Sony Financial Holdings Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sony Kabushiki Kaisha

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 20-F n REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 or ¥ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended March 31, 2010 or n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from/to or n SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report: Commission file number 1-6439 Sony Kabushiki Kaisha (Exact Name of Registrant as specified in its charter) SONY CORPORATION (Translation of Registrant’s name into English) Japan (Jurisdiction of incorporation or organization) 7-1, KONAN 1-CHOME, MINATO-KU, TOKYO 108-0075 JAPAN (Address of principal executive offices) Samuel Levenson, Senior Vice President, Investor Relations Sony Corporation of America 550 Madison Avenue New York, NY 10022 Telephone: 212-833-6722, Facsimile: 212-833-6938 (Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered American Depositary Shares* New York Stock Exchange Common Stock** New York Stock Exchange * American Depositary Shares evidenced by American Depositary Receipts. Each American Depositary Share represents one share of Common Stock. ** No par value per share. Not for trading, but only in connection with the listing of American Depositary Shares pursuant to the requirements of the New York Stock Exchange. -

Exective Appointments

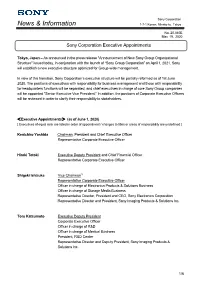

Sony Corporation News & Information 1-7-1 Konan, Minato-ku, Tokyo No. 20 -040E May 19, 2020 Sony Corporation Executive Appointments Tokyo, Japan – As announced in the press release "Announcement of New Sony Group Organizational Structure" issued today, in conjunction with the launch of “Sony Group Corporation” on April 1, 2021, Sony will establish a new executive structure optimized for Group-wide management. In view of this transition, Sony Corporation’s executive structure will be partially reformed as of 1st June 2020. The positions of executives with responsibility for business management and those with responsibility for headquarters functions will be separated, and chief executives in charge of core Sony Group companies will be appointed "Senior Executive Vice President." In addition, the positions of Corporate Executive Officers will be reviewed in order to clarify their responsibility to stakeholders. <Executive Appointments> (as of June 1, 2020) [ Executives of equal rank are listed in order of appointment / changes to titles or areas of responsibility are underlined ] Kenichiro Yoshida Chairman, President and Chief Executive Officer Representative Corporate Executive Officer Hiroki Totoki Executive Deputy President and Chief Financial Officer Representative Corporate Executive Officer Shigeki Ishizuka Vice Chairman*1 Representative Corporate Executive Officer Officer in charge of Electronics Products & Solutions Business Officer in charge of Storage Media Business Representative Director, President and CEO, Sony Electronics Corporation Representative Director and President, Sony Imaging Products & Solutions Inc. Toru Katsumoto Executive Deputy President Corporate Executive Officer Officer in charge of R&D Officer in charge of Medical Business President, R&D Center Representative Director and Deputy President, Sony Imaging Products & Solutions Inc. -

Annual Report 2013 201 3 年

Annual Report 2013 201 3 年 3 月期 アニュアルレポート 2013年 3月期 ソニー株式会社 Annual Report 2013 Business and CSR Review Contents For further information, including video content, please visit Sony’s IR and CSR websites. Letter to Stakeholders: 2 A Message from Kazuo Hirai, President and CEO 16 Special Feature: Sony Mobile 22 Special Feature: CSR at Sony Business Highlights Annual Report 26 http://www.sony.net/SonyInfo/IR/financial/ar/2013/ 28 Sony Products, Services and Content 37 CSR Highlights 55 Financial Section 62 Stock Information CSR/Environment http://www.sony.net/csr/ 63 Investor Information Investor Relations http://www.sony.net/SonyInfo/IR/ Annual Report 2013 on Form 20-F Effective from 2012, Sony has integrated its printed annual http://www.sony.net/SonyInfo/IR/library/sec.html and corporate social responsibility (CSR) reports into Financial Services Business one report that provides essential information on related (Sony Financial Holdings Inc.) developments and initiatives. http://www.sonyfh.co.jp/index_en.html 1 Letter to Stakeholders: A Message from Kazuo Hirai, President and CEO 2 BE MOVED Sony is a company that inspires and fulfills the curiosity of people from around the world, using our unlimited passion for technology, services and content to deliver groundbreaking new excitement and entertainment to move people emotionally, as only Sony can. 3 Fiscal year 2012, ended March 31, 2013, was my first year as President and CEO of Sony. It was a year full of change that enabled us to build positive momentum across the Sony Group. Since becoming President, I visited 45 different Sony Group sites in 16 countries, ranging from electronics sales offices to manufacturing facilities, R&D labs, and entertainment and financial services locations. -

Disruptive Innovation and Internationalization Strategies: the Case of the Videogame Industry Par Shoma Patnaik

HEC MONTRÉAL Disruptive Innovation and Internationalization Strategies: The Case of the Videogame Industry par Shoma Patnaik Sciences de la gestion (Option International Business) Mémoire présenté en vue de l’obtention du grade de maîtrise ès sciences en gestion (M. Sc.) Décembre 2017 © Shoma Patnaik, 2017 Résumé Ce mémoire a pour objectif une analyse des deux tendances très pertinentes dans le milieu du commerce d'aujourd'hui – l'innovation de rupture et l'internationalisation. L'innovation de rupture (en anglais, « disruptive innovation ») est particulièrement devenue un mot à la mode. Cependant, cela n'est pas assez étudié dans la recherche académique, surtout dans le contexte des affaires internationales. De plus, la théorie de l'innovation de rupture est fréquemment incomprise et mal-appliquée. Ce mémoire vise donc à combler ces lacunes, non seulement en examinant en détail la théorie de l'innovation de rupture, ses antécédents théoriques et ses liens avec l'internationalisation, mais en outre, en situant l'étude dans l'industrie des jeux vidéo, il découvre de nouvelles tendances industrielles et pratiques en examinant le mouvement ascendant des jeux mobiles et jeux en lignes. Le mémoire commence par un dessein des liens entre l'innovation de rupture et l'internationalisation, sur le fondement que la recherche de nouveaux débouchés est un élément critique dans la théorie de l'innovation de rupture. En formulant des propositions tirées de la littérature académique, je postule que les entreprises « disruptives » auront une vitesse d'internationalisation plus élevée que celle des entreprises traditionnelles. De plus, elles auront plus de facilité à franchir l'obstacle de la distance entre des marchés et pénétreront dans des domaines inconnus et inexploités. -

Announcement of Executive Appointments and the New Management Team

April 26, 2019 Sony Financial Holdings, Inc. Announcement of Executive Appointments and the New Management Team Tokyo, April 26, 2019——At a Board of Directors’ meeting held today, Sony Financial Holdings Inc. (“SFH”) resolved candidates for election to the position of Directors and Audit & Supervisory Boad Members as stated below. These executive appointments are consistent with reinforcing the management structure to enhance the sustainable corporate value of the Sony Financial Group (“SFG”). We strengthen governance, centering on the Board of Directors at SFH, the holding company. The new executive appointments include outside directors, members of Sony Corporation’s management team, and people from SFH’s management team as directors of SFH. The presidents of the three main subsidiaries (Sony Life Insurance Co., Ltd., Sony Assurance Inc. and Sony Bank Inc.) are allowing them to dedicate themselves to the management of their businesses. Under the new management team, we aim to promote further growth among SFG’s individual businesses and manifest synergies across SFG. Following approval at the Ordinary Meeting of Shareholders, the election of the new management team is subject to the approval of the Board of Directors and the Audit & Supervisory Board, all of which are to be held on June 21, 2019. 1. Changes in Directors <As of June 21, 2019> (1) Resignation Name Current Position *The Position of President, Representative Director of Sony Tomoo Hagimoto Director Life Insurance Co., Ltd. continues. *The Position of President, Representative Director of Sony Atsuo Niwa Director Assurance Inc. continues. *The Position of President, Representative Director of Sony Yuichiro Sumimoto Director Bank Inc. -

Q3 2018 Earnings Prepared Remarks

NEXON Co., Ltd. Q3 2018 Earnings Conference Call Prepared Remarks Nov 8, 2018 Owen Mahoney, Representative Director, President and Chief Executive Officer, NEXON Co., Ltd. Thank you all very much for joining us today. I’m pleased to report that we had another great quarter, with our business delivering solid results around the world. The results represent record Q3 revenues, operating income, and net income, and we also delivered the highest quarterly mobile revenues in our history. These excellent results were primarily driven by the continued strength of our biggest franchises across the regions. The credit for the sustained growth in these franchises goes to the outstanding work by our live operations and live development teams around the world. The work by these incredibly talented people is the key to building a sustainably growing, SaaS-like business. We believe Nexon has the best live teams in the world. Our world-class live teams are one way Nexon is different from the traditional games industry model. The games industry has recently been re-tooling to digital online and recurring revenue models. That’s been Nexon’s approach since day 1. Another difference is how we build for the future. In the traditional games approach, most of your revenues comes from games that were recently launched, in the last 1-2 quarters. In an online approach, most of your revenues comes from games you launched well over a year ago. That difference means in the traditional approach, the key point of analysis was to look for catalysts, which means evaluating the pipeline of new product launches. -

Q2 2021 Earnings Prepared Remarks

NEXON Co., Ltd. Q2 2021 Earnings Prepared Remarks August 11, 2021 Owen Mahoney, Representative Director, President and Chief Executive Officer, NEXON Co., Ltd. Thank you, Ara-san, and welcome everyone to Nexon’s Second Quarter 2021 Conference Call. Today I will provide a brief update on our second quarter performance and devote the rest of my time to detailing the strategies that position Nexon for significant growth in the coming quarters and years. Following that I will turn the call over to our CFO, Uemura-san, for a detailed financial review of our quarter and the guidance for Q3. In the second quarter, Nexon delivered revenue that was within our outlook at 56.0Bn yen -- down 13% on an as-reported basis and down 21% on a constant currency basis. The Kingdom of the Winds: Yeon, Mabinogi, and Sudden Attack exceeded our expectations while MapleStory in Korea came in lower-than-expected. On a platform basis, both PC and mobile revenues were in the range of our outlook. In short, some things went better than expected; others not as well; with the net result putting us within our expected range. On today’s call, I will provide context on how the management team has been investing our time in 2021. We see 2021 as an operational inflection point for improving our live games and polishing multiple new projects - each with the potential for enormous returns. Executing on any...one of these initiatives could dramatically change Nexon’s trajectory and bring step- function improvements to our revenue and profitability. I will start with the actions we’ve taken to improve the performance of MapleStory in Korea, which is facing tough comparisons following the last two years of significant growth, including a 98% jump in year-over-year revenue in 2020. -

Qas(Summary) (PDF 112KB)

Q&A (Summary) of Corporate Strategy Meeting for Fiscal 2018 Date: May 31, 2018 (Thursday), 15:30–17:00 (JST) Respondents*: Shigeru Ishii, President, Representative Director of Sony Financial Holdings Inc. Hiroaki Kiyomiya, Managing Director, Member of the Board of Sony Financial Holdings Inc. Tomoo Hagimoto, President, Representative Director of Sony Life Insurance Co., Ltd. Atsuo Niwa, President, Representative Director of Sony Assurance Inc. Yuichiro Sumimoto, President, Representative Director of Sony Bank Inc. * Respondents’ positions are as of the date of the meeting. Note: The original content has been revised and edited for ease of understanding. [Q&A] Q1: [SFH] It seems to me that connecting Sony Life, Sony Assurance and Sony Bank via APIs and account aggregation and forging ties with other financial institutions would be effective. What are your thoughts in this regard? A: We believe that sharing the Sony Life information accumulated by Lifeplanner sales employees and Sony Bank information would enable us to realize further sophisticated services. However, cooperation that involves personal information requires customer permission, so at this point rather than sharing the information we currently hold we are thinking of building a new platform. Q2: [SFH] In your medium-term plan, you have set the goal of consolidated adjusted ROE of more than 5%, which is your target for raising dividends. At what level do you aim to increase dividends, and around what level do you expect dividends to be in the final year of the plan? Rather than raising dividends by ¥2.5, might you be expected to raise them by ¥5 depending on profit levels? A: Our basic thoughts are to raise dividends by ¥2.5 per fiscal year, but if consolidated adjusted ROE is significantly higher than 5%, we might consider raising dividends by more than ¥2.5. -

Business of Video Games

Business of Video Games Fall Semester, September 6 to December 16, 2016 Course number: MKTG-UB.58.001 Location: T-UC25 Instructor: Joost van Dreunen, [email protected] Class meets on Thursdays, from 4:55 pm to 6:10 pm. COURSE DESCRIPTION Abstract This class discusses the interactive entertainment industry, and looks at how business strategies inform aesthetic practices in the development, distribution, and marketing of video games. Course Summary Video games are now a mainstream form of entertainment. In economic terms, this industry has experienced tremendous growth, despite a grueling recession, growing to an estimated $110 billion worldwide. A key development that has changed the playing field for both the producers and consumers of interactive entertainment is a shift away from physical retail to digital and online game distribution. The audience for games has also shifted—no longer the exclusive practice of hardcore gamers, video games have gained mass appeal in the form of social and casual gaming, on the internet, on consoles, and smartphones. At the same time, the development and publishing of games has become far more accessible. The game behind the game, in a manner of speaking, has changed. In this class, we explore the basic components of the current video game industry. Every week, we review major current events, will hear from people currently working in the industry, examine case studies, and discuss the overall business landscape. Central to each class is the notion that practical business considerations and the design-driven creative process do not have to be in opposition. COURSE OBJECTIVE This course aims to provide students with: ★ An understanding of games industry characteristics, its drivers and major players; ★ An overview of historical and current strategy questions confronted by game companies; ★ A rudimentary set of games business-related solutions applicable toward the developed, publishing, and distribution of interactive entertainment; ★ Enough information about the video games industry to formulate a credible business plan. -

Voltage / 3639

Voltage / 3639 COVERAGE INITIATED ON: 2021.04.27 LAST UPDATE: 2021.05.10 Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and findings. We will always present opinions from company management as such. Our views are ours where stated. We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at [email protected] or find us on Bloomberg. Research Coverage Report by Shared Research Inc. Voltage / 3639 RCoverage LAST UPDATE: 2021.05.10 Research Coverage Report by Shared Research Inc. | https://sharedresearch.jp INDEX How to read a Shared Research report: This report begins with the trends and outlook section, which discusses the company’s most recent earnings. First-time readers should start at the business section later in the report. Executive summary ----------------------------------------------------------------------------------------------------------------------------------- 3 Key financial data ------------------------------------------------------------------------------------------------------------------------------------- 5 Recent updates ---------------------------------------------------------------------------------------------------------------------------------------- 6 Highlights ------------------------------------------------------------------------------------------------------------------------------------------------------------ -

Nexon Expands Partnership with Electronic Arts Inc. to Publish EA SPORTS™ FIFA MOBILE in Japan

July 28, 2020 NEXON Co., Ltd. http://company.nexon.co.jp/en/ (Stock Code: 3659, TSE First Section) Nexon Expands Partnership with Electronic Arts Inc. to Publish EA SPORTS™ FIFA MOBILE in Japan Globally Revered EA SPORTSTM FIFA MOBILE to Deliver Authentic Football Experience Supported by Nexon’s Best-in-Class Live Service Recruiting Closed Beta Testing from August 7 TOKYO – July 28, 2020 – NEXON Co., Ltd. (“Nexon”) (3659.TO), a global leader in online games, today announced that it is expanding its partnership with Electronic Arts Inc. (“EA”) to release and operate EA SPORTS™ FIFA MOBILE in Japan. The upcoming launch of FIFA MOBILE 1 in Japan is the latest in a series of FIFA collaborations between Nexon and EA over the last decade. Most recently, Nexon released FIFA MOBILE 1 in Korea in June, reached #1 in the popular games ranking for both Google Play and App Store and surpassing two million downloads within two months. In addition, Nexon’s hit online game EA SPORTS™ FIFA ONLINE 4 has continued to maintain its top spot within the sports game genre in Korea since its release in 2018. “The EA SPORTSTM FIFA series is an iconic game franchise enjoyed by millions of football fans around the world and we’re excited to release this new title to the Japanese audience,” said Chan Park, the Head of Business Division of Nexon. “Nexon has a long history of successfully running FIFA titles for years and we are looking forward to continuing that tradition and best-in-class operations with an expansive live service plan for FIFA MOBILE 1 in Japan.” 1 “EA is very pleased to partner with Nexon to provide the best service for our Japanese players. -

"JPX-Nikkei Index 400"

JPX-Nikkei Index 400 Constituents (applied on August 30, 2019) Published on August 7, 2019 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3107 1 Daiwabo Holdings Co.,Ltd. 1333 1 Maruha Nichiro Corporation 3116 1 TOYOTA BOSHOKU CORPORATION 1605 1 INPEX CORPORATION 3141 1 WELCIA HOLDINGS CO.,LTD. 1719 1 HAZAMA ANDO CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3167 1 TOKAI Holdings Corporation 1721 1 COMSYS Holdings Corporation 3197 1 SKYLARK HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1802 1 OBAYASHI CORPORATION 3254 1 PRESSANCE CORPORATION 1803 1 SHIMIZU CORPORATION 3288 1 Open House Co.,Ltd. 1808 1 HASEKO Corporation 3289 1 Tokyu Fudosan Holdings Corporation 1812 1 KAJIMA CORPORATION 3291 1 Iida Group Holdings Co.,Ltd. 1820 1 Nishimatsu Construction Co.,Ltd. 3349 1 COSMOS Pharmaceutical Corporation 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1824 1 MAEDA CORPORATION 3382 1 Seven & I Holdings Co.,Ltd. 1860 1 TODA CORPORATION 3391 1 TSURUHA HOLDINGS INC. 1861 1 Kumagai Gumi Co.,Ltd. 3401 1 TEIJIN LIMITED 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3402 1 TORAY INDUSTRIES,INC. 1881 1 NIPPO CORPORATION 3405 1 KURARAY CO.,LTD. 1893 1 PENTA-OCEAN CONSTRUCTION CO.,LTD. 3407 1 ASAHI KASEI CORPORATION 1911 1 Sumitomo Forestry Co.,Ltd.