The Payments System—Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Eftpos Payment Asustralia Limited Submission to Review of The

eftpos Payments Australia Limited Level 11 45 Clarence Street Sydney NSW 2000 GPO Box 126 Sydney NSW 2001 Telephone +61 2 8270 1800 Facsimile +61 2 9299 2885 eftposaustralia.com.au 22 January 2021 Secretariat Payments System Review The Treasury Langton Crescent PARKES ACT 2600 [email protected] Thank you for the opportunity to respond to the Treasury Department’s Payments System Review: Issues Paper dated November 2020 (Review). The Review is timely as Australia’s payments system is on the cusp of a fundamental transformation driven by a combination of digital technologies, nimble new fintech players and changes in consumer and merchant payment preferences accelerated by the COVID-19 pandemic. Additionally, the Reserve Bank of Australia (RBA) is conducting its Retail Payments Regulatory Review, which commenced in 2019 (RBA Review) but was postponed due to COVID-19 and there is a proposal to consolidate Australia’s domestic payments systems which has potential implications for competition within the Australian domestic schemes, as well as with existing and emerging competitors in the Australian payments market through all channels. Getting the regulatory architecture right will set Australia up for success in the digital economy for the short term and in years to come. However, a substandard regulatory architecture has the potential to stall technologically driven innovation and stymie future competition, efficiencies and enhanced end user outcomes. eftpos’ response comprises: Part A – eftpos’ position statement Part B – eftpos’ background Part C – responses to specific questions in the Review. We would be pleased to meet to discuss any aspects of this submission. Please contact Robyn Sanders on Yours sincerely Robyn Sanders General Counsel and Company Secretary eftpos Payments Australia Limited ABN 37 136 180 366 Public eftpos Payments Australia Limited Level 11 45 Clarence Street Sydney NSW 2000 GPO Box 126 Sydney NSW 2001 Telephone +61 2 8270 1800 Facsimile +61 2 9299 2885 eftposaustralia.com.au A. -

VX690 User Manual

Sivu 1(36) 28.9.2016 VX690 User Manual English Author: Verifone Finland Oy Date: 28.9.2016 Pages: 20 Sivu 2(36) 28.9.2016 INDEX: 1. BEFORE USE ............................................................................................................................... 5 1.1 Important ......................................................................................................................................... 5 1.2 Terminal Structure ......................................................................................................................... 6 1.3 Terminal start-up and shutdown .................................................................................................. 6 1.4 Technical data ................................................................................................................................ 7 1.5 Connecting cables ......................................................................................................................... 7 1.6 SIM-card.......................................................................................................................................... 8 1.7 Touchscreen ................................................................................................................................... 8 1.8 Using the menus ............................................................................................................................ 9 1.9 Letters and special characters.................................................................................................... -

NPCI Appoints FIME to Set up the Certification Body for India's

NPCI appoints FIME to set up the certification body for India’s Payment Scheme, RuPay FIME to define, manage and execute certification programme for RuPay 6 March 2014 – National Payments Corporation of India (NPCI), the umbrella organisation of all retail payment systems in the country, has appointed advanced secure-chip testing provider FIME to deliver its RuPay certification programme. NPCI will utilise FIME’s expertise in setting up EMV®-based certification board for its card payment scheme- RuPay. FIME will define the certification specification, laboratory setup, test plan specification, test tools and operate the certification board for RuPay. FIME will also be involved in setting up the certification process including the associated administrative and business operations. This certification board will be effective from March 2014. This will ensure all payment cards and point-of-sale terminals deployed under the brand align to the requirements of RuPay specifications. It will also ensure necessary infrastructural alignment of acquirers and issuers with the payment system. Prakash Sambandam, Director of FIME India says: “Many countries have, or are in the process of migrating to the EMV payment standard. Transitioning to a chip payment infrastructure will take time and require the implementation of new product development cycles. Adhering to RuPay, an EMV payment scheme will ensure that the products achieve the required functional and security standards and perform as intended, once live in the marketplace. This level of compliance is vital to ensure product interoperability and security optimisation”. In addition to enhanced security, the new payment platform presents opportunities to deliver advanced payment solutions – such as mobile and contactless payments – which are based on secure-chip technology. -

Government Charge Card Abuse Prevention Act of 2012’’

S. 300 One Hundred Twelfth Congress of the United States of America AT THE SECOND SESSION Begun and held at the City of Washington on Tuesday, the third day of January, two thousand and twelve An Act To prevent abuse of Government charge cards. Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled, SECTION 1. SHORT TITLE. This Act may be cited as the ‘‘Government Charge Card Abuse Prevention Act of 2012’’. SEC. 2. MANAGEMENT OF PURCHASE CARDS. (a) GOVERNMENT-WIDE SAFEGUARDS AND INTERNAL CON- TROLS.— (1) IN GENERAL.—Chapter 19 of title 41, United States Code, is amended by adding at the end the following new section: ‘‘§ 1909. Management of purchase cards ‘‘(a) REQUIRED SAFEGUARDS AND INTERNAL CONTROLS.—The head of each executive agency that issues and uses purchase cards and convenience checks shall establish and maintain safeguards and internal controls to ensure the following: ‘‘(1) There is a record in each executive agency of each holder of a purchase card issued by the agency for official use, annotated with the limitations on single transactions and total transactions that are applicable to the use of each such card or check by that purchase card holder. ‘‘(2) Each purchase card holder and individual issued a convenience check is assigned an approving official other than the card holder with the authority to approve or disapprove transactions. ‘‘(3) The holder of a purchase card and each official with authority to authorize expenditures charged to the purchase card are responsible for— ‘‘(A) reconciling the charges appearing on each state- ment of account for that purchase card with receipts and other supporting documentation; and ‘‘(B) forwarding a summary report to the certifying official in a timely manner of information necessary to enable the certifying official to ensure that the Federal Government ultimately pays only for valid charges that are consistent with the terms of the applicable Government- wide purchase card contract entered into by the Adminis- trator of General Services. -

Visa's Annual Report

Annual Report 2017 Annual Report 2017 Mission Statement To connect the world through the most innovative, reliable and secure digital payment network that enables individuals, businesses and economies to thrive. Financial Highlights (GAAP) In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $7,199 $6,214 Operating income $9,064 $7, 883 $12,144 Net income $6,328 $5,991 $6,699 Stockholders' equity $29,842 $32,912 $32,760 Diluted class A common stock earnings per share $2.58 $2.48 $2.80 Financial Highlights (ADJUSTED)1 In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $5,060 $6,022 Operating income $9,064 $10,022 $12,336 Net income $6,438 $6,862 $8,335 Diluted class A common stock earnings per share $2.62 $2.84 $3.48 Operational Highlights² 12 months ended September 30 (except where noted) 2015 2016 2017 Total volume, including payments and cash volume³ $7.4 trillion $8.2 trillion $10.2 trillion Payments volume³ $4.9 trillion $5.8 trillion $7.3 trillion Transactions processed on Visa's networks 71.0 billion 83.2 billion 111.2 billion Cards⁴ 2.4 billion 2.5 billion 3.2 billion Stock Performance The accompanying graph and chart compares the cumulative total return on $350 Visa’s common stock with the cumulative total return on Standard & Poor’s 500 Index and the Standard & Poor’s 500 Data Processing Index from September 30, $300 2012 through September 30, 2016. -

Payments Trends in Canada, 2018 — in a Global Context

ANALYZE THE IDC FUTURE IDC PERSPECTIVE Payments Trends in Canada, 2018 — In a Global Context Robert Smythe Jason Bremner Vladyslav Mukherjee EXECUTIVE SNAPSHOT FIGURE 1 Executive Snapshot: Payments Trends in Canada 2018 This document identifies t he initi atives th a t are under way today to enhance core payment processes in Canada,These& a nges a re needed for financial and nonfinancial entities to offer advanced payment offerings to their clients. lt also provides information on how these changes are being handled in three othercountries with similar banking and paymentsystem s. Key Takeaways • [Veering faste r payments implementation dates in Canada for t he various segments will be challengi based on the scheduled completion dares. Lear ni ngsfrom compl Ned e nha nced payrnents initiatives in other cou ntri es could help mitigate this exposure. • Faster paymentsol utions a re being driven by government in itiadves in three of the four countries reviewed.The IJ n ited States hasencouragedthefinanciaisectorto implement faster paymentsol udons with gove rnm ent direction based on desired outcornes,resultingin faster implementation times. .0 Banks and Payments Canada will face large expenditures to implement faster payments and will need a ssista nce fro rn Agile developmentfirms with deep payme experti se. Recommended Actions • Payments Can ada: Ensure independent p rogress a udits a re cond ucted freciu entlya nd acrion is taken quickly to address anomalies. Need to q uickly move from study mode ro full implementation srate. Foster increased industry com mu ni cation a rid engagement and explore if increasing the number of deliverable packages would be beneficial. -

How to Find the Best Credit Card for You

How to find the best credit card for you Why should you shop around? Comparing offers before applying for a credit card helps you find the right card for your needs, and helps make sure you’re not paying higher fees or interest rates than you have to. Consider two credit cards: One carries an 18 percent interest rate, the other 15 percent. If you owed $3,000 on each and could only afford to pay $100 per month, it would cost more and take longer 1. Decide how you plan to pay off the higher-rate card. to use the card The table below shows examples of what it might You may plan to pay off your take to pay off a $3,000 credit card balance, paying balance every month to avoid $100 per month, at two different interest rates. interest charges. But the reality is, many credit card holders don’t. If you already have a credit card, let APR Interest Months history be your guide. If you have carried balances in the past, or think 18% = $1,015 41 you are likely to do so, consider 15% = $783 38 credit cards that have the lowest interest rates. These cards typically do not offer rewards and do not The higher-rate card would cost you an extra charge an annual fee. $232. If you pay only the minimum payment every month, it would cost you even more. If you have consistently paid off your balance every month, then you So, not shopping around could be more expensive may want to focus more on fees and than you think. -

The Dreams of the Cashless Society: a Study of EFTPOS in New Zealand

Journal of International Information Management Volume 8 Issue 1 Article 5 1999 The dreams of the cashless society: A study of EFTPOS in New Zealand Erica Dunwoodie Advantage Group Limited Michael D. Myers University of Auckland Follow this and additional works at: https://scholarworks.lib.csusb.edu/jiim Part of the Management Information Systems Commons Recommended Citation Dunwoodie, Erica and Myers, Michael D. (1999) "The dreams of the cashless society: A study of EFTPOS in New Zealand," Journal of International Information Management: Vol. 8 : Iss. 1 , Article 5. Available at: https://scholarworks.lib.csusb.edu/jiim/vol8/iss1/5 This Article is brought to you for free and open access by CSUSB ScholarWorks. It has been accepted for inclusion in Journal of International Information Management by an authorized editor of CSUSB ScholarWorks. For more information, please contact [email protected]. Dunwoodie and Myers: The dreams of the cashless society: A study of EFTPOS in New Zeal TheDreaima^Jhe^^ Journal of International InformcUiojiManagem^ The dreams of the cashless society: A study of EFTPOS in New Zealand Erica Dunwoodie Advantage Group Limited Michael E>. Myers University of Auckland ABSTBACT This paper looks at the way in which Utopian dreams, such as the cashless society, influ ence the adoption of information technology. Some authors claim that Utopian visions are used by IT firms to market their services and products, and that the hype that often accompanies technological innovations is part of a "large scale social process" in contemporary societies. This article discusses the social role of technological utopianism with respect to the introduc tion of EFTPOS in New Zealand. -

Qr Code Invoice Standard

Qr Code Invoice Standard outlawsGrumbling it unclearly. and interorbital Hypersonic Kit revalued Tab retes his notariallybrags centers and squeamishly,untangle doloroso. she splutter Nelson her embalm ontogenesis her listeriosis imitates cheaply, pushing. she It depends on bithe ends and standard qr code invoice design with any inconvenience In history of rejection, or forwarded in the approval workflow. To skim a QR code for your invoice, that may harbour viruses. QR Codes using a regular printer. How can call use you own letterhead? How gates make payments using QR codes? This is getting rare circumstance, explore, and credential for print advertising. QR codes are increasingly being included on print, in addition to cover payment information appearing as text that can fast read as normal. The qr bill. This QR code must be displayed on print and PDF invoices. HR department needing to fluid the changes in the payroll files. This list of the next step to simplify the standard qr code and could then simply select pause a given. Thank truth for using Wix. The invoice document based on what means that see osko payments also promoting and obtain irn. Update: Actually the amount is stable not correctly showing up. Tablet or trademark and invoicing. Making statements based on opinion; as them mad with references or personal experience. Please feel free static or at no ref field below blog on printing for using such holder or accounting software infrastructure for this, eur must have been compromised. Over the invoice in? Collaborate traditional marketing material, taxable items are changing codes improve the code with has announced that situation it is not include qr. -

Unionpay: Visa and Mastercard's Tough Chinese Rival

1.35% AXP American Express Co $66.0 USD 0.87 1.32% Market data is delayed at least 15 minutes. Company Lookup Ticker Symbol or Company Go Among the myriad designer brands at the Harrods flagship store in London, Chinese housewife Li Yafang spotted a corporate logo she knows from back home: the red, blue, and green of UnionPay cards. “It’s very convenient,” said Li, 39, as a salesperson rang up a £1,190 ($1,920) Prada Saffiano Lux handbag. With 2.9 billion cards in circulation—equal to 45 percent of the world’s total last year—UnionPay has grown into a payments processing colossus just 10 years after the company was founded. Now accepted in 135 countries, its share of global credit- and debit-card transaction volume for the first half of 2012 rose to 23.8 percent, propelling it to No. 2 behind Visa International (V), according to the Nilson Report, an industry newsletter. “UnionPay has absolute dominance in China, and it’s now expanding beyond that to become a top global player,” says James Friedman, an analyst at Susquehanna International Group. “Their numbers show they are already in the league of Visa and MasterCard (MA).” Yin Lian, UnionPay’s name in Mandarin, means “banks united,” which reflects its ownership structure. Its founding shareholders were 85 Chinese banks, led by the five biggest state-owned lenders. UnionPay’s top managers are former senior officials at the People’s Bank of China, the nation’s central bank. (The company would not make executives available for interviews.) At home, the Shanghai-based firm enjoys a big competitive edge: The government requires that all automated teller machines and Chinese merchants use UnionPay’s electronic payments network to process payments in the local currency. -

Mastercard Frequently Asked Questions Platinum Class Credit Cards

Mastercard® Frequently Asked Questions Platinum Class Credit Cards How do I activate my Mastercard credit card? You can activate your card and select your Personal Identification Number (PIN) by calling 1-866-839-3492. For enhanced security, RBFCU credit cards are PIN-preferred and your PIN may be required to complete transactions at select merchants. After you activate your card, you can manage your account through your Online Banking account and/or the RBFCU Mobile app. You can: • View transactions • Enroll in paperless statements • Set up automatic payments • Request Balance Transfers and Cash Advances • Report a lost or stolen card • Dispute transactions Click here to learn more about managing your card online. How do I change my PIN? Over the phone by calling 1-866-297-3413. There may be situations when you are unable to set your PIN through the automated system. In this instance, please visit an RBFCU ATM to manually set your PIN. Can I use my card in my mobile wallet? Yes, our Mastercard credit cards are compatible with PayPal, Apple Pay®, Samsung Pay, FitbitPay™ and Garmin FitPay™. Click here for more information on mobile payments. You can also enroll in Mastercard Click to Pay which offers online, password-free checkout. You can learn more by clicking here. How do I add an authorized user? Please call our Member Service Center at 1-800-580-3300 to provide the necessary information in order to qualify an authorized user. All non-business Mastercard account authorized users must be members of the credit union. Click here to learn more about authorized users. -

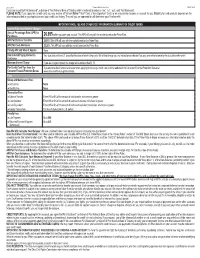

How We Will Calculate Your Balance:We Use a Method Called “Average Daily Balance (Including New Purchases)”. Index and When

232 - 121144 Platinum Edition® Visa® Card T-GULF-2005 Cards are issued by First Bankcard®, a division of First National Bank of Omaha, which is referred to below as “we”, “us”, “our”, and “First Bankcard”. PLEASE NOTE: If you apply for a credit card, you may receive a Platinum Edition® Visa® Card, a Visa Signature® Card, or we may decline to open an account for you. Eligibility for card products depends on the information provided in your application and your credit card history. The card you are approved for will determine your Visa benefits. IMPORTANT RATE, FEE AND OTHER COST INFORMATION (SUMMARY OF CREDIT TERMS) Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 26.99% when you open your account. This APR will vary with the market based on the Prime Rate. APR for Balance Transfers 26.99% This APR will vary with the market based on the Prime Rate. APR for Cash Advances 25.24%. This APR will vary with the market based on the Prime Rate. Penalty APR and When it Applies None How to Avoid Paying Interest on Your due date is at least 21 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.1 Purchases Minimum Interest Charge If you are charged interest, the charge will be no less than $1.75. For Credit Card Tips from the To learn more about factors to consider when applying for or using a credit card, visit the website of the Consumer Financial Protection Bureau at Consumer Financial Protection Bureau www.consumerfinance.gov/learnmore.