Memorandum Number: 201810007 Release Date: 3/9/2018 CC:TEGE:EOEG:ET2 POSTN-135283-17

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Expatriate & Secondment Arrangements

Expatriate & Secondment Arrangements Presentation for: Presented by: Executive Compensation Webinar Series Anthony J. Eppert June 8, 2017 713.220.4276 [email protected] Housekeeping: Technical Issues and Questions . Technical issues – If you are having difficulty viewing this presentation, please call Cisco WebEx Tech Support toll free at 866.229.3239 . Questions during this presentation – We encourage questions (even though your audio lines are muted) – To submit a question, simply type the question in the blank field on the right-hand side of the menu bar and press return – If time permits, your questions will be answered at the end of this presentation. And if there is insufficient time, the speaker will respond to you via e-mail shortly after this presentation i Housekeeping: Recording, CE Credits and Disclaimer . Recording – This presentation is being recorded for internal purposes only . Continuing education credits – A purpose of the webinar series is to provide FREE CE credits – To that end, each presentation is intended to provide 1 credit hour in the following areas: CLE: 1 credit hour (Texas) CPE: 1 credit hour (Texas) HRCI: This activity has been approved for 1 (HR (General)) recertification credit hours toward California, GPHR, PHRi, SPHRi, PHR, and SPHR recertification through the HR Certification Institute SHRM: This program is valid for 1 PDC for the SHRM-CPSM or SHRM-SCPSM – If you have any questions relating to CE credits, please direct them to Anthony Eppert at [email protected] or 713.220.4276 . Disclaimer – This presentation is intended for informational and educational purposes only, and cannot be relied upon as legal advice – Any assumptions used in this presentation are for illustrative purposes only – No attorney-client relationship is created due to your attending this presentation or due to your receipt of program materials ii Housekeeping: About Anthony “Tony” Eppert . -

U.S. Taxation of Americans Abroad

U.S. taxation of Americans abroad Global Mobility Services 2017 ______ kpmg.com U.S. taxation of Americans abroad The following information is not intended to be “written advice concerning one or more federal tax matters” subject to the requirements of section 10.37(a)(2) of Treasury Department Circular 230 as the content of this document is issued for general informational purposes only. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser. KPMG LLP (U.S.) does not provide legal services. * * * * * * If you are a citizen or resident of the United States who lives or works abroad, this publication is designed to help you understand your U.S. income tax obligations. Your tax situation may be especially challenging in the year that you move to or from the United States, and it is generally advisable to seek tax advice in both the U.S. and your host country before you move, if possible, thereby helping to prevent tax “surprises” in either country. United States tax law is continually changing. This booklet reflects U.S. income tax law as it applies to taxable years ending on or before December 31, 2016. You may also be interested in our companion publication, U.S. Taxation of Foreign Citizens, which is available online on the KPMG Global Mobility Services Web page on http://www.kpmg.com at this link. For further information, please contact your local KPMG International member firm’s office. -

Congress Move to Create Business Incentives

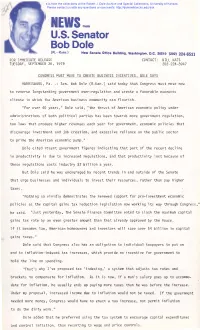

This press release is from the collections at the Robert J. Dole Archive and Special Collections, University of Kansas. Please contact us with any questions or comments: http://dolearchive.ku.edu/ask ·. NEWS,,om U.S. Senator Bob Dole (R.-Kans.) New Senate Office Building, Washington, D.C. 20510 (202) 224-6521 FOR IMMEDIATE RELEASE CONTACT: BILL KATS TUESDAY, SEPTEMBER 26, 1978 202-224-8947 CONGRESS MUST MOVE TO CREATE BUSINESS INCENTIVES, DOLE SAYS HARRISBURG, Pa. -- Sen. Bob Dole (R-Kan.) said today that Congress must move now to reverse loiJgs.tanding ,government over-regulation and create a favorable economic climate in -which the American· business community can flourish. "For over-40 years," Dole said, "the thrust of American economic policy under administrations of both politi_cal parties has been towards more government regulation, tax laws that produce higher revenues each year for government, economic policies that discourage investment and job creation, and excessive reliance on the public sector to prime the American ec onomic pump." Dole cited recent. government figures indicating that part of the recent decline in productivity is due to increased regulations, and that productivity lost because of . these regulations costs industry $2 billion a year. But Dole said he was encouraged by recent trends in and outside of the Senate that urge businesses and individuals to.invest their resources, rather than pay higher taxes. 11Nothing so vivi dl y demonstrates the renewed support for pro-investment economic policies as the capital _gains tax reduction legislation now working its way through Congress," he sai-d. "Just yesterday, the Senate· Finance Co1110ittee voted to slash the maximum capital gains tax rate by an even greater amount than that already approved by the House. -

Title 350, Chapter 40: Property Tax Exemptions

NEBRASKA ADMINISTRATIVE CODE Title 350 – Nebraska Department of Revenue, Property Assessment Division Chapter 40 – Property Tax Exemption Regulations Effective Date – 7/3/2013 Alphabetic Table of Contents SUBJECT STATUTORY AUTHORITY SECTIONS Agricultural and Neb. Rev. Stat. §§ 77-202, and 77-702. 004 Horticultural Society Property Tax Exemptions Application, County Neb. Rev. Stat. §§ 45-104.01, 77-202.01, 77-202.02, 77-202.03, 006 Review, and Appeal 77-202.04, 77-202.05, 77-202.10, 77-203, 77-702, 77-1502, and Procedures for Property Tax 77-5013. Exemptions Beginning Farmer Personal Neb. Rev. Stat. §§ 49-1202, 49-1203, 77-104, 77-105, 77-118, 012 Property Exemption 77-119, 77-120, 77-377, 77-702, 77-5203, and 77-5209.02. Disabled or Blind Neb. Rev. Stat. §§ 60-3,185, 60-3,189, 77-202.23, 77-202.24, 011 Honorably Discharged 77-202.25, and 77-702. Veteran Exemption Educational, Religious, Neb. Rev. Stat. §§ 77-202, and 77-702. 005 Charitable, and Cemetery Property Tax Exemptions General Rules Applicable to Neb. Rev. Stat. §§ 77-202, and 77-702. 002 Property Tax Exemptions Governmental Property Tax Neb. Rev. Stat. §§ 77-202, and 77-702. 003 Exemptions Motor Vehicle Tax Neb. Rev. Stat. §§ 60-3,189, 77-702, and 77-5013. 010 Exemptions Pre-existing Tax Liens on Neb. Rev. Stat. §§ 25-1555, 77-702, 77-1737, and 77-1862. 008 Tax Exempt Property Property Transfers or Use Neb. Rev. Stat. §§77-202, 77-202.03, and 77-702. 007 Conversions During Tax Year Public Notice of Property Neb. -

GENERAL A< TARIFFS and TRADE

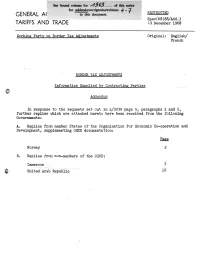

See bound volume for *S(sP*$ of this series for addenda/corrigenda/revisions // _ 2? RESTRICTED GENERAL A< to this document. Spec(68)88/Add.3 TARIFFS AND TRADE 19 December 1968 Working Party on Border Tax Adjustments Original: English/ French BOEDER TAX ADJUSTMENTS Information Supplied by Contracting Parties Addendum In response to the requests S6t out in L/3039 page 5, paragraphs 1 and 2, further replies which are attached hereto have been r6C6iv6d from th6 following Governments: • - A. Replies from member States of th6 Organisation for Economic Co-operation and Development, supplementing OECD documentation: Page Norway 2 - B. Replies from non-members of the OECD: Cameroon 5 United Arab Republic -^ Spec(68)88/Add.3 Page 2 Annex I NORWAY A. The following corrections should be made to the OEGD Pact-Finding Report (OBCD document C (68) 47): Part I £ggg_Ji: Norway should be mentioned under paragraph 20(c). Producers' goods are taxable in Norway. Page 13; Norway should be deleted from.paragraph 28. Only certain services are taxable. Reference is made to Part III, page 41. Page 39: Norway should be added to the list of countries under paragraph 93(a), but deleted from 93(b). As indicated above producers' goods ar6 taxable, but no adjustments are made at the border for this tax. Part III Page 42: As from 1 January 1968 the excise duty on articles of silver was reduced to 7.5 per cent. A proposal has been made, to the Storting to abolish as from 1 January 1969 the excise duty on articles of platinum, gold and silver as well as on imitation jewellery. -

Repealed Taxes and Fees

Repealed Taxes and Fees Overview and Table of Contents This section summarizes the state's transportation repealed taxes and fees. The taxes and fees in this section are arranged in alphabetical order. For the statewide motor vehicle excise tax, refer to the supplementary information following the general description of the tax. Repealed Taxes and Fees ................................................................................................ 287 Aircraft Pilot Registration Fee .............................................................................................. 288 Airman/Airwoman Registration Fee ..................................................................................... 289 Centennial License Plates ..................................................................................................... 290 Clean Air Excise Tax ............................................................................................................ 291 Mobile Home/Travel Trailer Dealer Excise Tax .................................................................. 292 Motor Vehicle Excise Tax (MVET), Statewide and Local ................................................... 293 Historical MVET Distributions ............................................................................................. 297 Motor Vehicle License Fee ................................................................................................... 298 Travel Trailer and Camper Excise Tax ................................................................................ -

The Uneasy Case for Equalization Payments

The Uneasy Case for Equalization Payments The Uneasy Case for Equalization Payments Dan Usher The Fraser Institute Vancouver, British Columbia Copyright © 1995 by The Fraser Institute. All rights reserved. No part of this book may be reproduced in any manner whatsoever without writ- ten permission except in the case of brief quotations embodied in critical articles and reviews. The author of this book has worked independently and opinions ex- pressed by him, therefore, are his own, and do not necessarily reflect the opinions of the members or the trustees of The Fraser Institute. Printed in Canada. Canadian Cataloguing in Publication Data Usher, Dan, 1934- The uneasy case for equalization payments Includes bibliographical references. ISBN 0-88975-153-6 1. Fiscal Equalization Program (Canada)—Evaluation. 2. Federal-provincial fiscal relations—Canada.* 3. Transfer payments—Canada. 4. Grants-in-aid—Canada. I. Fraser Institute (Vancouver, B.C.) II. Title HJ795.A1U73 1995 339.5’22 C95-911122-0 www.fraserinstitute.org Table of Contents About the author ..................vi Foreword by Michael A. Walker ...........vii Introduction .....................1 Part I: From Section 36(2) to the Canadian Equalization Formula ............9 Part II: Equality ...................27 Part III: Efficiency ..................61 Part IV: Equity ...................97 Part V: Reform ...................117 Endnotes .....................131 Appendix Tables ..................151 www.fraserinstitute.org About the author AN USHER IS A PROFESSOR of economics at Queen’s University in DKingston, Ontario. He is the author of The Price Mechanism and the Meaning of National Income Statistics (1969), The Measurement of Economic Growth (1980), The Economic Prerequisite to Democracy (1981), The Welfare Economics of Markets, Voting and Predation (1993) and two volumes of col- lected papers, National Accounting and Economic Theory and Welfare Eco- nomics and Public Finance (1994). -

Internationale Unternehmensbesteuerung

Internationale Unternehmensbesteuerung Deutsche Investitionen im Ausland. Ausländische Investitionen im Inland Bearbeitet von Prof. (em.) Dr. Dr. h.c. mult. Otto H. Jacobs, Prof. Dr. Dieter Endres, Prof. Dr. Christoph Spengel, Prof. Dr. Andreas Oestreicher, Prof. Dr. Andreas Schumacher, Hannah Nusser, Dr. Pia Dorfmüller, Dr. Barbara Zuber 8. Auflage 2016. Buch. Rund 1650 S. In Leinen ISBN 978 3 406 67941 4 Format (B x L): 14,1 x 22,4 cm Steuern > Internationales Steuerrecht Zu Leseprobe und Inhaltsverzeichnis schnell und portofrei erhältlich bei Die Online-Fachbuchhandlung beck-shop.de ist spezialisiert auf Fachbücher, insbesondere Recht, Steuern und Wirtschaft. Im Sortiment finden Sie alle Medien (Bücher, Zeitschriften, CDs, eBooks, etc.) aller Verlage. Ergänzt wird das Programm durch Services wie Neuerscheinungsdienst oder Zusammenstellungen von Büchern zu Sonderpreisen. Der Shop führt mehr als 8 Millionen Produkte. Druckerei C. H . Beck Jacobs: Internationale Unternehmensbesteuerung Medien mit Zukunft ..................................... Erstversand, 30.11.2015 Stichwortverzeichnis 1519 Stichwortverzeichnis Stichwortverzeichnis Stichwortverzeichnis Erstversand Die Ziffern bedeuten Seitenzahlen. Abgeltungsteuer 40, 46, 50 f., 135, – Dilutierungsmodell 1197 ff. 139, 140, 141, 142 f., 146, 429, 899, – Holding-Kapitalgesellschaft 932, 975, 1150, 1188, 1254 f., 1329 1199 ff. Abkommen über den Euro- – Holding-Personengesellschaft päischen Wirtschaftsraum 112 1201 ff. Abkommen über soziale Sicher- – Joint-Venture-Modell, heit 1354 ff. s. Dilutierungsmodell Abrechnungsgrundsätze – Optionsmodell 1198 f. – Betriebsstätte 542 f., 546 f., 630 f., – share deal, s. Akquisitionsmodelle, 761 ff., 797 ff. Inbound, Beteiligungserwerb – Direktgeschäfte 542, 546 f., 628, 638 ff. – Terminkauf 1197 ff. – Kapitalgesellschaft 543 ff., 547, – Vermögenserwerb 1192 ff., 628 ff., 644 ff. 1203 f. – Personengesellschaft 826 ff. – Outbound Abschirmwirkung 399, 405, 416, – asset deal, s. -

Tax Equalization Policy

Tax Equalization Policy www.theresforum.com This document is copyrighted ©. All rights reserved. This document is for the use of the purchaser only. Any redistribution or reproduction of part or all of the contents in any form is prohibited. You may not distribute or commercially exploit the content. Nor may you transmit it or store it in any other website or other form of electronic retrieval system. TAX EQUALIZATION POLICY Contents 1 Introduction 5 1.1 What is Tax Equalization? 5 1.2 Objectives 5 1.3 Scope 6 2 Definitions 8 3 Employee Company Income Tax Withholding 9 3.1 Estimated Hypothetical Tax Deduction and Tax Year End Equalization Calculation 9 3.2 Home Country Tax Return Calculation and Tax Year-End Equalization Calculation 10 3.3 Hypothetical Tax and Social Taxes 10 3.4 Employee Voluntary Pension Related Social Security Contribution 11 4 Treatment of Income 13 4.1 Income Subject to Equalization 13 4.2 Incomes included in Hypothetical Tax Calculation 13 4.3 Income included in Tax Equalization Settlement Calculations 14 4.4 Income Not Subject to Equalization 15 5 Actions Resulting in Potentially Higher Tax Costs to Assignee 17 5.1 Transferring Income into the Host Country 17 5.2 Sale of a Principal Residential Property 17 5.3 Inheritance of Estate 17 5.4 Stock Activity 18 5.5 Financial Investing in the Host Location 18 5.6 Remaining in Host Country after agreed Repatriation Date 18 5.7 Severance Payments 19 6 Responsibilities 20 6.1 Responsibilities of the Employee 20 6.2 Responsibilities of the Employer 21 6.3 Responsibilities of the Tax Advisers 22 6.4 Filing Positions 23 6.5 Filing State/Provincial/Cantonal Return 23 6.6 Payment of Host Country Income/Social Tax 23 6.7 Foreign Tax Credits 24 6.8 Penalties and Interest Fees 25 6.9 Deductions from Payroll 25 1 Introduction The purpose of this document is to explain the concept of tax equalization, why [Global Company Name] has a tax equalization policy and how the policy will be implemented. -

Working Paper PEIF-3 Tax Reforms and “Modell Deutschland”

1 Working Paper PEIF-3 Tax Reforms and “Modell Deutschland”: Lessons from Four Years of Red-Green Tax-Policy by Achim Truger and Wade Jacoby December 9, 2002 Abstract When the red-green (SPD-Bündnis90/DieGrünen) coalition took over the federal government from the Christian-Democrat/Free-Democrat (CDU/CSU/FDP) coalition in 1998, tax reforms had a very high political priority. And, in fact, the government pushed through an astonishing number of far-reaching tax reforms/tax changes within a period of little more than two years. This paper follows two aims. First, it gives a short description of the measures taken and evaluates them with respect to tax theory and the German tax reform debate of the 1990s. Second, it explicitly addresses the question whether the tax changes were influenced by the wish to reform the Modell Deutschland, i.e. whether something substantial was done to change Germany´s status as a perceived high tax country and if so, whether the attempt was successful. It will be shown that even though the problem of high taxes might have been many observers´ and, indeed, also the government´s dominant concern, there was much more to the German debate. The chapter will also ask whether generously cutting taxes was the right thing to do. It demonstrates that under Germany´s peculiar economic and institutional circumstances at the end of the 1990s, the attempt to cut taxes led to serious problems for fiscal policy, growth, and employment. 2 Tax Reforms and “Modell Deutschland”: * Lessons from Four Years of Red-Green Tax-Policy Achim Truger and Wade Jacoby 1. -

Worldwide R&D Incentives Reference Guide

Worldwide R&D Incentives Reference Guide 2020 Preface R&D incentives boom in 2020 and beyond Tax competition — driven by governments vying to attract and sustain economic activity in their jurisdiction — drove much global tax change in 2019 and is expected to generate even more in 2020. As countries formulate plans to reinvigorate their economies in the wake of COVID-19, we expect many to implement new, expanded or specially focused research and development (R&D) incentive programs. As you review particular jurisdictions, please note many of these programs will have been introduced after the data collection deadlines for this Guide. Therefore, not only do we strongly recommend you review EYs Global COVID-19 Response Tracker for the very latest program launches and changes, but we also recommend you speak to your EY Tax representatives for up-to-date information. According to EY’s annual Global outlook for tax policy, 2019 was another relative boom year for R&D incentives with over a third of responding jurisdictions making their R&D incentives more favorable. This trend could be explained by the fact that countries found themselves constrained by the Organisation for Economic Co-operation and Development’s base erosion and profit shifting (BEPS) recommendations, but at the same time, wanting to maintain or improve their competitive position. Similarly, a third of reporting jurisdictions are also incentivizing wider business investment via improved capital and other incentives and allowances, depreciation and amortization. Even better, 11 jurisdictions (Finland, Germany, Indonesia, Japan, Korea, Malaysia, New Zealand, Poland, Slovakia, Switzerland and the United Kingdom) are reducing the tax burden on companies by both creating or improving R&D incentives and other business incentives simultaneously. -

IRS Publication 54: Tax Guide for U.S. Citizens and Resident Aliens Abroad

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 8 Draft Ok to Print AH XSL/XML Fileid: … ations/P54/2020/A/XML/Cycle08/source (Init. & Date) _______ Page 1 of 36 6:32 - 16-Dec-2020 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing. Publication 54 Cat. No. 14999E Contents What's New .................. 2 Department of the Tax Guide for Reminders ................... 2 Treasury Internal Introduction .................. 2 Revenue U.S. Citizens Service Chapter 1. Filing Information ....... 3 Filing Requirements ........... 3 and Resident Nonresident Alien Spouse Treated as a Resident ........ 7 Estimated Tax .............. 8 Aliens Abroad Other Forms You May Have To File ................... 8 Chapter 2. Withholding Tax ........ 8 For use in preparing Income Tax Withholding ........ 8 30% Flat Rate Withholding ....... 9 Social Security and Medicare 2020 Returns Taxes ................. 9 Chapter 3. Self-Employment Tax .... 11 Who Must Pay Self-Employment Tax? ................. 11 Exemption From Dual-Country Social Security and Medicare Taxes .......... 11 COVID-19 Emergency Relief for Self-Employed Individuals ..... 12 Chapter 4. Foreign Earned Income and Housing: Exclusion – Deduction ............... 12 Who Qualifies for the Exclusions and the Deduction? ........ 12 Requirements .............. 12 Waiver of Time Requirements .... 16 COVID-19 Emergency Relief ..... 16 Foreign Earned Income Exclusion .............. 20 Foreign Housing Exclusion and Deduction .............. 22 Form 2555 ............... 23 Chapter 5. Deductions and Credits .............. 24 Items Related to Excluded Income ............... 24 Contributions to Foreign Charitable Organizations ..... 24 Contributions to Individual Retirement Arrangements ..... 24 Taxes of Foreign Countries and U.S. Territories ........... 24 How To Report Deductions ...... 26 Chapter 6. Tax Treaty Benefits ..... 26 Purpose of Tax Treaties .......