For More Information, Please See the Nigeria Food Security Outlook For

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nigeria's Constitution of 1999

PDF generated: 26 Aug 2021, 16:42 constituteproject.org Nigeria's Constitution of 1999 This complete constitution has been generated from excerpts of texts from the repository of the Comparative Constitutions Project, and distributed on constituteproject.org. constituteproject.org PDF generated: 26 Aug 2021, 16:42 Table of contents Preamble . 5 Chapter I: General Provisions . 5 Part I: Federal Republic of Nigeria . 5 Part II: Powers of the Federal Republic of Nigeria . 6 Chapter II: Fundamental Objectives and Directive Principles of State Policy . 13 Chapter III: Citizenship . 17 Chapter IV: Fundamental Rights . 20 Chapter V: The Legislature . 28 Part I: National Assembly . 28 A. Composition and Staff of National Assembly . 28 B. Procedure for Summoning and Dissolution of National Assembly . 29 C. Qualifications for Membership of National Assembly and Right of Attendance . 32 D. Elections to National Assembly . 35 E. Powers and Control over Public Funds . 36 Part II: House of Assembly of a State . 40 A. Composition and Staff of House of Assembly . 40 B. Procedure for Summoning and Dissolution of House of Assembly . 41 C. Qualification for Membership of House of Assembly and Right of Attendance . 43 D. Elections to a House of Assembly . 45 E. Powers and Control over Public Funds . 47 Chapter VI: The Executive . 50 Part I: Federal Executive . 50 A. The President of the Federation . 50 B. Establishment of Certain Federal Executive Bodies . 58 C. Public Revenue . 61 D. The Public Service of the Federation . 63 Part II: State Executive . 65 A. Governor of a State . 65 B. Establishment of Certain State Executive Bodies . -

Community Forum Sustainability Review

Community Forum Sustainability Review November 2012 This publication was produced for review by the United States Agency for International Development. It was prepared by RTI International. Nigeria Northern Education Initiative (NEI) Community Forum Sustainability Review Contract #: EDH-I-00-05-00026-00 Sub-Contract #: 778-04 RTI Prepared for: USAID/Nigeria Prepared by RTI International 3040 Cornwallis Road Post Office Box 12194 Research Triangle Park, NC 27709-2194 The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government. 2 COMMUNITY FORUM SUST AIN ABILITY Table of Contents Introduction ........................................................................................................................................ 5 Survey Design and Implementation .................................................................................................... 5 Survey Findings ................................................................................................................................... 6 Understanding of the Forum process ............................................................................................. 6 Activity Funding .............................................................................................................................. 7 Roles and Responsibilities ............................................................................................................... 7 Forum -

Soil Survey Papers No. 5

Soil Survey Papers No. 5 ANCIENTDUNE FIELDS AND FLUVIATILE DEPOSITS IN THE RIMA-SOKOTO RIVER BASIN (N.W. NIGERIA) W. G. Sombroek and I. S. Zonneveld Netherlands Soil Survey Institute, Wageningen A/Gr /3TI.O' SOIL SURVEY PAPERS No. 5 ANCIENT DUNE FIELDS AND FLUVIATILE DEPOSITS IN THE RIMA-SOKOTO RIVER BASIN (N.W. NIGERIA) Geomorphologie phenomena in relation to Quaternary changes in climate at the southern edge of the Sahara W. G. Sombroek and I. S. Zonneveld Scanned from original by ISRIC - World Soil Information, as ICSU ! World Data Centre for Soils. The purpose is to make a safe depository for endangered documents and to make the accrued ! information available for consultation, following Fair Use ' Guidelines. Every effort is taken to respect Copyright of the materials within the archives where the identification of the j Copyright holder is clear and, where feasible, to contact the i originators. For questions please contact soil.isricOwur.nl \ indicating the item reference number concerned. ! J SOIL SURVEY INSTITUTE, WAGENINGEN, THE NETHERLANDS — 1971 3TV9 Dr. I. S. Zonneveld was chief of the soils and land evaluation section of the Sokoto valley project and is at present Ass. Professor in Ecology at the International Institute for Aerial Survey and Earth Science (ITC) at Enschede, The Netherlands (P.O. Box 6, Enschede). Dr. W. G. Sombroek was a member of the same soils and evaluation section and is at present Project Manager of the Kenya Soil Survey Project, which is being supported by the Dutch Directorate for International Technical Assistance (P.O. Box 30028, Nairobi). The opinions and conclusions expressed in this publication are the authors' own personal views, and may not be taken as reflecting the official opinion or policies of either the Nigerian Authorities or the Food and Agriculture Organization of the United Nations. -

Poverty in the North-Western Part of Nigeria 1976-2010 Myth Or Reality ©2019 Kware 385

Sociology International Journal Review Article Open Access Poverty in the north-western part of Nigeria 1976- 2010 myth or reality Abstract Volume 3 Issue 5 - 2019 Every society was and is still affected by the phenomenon of poverty depending on the Aliyu A Kware nature and magnitude of the scourge. Poverty was there during the time of Jesus Christ. Department of History, Usmanu Danfodiyo University, Nigeria Indeed poverty has been an issue since time immemorial, but it has become unbearable in recent decades particularly in Nigeria. It has caused a number of misfortunes in the country Correspondence: Aliyu A Kware, Department of History, including corruption, insecurity and general underdevelopment. Poverty has always been Usmanu Danfodiyo University, Sokoto, Nigeria, Tel 0803 636 seen as negative, retrogressive, natural, artificial, man-made, self-imposed, etc. It is just 8434, Email some years back that the Federal Office of Statistics (FOS, NBS) has reported that Sokoto State was the poorest State in Nigeria, a statement that attracted serious heat back from Received: August 14, 2019 | Published: October 15, 2019 the Government of the State. The Government debunked the claim, saying that the report lacked merit and that it was politically motivated. In this paper, the author has used his own research materials to show the causes of poverty in the States of the North-western part of Nigeria during the period 1976 to 2010, and as well highlight the areas in the States, which have high incidences of poverty and those with low cases, and why in each case. Introduction However, a common feature of the concepts that relate to poverty is income, but that, the current development efforts at poverty North-western part of Nigeria, in this paper, refers to a balkanized reduction emphasize the need to identify the basic necessities of life part of the defunct Sokoto Caliphate. -

Awareness and Perceptions of Desertification in Dange/Shuni Local

The Pharma Innovation Journal 2019; 8(7): 196-203 ISSN (E): 2277- 7695 ISSN (P): 2349-8242 NAAS Rating: 5.03 Awareness and perceptions of desertification in TPI 2019; 8(7): 196-203 © 2019 TPI Dange/Shuni local government area Sokoto state Nigeria www.thepharmajournal.com Received: 16-05-2019 Accepted: 17-06-2019 Maishanu HM, Mainasara MM, Dahiru SS and Shuni IA Maishanu HM Department of Biological Abstract Sciences, Faculty of Science, This research project was conducted to assess the level of awareness and human perspectives regarding Usmanu Danfodiyo University desertification in Dange –shuni local government area of Sokoto state, Nigeria. The study was Sokoto, Nigeria undertaking by the use of structured questionnaire and personal communication (interview) on desertification. Analyses of data showed individual response on desertification with different opinion in Mainasara MM the study area. Base on the results, it was recommended that, intensive mass campaigned on tree planting Department of Biological to avoid desertification and to determine the deterioration of the physical, chemical and biological or Sciences, Faculty of Science, economic properties of the soil. Effective prevention of desertification requires both local management Usmanu Danfodiyo University and micro policy approaches that promote sustainability of ecosystem services. It is advisable to focus on Sokoto, Nigeria prevention, because attempts to rehabilitate desertification areas are costly and tend to deliver limited Dahiru SS results. Zamfara State College of -

Independent National Electoral Commission (INEC)

FEDERAL REPUBLIC OF NIGERIA Independent National Electoral Commission (INEC) SOKOTO STATE DIRECTORY OF POLLING UNITS Revised January 2015 DISCLAIMER The contents of this Directory should not be referred to as a legal or administrative document for the purpose of administrative boundary or political claims. Any error of omission or inclusion found should be brought to the attention of the Independent National Electoral Commission. INEC Nigeria Directory of Polling Units Revised January 2015 Page i Table of Contents Pages Disclaimer................................................................................... i Table of Contents ………………………………………………..... ii Foreword.................................................................................... iii Acknowledgement...................................................................... iv Summary of Polling Units........................................................... 1 LOCAL GOVERNMENT AREAS Binji.................................................................................... 2-6 Bodinga............................................................................. 7-13 Dange/Shuni...................................................................... 14-20 Gada.................................................................................. 21-30 Goronyo............................................................................. 31-36 Gudu.................................................................................. 37-40 Gwadabawa...................................................................... -

Trends in Cross-Border Mobility of Pastoralists and Its Implications on the Farmer-Herder Conflicts

TRENDS IN CROSS-BORDER MOBILITY OF PASTORALISTS AND ITS IMPLICATIONS ON THE FARMER-HERDER CONFLICTS Odunaiya Samson Kebbi State University of Science and Technology Aliero 1 EXECUTIVE SUMMARY Communities in Sokoto have experienced violence between farmers and pastoralists. The latter are divided into sedentary pastoralists, who are Nigerians and mostly herd in communities in Sokoto, and migratory pastoralists, who are transhumant herders migrating into Nigeria through the Sokoto-Niger Republic border in Tangaza local government area and other bordering communities. The destinations of migratory pastoralists in Nigeria have remained the same to this very day; however, there has been a change in the routes and migratory patterns. The alteration of the historical migratory trends and patterns can be attributed to encroachment of grazing routes by farmers, which have caused pastoralists to neglect grazing and seek alternative routes. Hence, roads and farmlands are used for passage. In addition, security challenges in Zamfara state, cattle rustling, superstitious traditional beliefs, unlawful allocation of grazing reserves by politicians for farming, and nighttime herding are other factors that have caused the change in migration patterns. The population of pastoralists migrating into Nigeria has increased significantly when compared to that of the past. This can be attributed to the increase in the population of pastoralists and livestock, and desertification in the Sahel which is forcing more pastoralists into Nigeria. Though the relationship between migratory pastoralists and farmers has been hostile in nature, the same cannot be said of the relationship between sedentary and migratory pastoralists, which has been peaceful and mutual. The continuous dispute caused by changes in migratory trends have tended to spark cycles of reprisal attacks and can cause regional tensions with the bordering country of Niger Republic. -

Determined Action Brings Real Change to Sokoto

#SokotoState Our World Friday, October 31, 2014 SOKOTO STATE REPUBLIC OF NIGerIA This supplement to USA TODAY was produced by United World Ltd., Suite 179, 34 Buckingham Palace Road, London SW1W 0RH – Tel: +44 (0)20 7305 5678 – [email protected] – www.unitedworld-usa.com Determined action brings real change to Sokoto Major changes introduced by the local government of Nigeria’s northwestern Sokoto State are enhancing life and employment opportunities for citizens and readying it for international investment oreign investment in institutions, such as Goldman “Nigeria is very unique we will soon be able to com- boost all sectors of society and Africa is set to reach Sachs and The Carlyle Group, with a lot of potential in agro- pete across the world.” the economy. DID YOU KNOW? its highest levels this and multinationals, including industry and minerals, and Dr. Wamakko is heading the The state’s capital, Sokoto Facts about Sokoto year since the 2008- Nestlé and Unilever, are at- it has the right quality and transformation that is sweep- City, is the seat of the former 09 global financial tracted to Africa’s strong eco- quantity of human resources. ing through his home region. Sokoto Caliphate – an empire LOCATION crisis, and the African Devel- nomic growth and improved The potential of the economy Located at the northwestern that grew during the 1800s to In the northwestern corner Fopment Bank, the UN and the governance. Singapore’s sov- is vast and diverse,” says Al- tip of the country, Sokoto State become one of largest and most of Nigeria, sharing OECD are all painting a rosy ereign wealth fund Temasek, haji (Dr.) Aliyu Magatakarda is reaping the benefits of elec- economically successful in pre- borders with the Republic outlook for the continent. -

Violence in Nigeria : a Qualitative and Quantitative Analysis

Marc-Antoine Pérouse de Montclos (ed.) West African Politics and Society series 3 Violence in Nigeria Violence in Nigeria Violence in Nigeria Most of the academic literature on violence in Nigeria is qualitative. It rarely relies on quantitative data because police crime statistics are not reliable, or not available, or not even published. Moreover, the training of A qualitative and Nigerian social scientists often focuses on qualitative, cultural, and political issues. There is thus quantitative analysis a need to bridge the qualitative and quantitative approaches of conflict studies. This book represents an innovation and fills a gap in this regard. It is the first to introduce a discussion on such issues in a coherent manner, relying on a database that fills the lacunae in A qualitative and quantitative data from the security forces. The authors underline the necessity of a trend analysis to decipher the patterns and the complexity of violence in very different fields: from oil production to cattle breeding, radical Islam to motor accidents, land conflicts to witchcraft, and so on. In addition, analysis they argue for empirical investigation and a complementary approach using both qualitative and quantitative data. The book is therefore organized into two parts, with a focus first on statistical Marc-Antoine studies, then on fieldwork. Pérouse de Montclos (ed.) Marc-Antoine Pérouse de Montclos (ed.) 3 www.ascleiden.nl 3 African Studies Centre Violence in Nigeria: “A qualitative and quantitative analysis” 501890-L-bw-ASC 501890-L-bw-ASC African Studies Centre (ASC) Institut Français de Recherche en Afrique (IFRA) West African Politics and Society Series, Vol. -

Accepted: 15Th May, 2021

UJMR, Volume 6 Number 1, June, 2021, pp 99 - 104 ISSN: 2616 - 0668 https://doi.org/10.47430/ujmr.2161 .013 Received: 19th April, 2021 Accepted: 15th May, 2021 Prevalence of Urinary Schistosomiasis among Almajiri Children in Silame, Sokoto State, North-western Nigeria 1Gamde, S.M. , 2Tongvwam, P.J., 1Hauwa, K., 3Ganau, A.M.,4Abdulahi,J.A.,5Gamde, D.S., and 6Pwajok, C.T.P 1Department of Medical Laboratory Services, Hospital Services Management Board, Sokoto State, Nigeria. 2Department of Medical Laboratory Science, Faculty of Health Sciences and Technology, University of Jos, Plateau State, Nigeria. 3Departments of Microbiology, School of Medical Laboratory Sciences, UsmanuDanfodiyo University, Sokoto State, Nigeria. 4Department of Chemical Pathology, School of Medical Laboratory Sciences, UsmanuDanfodiyo University, Sokoto State, Nigeria. 5Department of Microbiology, Faculty of Natural Sciences, AbubakarTafawaBalewa University, Bauchi State, Nigeria. 6National Veterinary Research Institute, Jos, Plateau State, Nigeria. Corresponding author:[email protected],08131943803 Abstract Urinary schistosomiasis is a severe threat to global health with uncountable morbidities in Africa including Nigeria where control interventions focused on children in public and private schools neglecting Almajiri children. This undermined control interventions as those infected contaminate the environments with infective stages of the parasite. The objective of the study was to identify the prevalence ofurinary schistosomiasis amongst Almajiri children in Silame, Sokoto State, North- westernNigeria. This was a cross-sectional descriptive study, socio-demographic data was collected in April 2020 on 206 consented Almajiri children in Silame and their urine samples were examined using the sedimentation method. The study showed a prevalence of 35.4% among the Almajiri children in Silame, Sokoto State, North-western Nigeria. -

A Survey of Common Toxic Plants of Livestock in Sokoto State, Nigeria

Scientific Research and Essay Vol. 2(2), pp. 040-042, February 2007 Available online at http://www.academicjournals.org/SRE ISSN 1992-2248 © 2007 Academic Journals Short Communication A survey of common toxic plants of livestock in Sokoto State, Nigeria B. M. Agaie, A. Salisu and A. A. Ebbo* Department of Physiology and Pharmacology, Faculty of Veterinary Medicine, Usmanu Danfodiyo University, Sokoto, P.M.B 2346, Nigeria. Accepted 19 December, 2006 Through structured questionnaire, two hundred livestock farmers and veterinary attendants were interviewed on various aspects of poisonous plants in Sokoto State. Forty one (41) poisonous plants were reported to exist in the state. They include Ipomea asarifolia (Duman kada), Sorgum bicolar (Bahuri), Erythrophleum africana (Samberu), Calotropis procera (Tumfafiya) and Mannihot esculenta (Kunnen rogo). Majority of the plants are found in the grassland and are shrubs. Leaves stem and bark are the major parts of the plants that are poisonous when consumed by livestock. Key words: Toxic plants, Livestock, Sokoto, Nigeria. INTRODUCTION Plants comprise the third largest category of poisons systems of management making them susceptible to poi- known around the world. They form a major part of soning by toxic plants. With increasing human activities livestock feed, thus toxicosis in animals consuming these such as construction, farming, deforestation and other plants can be expected. It is also known that poisonous forms of environmental degradation, which affects the plants constitute a major cause of economic loss in fauna and the flora, it becomes very important to re- livestock industry since the days of early settlement assess common poisonous plants found in the state. -

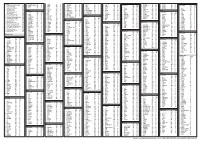

States and Lcdas Codes.Cdr

PFA CODES 28 UKANEFUN KPK AK 6 CHIBOK CBK BO 8 ETSAKO-EAST AGD ED 20 ONUIMO KWE IM 32 RIMIN-GADO RMG KN KWARA 9 IJEBU-NORTH JGB OG 30 OYO-EAST YYY OY YOBE 1 Stanbic IBTC Pension Managers Limited 0021 29 URU OFFONG ORUKO UFG AK 7 DAMBOA DAM BO 9 ETSAKO-WEST AUC ED 21 ORLU RLU IM 33 ROGO RGG KN S/N LGA NAME LGA STATE 10 IJEBU-NORTH-EAST JNE OG 31 SAKI-EAST GMD OY S/N LGA NAME LGA STATE 2 Premium Pension Limited 0022 30 URUAN DUU AK 8 DIKWA DKW BO 10 IGUEBEN GUE ED 22 ORSU AWT IM 34 SHANONO SNN KN CODE CODE 11 IJEBU-ODE JBD OG 32 SAKI-WEST SHK OY CODE CODE 3 Leadway Pensure PFA Limited 0023 31 UYO UYY AK 9 GUBIO GUB BO 11 IKPOBA-OKHA DGE ED 23 ORU-EAST MMA IM 35 SUMAILA SML KN 1 ASA AFN KW 12 IKENNE KNN OG 33 SURULERE RSD OY 1 BADE GSH YB 4 Sigma Pensions Limited 0024 10 GUZAMALA GZM BO 12 OREDO BEN ED 24 ORU-WEST NGB IM 36 TAKAI TAK KN 2 BARUTEN KSB KW 13 IMEKO-AFON MEK OG 2 BOSARI DPH YB 5 Pensions Alliance Limited 0025 ANAMBRA 11 GWOZA GZA BO 13 ORHIONMWON ABD ED 25 OWERRI-MUNICIPAL WER IM 37 TARAUNI TRN KN 3 EDU LAF KW 14 IPOKIA PKA OG PLATEAU 3 DAMATURU DTR YB 6 ARM Pension Managers Limited 0026 S/N LGA NAME LGA STATE 12 HAWUL HWL BO 14 OVIA-NORTH-EAST AKA ED 26 26 OWERRI-NORTH RRT IM 38 TOFA TEA KN 4 EKITI ARP KW 15 OBAFEMI OWODE WDE OG S/N LGA NAME LGA STATE 4 FIKA FKA YB 7 Trustfund Pensions Plc 0028 CODE CODE 13 JERE JRE BO 15 OVIA-SOUTH-WEST GBZ ED 27 27 OWERRI-WEST UMG IM 39 TSANYAWA TYW KN 5 IFELODUN SHA KW 16 ODEDAH DED OG CODE CODE 5 FUNE FUN YB 8 First Guarantee Pension Limited 0029 1 AGUATA AGU AN 14 KAGA KGG BO 16 OWAN-EAST