PROSUS N.V. (Currently Named Myriad International

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of the Recognized Foreign Exchanges Relative to the Reporting Requirement (3Rd December 2007)

List of the recognized foreign exchanges relative to the reporting requirement (3rd December 2007) Art. 15 para. 2 SESTA determines that securities dealers must report all the infor- mation necessary to ensure a transparent market (reporting requirement). In Art. 2 following SESTO-SFBC the appropriate implementing regulations are determined. Exceptions of the reporting requirement are recorded in Art. 4 SESTO-SFBC. Art. 4 letter a SESTO-SFBC determines that the securities dealer shall not be obliged to report transactions abroad in foreign securities admitted for trading on a Swiss stock exchange, provided that they are conducted on a foreign stock exchange recognized by Switzerland. According to established practice relative to the release of the reporting require- ment, recognized exchanges are the exchanges that are united in the World Fed- eration of Exchanges and/or the Federation of European Stock Exchanges (FESE). All foreign exchanges that are authorized by the Swiss Federal Banking Commis- sion in accordance with Art. 14 SESTO are also recognized exchanges concerning this matter, even they are neither member of the World Federation of Exchanges nor of the FESE. As an exception to this rule, besides the Deutsche Börse AG (member of World Federation of Exchanges) also the remaining German (regional) exchanges are recognized in this context. Name Location AMERICAN STOCK EXCHANGE New York, USA AMMAN STOCK EXCHANGE Amman, JORDAN ATHENS EXCHANGE Athens, GREECE AUSTRALIAN STOCK EXCHANGE Sydney, AUSTRALIA BAYERISCHE BÖRSE Munich, GERMANY BERMUDA STOCK EXCHANGE Hamilton, BERMUDA BOLSA DE COMERCIO DE BUENOS AIRES Buenos Aires, ARGENTINA BOLSA DE COMERCIO DE SANTIAGO Santiago, CHILE BOLSA DE VALORES DE COLOMBIA Bogota, COLOMBIA BOLSA DE VALORES DE LIMA Lima, PERU BOLSA DE VALORES DO SAO PAULO Sao Paulo, BRAZIL Name Location BOLSA MEXICANA DE VALORES Mexico, MEXICO BOLSAS Y MERCADOS ESPANOLES Barcelona, Bilbao, Madrid, Valencia, SPAIN BOMBAY STOCK EXCHANGE LTD. -

South Africa and Namibia

SOUTH AFRICA AND NAMIBIA SOUTH AFRICA $881.61 Bn $200.29 Bn Equity Market Debt Market 372 125 136% 260% 59% Capitalization Capitalization Number of Number of Domestic Total Equity Debt Market listed issuers Equity Market Market Cap/ Cap/GDP companies (bonds) Cap/GDP GDP 91,716,796,484 $2,127.21 Bn Equity Market Share Volume Traded Debt Market Total Nominal Traded NAMIBIA $138.37 Bn* $2.72 Bn 17% 953%* 19% Equity Market Debt Market 44* 10 Domestic Total Equity Domestic Capitalization Capitalization Number of Number of Equity Market Market Cap/ Debt Market listed issuers Cap/GDP GDP Cap/GDP companies (bonds) 193,100,874 41,296,398 Equity Market Share Volume Traded Debt Market Instrument Volume Traded *Includes dual-listings and ETFs. CFA Institute Research Foundation | 1 SOUTH AFRICA AND NAMIBIA • 1881: Kimberley Royal 1880s Stock Exchange established • 1886: Gold discovered on the reef • 1895: Durban Roodepoort • 1887: Johannesburg Stock 1890s Deep listed on the JSE Exchange (JSE) established • 1897: South African Breweries (SAB) listed on the JSE • 1901: Cape Town stock exchange established 1900s • 1904: Namibian Stock Exchange (NSX) founded 1910s • 1910: NSX closed • 1947: Stock Exchanges 1940s Control Act was passed in SA • 1963: JSE joins World 1960s Federation of Exchanges • 1990: Namibian independence from South Africa • 1992: NSX established (second time); First • 2000: JSE moves to corporate bond (SAB) issued 1990s Sandton; First ETF listed on in South Africa the JSE • 1996: Open outcry trading • 2001: FTSE agreement with ceases -

Longleaf Partners International Fund Commentary 2Q21

July 2021 Longleaf Partners International Fund Commentary 2Q21 Longleaf Partners International Fund added 1.19% in the quarter and 8.00% year-to- date, trailing the MSCI EAFE Index’s 5.17% and 8.83% for the same periods. US markets continued the monetary liquidity fueled run to ever sillier valuation levels, while non-US lagged relatively. The majority of our holdings were positive in the quarter. The Fund’s exposure to China and Hong Kong (including Netherlands-listed Prosus, whose business is driven by the Chinese consumer) was the biggest geographic headwind. FX was a moderate contributor to the Fund, as well as the MSCI EAFE index. Despite relative underperformance, it was a solid period for value per share growth at our holdings. “Value” had a (we believe temporary) pullback vs. “growth” in the second quarter on the back of lower interest rates and various other factors. Over the last year, we have seen interest rate consensus go from “low rates forever” for most of 2020 to “rates are definitely going up” in February/March of 2021 to what now feels like magical goldilocks thinking for growth stocks in the 1-2% US 10-year range. While we cannot predict precisely what rates will do in the near term, we welcome increased volatility on this all- Average Annual Total Returns for the Longleaf Partners International Fund (6/30/21): Since Inception (10/26/98): 7.45%, Ten Year: 4.50%, Five Year: 10.64%, One Year: 34.82%. Average Annual Total Returns for the MSCI EAFE (6/30/21): Since Inception (10/26/98): 5.62%, Ten Year: 5.89%, Five Year: 10.28%, One Year: 32.35%. -

Ishares AEX UCITS ETF EUR (Dist)

iShares AEX UCITS ETF EUR (Dist) IAEX August Factsheet Performance, Portfolio Breakdowns and Net Assets information as at: 31-Aug- 2021 All other data as at 10-Sep-2021 For Investors in Austria. Investors should read the Key Investor Information Document and Capital at risk. All financial investments Prospectus prior to investing. involve an element of risk. Therefore, the value of your investment and the income from it will The Fund seeks to track the performance of an index composed of 25 of the largest Dutch vary and your initial investment amount cannot companies listed on NYSE Euronext Amsterdam. be guaranteed. KEY FACTS KEY BENEFITS Asset Class Equity Fund Base Currency EUR Targeted exposure to the most traded Dutch stocks 1 Share Class Currency EUR 2 Direct investment into 25 companies, listed in the Netherlands Fund Launch Date 18-Nov-2005 Share Class Launch Date 18-Nov-2005 3 Single country exposure Benchmark AEX-Index ISIN IE00B0M62Y33 Key Risks: Investment risk is concentrated in specific sectors, countries, currencies or companies. Total Expense Ratio 0.30% Distribution Type Quarterly This means the Fund is more sensitive to any localised economic, market, political or regulatory Domicile Ireland events. The value of equities and equity-related securities can be affected by daily stock market Methodology Replicated movements. Other influential factors include political, economic news, company earnings and Product Structure Physical significant corporate events. Counterparty Risk: The insolvency of any institutions providing Rebalance Frequency Annual services such as safekeeping of assets or acting as counterparty to derivatives or other UCITS Yes instruments, may expose the Fund to financial loss. -

PROSUS N.V. (Previously Myriad International Holdings N.V) (Incorporated in the Netherlands) (Legal Entity Identifier: 635400Z5L

PROSUS N.V. (previously Myriad International Holdings N.V) (Incorporated in the Netherlands) (Legal Entity Identifier: 635400Z5LQ5F9OLVT688) ISIN: NL0013654783 Euronext Amsterdam and JSE Share code: PRX ("Prosus" or the "Company") RESULTS OF ANNUAL GENERAL MEETING Amsterdam, 18 August 2020 – Prosus N.V. (Prosus) (AEX and JSE: PRX) The annual general meeting (AGM) of Prosus N.V. was held through electronic communication today. Shareholders are advised that all resolutions set out in the notice of the AGM were passed by the requisite majority of shareholders represented at the annual general meeting and adopted. We note that the issued share capital of Prosus is as follows: Number of Nominal value Issued Authorised Class of share votes per share share capital share capital per share Ordinary Share N EUR0.05 1 1 624 652 070 5 000 000 000 (N shares) Ordinary Share A1 EUR0.05 1 3 511 818 10 000 000 (A shares) The number of ordinary shares that could have been voted at the meeting: 1 628 163 888. The total number of ordinary shares voted at the meeting was: 1,518,995,600 which is 93.3% of the total issued share capital. Details of voting results1: NO. AGENDA ITEM VOTES % VOTES % VOTES VOTES % of FOR AGAINST ABSTAIN TOTAL ISSUED SHARE CAPITAL VOTED 2 To approve the directors’ remuneration report 1,281,624,109 84.75 230,641,199 15.25 6,730,292 1,518,995,600 93.30% 3 To adopt the annual accounts 1,518,139,247 100.00 27,759 0.00 828,594 1,518,995,600 93.30% Proposal to make a distribution (including reduction of Prosus’s 4(a) issued capital and -

Esg Disclosure in Comparative Perspective: Optimizing Private Ordering in Public Reporting

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Penn Law: Legal Scholarship Repository ESG DISCLOSURE IN COMPARATIVE PERSPECTIVE: OPTIMIZING PRIVATE ORDERING IN PUBLIC REPORTING VIRGINIA HARPER HO* & STEPHEN KIM PARK** ABSTRACT Demand for corporate non-financial “environmental, social, and governance” (ESG) information from investors and governments is on the rise globally, and leading securities regulators and stock exchanges worldwide now encourage or mandate its disclosure by large firms. However, rising demand has been matched by growing dissatisfaction with ESG informational gaps in financial reports, on the one hand, and the dearth of investment-grade information in corporate sustainability reports and other public sources, on the other. These developments raise questions about whether the Securities and Exchange Commission (SEC) and its counterparts in other jurisdictions should continue to defer primarily to private market-based approaches to ESG disclosure, reform the disclosure framework to expressly address non-financial information, or seek to combine elements of both public disclosure regulation and private ordering in new ways. This Article anticipates these policy choices by assessing the range of approaches to ESG disclosure that have been adopted in the United States and six other influential jurisdictions: South Africa, Brazil, the European Union, the United Kingdom, Hong Kong, and * Professor of Law and Associate Dean for International & Comparative Law, University of Kansas School of Law. ** Associate Professor of Business Law and Satell Fellow in Corporate Social Responsibility, University of Connecticut. Prior versions of this Article were presented at the National Business Law Scholars Conference, the American Society of Comparative Law Workshop on Comparative Business and Financial Law at Fordham Law School, and the Notre Dame Law School Faculty Colloquium. -

R&Co Risk-Based International Index – Weighting

Rothschild & Co Risk-Based International Index Indicative Index Weight Data as of June 30, 2021 on close Constituent Exchange Country Index Weight(%) Jardine Matheson Holdings Ltd Singapore 1.46 LEG Immobilien SE Germany 0.98 Ajinomoto Co Inc Japan 0.95 SoftBank Corp Japan 0.89 Shimano Inc Japan 0.85 FUJIFILM Holdings Corp Japan 0.73 Singapore Exchange Ltd Singapore 0.72 Japan Tobacco Inc Japan 0.72 Cellnex Telecom SA Spain 0.69 Nintendo Co Ltd Japan 0.69 Carrefour SA France 0.67 Nexon Co Ltd Japan 0.66 Deutsche Wohnen SE Germany 0.65 Bank of China Ltd Hong Kong 0.64 REN - Redes Energeticas Nacion Portugal 0.63 Pan Pacific International Hold Japan 0.63 Japan Post Holdings Co Ltd Japan 0.62 Nippon Telegraph & Telephone C Japan 0.61 Roche Holding AG Switzerland 0.61 Nestle SA Switzerland 0.61 Novo Nordisk A/S Denmark 0.59 ENEOS Holdings Inc Japan 0.59 Nomura Research Institute Ltd Japan 0.59 Koninklijke Ahold Delhaize NV Netherlands 0.59 Jeronimo Martins SGPS SA Portugal 0.58 HelloFresh SE Germany 0.58 Toshiba Corp Japan 0.58 Hoya Corp Japan 0.58 Siemens Healthineers AG Germany 0.58 MS&AD Insurance Group Holdings Japan 0.57 Coloplast A/S Denmark 0.57 Kerry Group PLC Ireland 0.57 Scout24 AG Germany 0.57 SG Holdings Co Ltd Japan 0.56 Symrise AG Germany 0.56 Nitori Holdings Co Ltd Japan 0.56 Beiersdorf AG Germany 0.55 Mitsubishi Corp Japan 0.55 KDDI Corp Japan 0.55 Sysmex Corp Japan 0.55 Chr Hansen Holding A/S Denmark 0.55 Ping An Insurance Group Co of Hong Kong 0.55 Eisai Co Ltd Japan 0.54 Chocoladefabriken Lindt & Spru Switzerland 0.54 Givaudan -

Cambiar Europe Select Adr Commentary 2Q 2021 Market Review

CAMBIAR EUROPE SELECT ADR COMMENTARY 2Q 2021 MARKET REVIEW European equities continued their positive momentum recovery relative to the U.S. Cambiar’s constructive in the second quarter, with the MSCI Europe Index outlook for Europe is a function of reasonable valuations posting a gain of 7.4%. Although the region is trailing (average P/E in Europe is 3-4 multiple turns below the U.S. as it relates to vaccination progress and the S&P 500) and the region’s high leverage to the corresponding reopening timelines, the global revenue more traditional value industries, which are poised to footprint for many EU companies is providing sufficient demonstrate a meaningful earnings acceleration over a visibility for investors to bid up the space in anticipation forward 1–2 year timeframe. And although Europe/UK is of an ensuing earnings recovery. incurring a rise in prices, inflation readings remain well below levels that would warrant consideration in altering Given the asynchronized nature of the global rebound, the ECB’s accommodative posture. European markets are in the earlier innings of their EUROPE SELECT ADR CONTRIBUTORS DETRACTORS Top Five Avg. Weights Contribution Bottom Five Avg. Weights Contribution Deutsche Post 3.76 0.87 Siemens 3.76 -0.12 Entain 4.01 0.57 Enel 2.31 -0.15 Carlsberg 2.78 0.53 Aena SME 1.54 -0.21 ASML Holding 3.75 0.47 Koninklijke Philips 2.31 -0.26 Compagnie de Saint-Gobain 3.28 0.45 Prosus 3.51 -0.44 A complete description of Cambiar’s performance calculation methodology, including a complete list of each security that contributed to the performance of the Cambiar portfolio mentioned above is available upon request. -

Juin 2021 31 - 05 - 2021 Méthodologie

Guide Quantitatif Juin 2021 Cours arrêtés au 31-05-2021 Vincent COURTOIS Méthodologie Ce Stock-Guide se présente comme un modèle quantitatif conçu autour des données de la STOCK-GUIDE base Factset. Au total, il couvre 42 secteurs avec un maximum de 17 valeurs par secteur et combine des valeurs Big, Mid et Small Cap. Pour chaque secteur, une note est attribuée de 0 (la plus mauvaise note) à 5 (la plus forte), fonction de 5 critères : le momentum des BNA, la valorisation absolue et relative, les opinions « contrariennes » des analystes, la qualité des fondamentaux et la fiabilité historique des guidances. Notre opinion sectorielle est synthétisée par des flèches : vertes pour une opinion positive, oranges pour une opinion neutre et rouges pour une opinion négative. Valeurs par nationalité Valeurs par capitalisation Autres; 80; 14% 0-500M€; 49; 8% Fr.; 166; 30% 500M€-1000M€; 31; P-B; 19; 3% >10000M€; 270; 5% Belg.; 17; 3% 47% Esp.; 33; 6% It.; 35; 6% 1000M€-5000M€; 152; 26% U-K; 67; 12% US; 85; 15% 5000M€-10000M€; 79; All; 62; 11% 14% Avertissement : Entreprise d’investissement agréée par le CECEI le 25 juillet 1997 (Comité des Etablissements de Crédit et des Entreprises d’Investissement de la Banque de France) et par l’AMF (Autorité des Marchés Financiers), la FINANCIERE D’UZES est également membre d’Euronext. La FINANCIERE D’UZES relève des autorités compétentes que sont l’AMF et l’ACPR. Les informations contenues dans ce document ont été puisées aux meilleures sources mais ne sauraient entraîner notre responsabilité. Par ailleurs, La FINANCIERE D’UZES est organisée de manière à assurer l’indépendance de l’analyste ainsi que la gestion et la prévention des éventuels conflits d’intérêt. -

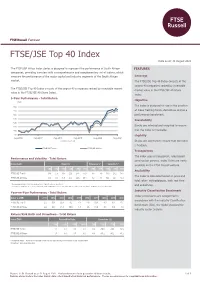

FTSE/JSE Top 40 Index

FTSE Russell Factsheet FTSE/JSE Top 40 Index Data as at: 31 August 2021 bmkTitle1 The FTSE/JSE Africa Index Series is designed to represent the performance of South African FEATURES companies, providing investors with a comprehensive and complementary set of indices, which measure the performance of the major capital and industry segments of the South African Coverage market. The FTSE/JSE Top 40 Index consists of the largest 40 companies ranked by investable The FTSE/JSE Top 40 Index consists of the largest 40 companies ranked by investable market market value in the FTSE/JSE All-Share value in the FTSE/JSE All-Share Index. Index. 5-Year Performance - Total Return Objective The index is designed for use in the creation of index tracking funds, derivatives and as a performance benchmark. Investability Stocks are selected and weighted to ensure that the index is investable. Liquidity Stocks are screened to ensure that the index is tradable. Transparency The index uses a transparent, rules-based Performance and Volatility - Total Return construction process. Index Rules are freely Index (ZAR) Return % Return pa %* Volatility %** available on the FTSE Russell website. 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR Availability FTSE/JSE Top 40 -0.6 2.5 14.5 22.6 27.8 53.0 8.5 8.9 17.3 23.2 15.5 The index is calculated based on price and FTSE/JSE All Share -0.1 4.0 15.9 25.2 26.6 49.1 8.2 8.3 16.4 22.5 15.2 total return methodologies, both real time * Compound annual returns measured over 3 and 5 years respectively and end-of-day. -

Monthly Index Key Facts

MONTHLY INDEX KEY FACTS Key Index Facts on 30/06/2021 EURONEXT INDICES AEX AMX BEL20 PX1 CACMD PSI20 ISE20 OBXP CESGP LC100 Low Carbon Financial Ratios AEX® AMX® BEL 20® CAC 40® CAC® Mid 60 PSI 20® ISEQ 20® OBX® CAC 40 ESG 100 Europe ® PAB Price/Earnings w Neg 31.16 482.97 - 72.23 49.16 12.91 114.11 0.84 68.02 27.72 Price/Book 10.56 4.88 2.71 4.56 3.00 2.14 3.09 3.98 3.74 5.70 Price/Cash Flow 62.98 9.65 8.56 19.23 10.51 8.75 18.02 2.33 17.07 15.55 Price/Sales 7.05 4.14 42.20 3.93 2.58 2.17 3.93 5.12 3.43 4.38 Dividend Yield 2.03% 1.78% 1.41% 2.10% 1.79% 3.54% 0.24% 2.51% 2.12% 2.20% Index Cap of Constituents (Millions) 0.0982 Largest € 135,770 € 4,393 € 16,426 € 183,588 € 5,208 € 1,419 € 24,745 € 20,398 € 113,331 € 134,618 Average € 30,814 € 2,076 € 6,363 € 37,487 € 2,082 € 592 € 6,179 € 5,014 € 28,559 € 26,036 Median € 19,858 € 1,934 € 4,038 € 25,053 € 1,654 € 558 € 870 € 3,510 € 19,805 € 15,296 Smallest € 4,365 € 813 € 1,444 € 5,078 € 61 € 38 € 203 € 348 € 4,562 € 4,489 Total index value € 770,345 € 51,893 € 127,252 € 1,499,466 € 124,929 € 10,650 € 123,582 € 125,355 € 1,142,372 € 2,603,601 Full Market Cap Of Constituents (Millions) Largest € 243,057 € 15,291 € 102,966 € 333,796 € 15,031 € 18,769 € 33,365 € 58,280 € 333,796 € 134,618 Average € 42,532 € 3,709 € 13,549 € 53,812 € 4,176 € 3,727 € 7,423 € 9,327 € 43,297 € 26,036 Median € 22,664 € 2,856 € 6,266 € 31,925 € 3,340 € 1,466 € 978 € 4,634 € 24,802 € 15,296 Smallest € 4,595 € 834 € 3,457 € 5,643 € 87 € 91 € 313 € 687 € 5,643 € 4,489 Total index value with full MC constituents € 1,063,309 -

Purple-Group-Annual-Report-2016

2Awards and Highlights 1 Purple Philosophy 2 Chairman’s Letter 4 Chief Executive Officer’s Letter 5 Chief Financial Officer’s Report 6 12Ethical Leadership 38Directors’ Responsibility 86 Notice of Annual General Meeting 86 and Corporate Citizenship 12 for Financial Reporting 38 Shareholder Rights 90 Summary Governance Results 19 Group Secretary’s Report 39 Brief Curriculum Vitae of Our People 20 Directors’ Report 40 Directors Standing for Re-election 90 Our Leadership Report of the Audit Committee 42 Form of Proxy 91 Executive Team Management Team 22 Report of the Independent Auditor 43 Notes to the Form of Proxy 92 Board Members 24 Consolidated Statement Corporate Information 93 of Profit or Loss 44 Your Thoughts Our Team 26 Consolidated Statement of 94 Other Comprehensive Income 45 Consolidated Statement of Financial Position 46 Consolidated Statement of Changes in Equity 47 Consolidated Statement 28 of Cash Flows 48 Navigate the Markets 28 Notes to the Consolidated Annual Our Brands – Emperor 30 Financial Statements 49 Our Brands – EasyEquities 32 Shareholder Analysis 85 Our Brands – GT247.com 34 Our Brands – GT Private Broking 36 INVESTING AND TRADING SOLUTIONS FOR EVERYONE First World Trader (FWT) t/a Emperor Asset Management Proprietary First World Trader Nominees Proprietary GT247.com Limited (EAM) Limited (FWTN) Non-discretionary Category I FAIS licence, Discretionary Category II FAIS licence, which Approved by the FSB to operate and hold which provides FWT the ability to conduct provides EAM the ability to conduct an clients’ assets in the name of the nominee. an intermediary and advisory service on intermediary investment management service STRATE approval to hold equity securities on derivatives, shares, money market, retail on derivatives, shares, money market and behalf of clients.