Target: | 490 (20%) Target Period: 12 months BUY July 26, 2021 Beats estimates with strong margins… About the stock: Ambuja Cement (a Holcim group company) is a large cement player with capacity of over 29.7 MT spread across North-Central (40%), West (~35%) and East (~25%) India. It has a large marketing set-up, pan-India presence and strong operational linkages with ACC. Particulars The upcoming new capacity at Rajasthan will enhance its cement capacity by Particular Amount 1.8 MT to 31.5 MT and clinker capacity by 3.0 MT Market cap | 80816 crore Debt (CY20) | 72 crore Result Update Result In the long run, the company plans to reach over ~50 MT capacity through Cash & Invest (CY20) | 686 crore significant de-bottlenecking and setting up of satellite grinding units EV | 80202 crore 52 week H/L | 410 / 196 Equity capital | 397.1 crore Q1FY22 Results: Ambuja Cement reported 149 bps QoQ expansion in margins Face value | 2 leading to better profitability despite cost pressure. Shareholding pattern Clocked revenue of | 3,371 crore, down 6.9% QoQ led by sales volumes de- (in %) Sep-20 Dec-20 Mar-21 Jun-21 growth of 11.3% to 6.4 MT. On a YoY basis, revenues were up 53.2% Promoter 63.3 63.3 63.3 63.3 EBITDA/t was up 10.8% QoQ to | 1,495/t (vs. last quarter EBITDA/t of FII 16.8 18.1 17.8 17.7 | 1,349/t). EBITDA margin was at 28.5%, up 149 bps QoQ, 112 bps YoY DII 13.3 11.5 12.4 12.5 Others 6.6 7.1 6.6 6.5 Reported PAT was at | 723.1 crore, up 59.5% YoY, 8.8% QoQ vs. -

DEBT CAPITAL MARKETS Advantage Debt Capital Markets @ YES BANK

DEBT CAPITAL MARKETS Advantage Debt Capital Markets @ YES BANK § Integrated approach of end to end Origination to Distribution resulting in efficient execution of mandates § Deep knowledge of the underlying market dynamics and strong structuring capabilities § Leveraging a strong in-house INR rates research team; supplemented by comprehensive coverage of Corporates through pro- active relationship teams § Ability to originate transactions for a wide range of issuers, across various sectors including Automobiles, Cement, Fertilizers, Infrastructure, Pharmaceuticals, Power and Retail etc § Superior Distribution Capabilities with strong relationships across various investor categories including Banks, Financial Institutions, Mutual Funds, Insurance Companies, Non Banking Finance Companies, Provident & Pension Funds, Foreign Portfolio Investors and Private Wealth Managers 40.0% YES BANK’s outperformance vis-à-vis market 35.0% Banks / Mutual 30.0% Funds 25.0% Insurance Indian Pvt. & PSU Companies INVESTORS 20.0% Corporates 15.0% YES BANK PensionProvident/ Funds 10.0% ISSUERS Non Banking Product Suite Finance Cos. Securitisation 5.0% Preference Shares Foreign Portfolio INR Bond Underwriting/ Syndication Investors 0.0% Financial Investment Advisory & Value Added Offerings Total issuance volume Pvt sector issuance volume Institutions Market YBL Domestic PSUs Emerging Business Houses Entrepreneurs CAGR over the last five years of the total market issuance volume and YES BANK’s origination volume RELATIONSHIPS Corporate Bond issuance volumes in