Romsey Town Centre Study, University of Southampton, 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Week Ending 27Th June 2008

TEST VALLEY BOROUGH COUNCIL – PLANNING SERVICES _____________________________________________________________________________________________________________ WEEKLY LIST OF PLANNING APPLICATIONS AND NOTIFICATIONS : NO. 25 Week Ending: 27th June 2008 _____________________________________________________________________________________________________________ Comments on any of these matters should be forwarded IN WRITING (including fax and email) to arrive before the expiry date shown in the second to last column For the Northern Area to: For the Southern Area to: Head of Planning Head of Planning Beech Hurst Council Offices Weyhill Road Duttons Road ANDOVER SP10 3AJ ROMSEY SO51 8XG In accordance with the provisions of the Local Government (Access to Information Act) 1985, any representations received may be open to public inspection. You may view applications and submit comments on-line – go to www.testvalley.gov.uk APPLICATION NO./ PROPOSAL LOCATION APPLICANT CASE OFFICER/ PREVIOUS REGISTRATION PUBLICITY APPLICA- TIONS DATE EXPIRY DATE 08/01552/FULLN Raise height of roof to Little Wanaka, Salisbury Road, Mr And Mrs Pike Mr Gregg Chapman 23.06.2008 facilitate first floor Abbotts Ann, Andover 16.07.2008 ABBOTTS ANN accomodation to include 7 Hampshire SP11 7NX dormer windows and the provision of 4 bedrooms, 3 bathrooms, 2 dressing rooms and balcony, together with extensions at ground floor to provide workshop/store, lobby and lounge and erection of detached garage 08/01617/TPON T1 (Yew) - Prune Greenhaven, 23 Hillside, Mrs Sarah Cotton -

E-NEWSLETTER January 2010

Three Rivers Community Rail Partnership E-NEWSLETTER January 2010 Welcome to the latest Three Rivers Community Rail Partnership e-newsletter, which is full of reports about our recent activities; what is happening at the stations along the ‘figure of 6’ route and information about some of the interesting projects that we have coming up. Community Rail Partnership Southampton Tunnel improvements Major engineering work took place in Southampton Tunnel from December 2009 into January of this year. As part of an upgrade of the railway line to accommodate larger freight containers, the tracks under the tunnel were renewed and lowered. Whilst the process caused some disruption to passengers, and included a closure of the line over Christmas, the long-term effects will benefit our region considerably. Congratulations to South West Trains and Network Rail for managing the process and closure so well and to the contractors who worked so hard - day and night - to finish the job on time. Above: Southampton Tunnel during the rail engineering works. A number of other structures in the area were either altered or removed to accommodate the new taller containers. The brick road-bridge carrying one half of St. Deny’s Road over the railway north of St. Denys station was demolished and a new concrete box-structure bridge was built. Also, part of the canopy over Platform 2 at St. Denys station needed to be removed as it was too low for the containers to fit underneath. Southampton Central footbridge repainted After several months closure for refurbishment, the public footbridge (right) located at the Civic Centre end of Southampton Central station has re-opened and now looks much smarter in a coat of blue paint. -

Dowd's Farm Residents Group Meeting – Notes

Dowd’s Farm residents group meeting – notes 27th June 2013 In attendance: Residents Shirley Ann Hennigan-Finlay Saffron Daffnias Pat Taylor Dave Sheath Nathan Thompson James Arnott Dave Cousins Helen Booth Helen Parker Rich Kenchington Others Ian Davis – Salvation Army (also resident) Councillor Louise Bloom (also resident) Jon Riddell – Area Co-ordinator, Eastleigh Borough Council PCSO Matt Wheeler Paula Windebank – Radian Apologies: Matt Ball Kevin Glyn-Davies - Town Clerk, Hedge End Town Council Councillor Derek Pretty PCSO Tracey Chilcott 1. Matters arising from minutes Update on Park and Stride scheme Jonathan Riddell confirmed that the Local Area Committee approved the funding for the scheme to go ahead. A budget has been set up for the work and an engineer has been appointed. A topographical study discovered that a full drainage scheme is needed, which will be built into the design. This is unfortunate as it means the works will be more complex than anticipated and a planning application is needed, which means it will not be ready for September as originally thought. The aim of the park and stride is to ease parking problems at the school. It will be managed by Hedge End Town Council. Residents were assured that the car park will be locked every evening, probably around 10pm. The car park will have the same height barrier to deter travellers. The planning application will include a period of public consultation so residents can voice feedback then if they have any. Community centre Ian Davis has been talking to groups who expressed an interest in using the centre when it is open. -

SITE: Land at Hedge End Retail Park, Tollbar Way, Hedge End, Southampton, SO30 2UN

HEDGE END, WEST END & BOTLEY Monday 12 January 2015 Case Officer Andy Grandfield SITE: Land at Hedge End Retail Park, Tollbar Way, Hedge End, Southampton, SO30 2UN Ref. F/14/75520 Received: 04/11/2014 (08/01/2015) APPLICANT: CBRE Lionbrook Property Fund PROPOSAL: Construction of new retail unit (gross floor area 929 sqm) and alterations to car park and vehicle access point (for sale of pet related products with associated veterinary services facility) AMENDMENTS: None RECOMMENDATION: Subject to: (1) Consideration of comments from Head of Housing and Environmental Health; (2) Additional information on the sequential test and retail impact; (3) Securing a section 106 agreement for contribution towards sustainable transport, environmental improvements to Eastleigh Town Centre/BID and off-site carbon fund (if BREEAM 'Excellent' is not achieved), Pets at Home to be first occupier of building. PERMIT CONDITIONS AND REASONS: (1) The development hereby permitted shall be implemented in accordance with the following plans numbered: PL 020 A, PL 021 B, PL 100 A, PL 101 A, PL 102, PL 200 A, PL 300, PL 301, PL350 A Reason: For the avoidance of doubt and in the interests of proper planning. (2) The development hereby permitted shall start no later than three years from the date of this decision. Reason: To comply with Section 91 of the Town and Country Planning Act 1990 (3) No development shall start until the following details have been submitted to and approved in writing by the Local Planning Authority: a) details and samples of the materials to be used in the construction of the external surfaces of the building. -

Eastleigh Borough Council Retail and Leisure Needs Assessment 2017 Final Report

EASTLEIGH BOROUGH COUNCIL RETAIL AND LEISURE NEEDS ASSESSMENT 2017 FINAL REPORT July 2017 One Chapel Place, London, W1G 0BG CONTENTS 1 INTRODUCTION 1 2 PLANNING POLICY REVIEW 3 NATIONAL PLANNING POLICY FRAMEWORK (NPPF) 3 CHANGES TO PERMITTED DEVELOPMENT RIGHTS 5 LOCAL PLANNING POLICY CONTEXT 5 SUMMARY 8 3 RETAIL AND TOWN CENTRE TRENDS 9 RETAIL TRENDS 9 SPECIAL FORMS OF TRADING AND INTERNET SHOPPING 10 FLOORSPACE ‘PRODUCTIVITY’ GROWTH 12 IMPACT OF OUT-OF-CENTRE RETAILING 12 CHANGING RETAILER REQUIREMENTS 13 VACANCY LEVELS 14 TRENDS IN RETAIL-LED INVESTMENT AND DEVELOPMENT 15 INDEPENDENTS AND MARKETS 16 SUMMARY 17 4 CATCHMENT AREA & SHOPPING PATTERNS 19 STUDY AREA AND ZONES 19 HOUSEHOLD TELEPHONE INTERVIEW SURVEY & MARKET SHARE ANALYSIS 21 5 TOWN CENTRE HEALTH CHECKS: METHODOLOGY 27 6 EASTLEIGH TOWN CENTRE - HEALTH CHECK ASSESSMENT 29 CONTEXT 29 RETAIL COMPOSITION & DIVERSITY OF USES 30 MULTIPLE AND INDEPENDENT RETAIL REPRESENTATION 34 MARKETS 34 VACANCIES 34 RETAILER DEMAND & REQUIREMENTS 35 PRIME ZONE A RENTS 35 ACCESSIBILITY & PEDESTRIAN FLOWS 36 CUSTOMER VIEWS AND PERCEPTIONS 38 ENVIRONMENTAL QUALITY 39 OUT-OF-CENTRE PROVISION 40 NEW INVESTMENT & POTENTIAL DEVELOPMENT 40 SUMMARY 40 7 HEDGE END DISTRICT CENTRE - HEALTH CHECK ASSESSMENT 42 CONTEXT 42 RETAIL COMPOSITION & DIVERSITY OF USES 42 VACANCIES 44 RETAILER DEMAND 45 PRIME ZONE A RENTS 45 ACCESSIBILITY 45 CUSTOMER VIEWS AND PERCEPTIONS 45 ENVIRONMENTAL QUALITY 47 OUT-OF-CENTRE PROVISION 47 SUMMARY 48 8 FRYERN CENTRE, CHANDLER’S FORD DISTRICT CENTRE - HEALTH CHECK ASSESSMENT 50 i -

Job Vacancy / Information Bulleti Nn

Produced fortnightly 6 February 2014 JJoobb VVaaccaannccyy // IInnffoorrmmaattiioonn BBuulllleettiinn for young people A collection of current job vacancies, training opportunities and informat ion, from various sources www.youngsouthampton.org www.youngsouthampton.org Glow in the Park are a series of 5k and 10k evening runs throughout parkland venues across the UK. All participants are encouraged to wear high-viz clothing, head torches, glow sticks and anything else that you can think of that GLOWS! Join in the fun at Southampton Common on the 19th February, whether you are a keen athlete or a novice runner just wanting to beat your personal targets – The Glow in the Park Runs are perfect for you! All abilities can run together in a safe, friendly and fun environment. So whether you are an individual, family, group or team everyone is welcome to sign up and Get Their Glow On! www.glowinthepark.co.uk CONTENTS Page No: Job Vacancies today in the Echo 3 Other vacancies 5 Volunteering opportunities 21 Information 22 Featured Career 25 Training 35 Apprenticeships 59 Advice / support 65 2 DDaaiillyy EEcchhoo VVaaccaanncciieess 6 February 2014 Please consult the relevant edition of the ECHO or visit the website for further details as all information below has been abbreviated. Vacancy information correct at time of publication. Some employers are unable to employ young people directly from school due to age restrictions in their insurance policies, so please check at the time of application. Trainee Insurance Broker Page 34 Chandlers Ford Norris and Fisher Required for busy commercial brokerage. This full time role would suit someone with a strong customer focus who enjoys a variety of tasks. -

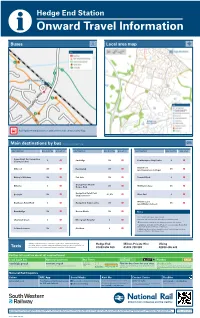

Hedge End Station I Onward Travel Information Buses Local Area Map

Hedge End Station i Onward Travel Information Buses Local area map Rail replacement buses from station forecourt off Stroudley Way. Contains Ordnance Survey data © Crown copyright and database right 2018 & also map data © OpenStreetMap contributors, CC BY-SA Main destinations by bus (Data correct at August 2019) DESTINATION BUS ROUTES BUS STOP DESTINATION BUS ROUTES BUS STOP DESTINATION BUS ROUTES BUS STOP Ageas Bowl (for Hampshire 8 A Curdridge X9 A Southampton City Centre 8 A County Cricket) Swanmore Allbrook X9 A Eastleigh ^ X9 A X9 A (and Swanmore College) Bishop's Waltham X9 A Fair Oak X9 A Townhill Park 8 A Grange Park Mobile Bitterne 8 A X9 A Waltham Chase X9 A Homes Park Hedge End Retail Park Botley ^ X9 A 8*, X9 A West End 8 A (Superstores) + Wildern Lane Bradbeers Retail Park 8 A Hedge End Town Centre X9 A X9 A (and Wildern School) Brambridge X9 A Horton Heath X9 A Notes Bus route 8 runs seven days a week. Chartwell Green 8 A Moorgreen Hospital 8 A Bus route X9 (and X10) run Mondays to Saturdays only. ^ Direct trains operate to this destination from this Station. * Alight bus at Bradbeers Retail Park, it's a short walk to Hedge End Retail Park (Superstores) via Tollbar Way. Colden Common X9 A Northam 8 A + Additional bus services depart for other local destinations from Hedge End Retail Park (Superstores). Hedge End Station has no taxi rank or cab office. Advance booking is Hedge End Millers Private Hire Viking essential, please consider using the following local operators: (Inclusion of Taxis this number doesn’t represent any endorsement of the taxi firm) 01489 696 969 01489 788 888 02380 406 633 Further information about all onward travel Local Cycle Info National Cycle Info Bus Times PlusBus See timetable eastleigh.gov.uk sustrans.org.uk displays at bus Find the bus times for your stop. -

The Peveril Edwin Jones

THE PEVERIL EDWIN JONES STOCK COUNTY HIGH SCHOOL EASTLEIGH SCHOOLWEAR AT PRICES YOU WILL NOT BETTER BOYS' WEAR QUEEN'S BUILDINGS AND PORTSWOOD GIRLS' WEAR QUEEN'S BUILDINGS EDWIN JONES & Co. Ltd. Tel. 3888 SOUTHAMPTON BRADBEERS (SMITH BRADBEER & CO. LTD.\ late Above Bar, Southampton) EST. 1837 Phone 87796 FOR VALUE IN LADIES' WEAR MENS' WEAR CHILDRENS' WEAR AND HOUSEHOLD BOYS' WEAR AND SOFT FURNISHINGS The Corner 80 MARKET ST. 38 MARKET ST. BRANCHES at ROMSEY & NEW MILTON For MEDICINE and Sick-room Requisites NURSE says WAINWRIGHTS are GOOD CHEMISTS and always at your SERVICE WAINWRIGHTS are AGENTS for PERFUMERY — LIP-STICK _ FACE POWDER by REVLON HELENA RUBENSTEIN — CHEN YEU _ COTY — YARDLEY — ATKINSON — 4711, etc. FRANK WAINWRIGHT & SON, LTD. EASTLEIGH, BISHOPSTOKE, CHANDLERS-FORD B. H. WILDING & SONS Noted for Hardware C , hina anb Prorating fhlattriaN Watch out for our vans 73 HIGH STREET, EASTLEIGH Tel. 87373 THE PEVERIL DIEU DEFEND LE DROIT THE MAGAZINE OF THE COUNTY HIGH SCHOOL, EASTLEIGH • Vol. III AUTUMN 1953 No. 17 , FOREWORD By The Headmaster Fr WAS not to be expected that the renaissance of initiative and adventure, spread throughout our country and empire by the accession and coronation of our gracious and radiant young Queen, should be lacking in the School, and now, in this coronation issue of THE PEVERIL, we have visual evidence that it exists. The Editor and his assistants are to be congratulated on producing, out of their limited resources, a number worthy of the occasion. But neither the School nor THE PEVERIL can rest there. We the readers of this magazine, will be living through the new Elizabethan Age, and it is for us and our contemporaries to ensure that the glories and achievements of this reign shall surpass those of the first 'Elizabeth. -

Fareham Retail and Commercial Leisure Study Final Report

Fareham Retail and Commercial Leisure Study Final Report Fareham Borough Council 11 January 2017 15096/PW/PW Nathaniel Lichfield & Partners 14 Regent's Wharf All Saints Street London N1 9RL nlpplanning.com This document is formatted for double sided printing. © Nathaniel Lichfield & Partners Ltd 2017. Trading as Nathaniel Lichfield & Partners. All Rights Reserved. Registered Office: 14 Regent's Wharf All Saints Street London N1 9RL All plans within this document produced by NLP are based upon Ordnance Survey mapping with the permission of Her Majesty’s Stationery Office. © Crown Copyright reserved. Licence number AL50684A Fareham Retail and Commercial Leisure Study : Final Report Contents 1.0 Introduction 1 Overview .......................................................................................................... 1 Report Structure ............................................................................................... 2 2.0 The Hierarchy of Centres 3 Introduction ...................................................................................................... 3 Centres in Fareham and the Surrounding Area ................................................ 3 Existing Retail Provision in Fareham Borough ................................................. 5 Demographic Trends in the Sub-Region .......................................................... 8 3.0 Retail Need Assessment 10 Introduction .................................................................................................... 10 Study Area .................................................................................................... -

Hedge End Southampton So30 4Rt

Prime Retail Investment Opportunity THE FIRST PURPOSE BUILT NEXT FASHION, HOME & GARDEN STORE NEXT GROUP PLC CHARLES WATTS WAY HEDGE END SOUTHAMPTON SO30 4RT enter uuu Prime Retail Investment Opportunity NEXT GROUP PLC t previous next u Investment Summary • A “Trophy” Retail Superstore opportunity located in Hedge End, Southampton. • An affluent catchment with 745,237 persons living within a 20 minute drive time. • Prominent position at the entrance/exit to Junction 7, M27, immediately adjacent to Hedge End Retail Park and opposite to the large M&S and Sainsbury’s superstores. • Benefits from excellent critical mass being located at the heart of one of the South’s largest Retail Warehouse Shopping destinations (735,000 sq ft). u investment summary • Freehold. u location • A new 86,523 sq ft (GIA) quality retail development built and warranted by Next to an extremely high specification. u demographics • Open A1 non-food planning consent. u situation & • The UK’s first purpose built Next “Fashion, Home and retail warehousing Garden” format store. M27 • A New 21 year 3 month lease, (20 years unexpired) to the u description A334 Charles Watts Way undoubted covenant of Next Group Plc. u accommodation, • A commencing rent of £1,454,313 pax with a fixed uplift tenure & planning at Year 5, measured by CPI with 1.5% and 3% collar Junction 7 and cap. u tenancy • Offers are invited in excess of £28,940,000 (Twenty-Eight Million, Nine Hundred and Forty Thousand Pounds), u income & x which reflects a Net Initial Yield of 4.75%, assuming purchasers costs of 5.8%.