Quarterly Market Report JANUARY 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Major Lease Transactions Downtown Houston

MAJOR LEASE TRANSACTIONS DOWNTOWN HOUSTON This is a comprehensive list of publicly available leases in Downtown Houston, including new-to-Downtown, expansions and renewals. Year Company Type To From Square Feet 512,845 Enterprise Plaza 2020 Enterprise Products Partners Renewal (incl. 2019 (1100 Louisiana) expansion: 22,301) 2020 JP Morgan Chase New/Relocation 600 Travis 1111 Fannin 253,230 5 Houston Center 2020 Venture Global LNG Renewal/Expansion 58,514 (1401 McKinney) (Expansion: 29,257 2020 Summit Midstream Partners, LP New to Downtown/Sublease 910 Louisiana The Woodlands 48,632 LyondellBasell Tower 2020 Mitsubishi International Corporation Renewal 45,838 (1221 McKinney) Pennzoil Place – North Tower 2020 Cheniere Energy Expansion 33,127 (700 Milam) Texas Tower Wells Fargo Plaza 2020 DLA Piper Relocation/Expansion 31,843 (845 Texas) (1000 Louisiana) (Expansion: 6,836) Bank of America Tower 2020 Waste Management Expansion 31,750 (800 Capitol) USA: Office of the Comptroller and Fulbright Tower 2020 Renewal 27,223 Office of the Currency (1301 McKinney) One Allen Center 2020 TPC Group Renewal 24,803 (500 Dallas) Fulbright Tower 2020 AXIP Energy Services Renewal 24,657 (1301 McKinney) 2020 Chevron Expansion 1600 Smith 23,699 2020 Plains All American Refining, L.P. Expansion Three Allen Center (333 Clay) 23,172 Source: Central Houston, Inc. Updated 08-31-2020. 1 Year Company Type To From Square Feet 2020 Lone Star Legal Aid Renewal 500 Jefferson 20,020 2020 Squire Patton Boggs Renewal 600 Travis 15,641 2 Houston Center 2020 USA: Office of the Comptroller Renewal 14,624 (909 Fannin) 2020 Rockcliff Energy, LLC Renewal 1301 McKinney 14,403 (Short-Term) 2020 Enbridge, Inc. -

A Self-Guided Walking Tour of Downtown Houston's Buildings

Tunnel Geology: A Self-Guided Walking Tour of Downtown Houston’s Buildings (2019) TEAL LOOP – 1/8 MILE (~10 MIN) FROM TOTAL PLAZA TO ENTERPRISE PLAZA Flooring Granodiorite (grey intermediate intrusive igneous) Granodiorite (quartz 20-60% and plagioclase 65- 90%) with uniform small-medium grained crystals, weathering present in different tiles Accent Slate (dark grey-green low grade metamorphic) 1 Copyright © 2019 Red Shoes. Red Wine. www.redshoesredwine.com ENTERPRISE PLAZA – 1100 LOUISIANA Flooring/Walls Tufa (Travertine, continental sedimentary) Travertino Romano (trade) from Tivoli near Rome in Italy Also known as Romano Classico or Travertine Classico and Travertino Romano Antico (darker varieties) Walls and flooring all travertine Tufa/Travertine: formed by algae/calcium carbonate in hot springs, phytoherms (freshwater reefs) and thrombolite-stromatolites; not to be confused with tuff/tufo (igneous) Tunnel Geology: A Self-Guided Walking Tour of Downtown Houston’s Buildings (2019) 2 TEAL LOOP – 1/8 MILE (~10 MIN) Observed: stromatolite patterns/precipitation growth dominant feature, some vugs partially to fully filled with more transparent cement ONE ALLEN CENTER – 500 DALLAS Flooring/Walls Fossiliferous Limestone (light tan sedimentary) Observed: gastropod fossilsand others unidentified Accents Marble (brown metamorphic) “Dirty” marble with fractures and calcite veins Marble veins: due to various mineral impurities such as clay, silt, sand Transition into Circular Court Best guess: Diabase/Gabbro (dark grey-black mafic intrusive igneous) -

Major Lease Transactions Downtown Houston

MAJOR LEASE TRANSACTIONS DOWNTOWN HOUSTON This is a comprehensive list of publicly available leases in Downtown Houston, including new‐to‐Downtown, expansions and renewals. Year Company Type To From Square Feet 512,845 Enterprise Plaza 2020 Enterprise Products Partners Renewal (incl. 2019 (1100 Louisiana) expansion: 22,301) 2020 JP Morgan Chase New/Relocation 600 Travis 1111 Fannin 253,230 2020 EP Energy Relocation/Sublease 601 Travis 1001 Louisiana 62,261 5 Houston Center 2020 Venture Global LNG Renewal/Expansion 58,514 (1401 McKinney) (Expansion: 29,257 2020 Summit Midstream Partners, LP New to Downtown/Sublease 910 Louisiana The Woodlands 48,632 LyondellBasell Tower 2020 Mitsubishi International Corporation Renewal 45,838 (1221 McKinney) 2020 Indigo Minerals Renewal 600 Travis 45,125 Pennzoil Place – North Tower 2020 Cheniere Energy Expansion 33,127 (700 Milam) Texas Tower Wells Fargo Plaza 2020 DLA Piper Relocation/Expansion 31,843 (845 Texas) (1000 Louisiana) (Expansion: 6,836) Bank of America Tower 2020 Waste Management Expansion 31,750 (800 Capitol) USA: Office of the Comptroller and Fulbright Tower 2020 Renewal 27,223 Office of the Currency (1301 McKinney) 2020 Riviera Resources Relocation 717 Texas 600 Travis 27,114 One Allen Center 2020 TPC Group Renewal 24,803 (500 Dallas) Source: Central Houston, Inc. Updated 09-30--2020. 1 Year Company Type To From Square Feet Fulbright Tower 2020 AXIP Energy Services Renewal 24,657 (1301 McKinney) 2020 Chevron Expansion 1600 Smith 23,699 2020 Plains All American Refining, L.P. Expansion Three Allen Center (333 Clay) 23,172 2020 Momentum Midstream Renewal 600 Travis 22,575 2020 Lone Star Legal Aid Renewal 500 Jefferson 20,020 2020 Squire Patton Boggs Renewal 600 Travis 15,641 2 Houston Center 2020 USA: Office of the Comptroller Renewal 14,624 (909 Fannin) 2020 Rockcliff Energy, LLC Renewal 1301 McKinney 14,403 2020 Enbridge, Inc. -

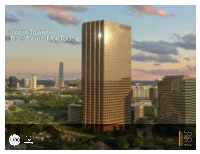

Iconic Tower — Transformed for Today Rebuilding the Tenant Experience from the Ground Up

Iconic Tower — Transformed for Today Rebuilding the tenant experience from the ground up —————— —————— This landmark tower has been transformed A new freestanding restaurant with an engaging into a modern, sustainable, innovation hub to outdoor space will be ideal for activities; a new food support Houston’s leading creative companies — hall-style café on the ground level offers healthy designed to meet or exceed the demands and convenient menu options; new common-areas of a changing workforce, today and tomorrow. include a comfortable lobby lounge ideal for coffee, —————— connecting or disconnecting; plus access to a spa- Meticulously maintained and operated since styled fitness center featuring health and wellness this iconic property was first commissioned as activities for group or self-paced programs. a global corporate headquarters by a leading —————— energy company. 5555 San Felipe is owner-operated and —————— maintained with an eco-friendly and sustainable With a focus on helping modern organizations approach. Our award-winning project is LEED Gold inspire talent, every aspect of the renovation certified and participates in various campaigns delivers a more perfect balance between hospitality for recycling, conservation and green-building and workspace — from the arrival experience, to operations. At every level, our tenants and their three levels of new and enhanced amenities. satisfaction come first. Transformation —————— Everything your team needs to thrive M-M Properties set a vision of rebuilding the tenant experience from the ground up. There are new modern finishes, three full floors of curated amenities and light-filled spaces. There will also be a new, freestanding signature restaurant. 5555 San Felipe is an inspired and FREESTANDING RESTAURANT – ACTIVITY LAWN collaborative office environment — the destination workplace — for today’s valuable employees. -

Downtown Houston Development Continues Despite Covid-19

MEDIA CONTACTS Angie Bertinot / Central Houston [email protected] / 713-650-3022 Whitney Radley / The CKP Group [email protected] / 832-930-4065 x 106 FOR IMMEDIATE RELEASE JANUARY 19, 2021 DOWNTOWN HOUSTON DEVELOPMENT CONTINUES DESPITE COVID-19 More than $1.9 billion in construction projects currently underway with more on the horizon HOUSTON, TX — While the Greater Houston Area begins to recover from the COVID-19 pandemic, Downtown Houston has shown its trademark resilience and grit in the face of the unexpected. Over the past year, office employees have adapted to working from home, hospitality groups have rolled out new services options and staycations, residential properties have adopted technology to conduct virtual space tours and the construction sector has continued grow. More than $1.9 billion in construction projects are currently underway in Downtown Houston, an area defined by IH-45 to the west and south, Highway 59 to the east and IH-10 to the north. “In recent years, Downtown Houston has transitioned from a central business district to a prime destination to live, work, play and stay,” said Bob Eury, president and CEO of the Houston Downtown Management District. “While the pandemic has resulted in some set- backs, we’re seeing confidence in the market: businesses and office employees have adapted to the new normal with agility, developers are leveraging the opportunity to maximize construction across all sectors and the area remains a culinary and cultural destination for Houstonians and visitors.” Office Projects Downtown Houston remains a dynamic business center with a workforce of approximately 158,000 employees and more than 51 million square feet of office space. -

Houston's Office Market Weakens Over the Quarter and Braces Itself Moving

Research & Forecast Report HOUSTON | OFFICE Q1 2020 Houston’s office market weakens over the quarter and braces itself moving forward amid $20 oil Lisa Bridges Director of Market Research | Houston Commentary by Patrick Duffy MCR Market Indicators Annual Quarterly Quarterly Colliers generally uses this space to discuss the trends we see Relative to prior period Change Change Forecast* in market data and in conversations we have with our clients, prospects and friendly competitors. We take that data and attempt VACANCY to project activity going forward. The bulk of the first quarter was, NET ABSORPTION for all practical purposes, pre-COVID. Net “move-in” data, as well as new leases signed, were likely unimpacted for Q1 based on the DELIVERIES virus or only marginally impacted. Our industry has a lead time of UNDER CONSTRUCTION at least 4-6 months before a lease is signed or space made ready for occupancy. The real impact of this COVID crisis will not present *Projected in the data until later in Q2. Inertia will carry us for a few more weeks. The world is focused on the COVID driven economic slowdown. Houston has two issues to watch – COVID and a collapse in oil prices. The oil issue is driven by Saudi Arabia and Russia failing to reach an agreement on production and by the severe decline of oil and gas demand driven by the COVID shutdown. Oil has been Summary Statistics Houston Office Market Q1 2019 Q4 2019 Q1 2020 in the low 20’s since the collision of these two events. The Energy Information Administration is projecting that supply will continue to Vacancy Rate 19.4% 19.8% 20.0% outpace demand for the balance of this year by approximately 10MM barrels per day. -

Downtown Houston Market Update

Q 3 2019 Downtown Houston Market Update Central Houston and Houston Downtown Management District Downtown had a busy summer particularly with hotel openings and property ren- ovations. The AC Hotel by Marriott opened in July in the 105-year-old renovated Houston Bar Center and is the first AC-branded property in Houston and the second in Texas. The European-themed hotel is 10 stories, has 195 guest rooms, spans a total 92,833 square feet and features a 3,650-square-foot Zoe Ballroom, formerly the site of a silent movie theater. Cambria Hotel Houston Downtown Convention Center opened shortly afterwards in early-August. The historic building, built in 1926, is formerly known as the Great Southwest Building and the Petroleum Building and features 226 rooms, a fitness center, ballroom and multifunction meeting spaces. Downtown Houston Market Report Q3 2019 1 EXEcuTIVE SummARY (CONTINUED) This is also the first Houston location for Cambria Hotel & Suites, part of Choice Hotels International Inc. Lastly, the 354-room C. Baldwin Hotel will officially debut its property-wide remake in October under Hilton’s Curio Collection, a franchise based on its own historic hotel-themed identity. Located in the C. Baldwin is celebrity chef Chris Cosentino’s 145-seat restaurant, Rosalie Italian, that will serve rustic, Italian American fare including breakfast, lunch, dinner and a Sunday brunch featuring its Sunday Gravy dinners. Meanwhile, several large renovation projects were in the headlines during the third quarter. The Four Seasons Hotel Houston announced in September it is proceed- ing with a $16.6 million upgrade and is presently finalizing plans and timeline. -

Major Lease Transactions Downtown Houston

MAJOR LEASE TRANSACTIONS DOWNTOWN HOUSTON This is a comprehensive list of publicly available leases in Downtown Houston, including new-to-Downtown, expansions and renewals. Year Company Type To From Square Feet 512,845 Enterprise Plaza 2020 Enterprise Products Partners Renewal (incl. 2019 (1100 Louisiana) expansion: 22,301) 2020 Summit Midstream Partners, LP New to Downtown/Sublease 910 Louisiana The Woodlands 48,632 LyondellBasell Tower 2020 Mitsubishi International Corporation Renewal 45,838 (1221 McKinney) Pennzoil Place – North Tower 2020 Cheniere Energy Expansion 33,127 (700 Milam) Texas Tower Wells Fargo Plaza 2020 DLA Piper Relocation/Expansion 31,843 (845 Texas) (1000 Louisiana) (Expansion: 6,836) Bank of America Tower 2020 Waste Management Expansion 31,750 (800 Capitol) 2020 Chevron Expansion 1600 Smith 23,699 Three Allen Center 2020 Plains All American Refining, L.P. Expansion 23,172 (333 Clay) Two Houston Center 2020 Office of the Comptroller of the Currency New to Downtown 14,624 (909 Fannin) One Allen Center 2020 Phelps Dunbar LLP Relocation 910 Louisiana 11,885 (500 Dallas) Esperson Building 2020 Set Solutions, Inc. New to Downtown 1800 West Loop South 11,480 (808 Travis) Relocation/Expansion in same Esperson Building 2020 Kirby, Mathews & Walrath, P.L.L.C. 10,511 building (808 Travis) Source: Central Houston, Inc. Updated 04-30-2020. 1 Year Company Type To From Square Feet 2020 Korn Ferry International Relocation in same building 700 Louisiana 8,130 LyondellBassell Tower 2020 NGP Energy Capital Relocation/Expansion 717 -

TC ENERGY CENTER 700 Louisiana St, Houston, TX 77002 “PLUG & PLAY” SUBLEASE 13,501 RSF - SUITE 2400

TC ENERGY CENTER 700 Louisiana St, Houston, TX 77002 “PLUG & PLAY” SUBLEASE 13,501 RSF - SUITE 2400 SPACE HIGHLIGHTS 46 Workstations 19 Private offices 3 Conference rooms (1 Board room) Elevator lobby exposure 1 Internal server room with storage/filing BUILDING NOTES Tunnel connected Gold LEED Certification Ample parking in Alley Theatre garage 24/7 security Lobby renovations planned PREMISES RENTAL RATE 13,501 RSF $16.00 NNN TERM OPEX Through 8/31/2025 $17.31 DAVID G. GUION Executive Managing Director +1 713 963 2810 [email protected] JOE RAMBIN Director +1 713 963 2877 [email protected] Copyright © 2015 Cushman & Wakefield. All rights reserved. Publication date mm.dd.yy cushmanwakefield.com TC ENERGY CENTER 700 Louisiana St, Houston, TX 77002 FOR SUBLEASE 13,501 RSF - SUITE 2400 FLOOR PLAN cushmanwakefield.com ©2020 Cushman & Wakefield. All rights reserved. The information contained in this communication is strictly confidential. This information has been obtained from sources believed to be reliable but has not been verified. No warranty or representation, express or implied, is made as to the condition of the property (or properties) referenced herein or as to the accuracy or completeness of the information contained herein, and same is submitted subject to Copyrighterrors, omissions, © change 2015 of Cushman price, rental or& other Wakefield. conditions, Allwithdrawal rights without reserved. notice, and Publication to any special listingdate conditions mm.dd.yy imposed by the property owner(s). Any projections, opinions or estimates are subject to uncertainty and do not signify current or future property performance. TC ENERGY CENTER 700 Louisiana St, Houston, TX 77002 FOR SUBLEASE 13,501 RSF - SUITE 2400 PROPERTY PHOTOS DAVID G. -

Houston Office Market Report Fourth Quarter 2020

HOUSTON OFFICE MARKET REPORT FOURTH QUARTER 2020 TABLE OF CONTENTS FOR MORE INFORMATION ECONOMIC OVERVIEW ...........................................2 WADE BOWLIN President, Property Services OFFICE MARKET ASSESSMENT .............................3 Central Division 713.209.5753 NET ABSORPTION & VACANCY ................................4 [email protected] RENTAL RATES & LEASING ACTIVITY ......................5 CONSTRUCTION .....................................................6 ARIEL GUERRERO Senior Vice President, Research SUBMARKET STATISTICS & RECENT DEALS ...........7 713.209.5704 THE TEAM ...............................................................8 [email protected] 4 Q2020 HOUSTON OFFICE MARKET ECONOMIC OVERVIEW Even though many of the challenges and uncertainties that defined 2020 are still with us, we start 2021 with cautious optimism because in December, the U.S. Food and Drug Administration issued emergency use authorization for two different vaccines for the prevention of COVID-19. As a greater share of the population is vaccinated, the robustness and pace of the economic recovery will follow as we return to public spaces like offices and restaurants in greater numbers. There is also hope in broader macroeconomic trends. During the pandemic, Americans trimmed back spending on discretionary purchases with the personal savings rate peaking in April at 33.7% and now 12.9% in November, well above the rate of 7.5% in 2019. This means many households have reserves to boost their spending once they have confidence the pandemic is over. This coupled with a low interest rate environment and the recent passage of the $900 billion pandemic relief package, mean the economy is poised for a sharp and sustained rebound. Looking at Houston in particular, we still have a long road to a full recovery. Using seasonally adjusted data, Houston is down 184.1 thousand jobs from February through November. -

Office Market

Q4 2020 | HOUSTON OFFICE MARKET Office Market Sees Continued Fallout Through Year’s End Pandemic, Oil Collapse Lead to Worst Year on Record for Market OVERVIEW ANNUAL TRENDLINES 2020 the Year of the Pandemic The Houston metro office market saw its most challenging year on record as the 5-YEAR TREND global pandemic and collapse in the energy sector led to negative absorption of JOB GROWTH 6.4 million SF over the year. Despite an uptick in leasing activity at year’s end, the fourth quarter saw negative absorption of 1.0 million SF. Impacts to the market -5.0k jobs were felt beyond negative absorption, as sublease supply increased by 934k Year-over-Year Office Employment* SF over the fourth quarter, ending the year at 6.8 million SF available across the metro. The uptick in sublease supply was fueled by the energy sector as Schlum- berger listed over 400k SF across multiple locations, while Maverick Natural ABSORPTION Absorption Resources, TechnipFMC, and McDermott all added sublease listings with term (1.0M) sf in high quality product. With absorption in the red and an increase in sublease 2020 Q4 absorption supply, both vacancy and availability saw upticks, ending the year at new highs of for all classes of space 19.5% and 25.8%, respectively. The market continues to be reshaped by the pandemic and outlook of economic DIRECT VACANCY uncertainty over the near term. As such, leasing activity has been heavily weighted Direct Vacant Available % to short term renewals and blend and extend activity. New leasing has seen much 19.4 Increased 40 bps more of a focus on value over the lure of new construction that dominated the over the quarter decade. -

HOUSTON OFFICE | Q1 2021 QUARTERLY MARKET REPORT Office Market Anxiously Awaiting Much Needed “Return to the Office”

HOUSTON OFFICE | Q1 2021 QUARTERLY MARKET REPORT Office Market anxiously awaiting much needed “return to the office” APRIL 2021 SUPPLY & DEMAND EXECUTIVE SUMMARY Net Absorption Deliveries Vacancy 5 28% VACANCY RATE AT 23.8% 4 24% The overall vacancy rate in the Houston office market was up 30 basis points Millions (SF) quarter-over-quarter, and up 230 basis 3 20% points year-over-year. The vacancy rate for Class A properties is at 26.2%, and 2 16% Class B at 22.1%. In the first quarter, overall net absorption totaled negative 1 12% 798,000 sq. ft.—Class A represented negative 494,000 sq. ft. of that tally, while 0 8% Class B registered negative 229,000 sq. ft. Of the 4.1 million sq. ft. currently under -1 4% construction, 45.6% of that space has been spoken for. Of the two properties -2 0% completed so far in 2021, totaling 105,400 Q1 Q1 Q1 Q1 Q1 Q1 Q1 Q1 Q1 Q1 Q1 sq. ft., 66,130 sq. ft. of that space has 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 been leased. The overall Houston average asking full-service rent is at $29.29 per sq. ft.—basically unchanged from one MARKET INDICATORS year ago at $29.28 per sq. ft.—while Class A space in the Central Business District is averaging $41.72 per sq. ft. CURRENT PRIOR QUARTER PRIOR YEAR Q1 2021 Q4 2020 Q1 2020 HOUSTON ECONOMIC INDICATORS Vacant Total 23.8% 23.5% 21.5% Houston ended 2020 behind the nation in its comeback from the COVID-19- Vacant Direct 22.5% 22.3% 20.4% driven job collapse.