(ADS) in Life and Annuities (L&A) Insurance Services 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Research Paper IJMSRR Impact Factor 0.348 E- ISSN - 2349-6746 ISSN -2349-6738

Research Paper IJMSRR Impact Factor 0.348 E- ISSN - 2349-6746 ISSN -2349-6738 A STUDY ON PERFORMANCE OF MAJOR IT COMPANIES OF INDIA Prof. (Dr). C.K.Madhusoodhanan Professor, Dept. of Management Studies, Sree Narayana Gurukulam College of Engineering, Kolenchery Kerala. A.V Rejimon Assistant Professor, Dept. of Management Studies, Sree Narayana Gurukulam College of Engineering, Kolenchery, Kerala. Introduction Globalisation, liberation and privatisation were initiated by the Narsimha Rao government in early nineties. The new economic policy of the government of India generated industrial growth. It led to unprecedented development of industries. I T industry became one of the most flourishing industries in India. The investment in I T Sector has increased since India opened up the economy for private sector. Emergence of Globalised economy witnessed growth of I T industry. Many new cooperates entered the industry. Different types of investors showed keen interest in investing in I T stocks because of the higher rate of return. In portfolio selection the investors are confronted with an issue of identifying the right company having intrinsic value for the investment. The issue to be discussed with is how to select the right company in the context of mushroom growth of IT companies with plenty of new entrance with little history but with great volume of profit. Literature Review The origin of Fundamental analysis for the share price valuation can be dated back to Graham and Dodd (1934) in which the authors have argued the importance of the fundamental factors in share price valuation. Theoretically, the value of a company, hence its share price, is the sum of the present value of future cash flows discounted by the risk adjusted discount rate. -

Work-Life Balance a Strategic Human Resource Policies and Practices Followed by Indian Organizations

IRA-International Journal of Management & Social Sciences ISSN 2455-2267; Vol.05, Issue 03 (2016) Pg. no. 427-435 Institute of Research Advances http://research-advances.org/index.php/RAJMSS Work-life Balance a Strategic Human Resource Policies and Practices followed by Indian Organizations Mrs. Pratibha Barik1, Dr. (Mrs.) B.B. Pandey2 1Research Scholar, Department of Management Studies, Guru Ghasidas Vishwavidyalaya, Koni (Bilaspur), India. 2Assistant Professor, Department of Management Studies, Guru Ghasidas Vishwavidyalaya, Koni (Bilaspur), India. Type of Review: Peer Reviewed. DOI: http://dx.doi.org/10.21013/jmss.v5.n3.p5 How to cite this paper: Barik, P., & Pandey, B. (2016). Work-life Balance a Strategic Human Resource Policies and Practices followed by Indian Organizations. IRA-International Journal of Management & Social Sciences (ISSN 2455-2267), 5(3), 427-435. doi:http://dx.doi.org/10.21013/jmss.v5.n3.p5 © Institute of Research Advances This work is licensed under a Creative Commons Attribution-Non Commercial 4.0 International License subject to proper citation to the publication source of the work. Disclaimer: The scholarly papers as reviewed and published by the Institute of Research Advances (IRA) are the views and opinions of their respective authors and are not the views or opinions of the IRA. The IRA disclaims of any harm or loss caused due to the published content to any party. 427 IRA-International Journal of Management & Social Sciences ABSTRACT The study examines the innovative work-life balance policies and practices implemented by various Indian Companies. As with the increase of women workforce, dual earner families and increase in nuclear families have generated the need for the employees to balance their work and personal life. -

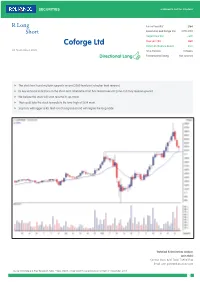

Coforge Ltd Potential Absolute Return 29% 03 November 2020 Time Horizon 9 Weeks Directional Long Fundamental Rating Not Covered

R Long Future Price (Rs)* 2164 Short Recommended Range (Rs) 2170-2150 Target Price (Rs) 2800 Stop Loss (Rs) 1880 Coforge Ltd Potential Absolute Return 29% 03 November 2020 Time Horizon 9 Weeks Directional Long Fundamental Rating Not covered f The stock has found multiple supports around 2080 level post a higher level reversal. f Its key technical indicators on the short-term timeframe chart has tested oversold zone and may reverse upward. f We believe the stock will soon resume its up-move. f That could take the stock towards its life-time-high of 2814 mark. f Stop loss will trigger at Rs 1880 (on closing basis) and will negate the long trade Technical & Derivatives Analyst: Jatin Gohil Contact: (022) 4215 7024/ 7498411546 Email: [email protected] Source: Bloomberg & RSec Research; Note: * Near Month- Single Stock Future price as on 12:15pm 3rd November, 2020 1 Recommendation Summary R Long Short Sr. Reco. Date Time Call Closure Recommendation Company Name Reco. Target Stop Call Status Current Return No Horizon date Price* Loss Price (%) Open Position 1 09-Sep-20 9 Weeks Short Bajaj Finance 3,413 2,550 3,770 Open 3456 -1.3% 2 20-Oct-20 10 Weeks Long Dabur 528 630 484 Open 516 -2.1% 3 21-Oct-20 6 Weeks Long M&M Financial 129 152 119 Open 126 -2.3% 4 30-Oct-20 6 Weeks Short JSW Steel 311 265 345 Open 314 0.9% 5 02-Nov-20 10 Weeks Long MFSL 615 800 545 Open 614 -0.1% Closed Positions 1 09-Oct-20 6 Weeks 28-Oct-20 Long Larsen & Toubro 900 1,065 842 Profit Booked 978 8.7% 2 15-Oct-20 6 Weeks 27-Oct-20 Long Kotak Bank 1,349 1,550 1,235 -

Cloud Transformation/ Operation Services & Xaas

Cloud Transformation/ A research report Operation Services & XaaS comparing provider strengths, challenges U.S. 2019 and competitive differentiators Quadrant Report Customized report courtesy of: November 2018 ISG Provider Lens™ Quadrant Report | November 2018 Section Name About this Report Information Services Group, Inc. is solely responsible for the content of this report. ISG Provider Lens™ delivers leading-edge and actionable research studies, reports and consulting services focused on technology and service providers’ strength and Unless otherwise cited, all content, including illustrations, research, conclusions, weaknesses and how they are positioned relative to their peers in the market. These assertions and positions contained in this report were developed by and are the sole reports provide influential insights accessed by our large pool of advisors who are property of Information Services Group, Inc. actively advising outsourcing deals as well as large numbers of ISG enterprise clients who are potential outsourcers. The research and analysis presented in this report includes research from the ISG Provider Lens™ program, ongoing ISG Research programs, interviews with ISG advisors, For more information about our studies, please email [email protected], briefings with services providers and analysis of publicly available market information call +49 (0) 561-50697537, or visit ISG Provider Lens™ under ISG Provider Lens™. from multiple sources. The data collected for this report represents information that ISG believes to be current as of September 2018, for providers who actively participated as well as for providers who did not. ISG recognizes that many mergers and acquisitions have taken place since that time but those changes are not reflected in this report. -

Innovating with Infosys Finacle

PREFACE CUSTOMER CHANNEL/ PRODUCT SERVICE DISTRIBUTION INNOVATION INNOVATION INNOVATION INNOVATIVE INNOVATION CUSTOMS PROCESS IN PROJECT COMPONENT INNOVATION MANAGEMENT DEVELOPED Innovation continues to be the leitmotif of and felicitate our innovative partners. In this the global banking industry. A perfect storm booklet, I am proud to present the winners of of rising customer expectations, increasing the 2015 edition of the Infosys Finacle Client competitive pressures and stringent compliance Innovation Awards. demands is compelling more and more banks to In 2015, we received an overwhelming response pursue innovation for sustainable competitive in the form of 104 nominations across 6 advantage. innovation categories. Each nomination was Against this background, I am increasingly judged on the merits of the degree of innovation, enthused to see that many of our partners in the complexity of the initiative, and benefits financial services industry are leveraging Finacle delivered. Every nomination is an affirmation of solutions to develop deeper connections with how our clients are embracing breakthrough stakeholders, power continuous innovation, and innovations quickly to take advantage of global accelerate growth in the digital world. technology shifts and deliver differentiated products and services, based on their customers’ We instituted the Infosys Finacle Client unique requirements. Innovation Awards in 2014 to formally recognize 2 I External Document © 2016 EdgeVerve Systems Limited We found the entire process of inviting and -

Coforge Ltd (NIITEC)

Coforge Ltd (NIITEC) CMP: | 2456 Target: | 2690 ( 10%) Target Period: 12 months HOLD October 23, 2020 Robust operating performance… Coforge Ltd (Coforge) registered healthy revenue growth, up 8.1% QoQ in constant currency terms, above our estimate of 7.0% QoQ growth. The revenue growth was broad based across verticals mainly led by insurance (up 13.5% QoQ) and BFS (up 10.2% QoQ). Digital revenues (including IP) also increased 18.7% QoQ. Further, Coforge has guided for revenue growth Particulars of 6% YoY organic growth in FY21E and 17.8% EBITDA margin in FY21E Particular Amount before Esop cost. Market Capi (| Crore) 15,116.7 Healthy deal pipeline, digital to drive growth Total Debt (| Crore) 4.8 Update Result Cash & Invests (| Crore) 917.1 Coforge is witnessing healthy traction in cloud, data and artificial intelligence EV (| Crore) 14,204.4 (AI). This has led to healthy growth in digital revenues. The company is driving this growth via partnerships with large players in cloud like Microsoft 52 week H/L 2813 / 739 Azure, Google cloud and AWS and partnering with product start-ups that Equity capital 62.5 can help it to drive new age technology growth. Hence, we expect the Face value 10.0 company to benefit from improved traction in digital technology, going forward. Further, we expect Coforge to witness healthy traction in the BFS Key Highlights and insurance vertical led by large deal wins and wallet share gain in travel segment. In addition, the company expects strong revenue growth in Dollar revenue to improve in coming quarters based on large deal won and healthcare vertical (as seen in this quarter). -

India Meets Britain Tracker 2020 17 © 2021 Grant Thornton UK LLP

India meets Britain Tracker The latest trends in Indian investment in the UK 2021 About our research Our Tracker, developed in collaboration with the Confederation of Indian Industry, identifies the top fastest-growing Indian companies in the UK as measured by percentage revenue growth year-on-year. The Tracker includes Indian-owned corporates with operations headquartered or with a significant base in the UK, with turnover of more than £5 million, year-on-year revenue growth of at least 10% and a minimum two-year track record in the UK, based on the latest published accounts filed as at 31 March 2021, where available. Turnover figures have been annualised where periods of less or more than 12 months have been reported1. In the UK, to reflect the pandemic challenges, companies were granted a three-month extension to the usual filing period. Indian companies that took advantage of this option may therefore not appear in this year’s research. Our report also highlights the top Indian employers – those companies that employ more than 1,000 people in the UK2. To compile the India meets Britain Tracker 2021, Grant Thornton analysed data from 850 UK- incorporated limited companies that are owned directly or indirectly, or controlled, by either an Indian-incorporated parent or an Indian citizen resident outside the UK3. 1 As our research relies on published and filed accounts, there is inevitably a time lag between the recording of the performance of the companies and the publication of this report. 2 Employment numbers may include employees -

Information Nation

SPRING/SUMMER 2003 STERNbusiness InformationCrossing Nation Borders CEO Interviews: How UPS Delivers How Bic Stays on the Ball CreativeNiall Ferguson onThinking: Anglobalization India’s Software Giant EntrepreneurshipWhy Major Economies Don't in Move the in SyncDigitalUnderstanding Age New Consumer Markets Wal-Mart’s Foreign Travels Rx Coverage: Curing Telecom and Argentina a letter fro m the dean It’s more than fit- Metropolitan Opera, Munich’s Bayerische Staatsoper, ting that this issue and Milan’s La Scala. focuses on the topic Meeting in the heart of Europe, and with people of globalization and from different business cultures and scholarly crossing borders. In disciplines, added a great deal of context to all our recent months, Stern discussions. Of course, history is an important com- has seen significant ponent of context. Business history – long a strength milestones in our at Stern – has been augmented by the arrival in international efforts. This past January the inaugu- January of Professor Niall Ferguson, who recently ral, 28-person class of executive MBA students from joined us from Oxford University and is the author TRIUM, the program Stern offers jointly with the of the definitive two-volume history of the London School of Economics and the HEC School of Rothschild banking empire. His most recent book, Management in Paris, completed their studies. The Empire – which is partially excerpted in this issue – second TRIUM class, with 35 members, completed is a significant contribution to the growing literature its first module at our campus in New York that on globalization. same month. This innovative program, geared As several articles in this issue argue, toward inculcating a global perspective in its stu- understanding the historical development of dents, will continue throughout the year with international markets, companies, and financial sessions in Paris, London, Brazil, and Hong Kong. -

Lnt-Infotech-Annual-Report-FY16.Pdf

ANNUAL REPORT 2015-16 Let’s S lve Inside Message from the 1. Corporate Overview Founder Chairman 01 Message from the Founder Chairman 02 Let’s Solve 04 The Journey So Far… 06 At a Glance 10 Message from the CEO 12 Board of Directors 15 Key Leadership Team 16 Corporate Information 17 Key Financial Highlights 18 Corporate Social Responsibility 2. Our DNA 20 Client-Centricity 21 Digital Leadership 22 Best Place to Learn, Evolve, Grow 3. Statutory Reports 26 Directors’ Report 55 Corporate Governance Report 62 Management Discussion and Analysis 76 Risk Management Framework 4. Financial Statements Mr. A. M. Naik, Founder Chairman, was conferred the Order of the Standalone Dannebrog as Knight First Class by Her Majesty, Queen Margrethe of 77 Independent Auditor’s Report Denmark. The knighthood is royal acknowledgement of Mr. Naik’s role in 82 Balance Sheet fostering Indo-Danish ties in the fields of business, commerce and culture. 83 Statement of Profit & Loss 84 Cash Flow Statement 86 Notes forming part of accounts Prior experience in enabling Consolidated technology-driven growth across 118 Independent Auditor’s Report 122 Balance Sheet multiple businesses gave your 123 Statement of Profit & Loss 124 Cash Flow Statement company an unmatched 126 Notes forming part of accounts ‘Business-to-IT connect’ Message from the Founder Chairman The management team at L&T Infotech is increasingly building competencies in new-age technologies like Digital & Automation Dear Shareholders, Information Technology is increasingly becoming the axis on which a clear differentiator in markets where services were vulnerable our world rotates. Technology pervades multiple aspects - building to commoditisation. -

Rethinking Retail Insights from Consumers and Retailers Into an Omni-Channel Shopping Experience

STUDY Rethinking Retail Insights from consumers and retailers into an omni-channel shopping experience The growth and maturity of digital channels have steadily increased the expectations of the consumers, who now look for an integrated shopping experience across all their touch points with a retailer – be it an online comparison, a feedback from social media, a delivery system, or an in-store experience. An Infosys study reveals retail insights from 1,000 consumers and 50 retailers across the United States. Key highlights include the need for consistency in brand interaction across channels, rising expectations for personalization among consumers, and how retailers are focusing on providing seamless omni-channel shopping experiences. Consumers The effect of consistency across retail organizations A majority of consumers see consistency personal information / purchasing history of numerous facets of retail operations to be consistent across different branches as important across both physical of a brand, while a slightly higher number and online stores and across different (44%) expect this across physical and physical branches. Consistency in the online stores. Despite this, a majority 59% range of products available, is regarded (86%) said that personalization has at least as important, by 72% of respondents some impact on what they purchase, and of shoppers for physical and online stores and by one-quarter (25%) say personalization who have 77% across different physical branches. significantly influences what they Similarly, consistency in the location of / purchase. experienced ease of finding products is important for Just over two-thirds (69%) of respondents 68% of respondents across physical and say a retailers’ consistency across various personalization online stores and 75% of respondents channels affects their loyalty to a brand. -

John Hancock Emerging Markets Fund

John Hancock Emerging Markets Fund Quarterly portfolio holdings 5/31/2021 Fund’s investments As of 5-31-21 (unaudited) Shares Value Common stocks 98.2% $200,999,813 (Cost $136,665,998) Australia 0.0% 68,087 MMG, Ltd. (A) 112,000 68,087 Belgium 0.0% 39,744 Titan Cement International SA (A) 1,861 39,744 Brazil 4.2% 8,517,702 AES Brasil Energia SA 14,898 40,592 Aliansce Sonae Shopping Centers SA 3,800 21,896 Alliar Medicos A Frente SA (A) 3,900 8,553 Alupar Investimento SA 7,050 36,713 Ambev SA, ADR 62,009 214,551 Arezzo Industria e Comercio SA 1,094 18,688 Atacadao SA 7,500 31,530 B2W Cia Digital (A) 1,700 19,535 B3 SA - Brasil Bolsa Balcao 90,234 302,644 Banco Bradesco SA 18,310 80,311 Banco BTG Pactual SA 3,588 84,638 Banco do Brasil SA 15,837 101,919 Banco Inter SA 3,300 14,088 Banco Santander Brasil SA 3,800 29,748 BB Seguridade Participacoes SA 8,229 36,932 BR Malls Participacoes SA (A) 28,804 62,453 BR Properties SA 8,524 15,489 BrasilAgro - Company Brasileira de Propriedades Agricolas 2,247 13,581 Braskem SA, ADR (A) 4,563 90,667 BRF SA (A) 18,790 92,838 Camil Alimentos SA 11,340 21,541 CCR SA 34,669 92,199 Centrais Eletricas Brasileiras SA 5,600 46,343 Cia Brasileira de Distribuicao 8,517 63,718 Cia de Locacao das Americas 18,348 93,294 Cia de Saneamento Basico do Estado de Sao Paulo 8,299 63,631 Cia de Saneamento de Minas Gerais-COPASA 4,505 14,816 Cia de Saneamento do Parana 3,000 2,337 Cia de Saneamento do Parana, Unit 8,545 33,283 Cia Energetica de Minas Gerais 8,594 27,209 Cia Hering 4,235 27,141 Cia Paranaense de Energia 3,200 -

Mindtree Ltd (MINLIM) | 454 Target : | 470 Target Period : 12 Months Potential Upside : 4%

Analyst Meet Update August 22, 2017 Rating matrix Rating : Hold MindTree Ltd (MINLIM) | 454 Target : | 470 Target Period : 12 months Potential Upside : 4% MindTree 3.0 – Focus on digital leadership What’s Changed? We attended MindTree’s (MTL) analyst meet wherein the management Target Unchanged emphasised on how ‘Digital’ is the crux to any business innovation and EPS FY18E Unchanged differentiation. The management highlighted: 1) Developing deep EPS FY19E Unchanged expertise by focusing on select packages as Salesforce, HANA, Adobe. 2) Rating Unchanged elevating the customer experience by modernising the ecosystem & Key Financials processes and harnessing the power of data and 3) continued focus on | Crore FY16 FY17 FY18E FY19E improving profitability by consistent revenue growth, stability in top 10 Net Sales 4,673 5,236 5,403 6,229 accounts and operational efficiency. MTL maintains its stance of being EBITDA 821 705 697 903 better placed to capture incremental opportunities given its diverse Net Profit 553 419 441 545 portfolio offerings (digital, IoT, platforms, enterprise services). We keep EPS (|) 32.9 24.9 26.9 33.3 our estimates intact with MTL’s rupee revenue, PAT set to grow at a CAGR of 9.1%, 14.1%, respectively, in FY17-19E with average EBITDA Valuation summary margins of 13.6% in the same period. FY16 FY17 FY18E FY19E Answering ‘WHAT’ of digital transformation… P/E 13.8 18.2 16.9 13.6 MTL’s management mentioned its business proposition is captured in Target P/E 14.3 18.9 17.5 14.1 answering the ‘What’ of Digital Transformation.