2019 Full Year Results ASX Appendix 4E

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

June 2011 Yearly Report

Alleron Investment Management Limited Yearly Report June 2011 Portfolio performance and attribution analysis Market commentary Portfolio commentary Since Inception (Annualised) Year to Date Global markets were lead, over Positives: financial year, by the strong per- CEU: The company’s revenue such Portfolio +10.297% +4.468% formance of the US market which that cash flow now funds their dis- Benchmark + 6.158% +11.503% responded strongly to Federal Re- tribution and reduces their risk pro- serve Bank policy of a second round file. Top 3 and bottom 3 performing stocks of quantitative easing. This along AXA: The stock price was sup- Top 3: ConnectEast Group (CEU), AXA Asia Pacific Holdings with continued government spend- (AXA), Oil Search (OSH). ported by the accepted takeover ing allowed the US economy and offer from AMP and AXA SA. company earnings to maintain Bottom 3: Seven West Media Limited (SWM), Resmed Inc. (RMD), growth into the beginning of 2011. OSH: The company has secured Computershare (CPU). While growth in the US continued, offtake agreements to their LNG European countries were besieged output which remains on schedule. Portfolio changes by the familiar problem of periph- Negatives: Stocks joined or increased significantly: eral nation debt and increased risks of sovereign debt default. Contrar- SWM: Company earnings were hurt Downer Limited (+2.25% New Stock): An Engineering and Contract- ily, strong activity in emerging by weak advertising activity from ing company. The company has developed a strong order book pro- economies has forced monetary uncertainly over the resource tax. viding significant growth potential and has cleared the way to success- authorities there to tighten policy to RMD: Earnings translation was hurt fully complete troubled contracts. -

Monthly NTA and Performance Update

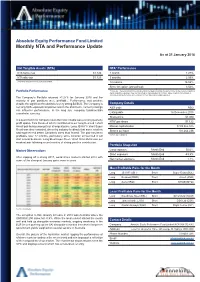

Absolute Equity Performance Fund Limited Monthly NTA and Performance Update As at 31 January 2018 Net Tangible Assets (NTA) NTA* Performance NTA before tax $1.122 1 month 1.27% NTA after tax $1.123 3 months 2.59% $ currency notation refers to Australian Dollars. 12 months 16.02% Since inception (annualised) 3.52% Portfolio Performance *Before tax. These calculations are unaudited and intended to illustrate the performance of the investment portfolio minus corporate expenses. They are calculated on a pre-dividend NTA basis. ‘Since inception (annualised)’ is annualised NTA performance since listing at $1.065 after listing related expenses The Company’s Portfolio returned +1.27% for January 2018 and the majority of pair positions were profitable. Performance was positive despite the significant headwind of a very strong $A/$US. The Company is Company Details net long $US-exposed companies and in the short term, currency swings ASX code AEG can influence performance. In the long run, company fundamentals overwhelm currency. Listing date 16 December 2015 Share price $1.080 In a quiet month for company news the most notable was a strong quarterly NTA* per share $1.122 profit update from Resmed which contributed to our long Resmed / short Ansell pair being amongst our strongest pairs. Long JB Hi-Fi / short Super Market capitalisation $109,365,375 Retail was also rewarded, driven by industry feedback that some retailers Shares on Issue 101,264,236 had experienced better Christmas sales than feared. The pair has been profitable over 12 months, particularly since Amazon announced it will *Before tax ex-dividend start a local business. -

June 2019 42

y 4 6 Equit 2019 June High Conviction High Quarterly NewsletterQuarterly No. Selector Fund In this quarterly edition, we review performance and attribution for the quarter. We highlight the importance of innovation and culture within organisations and profile ResMed and Cochlear, two leading healthcare businesses. We visit Fisher & Paykel Healthcare in New Zealand and look at one of the biggest growth industries in the world today, cyber security. Photo. Selector analyst trekking through the Atlas Mountains and local Berber kids. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 8, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au P Selector is a boutique fund manager. Our team, combined, have over 150 years of experience in financial markets. We believe in long-term wealth creation and building lasting relationships with our investors. We focus on stock selection, the funds are high conviction, concentrated and index unaware. As a result, the portfolios have low turnover and produce tax effective returns. Selector has a 15-year track record of outperformance and we continue to seek businesses with leadership qualities, run by competent management teams, underpinned by strong balance sheets and with a focus on capital management. Selector High Conviction Equity Fund Quarterly Newsletter #64 CONTENTS IN BRIEF – JUNE QUARTER 3 PORTFOLIO OVERVIEW 5 PORTFOLIO CONTRIBUTORS 7 MARKET INSIGHTS AND OBSERVATIONS 13 INNOVATION + CULTURE = SUCCESS 17 RESMED INC. 20 WAKE-UP CALL 31 FISHER & PAYKEL HEALTHCARE – JUNE 2019 42 RISK OUT…UPFRONT 45 COMPANY VISIT DIARY – JUNE 2019 QUARTER 57 2 Selector Funds Management IN BRIEF – JUNE QUARTER Dear Investor, Looking back on 2019, it would be fair to say that few identify the businesses we want to own on a case by case foresaw how the events of the financial year would basis, understand them to the best of our abilities and unfold. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Blasting Without Wires in Surface and Underground

DRILLING AND BLASTING Blasting without wires in surface and underground A WebGen™ unit is encoded at CMOC Northparkes mine by an Orica engineer, ready for loading. ince the launch of WebGen™, the ENABLING NEW MINING METHODS UNDERGROUND world’s first wireless initiating system WebGen™ has demonstrated its success in various in early 2017, Orica has executed underground mines and led to the development of several more than 500 blasts fired using the new mining techniques that would have otherwise been wireless technology in both surface deemed impossible to execute without wireless blasting S and underground mines around the technology. world. At Musselwhite mine, an underground mine owned and WebGen™ is one of the most exciting blasting technologies operated by Newmont, located on the southern shore of to be developed since the introduction of electronic blasting Lake Opapimiskan in Canada uses a Temporary Rib Pillar systems in the early 2000’s. This revolutionary system (TRP) method enabled by WebGen™ to extract ore pillars allows for groups of in-hole primers to be wirelessly that previously could not be recovered in underground initiated by a firing command that communicates through operations. rock, air and water. This eliminates the need for down- wires and surface connecting wires, enabling new mining Using the WebGen™ enabled TRP method, the main ore methods and blasting techniques that are safe and reliable of the panel were blasted and extracted while the TRP held – removing people from harm’s way, reducing operating back the waste rock backfill. For Newmont, this delivered costs, and at the same time increasing productivity benefits. -

Annual Report 1999 an International Financial Services Group

An international financial services group Annual Report 1999 National Australia Bank Limited ACN004044937 The National’s International Franchise Our Vision Contents To be the world’s leading financial services company. 1999 @ a Glance 2 Our Mission Financial Highlights 4 We tailor financial services to help Corporate Highlights 6 individuals, families, businesses and The Board of Directors 8 communities to achieve their goals. Group Leadership Team 10 Our Values Year in Review by the Chairman Service to our customers and the Managing Director 11 Quality in everything we do Business and Personal Professionalism and ethics in all our Financial Services 16 actions Products and Services 18 Competitiveness and a will to win Growth and development of our Global Wholesale Financial Services 20 people National Services Information Continuous productivity improvement Technology Enterprises 22 Growing profit for our stakeholders Community Relations 24 Key Business Units 26 Financial Information and Analysis Description of Business 30 Financial Review 36 Financial Calendar United Kingdom Asia Australia United States Report of the Directors 75 15 December 1999 Final dividend payable Financial Report Financial Statements 80 16 December 1999 Annual General Meeting Notes to the 27 January 2000 1999–2000 Q1 Results Financial Statements 84 Directors’ Declaration 165 4 May 2000 1999–2000 Q2 Results Auditors’ Report 165 July 2000 Interim 1999–2000 dividend paid Form 20-F Cross Reference Index 166 27 July 2000 1999–2000 Q3 Results Shareholder Information -

Orora Investor Briefing November 2013 Contents

Orora Investor Briefing November 2013 Contents • The demerger of Orora Limited • About Orora Limited • Strategic Direction of Orora • Orora Leadership • Board & Management Teams • Summary Orora Ltd 2 The demerger of Orora Limited The steps to the demerger 3 Demerger to be completed this calendar year Event Date Announced intention to demerge 1 August 2013 Scheme Booklet lodged with ASX 1 November 2013 Scheme and General Meeting (SGM) 9 December 2013 Demerger effective date (last date Amcor shares will trade cum-entitlement) 17 December 2013 Orora shares commence trading (deferred settlement basis) 18 December 2013 Scheme record date 24 December 2013 Demerger implemented 31 December 2013 Orora shares commence trading (normal settlement basis) 3 January 2014 Process is “on track” Orora Ltd 4 About Orora Limited The newest global packaging brand 5 Orora is set up for success • Strong, well-positioned core business • Focused portfolio & good industry structures • Stable, defensive earnings streams • Experienced Board & Executive Team with track record of performance • Cost reduction opportunities a key factor in expected near term earnings growth • Strong financial profile/metrics • Strong balance sheet • Well-capitalised businesses • Near-term earnings growth in company’s direct control • Strong cash flows • Proposed dividend payout 60 – 70% - dividends to be franked to the extent practicable • Disciplined approach to future growth • Capital management optionality Orora Ltd 6 The Orora Limited Group – A focused company Orora Australasia 26 -

2019 Voting Record As at 30 June 2019

2019 Voting Record as at 30 June 2019 Solaris Core Australian Equity Fund Solaris High Alpha Australian Equity Fund Solaris Core Australian Equity Fund (Total Return) Stock Company Name Meeting Date Item Resolutions Solaris Resolution Management/ Decision Type Shareholder Proposal MQG Macquarie Group Limited 26/07/2018 2a Elect Peter H Warne as Director For Ordinary Management MQG Macquarie Group Limited 26/07/2018 2b Elect Gordon M Cairns as Director For Ordinary Management MQG Macquarie Group Limited 26/07/2018 2c Elect Glenn R Stevens as Director For Ordinary Management MQG Macquarie Group Limited 26/07/2018 3 Approve the Remuneration Report For Ordinary Management MQG Macquarie Group Limited 26/07/2018 4 Approve Participation of Nicholas Moore in the Macquarie Group Employee Retained Equity Plan For Ordinary Management MQG Macquarie Group Limited 26/07/2018 5 Approve Issuance of Macquarie Group Capital Notes For Ordinary Management JHX James Hardie Industries plc 10/08/2018 1 Accept Financial Statements and Statutory Reports For Ordinary Management JHX James Hardie Industries plc 10/08/2018 2 Approve the Remuneration Report For Ordinary Management JHX James Hardie Industries plc 10/08/2018 3a Elect Persio Lisboa as Director For Ordinary Management JHX James Hardie Industries plc 10/08/2018 3b Elect Andrea Gisle Joosen as Director For Ordinary Management JHX James Hardie Industries plc 10/08/2018 3c Elect Michael Hammes as Director For Ordinary Management JHX James Hardie Industries plc 10/08/2018 3d Elect Alison Littley as Director -

(ASX100) Women on Boards Analysis

Australia/NZ | Australia Thematic Investing (Citi) Equities 18 August 2011 │ 32 pages ESG: ASX100 Women on Board Analysis Increasing Focus on Board Diversity Women on Boards of ASX100 Companies — The ASX Corporate Governance Council’s new principles and recommendations on diversity commenced on 1 January Elaine Prior 2011. This is likely to lead to increasing focus on companies’ approaches to diversity +61-2-8225-4891 issues, including female representation on company boards. This report looks at data [email protected] on women directors on ASX100 company boards. The number of women directors has Felipe Faria increased, particularly in recent months (Figure 5 to Figure 8). Board diversity may [email protected] enhance effectiveness, by providing a wider range of perspectives and knowledge. Women on Boards Data — We collected and analysed data on female board directors of S&P/ASX100 companies from FY08 to 8 August 2011 (Figure 5 to Figure 9). At 8 August 2011 there were 134 women on ASX100 boards, a 46% increase from FY08. ASX100 companies with no female board directors were AQP, CQO, EGP, FMG, IPL, JHX, LEI, LYC, OSH, PDN, PRY, RHC, RMD, SGM and SWM. Companies with three female directors (the highest number identified) are AMP, BEN, CBA, MQG, QAN, QBE and WBC. Seven female directors each currently hold three ASX100 directorships. Business Case for Gender Diversity — Reibey Institute research found that those ASX500 companies with women directors on 30 June 2010 had a 3-year return on equity (ROE) 10.7% higher than those without any women directors. The 5-year ROE was 11.1% higher. -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Amcor Rigid Plastics June 2017 Agenda 02

Amcor Rigid Plastics June 2017 Agenda 02 1 Safety briefing 2 Amcor Rigid Plastics a Key Messages b Leadership Team c Business Overview d Latin America Update 3 Amcor Rigid Plastics North America f Key Messages g Business Overview 4 Summary Safety – Manchester Evacuation Route 03 Safe zone Safety instructions for fire emergency: Exit through cafeteria Walk away from the building Turn left, proceed to safe zone Lobby Area Staying safe Required safety behaviors for visitors 04 Listen to your guide and pay attention to signs. Obey all instructions (verbal or written) Take Action, Take Care! is Amcor’s safety philosophy and a cornerstone of staying safe in our site. If you see something you think is No jewelry unsafe during your visit, Take Action Consult your guide in case No mobile phones by telling your guide. Take Care of of concern yourself and others by staying with your guide at all times, not touching anything, and following a few basic rules: Pay attention to vehicles and stay in No cameras allowed on site pedestrian walkways Except by special permission Make eye contact with drivers before crossing pathways Don’t touch machinery Hold the handrails on stairs or equipment Agenda 05 1 Safety briefing 2 Amcor Rigid Plastics a Key Messages b Leadership Team c Business Overview d Latin America Update 3 Amcor Rigid Plastics North America f Key Messages g Business Overview 4 Summary Amcor Rigid Plastics Key Messages 06 Safety is always the top priority Outstanding leaders committed to outperformance and delivering value to stakeholders Strong position: footprint, markets, technology and customers In attractive segments With substantial growth potential Amcor Rigid Plastics Safety Highlights 07 Co-worker safety is always our top priority.