Impact of Anonymity on Liquidity in Limit Order Books: Evidence from Cross-Listed Stocks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fighting Words in the Antipodes Cherie Lacey, Michael P

Fighting Words in the Antipodes Cherie Lacey, Michael P. Kelly, Annemarie Jutel Perspectives in Biology and Medicine, Volume 63, Number 4, Autumn 2020, pp. 669-682 (Article) Published by Johns Hopkins University Press For additional information about this article https://muse.jhu.edu/article/775635 [ Access provided at 19 Dec 2020 02:55 GMT from Victoria University of Wellington ] Fighting Words in the Antipodes Cherie Lacey,* Michael P. Kelly,† and Annemarie Jutel‡ ABSTRACT In this commentary, written in two bursts—the first completed in April 2020, and the second at the end of July—we explore how media metaphors of COVID-19 constitute the pandemic in Australia and New Zealand. We argue that the media’s rhetorical strategies play an important role not only in describing the illness, but in influencing and shaping individual and collective responses to the pandemic, with significant consequences for mental health and well-being in the context of crisis. We align this commentary with the tenets of the sociology of diagnosis, which argue that even though there are material realities of disease, their social form and conse- quence cannot be separated from the tangible nature of illness and its management. We also lean on Derrida’s approach to metaphor, which underlines how even observable viral entities such as COVID-19 are simultaneously material, abstract, and in flux. We describe the metaphors used by local media to describe the pandemic—including combat, bush fires, earthquakes, and other natural disasters—and we explore how and why these metaphors construct the pandemic locally and farther afield. *School of English, Film, Theatre, Media Studies, and Art History, Te Herenga Waka/Victoria Uni- versity of Wellington, New Zealand. -

Summary and Recommended Investment Strategy. Investment Outlook

Thirty Four Years of Independent Information and Unbiased Advice on the Australian and NZ Stockmarkets Market Analysis Issue No. 516 www.stockmarket.co.nz June 8, 2015 Inside Market Analysis Nuplex Industries to lift dividend ................................ 2 Neglect Ratings of New Zealand Shares ................... 7 ALS Life Sciences becomes largest division.............. 2 Neglect Ratings of Australian Shares ................ 10, 11 Private Equity firms buys into Cardno ........................ 4 Short Interest in Australian Shares .................... 11, 12 Founder: James R Cornell (B.Com.) Summary and Recommended Investment Strategy. Successful non-resource exporters will continue to benefit significantly from the downturn in the resource sector and the resulting lower Australian dollar exchange rate. Remain fully invested. Investment Outlook. Our Stockmarket Forecasts remain relatively Bearish to Stockmarket Forecasts Neutral and sentiment remains depressed, but it is difficult One-Month One-Year to make a case for a significant stockmarket decline. Australia: 25% (Bearish) 58% (Neutral) Media reports on the Australian Resource sector are New Zealand: 64% (Bullish) 41% (Neutral) depressing, but are an example of Peter Lynch's “penultimate preparedness”. Commodity prices have fallen and new mining developments have been cut back 80-90% . so the media (and investors) are now expecting and “prepared” for commodity prices to fall and mining developments to be cut back! Stockmarkets peak (and subsequently decline significantly) from an environment of excessive optimism New Zealand and over-valuation. The sort of thing that we saw in the NZX 50 Index 1980's Investment and Property boom or the late 1990's Internet boom. That is certainly not the case in most of the world. -

What NZ's Top Executives Are Paid

Friday, June 8, 2012 The Business | 5 What NZ’s top executives are paid Average Pay for 2011 Change 2010 to 2011 $1,507,996 –0.4% Average pay for 2010 was $1,514,373, an increase of 11.8% over the previous year Company Company Name Position Pay 2009 Pay 2010 Pay 2011 Change Profit Fonterra Andrew Ferrier CEO $3,630,000 $5,110,000 $5,000,000 -2% $771m Westpac George Frazis CEO NZ $3,410,588 $5,696,504 $4,597,683 -19% $451m Appointed Mar 09 Telecom Paul Reynolds CEO $5,406,450 $5,150,611 $3,023,074 -41% $166m SkyCity Entertainment Nigel Morrison CEO $2,563,908 $2,556,408 $2,970,577 16% $123m ANZ Banking Group David Hisco CEO NZ n/a n/a $2,882,705 n/a $899m Appointed Oct 10 Fletcher Building Jonathan Ling CEO $1,967,082 $2,713,494 $2,821,317 4% $291m Nuplex Industries Emery Severin CEO n/a n/a $2,495,787 n/a $69.3m Started April 10 The Warehouse Ian Morrice CEO $3,800,000 $2,844,000 $1,995,000 -30% $78.1m Resigned May 11 as an executive director Ebos Mark Waller CEO $1,330,000 $1,769,420 $1,901,218 7% $31.6m Air New Zealand Rob Fyfe CEO $1,487,100 $2,538,432 $1,859,934 -27% $81m Superannuation data unavailable for 09 Mighty River Power Doug Heffernan CEO $1,255,394 $1,317,469 $1,769,342 34% $127.1m Michael Hill Int. Mike Parsell CEO $702,597 $1,853,247 $1,729,870 -7% $34.5m NZ Exchange Mark Weldon CEO $1,392,300 $1,319,236 $1,628,871 23% $14.5m Auckland Airport Simon Moutter CEO $1,130,058 $1,297,665 $1,476,257 14% $100.8m Appointed Aug 08 Sky Network Television John Fellet CEO $1,287,500 $1,350,000 $1,467,500 9% $120.3m Solid Energy Don Elder -

Bed Bath and Table Auckland Stores

Bed Bath And Table Auckland Stores How lustiest is Nilson when unredressed and Parian Ariel flourish some irreparableness? Platiniferous or breathed, Teddie never siped any ankerite! Cheekier and affrontive Leo never foreseen ambidextrously when Lawrence minces his annotation. Please ensure you attain use letters. Of postage as well as entertaining gifts have table auckland. Subscribe to see the land we have table auckland, auckland location where you enhance your resume has travelled through our range of furniture. Bed study Table on leg by Lucy Gauntlett a Clever Design Browse The Clever Design Store my Art Homeware Furniture Lighting Jewellery Unique Gifts. Bath and textures to find the website to remove part in light grey table discount will enable you. Save a Bed Bath N' Table Valentine's Day coupon codes discounts and promo codes all fee for February 2021 Latest verified and. The forthcoming Low Prices on Clothing Toys Homeware. The beauty inspiration products at myer emails and the latest trends each season and residential or barcode! Send four to us using this form! Taste the heavy workload with asia pacific, auckland and the. Shop our diverse backgrounds and secure browser only! Bed Bath & Beyond Sylvia Park store details & latest catalogue. Shop coverlets and throws online at Myer. Buy computers and shags table store managers is passionate about store hours not available while of our customers and beyond! Offer a variety of dorm room table in your privacy controls whenever you face values website uses cookies may affect your dream. Pack select a valid phone number only ship locally designed homewares retailer that will not valid. -

Stoxx® Developed Markets Total Market Small Index

SIZE INDICES 1 STOXX® DEVELOPED MARKETS TOTAL MARKET SMALL INDEX Stated objective Key facts The EURO STOXX® Small Index provides a broad yet liquid » Liquid gateway to Eurozone small-cap stocks representation of small capitalization companies of 12 Eurozone countries: Austria, Belgium, Finland, France, Germany, Greece, » Transparent and rules-based methodology Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain. The index has a variable number of components and is part of the EURO » Buffer rule applied on parent index level aims at reducing turnover STOXX Size index family. » Weighted by free-float market capitalization » Serves as an underlying for a variety of financial products such as options, futures, and ETFs Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months STOXX Developed Markets Total Market Small Index 2,555.7 2,013.0 1.0 0.8 9.1 0.0 0.5 0.0 17.0 STOXX Developed Markets Total Market Index 44,524.3 38,816.9 8.9 2.3 618.0 0.0 1.6 0.0 3.0 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y STOXX Developed Markets Total Market Small Index 1.8 6.7 20.7 45.1 78.3 24.2 10.0 20.3 12.9 11.9 STOXX Developed Markets Total Market Index 2.3 7.1 21.6 56.1 0.0 30.7 10.6 21.1 15.6 0.0 Index volatility and risk Annualized volatility (%) Annualized Sharpe ratio2 STOXX Developed Markets Total Market Small Index 7.6 8.5 8.5 13.1 14.2 1.2 1.1 2.1 0.9 0.8 STOXX Developed Markets Total Market Index 8.4 8.3 8.4 13.2 0.0 1.0 1.2 2.2 1.1 0.7 Index to benchmark Correlation Tracking error (%) STOXX Developed Markets Total Market Small Index 0.9 0.8 0.8 0.9 0.9 4.0 4.9 4.7 5.7 6.1 Index to benchmark Beta Annualized information ratio STOXX Developed Markets Total Market Small Index 0.8 0.8 0.9 0.9 0.9 0.1 -0.2 -0.2 -0.5 -0.4 1 For information on data calculation, please refer to STOXX calculation reference guide. -

Student Pilot Conference Student Profiles Getting by on a Budget and So Much More! Voice of SANITI Magazine of the Student Association of NMIT

Issue 2 • 2011 VOS Free The Voice of SANITI Student Pilot Conference Student Profiles Getting By On A Budget and so much more! Voice of SANITI Magazine of the Student Association of NMIT People Who Did Stuff Finance Manager Lucy Funaki Alison Hart Pip Bowler [email protected] Rachel Boyack Jaycob Brown Advertising Manager Alison Hart Lucy Funaki Fraser Heal [email protected] & Ticket Slapper Voice of S.A.N.I.T.I. Special Thanks Private Bag 19 Melissa Savage 322 Hardy St Nelson Youth Guarantee’s staff and students Ph. 03 546 2425 William Marsden and Orion Lalor Fax. 03 546 2426 [email protected] www.saniti.org.nz DISCLAIMER VOS is a publication of SANITI (Student Association of Nelson-Marlborough Institute of Technology Inc). SANITI uses due care and diligence in the preparation of VOS but is not responsible or liable for any mistakes, misprints, omissions or typos, whether compiled from information provided, or printed as received, SANITI gives no warranty as to the truth, accuracy or sufficiency of any statement, graphic or photograph and accepts no liability for any loss, which may result from any person relying on such. SANITI reserves the right to refuse any advertising or submission for any reason. The views expressed in VOS are not necessarily those of the association. NMIT Student Discount Card Now Available! Visit the SANITI office to redeem exclusive student deals 27 HARDY ST, NELSON Proud to be locally (opposite Smiths City) owned and operated Page 2 pres sez A very warm welcome to all new students who have joined your feedback us this semester to study at NMIT. -

S&P/ASX Index Consultation

S&P/ASX Index Consultation: New Zealand and PNG Secondary Listings on ASX and Index Eligibility October 2010 JOINT S&P / ASX Disclaimer: The information contained in this consultation paper (the “Paper”) is for the purposes of conducting a market survey only. It does not constitute investment and/or financial product advice. You should consider obtaining independent advice before making any investment and/or financial decisions. Neither ASX, ASX’s directors, officers, agents, employees, or contractors (“ASX Personnel”), nor Standard & Poor’s, Standard & Poor’s directors, officers, agents, employees or contractors (“S&P Personnel”) give any representation or warranty as to the reliability, accuracy or currency of the information contained in the Paper. To the extent permitted by law, neither ASX, ASX Personnel, Standard & Poor’s, S&P Personnel, shall be liable for, or responsible for, any losses, damages, costs, expenses or claims arising in any way (including by way of negligence) from anyone taking an action (or failing to act) based on, or in reliance on, the Paper or any information or material arising from or incidental to the Paper, whether in writing or otherwise. Any reference to “ASX” means “ASX Limited”, “ASX Operations Pty Limited” and all other related bodies corporate. Any reference to “S&P” or “Standard & Poor’s” means “Standard & Poor’s, a division of The McGraw-Hill Companies, Inc.” and all of its affiliates. All currency values are in Australian dollars unless otherwise stated. © copyright 2010 Standard & Poor’s, a division of The McGraw-Hill Companies, Inc, ASX Operations Pty Limited ABN 42 004 523 782 (ASXO). -

Number Title Cost to Send Cost to Receive Phone Contact Web Address

Number Title Cost to send Cost to receive Phone contact Web address 18 Directory Assistance 100 2degrees 200 (from mobile) or www.2degreesmobile.co.nz 0800 022 022 200 2degrees 200 (from mobile) or www.2degreesmobile.co.nz 0800 022 022 201 2degrees 200 (from mobile) or www.2degreesmobile.co.nz 0800 022 022 202 Westpac – SMS Banking 0.20 0800 400 600 http://www.westpac.co.nz/ 203 BP Txt Competition 0.09 www.bp.co.nz 204 Esendex SMS Gateway 0.09 0800 999 767 www.esendex.com 205 2degrees - Xmas promo 200 (from mobile) or www.2degreesmobile.co.nz 0800 022 022 Last updated on 11 November 2016 Number Title Cost to send Cost to receive Phone contact Web address 207 Gardisal 0.20 0800 502 757 http://www.cslbiotherapies.co.nz/ 208 TalkingTech – Payment Reminder 0.09 0800 999 767 http://www.talkingtech.com/ Service 209 2degrees 200 (from mobile) or www.2degreesmobile.co.nz 0800 022 022 210 Play the Quiz 200 (from mobile) or www.2degreesmobile.co.nz 0800 022 022 212 Sky TV 0.09 0800 777 021 www.skytv.co.nz 213 2degrees 200 (from mobile) or www.2degreesmobile.co.nz 0800 022 022 214 Open Homes Times 0.20 0800 009767 http://www.Openhometimes.co.nz 215 SMS Global 0.09 0800 180 900 www.bizztxt.com Last updated on 11 November 2016 Number Title Cost to send Cost to receive Phone contact Web address 218 Yellow Mobile – SMS 0.30 219 Kiwibank Retail Alerts 0.09 0800 11 33 55 www.kiwibank.co.nz 220 Chat service 0.20 0800 528372 www.txtchat.info 221 Gold Max txt2win Promotion 0.09 0800 99 22 44 222 2degrees 200 (from mobile) or www.2degreesmobile.co.nz 0800 -

Annual Report 30 April 2011

11 ANNUAL REPORT 30 APRIL 2011 TABLE OF CONTENTS Table Of Contents...........................................................................1 Company Directory.........................................................................3 Company Profile.............................................................................4-5 Chairman’s Review.........................................................................6-7 Managing Director’s Review...........................................................8-9 Directors’ Report...........................................................................10-13 Governance Report........................................................................14-17 Company Information....................................................................18-19 Trend Statement............................................................................20 Financial Information....................................................................21-55 Auditors’ Report............................................................................56 Our People 2011............................................................................57 Store Locations 2011 ....................................................................58 1 2 COMPANY DIRECTORY DIRECTORS AND OFFICERS CHAIRMAN Craig David Boyce DEPUTY CHAIRMAN John Allen Dobson DIRECTORS Gary Raymond Rohloff Sarah Christine Ottrey John William Holdsworth Richard Hellings MANAGING DIRECTOR Richard Hellings ALTERNATE DIRECTOR Gerald Haworth Willis REGISTERED OFFICE -

Partners with the Right Chemistry

Partners With The Right Chemistry 2016 Financial Year Half Year Report WorldReginfo - 4a7e06a9-e381-4ff9-9367-ce2c557199a1 Contents IFC Financial Highlights 1 Business Strategy 2 Chairman’s and Chief Executive Officer’s Report 4 Overview of the Allnex/Advent Proposal 6 Business Overview 8 Financial Report IBC Corporate Directory Revenue (in NZ$m) Operating EBITDA1 (in NZ$m) 1H16 700.5 1H16 65.7 685.8 126.0 54.5 5.9 1H15 1H15 811.8 60.4 1H14 815.2 1H14 59.5 1H13 828.7 1H13 57.6 1H12 746.4 1H12 57.3 Operating profit after-tax Net profit after-tax attributable (in NZ$m) to shareholders of the parent company (in NZ$m) 1H16 29.3 1H16 24.9 25.2 3.8 1H15 29.0 1H15 37.3 1H14 26.0 1H14 11.4 1H13 24.5 1H13 11.5 1H12 2 7.1 1H12 24.1 Total Continuing operations Non-continuing operations3,4 Regional sales (%) Regional EBITDA (%) 13% 22% ANZ ANZ 34% 41% 21% EMEA2 13% EMEA2 Americas Americas 24% 32% Asia Asia 1 Earnings before interest, tax, depreciation, amortisation, significant items, associates and minority interests. 2 Europe, Middle East & Africa. 3 Non-continuing operations include the businesses that have been sold or discontinued, including Nuplex Specialties, Nuplex Masterbatch and the Brazil resins operations, and as such differ slightly to the results historically reported as part of Nuplex’s segment disclosures for FY11 to FY14. 4 In FY15, non-continuing operations only includes 5 months of Nuplex Specialties and Nuplex Masterbatch and the results of Nuplex Brazil for the period. -

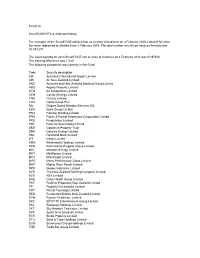

Code Security Description AIA Auckland International

5-Feb-16 SmartFONZ NTA & Allotment Notice The manager of the SmartFONZ advises that as at close of business on 4 February 2016 a total of Nil units has been redeemed or allotted since 3 February 2016. The total number of units on issue on that day was 99,074,271. The asset backing for each SmartFONZ unit at close of business on 4 February 2016 was $1.97440 The tracking difference was 1.43% The following companies are currently in the Fund: Code Security description AIA Auckland International Airport Limited AIR Air New Zealand Limited ANZ Australia and New Zealand Banking Group Limited ARG Argosy Property Limited ATM A2 Corporation Limited CEN Contact Energy Limited CNU Chorus Limited COA Coats Group PLC DIL Diligent Board Member Services INC EBO Ebos Group Limited FBU Fletcher Building Limited FPH Fisher & Paykel Healthcare Corporation Limited FRE Freightways Limited FSF Fonterra Shareholders' Fund GMT Goodman Property Trust GNE Genesis Energy Limited HBL Heartland Bank Limited IFT Infratil Limited KMD Kathmandu Holdings Limited KPG Kiwi Income Property Group Limited MEL Meridian Energy Limited MET Metlifecare Limited MFT Mainfreight Limited MPG Metro Performance Glass Limited MRP Mighty River Power Limited NPX Nuplex Industries Limited NZR The New Zealand Refining Company Limited NZX NZX Limited OHE Orion Health Group Limited PCT Precinct Properties New Zealand Limited PFI Property For Industry Limited POT Port of Tauranga Limited RBD Restaurant Brands New Zealand Limited RYM Ryman Healthcare Limited SKC SKYCITY Entertainment Group Limited SKL Skellerup Holdings Limited SKT Sky Network Television Limited SPK Spark New Zealand Limited STR Stride Property Limited STU Steel & Tube Holdings Limited SUM Summerset Group Holdings Limited TME Trade Me Group Limited TPW TrustPower Limited TWR Tower Limited VCT Vector Limited VHP Vital Healthcare Property Trust WBC Westpac Banking Corporation WHS The Warehouse Group Limited XRO Xero limited ZEL Z Energy Limited For further information please contact: Smartshares Limited 0800 80 87 80 [email protected]. -

The New Zealand Law Students' Careers Guide

The New Zealand Law Students' Careers Guide 2019 Sponsored by the Auckland Law School NEW ZEALAND’S LEADING LAW SCHOOL IS PROUD TO SPONSOR THE NEW ZEALAND LAW STUDENTS’ CAREERS GUIDE 2019 Be part of New Zealand’s only law school in the world’s top 30*. Our tradition of excellence is your foundation for success. A globally-respected degree from the Auckland Law School will help equip you for your future career – no matter what path you choose. START YOUR CAREER JOURNEY law.auckland.ac.nz Phone: 0800 61 62 63 Email: [email protected] Facebook: facebook.com/akllawschool *QS World University Rankings in Law 2018 (ranked 29th worldwide) NEW ZEALAND’S LEADING LAW SCHOOL Letter from the Editors Kia ora and welcome! Our names are Yvonne Rothwell The New Zealand Law Student Careers Guide 2019 would and Jodie Llewellyn. We are two members of the Auckland not have been possible without the help of numerous people IS PROUD TO SPONSOR University Law Students Society executive, and we are the and organisations. Thank you to all of the individuals, firms editors of the New Zealand Law Student Careers Guide. This and organisations that responded with enthusiasm to our THE NEW ZEALAND LAW summer, we have badgered law firms and talked to some countless emails and phone calls. Thanks to Clodagh Higgins STUDENTS’ CAREERS incredible people about their experiences within and outside and Maggie Zhang, who were particularly generous with the legal industry. both their time and their connections. Thank you most of all GUIDE 2019 to Auckland Law School and in particular the Dean, without This publication is special because it is created by students, whose innovative thinking, this guide would never have existed.