What Is Slightly Disturbing Is That Local Radio in This Country Is

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Meeting of the Board of Directors in Public

Meeting of the Board of Directors in Public Wednesday 25 November 2015 from 09.00am Chelm sford City Council, Civic Centre, Duke Street, Chelmsford, Essex CM1 1JE 1 This Page Deliberately Blank 2 North Essex Partnership University NHS Foundation Trust Meeting of the Board of Directors to be held in Public on Wednesday 25 November 2015 in the Marconi Room, Civic Centre, Chelmsford City Council, Civic Centre, Duke Street, Chelmsford, Essex CM1 1JE at 09.00am Declarations and Minutes Lead Time Page 1. Apologies for Absence [Receive] CP 09.00 005 2. Declarations of Interest in Agenda Items [Receive] CP 09.00 006 3. a) Minutes of the Meeting held on 23 September 2015 CP 09.05 007 [Receive & Approve] b) Matters arising from the Minutes of the Meeting held CP 09.10 019 on 23 September 2015 [Discuss] 4. Chief Executive’s Report [Receive] AG 09.15 022 Quality 5. CQC Improvement Plan and Framework - Update [Receive] NH 09.25 024 6. Ligature Point Management and Removal [Receive] NH 09.40 032 7. Patient Survey 2015 – Results [Receive] MC 09.50 044 8. Service User and Patient Experience and Involvement MC 10.00 045 [Receive] Setting Strategy 9. Mental Health Strategic review - Update [Discuss & Note] MC 10.15 053 Comfort Break 10.30 Monitoring 10. Finance Report for the Seven Months Ending 31 October DG 10.45 054 2015 (Month 7) [Note] 11. Performance: a) Operational Performance Summary to 31 October VM 10.55 069 2015 [Receive & Note] b) Workforce Report [Receive & Note] LA 11.05 075 12. Nursing Agency Rules LA/DG 11.10 097 3 13. -

Completed Acquisition by Global Radio Uk Ltd of Gcap Media Plc

COMPLETED ACQUISITION BY GLOBAL RADIO UK LTD OF GCAP MEDIA PLC UNDERTAKINGS TO BE GIVEN BY GLOBAL RADIO UK LTD TO THE OFFICE OF FAIR TRADING PURSUANT TO SECTION 73 OF THE ENTERPRISE ACT 2002 WHEREAS: (a) On 6 June 2008 Global acquired GCAP; (b) It appears to the OFT that, as a consequence of that transaction, a relevant merger situation has been created in the UK; (c) The OFT has a duty to refer a completed merger to the CC for further investigation where it believes that it is or may be the case that the creation of that merger situation has resulted or may be expected to result in a substantial lessening of competition within any market or markets in the UK for goods or services; (d) Under section 73 of the Act the OFT may, instead of making such a reference and for the purpose of remedying, mitigating or preventing the substantial lessening of competition concerned or any adverse effect which may be expected to result from it, accept undertakings to take such action as it considers appropriate, from such of the parties concerned as it considers appropriate, in particular having regard to the need to achieve as comprehensive a solution as is reasonable and practicable to the substantial lessening of competition and any adverse effects resulting from it; (e) The OFT considers that, in the absence of appropriate undertakings, it would be under a duty to refer the acquisition of GCAP to the CC; and (f) The OFT further considers that the undertakings given below by Global are appropriate to remedy, mitigate or prevent the substantial lessening of competition, or any adverse effect which has or may have resulted from it, or may be expected to result from it, as specified in the Decision. -

Digital One’S Response to the Ofcom Consultation “Future Pricing of Spectrum Used for Terrestrial Broadcasting”

Digital One’s Response to the Ofcom Consultation “Future pricing of spectrum used for terrestrial broadcasting” 1. Digital One operates the UK’s only national commercial DAB digital radio multiplex. Its shareholders are GCap Media (63%) and Arqiva (37%). Digital One’s transmission network (which is operated by Arqiva) is the world’s biggest DAB digital radio network with coverage well in excess of 85% of the British population. Digital One’s multiplex broadcasts: - the three INRs (Classic FM, Virgin Radio and talkSPORT); - four digital-only national stations (Capital Life, Core, Oneword and Planet Rock) with a further station being launched in the next few months; - TV channels and an Electronic Programme Guide broadcast as part of BT Movio. Digital One is a leading stakeholder in the UK’s Digital Radio Development Bureau and the WorldDAB Forum (which is responsible for the DAB digital radio standard and works to coordinate the international roll-out of Eureka 147 based technologies). 2. Digital One is licensed under the 1996 Broadcasting Act, and has licence obligations which help deliver public policy benefits. These limit Digital One’s ability to use the spectrum it has been allocated in the most efficient manner (in economic terms). For example: - the obligation to operate a transmitter network which delivers high population coverage; - the obligation (at the direction of the Secretary of State for the Department of Culture, Media and Sport) to carry the three INRs and to offer each INR an amount of capacity dictated by the regulator; -

Classic FM Relocates

Classic FM Relocates Lawrie Hallett MIBS reports on Classic FM’s move last year to GCAP’s London Radio Centre. Classic FM’s production studio at Leicester Square n 9 May 2006 the UK’s two largest only when this rival group was unable to June/July 1999 edition of Line Up.) commercial radio companies – the raise the considerable pre-launch capital Classic FM enhanced its presence on O Capital Radio Group and the GWR needed for its proposed service that the FM (it now has 42 transmitters across the Group – completed their merger to form contract was awarded instead to Classic FM country) as well as raising its profile GCap Media plc. Soon after its formation, as the runner-up in the contest. through involvement in the ‘Digital 1’ and doubtless recognising the potential cost Once it had the green-light, Classic FM national DAB multiplex. It has also savings and operational synergies which wasted little time in getting on-air in 1993, broadcast via the Sky satellite TV system should arise, it was decided to consolidate and its transmitter network quickly since 1999 and the same service is available the London departments under a single expanded to cover 82% of the total on Virgin’s digital cable system, the Tiscali roof. The chosen location was what had population – just over the 80% required by (formerly Home Choice) network and, of been the Capital Group’s Leicester Square the INR1 licence. The old GWR Group had course, via the Internet. headquarters, so the former GWR broadcast provided technical expertise and support stations as well as a newly combined for the fledgling national broadcaster, and in Location, Location, Location national sales team have all taken up 1997 it bought out the entire company. -

Radio Evolution: Conference Proceedings September, 14-16, 2011, Braga, University of Minho: Communication and Society Research Centre ISBN 978-989-97244-9-5

Oliveira, M.; Portela, P. & Santos, L.A. (eds.) (2012) Radio Evolution: Conference Proceedings September, 14-16, 2011, Braga, University of Minho: Communication and Society Research Centre ISBN 978-989-97244-9-5 Live and local no more? Listening communities and globalising trends in the ownership and production of local radio 1 GUY STARKEY University of Sunderland [email protected] Abstract: This paper considers the trend in the United Kingdom and elsewhere in the world for locally- owned, locally-originated and locally-accountable commercial radio stations to fall into the hands of national and even international media groups that disadvantage the communities from which they seek to profit, by removing from them a means of cultural expression. In essence, localness in local radio is an endangered species, even though it is a relatively recent phenomenon. Lighter- touch regulation also means increasing automation, so live presentation is under threat, too. By tracing the early development of local radio through ideologically-charged debates around public-service broadcasting and the fitness of the private sector to exploit scarce resources, to present-day digital environments in which traditional rationales for regulation on ownership and content have become increasingly challenged, the paper also speculates on future developments in local radio. The paper situates developments in the radio industry within wider contexts in the rapidly-evolving, post-McLuhan mediatised world of the twenty-first century. It draws on research carried out between July 2009 and January 2011for the new book, Local Radio, Going Global, published in December 2011 by Palgrave Macmillan. Keywords: radio, local, public service broadcasting, community radio Introduction: distinctiveness and homogenisation This paper is mainly concerned with the rise and fall of localness in local radio in a single country, the United Kingdom. -

Hallett Arendt Rajar Topline Results - Wave 3 2019/Last Published Data

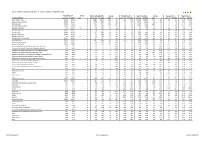

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2019/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W3 2019 000's % Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 000's % Last Pub W3 2019 Last Pub W3 2019 Bauer Radio - Total 55032 55032 0 0% 18083 18371 288 2% 33% 33% 156216 158995 2779 2% 8.6 8.7 15.3% 15.9% Absolute Radio Network 55032 55032 0 0% 4743 4921 178 4% 9% 9% 35474 35522 48 0% 7.5 7.2 3.5% 3.6% Absolute Radio 55032 55032 0 0% 2151 2447 296 14% 4% 4% 16402 17626 1224 7% 7.6 7.2 1.6% 1.8% Absolute Radio (London) 12260 12260 0 0% 729 821 92 13% 6% 7% 4279 4370 91 2% 5.9 5.3 2.1% 2.2% Absolute Radio 60s n/p 55032 n/a n/a n/p 125 n/a n/a n/p *% n/p 298 n/a n/a n/p 2.4 n/p *% Absolute Radio 70s 55032 55032 0 0% 206 208 2 1% *% *% 699 712 13 2% 3.4 3.4 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1779 1824 45 3% 3% 3% 9294 9435 141 2% 5.2 5.2 0.9% 1.0% Absolute Radio 90s 55032 55032 0 0% 907 856 -51 -6% 2% 2% 4008 3661 -347 -9% 4.4 4.3 0.4% 0.4% Absolute Radio 00s n/p 55032 n/a n/a n/p 209 n/a n/a n/p *% n/p 540 n/a n/a n/p 2.6 n/p 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 741 721 -20 -3% 1% 1% 3438 3703 265 8% 4.6 5.1 0.3% 0.4% Hits Radio Brand 55032 55032 0 0% 6491 6684 193 3% 12% 12% 53184 54489 1305 2% 8.2 8.2 5.2% 5.5% Greatest Hits Network 55032 55032 0 0% 1103 1209 106 10% 2% 2% 8070 8435 365 5% 7.3 7.0 0.8% 0.8% Greatest Hits Radio 55032 55032 0 0% 715 818 103 14% 1% 1% 5281 5870 589 11% 7.4 7.2 0.5% -

Bauer Media Group Phase 1 Decision

Completed acquisitions by Bauer Media Group of certain businesses of Celador Entertainment Limited, Lincs FM Group Limited and Wireless Group Limited, as well as the entire business of UKRD Group Limited Decision on relevant merger situation and substantial lessening of competition ME/6809/19; ME/6810/19; ME/6811/19; and ME/6812/19 The CMA’s decision on reference under section 22(1) of the Enterprise Act 2002 given on 24 July 2019. Full text of the decision published on 30 August 2019. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties or third parties for reasons of commercial confidentiality. SUMMARY 1. Between 31 January 2019 and 31 March 2019 Heinrich Bauer Verlag KG (trading as Bauer Media Group (Bauer)), through subsidiaries, bought: (a) From Celador Entertainment Limited (Celador), 16 local radio stations and associated local FM radio licences (the Celador Acquisition); (b) From Lincs FM Group Limited (Lincs), nine local radio stations and associated local FM radio licences, a [] interest in an additional local radio station and associated licences, and interests in the Lincolnshire [] and Suffolk [] digital multiplexes (the Lincs Acquisition); (c) From The Wireless Group Limited (Wireless), 12 local radio stations and associated local FM radio licences, as well as digital multiplexes in Stoke, Swansea and Bradford (the Wireless Acquisition); and (d) The entire issued share capital of UKRD Group Limited (UKRD) and all of UKRD’s assets, namely ten local radio stations and the associated local 1 FM radio licences, interests in local multiplexes, and UKRD’s 50% interest in First Radio Sales (FRS) (the UKRD Acquisition). -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 22Nd June 2008

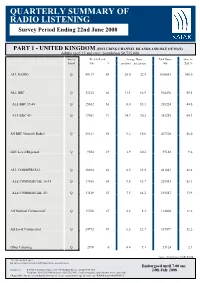

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 22nd June 2008 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 50,735,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % ALL RADIO Q 45117 89 20.0 22.5 1016681 100.0 ALL BBC Q 33323 66 11.1 16.9 564476 55.5 ALL BBC 15-44 Q 15362 61 8.0 13.1 201224 44.6 ALL BBC 45+ Q 17961 71 14.3 20.2 363252 64.3 All BBC Network Radio¹ Q 29611 58 9.2 15.8 467328 46.0 BBC Local/Regional Q 9504 19 1.9 10.2 97148 9.6 ALL COMMERCIAL Q 30984 61 8.5 13.9 431081 42.4 ALL COMMERCIAL 15-44 Q 17465 69 9.5 13.7 239533 53.1 ALL COMMERCIAL 45+ Q 13519 53 7.5 14.2 191547 33.9 All National Commercial¹ Q 13760 27 2.2 8.3 114002 11.2 All Local Commercial Q 24992 49 6.2 12.7 317079 31.2 Other Listening Q 2978 6 0.4 7.1 21124 2.1 Source: RAJAR/Ipsos MORI/RSMB ¹ See note on back cover. For survey periods and other definitions please see back cover. Embargoed until 7.00 am Enquires to: RAJAR, Paramount House, 162-170 Wardour Street, London W1F 8ZX 24th July 2008 Telephone: 020 7292 9040 Facsimile: 020 7292 9041 e mail: [email protected] Internet: www.rajar.co.uk ©Rajar 2008. -

Celebrating 40 Years of Commercial Radio With

01 Cover_v3_.27/06/1317:08Page1 CELEBRATING 40 YEARS OF COMMERCIAL RADIOWITHRADIOCENTRE OFCOMMERCIAL 40 YEARS CELEBRATING 01 9 776669 776136 03 Contents_v12_. 27/06/13 16:23 Page 1 40 YEARS OF MUSIC AND MIRTH CONTENTS 05. TIMELINE: t would be almost impossible to imagine A HISTORY OF Ia history of modern COMMERCIAL RADIO music without commercial radio - and FROM PRE-1973 TO vice-versa, of course. The impact of TODAY’S VERY privately-funded stations on pop, jazz, classical, soul, dance MODERN BUSINESS and many more genres has been nothing short of revolutionary, ever since the genome of commercial radio - the pirate 14. INTERVIEW: stations - moved in on the BBC’s territory in the 1960s, spurring Auntie to launch RADIOCENTRE’S Radio 1 and Radio 2 in hasty response. ANDREW HARRISON From that moment to this, independent radio in the UK has consistently supported ON THE ARQIVAS and exposed recording artists to the masses, despite a changing landscape for AND THE FUTURE broadcasters’ own businesses. “I’m delighted that Music Week 16. MUSIC: can be involved in celebrating the WHY COMMERCIAL RadioCentre’s Roll Of Honour” RADIO MATTERS Some say that the days of true ‘local-ness’ on the UK’s airwaves - regional radio for regional people, pioneered by 18. CHART: the likes of Les Ross and Alan Robson - are being superseded by all-powerful 40 UK NO.1 SINGLES national brands. If that’s true, support for the record industry remains reassuringly OVER 40 YEARS robust in both corners of the sector. I’m delighted that Music Week can be involved in celebrating the RadioCentre’s 22. -

The Digitalisation of Radio

The digitalisation of radio How the United Kingdom has handled the rollout of digital radio – lessons for New Zealand. A report for the Robert Bell Travelling Scholarship University of Canterbury Kineta Knight May 2009 CONTENTS Introduction 3 DAB – an overview 5 Part One – New Zealand media figures react to DAB 6 Part Two – DAB in the United Kingdom DAB terminology 8 Introduction 9 Establishing DAB in the UK: the benefits 13 Barrier to not adopting DAB 16 Launching DAB 17 Cost of DAB 19 Logistics of starting up DAB 20 Promoting DAB 21 Consumer uptake of DAB sets 22 Downfalls of DAB 24 The infamous pulling-out GCap 28 Internet streaming vs. DAB 30 Part Three – Current state of DAB in the United Kingdom Introduction 32 How the recession has affected DAB 33 Channel 4 35 DRWG – the way forward 38 DAB’s future in the UK 40 DAB+ for the future? 42 Part Four – Would DAB+ work in New Zealand? 44 Conclusions and recommendations 46 Works cited 48 2 Introduction Digital technology is now at the forefront of international media, quickly leaving the analogue medium behind. With the evolution of television in New Zealand moving into the digital age, such as Sky Television and the introduction of Freeview, the switching of radio from analogue to a digital form promises to follow closely behind. The reason digital radio is of major interest in New Zealand is because the Government, along with a digital service provider and some of the nation’s major broadcasters, have been trialling a digital service. But, for New Zealand there are still uncertainties over which digital option to choose, how best to introduce it and control growth, what impact it will have on existing stations, and what will happen to the current market when new stations are established? New Zealand broadcasting and telecommunications company Kordia has already trialled a digital service, Digital Audio Broadcasting (DAB), but the Government is yet to commit to a long-term rollout of the technology. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 25Th June 2017

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 25th June 2017 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 54,466,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 49206 90 19.0 21.0 1033226 100.0 All BBC Radio Q 34945 64 9.9 15.5 539982 52.3 All BBC Radio 15-44 Q 14249 56 5.7 10.2 144999 38.0 All BBC Radio 45+ Q 20696 71 13.6 19.1 394983 60.6 All BBC Network Radio1 Q 32136 59 8.5 14.5 464642 45.0 BBC Local Radio Q 8632 16 1.4 8.7 75340 7.3 All Commercial Radio Q 35881 66 8.5 13.0 464812 45.0 All Commercial Radio 15-44 Q 18510 73 8.8 12.0 222329 58.3 All Commercial Radio 45+ Q 17371 60 8.3 14.0 242483 37.2 All National Commercial1 Q 19905 37 3.2 8.7 172369 16.7 All Local Commercial (National TSA) Q 27277 50 5.4 10.7 292443 28.3 Other Radio Q 3903 7 0.5 7.3 28431 2.8 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 3rd August 2017 information for the purposes of the Criminal Justice Act 1993. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 3Rd April 2016

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 3rd April 2016 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 53,575,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 47823 89 18.8 21.0 1006462 100.0 All BBC Radio Q 34869 65 10.2 15.6 544682 54.1 All BBC Radio 15-44 Q 14423 57 5.8 10.2 147513 39.1 All BBC Radio 45+ Q 20446 72 14.1 19.4 397169 63.1 All BBC Network Radio1 Q 32014 60 8.8 14.7 469102 46.6 BBC Local Radio Q 8793 16 1.4 8.6 75580 7.5 All Commercial Radio Q 34277 64 8.1 12.7 434436 43.2 All Commercial Radio 15-44 Q 18057 71 8.6 12.0 217166 57.5 All Commercial Radio 45+ Q 16221 57 7.7 13.4 217270 34.5 All National Commercial1 Q 18220 34 2.7 8.1 147175 14.6 All Local Commercial (National TSA) Q 26884 50 5.4 10.7 287261 28.5 Other Radio Q 3816 7 0.5 7.2 27344 2.7 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Please note that the information contained within this quarterly data release has yet to be announced or otherwise made public Embargoed until 00.01 am and as such could constitute relevant information for the purposes of section 118 of FSMA and non-public price sensitive 19th May 2016 information for the purposes of the Criminal Justice Act 1993.