The Employment Structure in Epping Forest District

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Epping Forest District Council Epping Forest District Local Plan Employment Land Supply Assessment

Epping Forest District Council Epping Forest District Local Plan Employment Land Supply Assessment Issue | December 2017 This report takes into account the particular instructions and requirements of our client. It is not intended for and should not be relied upon by any third party and no responsibility is undertaken to any third party. Job number 248921-22 Ove Arup & Partners Ltd 13 Fitzroy Street London W1T 4BQ United Kingdom www.arup.com Epping Forest District Council Epping Forest District Local Plan Employment Land Supply Assessment Contents Page 1 Introduction 2 1.1 Purpose of the Report 2 1.2 Structure of the Report 4 2 Employment Sites Audit 5 2.1 Step 1: Collating Data Sources 5 2.2 Step 2: Filtering of Employment Sites 6 2.3 Step 3: Checking for Duplicate Employment Sites 7 2.4 Identifying Sites with Strategic Opportunities for Providing Employment Land 8 3 Findings of More Detailed Site Assessment 10 3.1 Overview of Methodology 10 3.2 Filtering of Employment Sites Following Site Visits 11 3.3 Overview of Land Supply for B Use Class Sites 18 3.4 Sites with Strategic Opportunities for Providing Employment Land 29 4 Summary and Implications for the Local Plan 32 4.1 Supply Assessment Summary 32 4.2 Implications for the Local Plan 33 Appendices Appendix A Employment Sites Audit Appendix B Methodology for Site Assessment Appendix C Site Proformas for Existing and Potential New Employment Sites Appendix D Employment Maps | Issue | December 2017 Epping Forest District Council Epping Forest District Local Plan Employment Land Supply Assessment 1 Introduction 1.1 Purpose of the Report The adopted Local Plan for the District is the Epping Forest District Local Plan (1998) and Alterations (2006). -

Epping Forest District Bishops Hall Lambourne Tq

EPPING FOREST DISTRICT BISHOPS HALL LAMBOURNE TQ 475 953 Remnants of design and planting under the auspices of Lord Lambourne, who served as president of the RHS (1919-1928). He was well known for his interest in rare plants, both hardy and exotics, which were raised within his series of specialised glasshouses and within the grounds of Bishops Hall representing late 19th and early 20th century work. HISTORIC DEVELOPMENT The Bishops of Norwich held the estate of Bishops Hall in Lambourne from the 13th century until 1536 when the estate was transferred to King Henry VIII. The principal building was situated at the site known as Bishops Moat. Sometime during the ownership of William Walker (d. 1708) and his son Thomas (d. 1748) the manor house was relocated further west from Bishops Moat. The Lockwoods purchased the manor of Lambourne in 1782. By the 1830’s with the addition of Bishops Hall, which became the family seat, the estate comprised the manors of Bishops Hall, Lambourne, St. John’s (originally Lambourne-and-Abridge) and Dews Hall (demolished by mid-19th century). It was not until Lieut. Col. The Right Hon. Amelius Richard Mark Lockwood, P.S., C.V.O., M.P., K.L., J.P. took over the estate that evidence of major work on the property began. In 1910, Col. Lockwood was described as a, ‘… keen hunter, with a stuffed woodcock displayed in Bishops Hall shot by King Edward VII when the guest of Col. Lockwood. The entry for Bishops Hall in the same publication is: ‘…his picturesque Essex seat,’ ‘standing in about one hundred acres of grounds and commanding wide and extensive views, the fine old mansion, Bishops Hall, show great advantage amid the exquisitely laid out gardens, with Col. -

LOCAL GOVERNMENT COMMISSION for ENGLAND PERIODIC ELECTORAL REVIEW of EPPING FOREST Final Recommendations for Ward Boundaries In

S R A M LOCAL GOVERNMENT COMMISSION FOR ENGLAND Deerpark Wood T EE TR S EY DS LIN Orange Field 1 Plantation 18 BURY ROAD B CLAVERHAM Galleyhill Wood Claverhambury D A D O D LR A O IE R F Y PERIODIC ELECTORAL REVIEW OF EPPING FOREST R LY U B O M H A H Bury Farm R E V A L C Final Recommendations for Ward Boundaries in Loughton and Waltham Abbey November 2000 GR UB B' S H NE Aimes Green ILL K LA PUC EPPING LINDSEY AND THORNWOOD Cobbinsend Farm Spratt's Hedgerow Wood COMMON WARD B UR D Y R L A D N Monkhams Hall N E E S N I B B Holyfield O C Pond Field Plantation E I EPPING UPLAND CP EPPING CP WALTHAM ABBEY NORTH EAST WARD Nursery BROADLEY COMMON, EPPING UPLAND WALTHAM ABBEY E AND NAZEING WARD N L NORTH EAST PARISH WARD A O School L N L G L A S T H R N E R E E F T ST JOHN'S PARISH WARD Government Research Establishment C Sports R The Wood B Ground O U O House R K G Y E A L D L A L M N E I E L Y E H I L L Home Farm Paris Hall R O Warlies Park A H D o r s e m Griffin's Wood Copped Hall OAD i l R l GH HI EPPING Arboretum ƒƒƒ Paternoster HEMNALL House PARISH WARD WALTHAM ABBEY EPPING HEMNALL PIC K H PATERNOSTER WARD ILL M 25 WARD z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z z EW WALTHAM ABBEY EYVI ABB AD PATERNOSTER PARISH WARD RO IRE SH UP R School School Raveners Farm iv e r L Copthall Green e e C L N L R a A v O H ig The Warren a O ti K D o K C A n I E T O WALTHAM ABBEY D R M MS Schools O I L O E R B Great Gregories OAD ILL R Farm M H FAR Crown Hill AD O Farm R Epping Thicks H IG H AD N RO -

Abridge Buckhurst Hill Chigwell Coopersale Epping Fyfield

Abridge Shell Garage, London Road Buckhurst Hill Buckhurst Hill Library, 165 Queen’s Road (Coronaviris pandemic – this outlet is temporarily closed) Buckhurst Hill Convenience Store, 167 Queen’s Road (Coronaviris pandemic – this outlet is temporarily closed) Premier & Post Office, 38 Station Way (Coronaviris pandemic – this outlet is temporarily closed) Queen’s Food & Wine, 8 Lower Queen’s Road Valley Mini Market, 158 Loughton Way Valley News, 50 Station Way Waitrose, Queens Road Chigwell Lambourne News, Chigwell Row Limes Centre, The Cobdens (Coronaviris pandemic – this outlet is temporarily closed) Chigwell Parish Council, Hainault Road (Coronaviris pandemic – this outlet is temporarily closed) L. G. Mead & Son, 19 Brook Parade (Coronaviris pandemic – this outlet is temporarily closed) Budgens Supermarket, Limes Avenue Coopersale Hambrook, 29 Parklands Handy Stores, 30 Parklands Epping Allnut Stores, 33a Allnuts Road Epping Newsagent, 83 High Street (Coronaviris pandemic – this outlet is temporarily closed) Epping Forest District Council Civic Offices, 323 High Street (Coronaviris pandemic – this outlet is temporarily closed) Epping Library, St. Johns Road (Coronaviris pandemic – this outlet is temporarily closed) House 2 Home, 295 High Street M&S Simply Food, 237-243 High Street Tesco, 77-79 High Street Fyfield Fyfield Post Office, Ongar Road High Ongar Village Store, The Street Loughton Aldi, Epping Forest Shopping Park Baylis News, 159 High Road Epping Forest District Council Loughton Office, 63 The Broadway -

North Essex Parking Partnership Joint Committee for On-Street Parking

NORTH ESSEX PARKING PARTNERSHIP JOINT COMMITTEE FOR ON-STREET PARKING 1 October 2020 at 1.00pm Online meeting, held on Zoom and broadcast via the YouTube channel of Colchester Borough Council. Members Present: Councillor Nigel Avey (Epping Forest District Council) Councillor Michael Danvers (Harlow District Council) Councillor Richard Van Dulken (Braintree District Council) Councillor Deryk Eke (Uttlesford District Council) Councillor Mike Lilley (Colchester Borough Council) (Deputy Chairman) Councillor Robert Mitchell (Essex County Council) (Chairman) Substitutions: None. Apologies: Councillor Michael Talbot (Tendring District Council) Also Present: Richard Walker (Parking Partnership) Lou Belgrove (Parking Partnership) Liz Burr (Essex County Council) Trevor Degville (Parking Partnership) Rory Doyle (Colchester Borough Council) Qasim Durrani (Epping Forest District Council) Jake England (Parking Partnership) Linda Howells (Uttlesford District Council) Samir Pandya (Braintree District Council) Miroslav Sihelsky (Harlow Council) Ian Taylor (Tendring District Council) James Warwick (Epping Forest District Council) 74. Have Your Say! Dr Andrea Fejős and Professor Christopher Willett attended and, with the permission of the Chairman, addressed the meeting to ask that proposed Traffic Regulation Order (TRO) T29664816 [Manor Road, Colchester] be approved. Although the TRO had been recommended for rejection by Colchester Borough Council, due to lack of local support, Dr Fejős argued that the Committee could still approve it. The TRO had been requested by Dr Fejős and Professor Willett in order to stop vehicles parking in front of a flat’s front window which they noted was the only alternative exit/fire escape for the property. It would prevent such parking and involve moving the parking space to further along the road, on the opposite side of the road. -

© Georgina Green ~ Epping Forest Though the Ages

© Georgina Green ~ Epping Forest though the Ages Epping Forest Preface On 6th May 1882 Queen Victoria visited High Beach where she declared through the Ages "it gives me the greatest satisfaction to dedicate this beautiful Forest to the use and enjoyment of my people for all time" . This royal visit was greeted with great enthusiasm by the thousands of people who came to see their by Queen when she passed by, as their forefathers had done for other sovereigns down through the ages . Georgina Green My purpose in writing this little book is to tell how the ordinary people have used Epping Fo rest in the past, but came to enjoy it only in more recent times. I hope to give the reader a glimpse of what life was like for those who have lived here throughout the ages and how, by using the Forest, they have physically changed it over the centuries. The Romans, Saxons and Normans have each played their part, while the Forest we know today is one of the few surviving examples of Medieval woodland management. The Tudor monarchs and their courtiers frequently visited the Forest, wh ile in the 18th century the grandeur of Wanstead House attracted sight-seers from far and wide. The common people, meanwhile, were mostly poor farm labourers who were glad of the free produce they could obtain from the Forest. None of the Forest ponds are natural . some of them having been made accidentally when sand and gravel were extracted . while others were made by Man for a variety of reasons. -

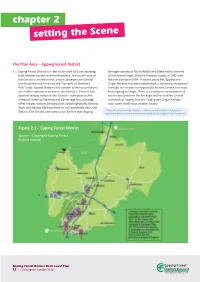

Chapter 2 Setting the Scene

chapter 2 setting the Scene The Plan Area – Epping Forest District 2.1 Epping Forest District is in the south-west of Essex abutting through stations at North Weald and Blake Hall to the end both Greater London and Hertfordshire. The south–west of of the line at Ongar. Blake Hall station closed in 1981 with the District is served by the London Underground Central the line closing in 1994. In recent years the ‘Epping and Line (both the main line and the ‘Hainault via Newbury Ongar Railway’ has been established, a nationally recognised Park’ loop). Epping Station is the eastern terminus and there heritage rail service running on this former Central Line track are 7 other stations in service in the District 1. There is one from Epping to Ongar. There is currently no operational rail national railway station in the District – at Roydon on the connection between the heritage rail line and the Central Liverpool Street to Stansted and Cambridge line, although Line track at Epping, but the ‘Epping and Ongar Railway’ other railway stations (Broxbourne, Sawbridgeworth, Harlow runs some shuttle bus services locally. Town and Harlow Mill) are close to, and accessible from, the 2 District. The Central Line used to run further than Epping, These are Theydon Bois, Debden, Loughton and Buckhurst Hill, together with the stations on the branch line at Roding Valley, Chigwell and Grange Hill Figure 2.1 – Epping Forest District Source – Copyright Epping Forest District Council Epping Forest District Draft Local Plan 12 | Consultation October 2016 2.2 The M25 runs east-west through the District, with a local road 2.6 By 2033, projections suggest the proportion of people aged interchange at Waltham Abbey. -

Public Register of Licensed Mobile Park Home Sites in the District

PUBLIC REGISTER OF LICENSED MOBILE PARK HOME SITES IN THE DISTRICT Licence Number: LN000000132 Issued: 10/09/2013 Site owner: Mr Wood Name of Site: Ashwood Farm Type: Residential Number of Mobile Homes: 1 Other information: Pitch is not in use Licence Number: LN000000127 Issued: 05/11/2012 Site owner: Mr J & Mrs S Wenman Name of Site: Abridge Park Homes, Abridge Mobile Home Park, London Road, Abridge, Romford, Essex Type: Residential Number of Mobile Homes: 65 Licence Number: LN000000128 Issued: 05/11/2012 Site owner: Sines Park Homes Name of Site: Breach Barns Mobile Homes, Breach Barns Mobile Home Park, Galley Hill, Waltham Abbey, Essex Type: Residential Number of Mobile Homes: 250 Licence Number: LN000000130 Issued: 14/11/2012 Site owner: Mrs Marie Zabell Name of Site: Ludgate House Mobile Home Park, Hornbeam Lane, High Beach, Sewardstone, London, E4 7QT Type: Residential Number of Mobile Homes: 20 Licence Number: LN000000126 Issued: 14/11/2012 Site owner: Mrs Marie Zabell Name of Site: The Owl Caravan Park, The Owl Park Home Site Lippitts Hill, High Beach, Loughton Type: Residential Number of Mobile Homes: 20 Licence Number: LN000000125 Issued: 14/11/2012 Site owner: Mrs Marie Zabell Name of Site: The Elms Mobile Home Park, Lippitts Hill, High Beach, Loughton Type: Residential Number of Mobile Homes: 39 Licence Number: LN000002644 Issued: 23/02/2017 Site owner: Dr Claire Zabell Name of Site: The Elms Mobile Home Park, Lippitts Hill, High Beach, Loughton Type: Residential Number of Mobile Homes: 16 Licence Number: LN000000820 Issued: -

Highway Verge Management

HIGHWAY VERGE MANAGEMEN T Planning and Development Note Date 23rd January 2019 Version Number 2 Highway Verge Management Review Date 30th March 2024 Author Geoff Sinclair/Richard Edmonds Highway Verge Management PLANNING AND DEVELOPMENT NOTE INTRODUCTION Planning and Development Notes (PDN) aim to review and collate the City Corporation’s (CoL) property management issues for key activities, alongside other management considerations, to give an overview of current practice and outline longer term plans. The information gathered in each report will be used by the CoL to prioritise work and spending, in order to ensure firstly that the COL’s legal obligations are met, and secondly that resources are used in an efficient manner. The PDNs have been developed based on the current resource allocation to each activity. An important part of each PDN is the identification of any potential enhancement projects that require additional support. The information gathered in each report will be used by CoL to prioritise spending as part of the development of the 2019-29 Management Strategy and 2019-2022 Business Plan for Epping Forest. Each PDN will aim to follow the same structure, outlined below though sometimes not all sections will be relevant: Background – a brief description of the activity being covered; Existing Management Program – A summary of the nature and scale of the activity covered; Property Management Issues – a list of identified operational and health and safety risk management issues for the activity; Management Considerations -

Harlow Local Development Plan Examination 2019 List of Matters and Questions Matter 1: Duty to Co‐Operate An

Harlow Local Development Plan Examination 2019 List of Matters and Questions Matter 1: Duty to co‐operate and other legal requirements 1) This hearing statement sets out the Council’s response in relation to the Inspector’s Specific Matters and Questions in Matter 1: Duty to co‐operate and other legal requirements. Full details in respect of how the Council has accorded with the Duty to Cooperate, including the key organisations it has engaged with, is set out in the Duty to Cooperate Compliance Statement August 2018 (HSD14), that was submitted with the Harlow Local Development Plan (HLDP) in October 2018. 1.1 Duty to Co-operate: 2) The Localism Act 2011 placed a duty on Councils to co‐operate on strategic planning matters that cross administrative boundaries. The Government considered that strategic policy‐making authorities should collaborate to identify the relevant strategic matters which they need to address in their plans. As a former new town, with tight administrative boundaries, Harlow Council has, over the years worked collaboratively with a range of other bodies on strategic planning and related matters affecting the M11 corridor and west Essex and east Hertfordshire. This dates back to when Regional Spatial Planning Strategies provided an overarching strategic plan making framework for the wider area. 3) Specific bodies the Council has co‐operated with in the production of the Harlow Local Development Plan include the following: Neighbouring Local Planning and highway authorities, including East Hertfordshire, Epping Forest -

Minutes from the PFCC Thurrock Online Public Meeting

Minutes of the Police, Fire and Crime Commissioner for Essex Thurrock Online Public Meeting 12th May 2020 Panel Members PFCC Roger Hirst, Dep PFCC Jane Gardner, Ch/Insp Richard Melton, Essex Police, Mark Diggory, ECFRS Station Manager Questions Answers A member of the public has consistently reported drug dealing taking place Ch/Insp Melton – drug dealing does not have a place in the district. It brings next door to them and nothing seems to be done. What was the point in all kinds of other crime with it including turf wars and knife crime. reporting? Fortunately, there are not too many rival gangs in Thurrock. The C17 who were operating out of London via county lines in Thurrock has had significant disruption through great activity thanks to the efforts of the Essex Police Op Raptor teams. It is vital people keep reporting in crime as the information is gathered as intelligence and is shared with partners where applicable, to help build a case and achieve a significant prosecution rather than a quick win. He requested for the public to keep the information coming through. How many arrests have been made in Thurrock for public not achieving PFCC – Thurrock FPNs are slightly lower than other areas. Police will only social distancing compared to reports made by the public? respond to gatherings etc in public areas as they cannot enter homes and gardens without a significant reason. To date there has been around 150 fixed penalty notices and only 18 people arrested county wide. Ch/Insp Melton advised the interaction they have had with the public has been largely positive and often just a case of educating around the lockdown measures. -

Town/ Council Name Ward/Urban Division Basildon Parish Council Bowers Gifford & North

Parish/ Town/ Council Name Ward/Urban District Parish/ Town or Urban Division Basildon Parish Council Bowers Gifford & North Benfleet Basildon Urban Laindon Park and Fryerns Basildon Parish Council Little Burstead Basildon Urban Pitsea Division Basildon Parish Council Ramsden Crays Basildon Urban Westley Heights Braintree Parish Council Belchamp Walter Braintree Parish Council Black Notley Braintree Parish Council Bulmer Braintree Parish Council Bures Hamlet Braintree Parish Council Gestingthorpe Braintree Parish Council Gosfield Braintree Parish Council Great Notley Braintree Parish Council Greenstead Green & Halstead Rural Braintree Parish Council Halstead Braintree Parish Council Halstead Braintree Parish Council Hatfield Peverel Braintree Parish Council Helions Bumpstead Braintree Parish Council Little Maplestead Braintree Parish Council Little Yeldham, Ovington & Tilbury Juxta Clare Braintree Parish Council Little Yeldham, Ovington & Tilbury Juxta Clare Braintree Parish Council Rayne Braintree Parish Council Sible Hedingham Braintree Parish Council Steeple Bumpstead Braintree Parish Council Stisted Brentwood Parish Council Herongate & Ingrave Brentwood Parish Council Ingatestone & Fryerning Brentwood Parish Council Navestock Brentwood Parish Council Stondon Massey Chelmsford Parish Council Broomfield Chelmsford Urban Chelmsford North Chelmsford Urban Chelmsford West Chelmsford Parish Council Danbury Chelmsford Parish Council Little Baddow Chelmsford Parish Council Little Waltham Chelmsford Parish Council Rettendon Chelmsford Parish