Comprehensive Annual Financial Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

20 20 D Ir E C T O Ry

“Helping communities achieve Northeastsuccess Michigan through Council intergovernmental of Governments cooperation and coordination” 2020 DIRECTORY 80 Livingston Blvd, Suite U-108 P.O. Box 457, Gaylord, MI 49734 989.705.3730 Phone 20 989.705.3729 Fax www.discovernortheastmichigan.org 20 Serving the counties of: Alcona, Alpena, Cheboygan, Crawford, Montmorency, Oscoda, Otsego, and Presque Isle Helping communities achieve success through intergovernmental cooperation & coordination” NEMCOG 2020 DIRECTORY Table of Contents NEMCOG Region Map ....................................................................................................... i State Planning and Development Regions ..................................................................... ii Michigan Associations of Regions, Directory of Regions .............................................. iii About MAR ..................................................................................................................... iv About State-Designated Planning & Development Region ........................................... v NEMCOG Board of Directors .......................................................................................... vi NEMCOG Staff Directory ............................................................................................ vii-ix County Road Commissions ......................................................................................... x-xii Alcona County ................................................................................................................ -

Underground Spotlight Page 18

SPRING 2015 Underground Spotlight Page 18 MEMBER PROFILE: ASSOCIATE MEMBER PROFILE: Hoffman Bros., Inc. Hymmco Page 8 Page 12 Lansing, MI Lansing, PERMIT #718 PERMIT PAID P. O. Box 1640, Okemos, MI 48805-1640 MI Okemos, 1640, Box O. P. U.S. POSTAGE U.S. MITA, Michigan Infrastructure & Transportation Association Transportation & Infrastructure Michigan MITA, PRST STD PRST √ √ Call MITA’s Bene ts Consultant! association benets company Authorized Administrator for the Michigan Infrastructure and Transportation Association’s Blue Cross® Blue Shield® of Michigan and Blue Care Network Health Insurance Program Outreach Spotlight The Grassroots Efforts Behind Proposal 1: Paying Tribute To A Job Well Done By Mariam Robinson he Safe Roads YES campaign for lowing companies who invested in either Proposal 1 was not only the tough- large signs for their company buildings or Test in MITA history, but also one of billboards in their area of the state: Ajax the most controversial ballot initiatives to Paving Industries, Inc., Fonson, Inc. and M be seen in Michigan in the last 50 years. We & M Excavating Company. Large signs and must remember that even under the best of billboards are very eye-catching, and they circumstances, ballot campaigns are typi- require a certain level of investment. Thank cally the most difficult to win because of the you for putting in the effort to publicly dis- need to educate the public for support. play your support in the months leading up Though our fight to win the Proposal to the election. 1 campaign was not successful on May The bottom line is that this was a tough 5th, the grassroots efforts of many MITA campaign. -

2019 Emmet County Directory

2019 EMMET COUNTY DIRECTORY -1- I N D E X Page Aging Committee 13 Airport Board of Control 13 Ambulance Advisory Committee 13 Appointed Officials 12 Board of Canvassers 13 Board of Commissioners 11 Board of Commissioner District Areas 11 Brownfield Redevelopment Authority 13 Building Inspection Appeal Board 14 Circuit Court Officers 7 Community Corrections Advisory Board 14 County Boards and Committees 13 Crooked River (Alanson) Locks Consortium 18 Department of Human Services 14 Department of Public Works 14 District Court Officers 8 Economic Development Corporation 15 Elected Officials 10 Election Commission 15 EMS 12 Fair Advisory Council 15 Federal Officials 5 Friend of the Court Referee Hearings 7 Harbor, Inc. 15 Health Department Board 15 Historical Commission 15 Housing Council 16 Jury Commission 16 Jury Terms 7 Lakeview Academy 9 Land Bank Authority 16 Local Casino Revenue Sharing Board 16 Local Emergency Planning Agency 16 Medical Examiner 16 Mental Health Board 16 Northeast/Northwest Michigan Council of Governments 16 Northern Lakes Economic Alliance 17 Northern Michigan Counties Association 17 Northern Michigan Substance Abuse Services 17 Parks & Recreation Committee 17 Planning Commission 17 Plat Board 17 Probate Court Officers 9 Regional Transportation 17 Road Commission 18 SANE 18 Sanitary Code Appeal 18 State Officials 6 Surveyor 18 Telephone Directory 3 Township Clerks 19 Workforce Development Board 18 Zoning Appeal Board 18 -2- TELEPHONE DIRECTORY EMMET COUNTY OFFICES OFFICE HOURS : Monday thru Friday - 8:00 A.M. - 5:00 P.M. Building Department & Planning, Zoning & Construction Resources: Monday thru Friday - 8:00 A.M. - 5:00 P.M. Veterans Affairs Office: Tuesday thru Friday - 9:00 A.M. -

Michigan Supreme Court Chief Justice Bridget Mccormack

MAC Legislative Conference Michigan Supreme Court Chief Justice Bridget M. McCormack April 16, 2020 “Court Reform in Michigan in 2020 and Beyond” CHIEF JUSTICE BRIDGET M. McCORMACK | INDEPENDENCE ∙ ACCESSIBILITY ∙ ENGAGEMENT ∙ EFFICIENCY Today’s Presentation •Judicial Response to COVID-19 Crisis •Jail and Pretrial Reform •Trial Court Funding Commission Report •Juvenile Justice •Q & A CHIEF JUSTICE BRIDGET M. McCORMACK | INDEPENDENCE ∙ ACCESSIBILITY ∙ ENGAGEMENT ∙ EFFICIENCY “When restaurants close, the public is urged to pick up takeout. But there is no such thing as takeout justice. While courts can postpone routine matters (like traffic tickets), judges and court staff must continue to provide essential services and protect public safety.” CHIEF JUSTICE BRIDGET M. McCORMACK | INDEPENDENCE ∙ ACCESSIBILITY ∙ ENGAGEMENT ∙ EFFICIENCY Essential Court Functions • Protecting vulnerable people • Hearings and arraignments for criminal defendants • Proceedings related to quarantine and other public health matters • Personal protection orders • Search warrants and other law enforcement actions CHIEF JUSTICE BRIDGET M. McCORMACK | INDEPENDENCE ∙ ACCESSIBILITY ∙ ENGAGEMENT ∙ EFFICIENCY Judicial Response to COVID-19 • First step was a web page dedicated to the crisis • Series of administrative orders targeted to slow the spread of COVID-19 • Guidance regarding essential functions • Detailed FAQS • Virtual Courtroom Resources CHIEF JUSTICE BRIDGET M. McCORMACK | INDEPENDENCE ∙ ACCESSIBILITY ∙ ENGAGEMENT ∙ EFFICIENCY Michigan Virtual Courtroom Task -

Analysis of 2016 General Election

Analysis of 2016 General Election On Tuesday, November 8, voters cast their ballot to decide a number of national, state, and local races and issues. While the results are in, the work needed to create a better society is not finished. It is important that we each seek to heal divisions, pray for elected officials, and engage with them about issues facing our nation, state, and local communities. Archbishop Joseph Kurtz of Louisville, the president of the U.S. Conference of Catholic Bishops (USCCB), congratulated President-Elect Donald Trump and others who were chosen by the American people on November 8th. He also issued a statement calling for all to work for the common good. The following analysis provides an overview of the results in the race for President, the U.S. House of Representatives, the State House of Representatives, the Michigan Supreme Court, and the State Board of Education. The Michigan State University Board of Trustees, University of Michigan Regents, and the Wayne State University Governors are also included as they are decided by voters at the statewide ballot. This piece will also take a look at the political landscape in Michigan going forward. Trump/Pence Win 75 of Michigan’s 83 Counties At the end of the night and early into the hours of Wednesday, November 9, Michigan proved to be a battleground state in the presidential election, defying polls that suggested Hillary Clinton had a significant lead. In fact, the Detroit Free Press mistakenly called Michigan for Secretary Clinton as early as 9 pm. Unofficial results from the Michigan Secretary of State show that Donald Trump narrowly won Michigan with a total of 2,277,914 votes out of 4,785,223 (47.60%) compared to Clinton’s 2,264,807 (47.33%). -

A Citizen's Guide to Michigan Campaign Finance 2014 Big Money Dominates Michigan Politics

A Citizen’s Guide to Michigan Campaign Finance 2014 Big Money Dominates Michigan Politics The Michigan Campaign Finance Network is a nonprofit, nonpartisan organization that conducts research and provides public education on money in Michigan politics. Board of Directors John R. Chamberlin Jan C. Dolan Patricia L. Donath John M. Koval H. Lynn Jondahl John P. Mayer Alma Wheeler Smith John J. H. Schwarz Rich Robinson, Executive Director © October 2015 Michigan Campaign Finance Network Data and information may be used for public education with attribution. This report was researched and written by Rich Robinson. The work of the Michigan Campaign Finance Network is sustained by voluntary contributions from concerned Michigan citizens. This project was made possible by the Mariel Foundation. Michigan Campaign Finance Network 600 W. St. Joseph, Suite 3G, Lansing, MI 48933 Phone: (517) 482-7198 | Email: [email protected] | Website: www.mcfn.org Table of Contents Forward �������������������������������������������������������������������������������������������������������������������������������������� 5 Federal Overview ����������������������������������������������������������������������������������������������������������������������� 6 Federal Contribution Limits 8 U� S� House of Representatives - Michigan���������������������������������������������������������������������������� 9 Primary Elections 9 General Elections 11 U� S� Senate - Michigan ���������������������������������������������������������������������������������������������������������� -

House of Representatives 98Th Legislature REGULAR SESSION of 2015

No. 1 STATE OF MICHIGAN JOURNAL OF THE House of Representatives 98th Legislature REGULAR SESSION OF 2015 House Chamber, Lansing, Wednesday, January 14, 2015. 12:00 Noon. Pursuant to the requirements of the Constitution, the Representatives-elect to the House of Representatives of the State of Michigan for the years 2015 and 2016, assembled in Representative Hall in the Capitol at Lansing on the second Wednesday in January, the 14th of January, 2015 at 12:00 o’clock noon, and in accordance with law, were called to order by Gary L. Randall, Clerk of the preceding House. Rep. Ed McBroom, from the 108th District, offered the following invocation: “Dear Father, I come before You today, with this assembly, to ask for Your mercy. Too often, it is correct to say we have forgotten You. Please have mercy on the members of this house and the people of our state. We have all failed to recognize Your claim for our complete and total worship. We have taken for granted the amazing blessings You have long bestowed on us as if we ourselves had created the bounty of the earth, the blessings of babies, the joys of living, and the honor of age. We have assumed to ourselves the credit for our successes and the benefits of our work all while ignoring or even repudiating the fruits of our sins. The terrors and sorrows all of our society experiences we dismiss as having no connection to our own failure to acknowledge You. Yet You have well described our human state so well in the scriptures: ‘God is not mocked. -

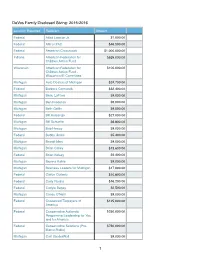

Devos Giving Tracking

DeVos Family Disclosed Giving: 2015-2016 Location Reported Recipient Amount Federal Alfed Lawson Jr. $1,000.00 Federal Alticor PAC $46,500.00 Federal American Crossroads $1,000,000.00 Indiana American Federation for $525,000.00 Children Action Fund Wisconsin American Federation for $100,000.00 Children Action Fund - Wisconsin IE Committee Michigan Auto Dealers of Michigan $24,700.00 Federal Barbara Comstock $32,400.00 Michigan Beau LaFave $9,000.00 Michigan Ben Frederick $9,000.00 Michigan Beth Griffin $9,000.00 Federal Bill Huizenga $27,000.00 Michigan Bill Schuette $6,800.00 Michigan Bob Howey $9,000.00 Federal Bobby Jindal $5,400.00 Michigan Brandt Iden $9,000.00 Michigan Brian Calley $13,600.00 Federal Brian Kelsey $5,400.00 Michigan Bronna Kahle $9,000.00 Michigan Business Leaders for Michigan $17,000.00 Federal Carlos Curbelo $10,800.00 Federal Carly Fiorina $16,200.00 Federal Carlyle Begay $2,500.00 Michigan Casey O’Neill $9,000.00 Federal Concerned Taxpayers of $125,000.00 America Federal Conservative Authentic $250,000.00 Responsive Leadership for You and for America Federal Conservative Solutions (Pro- $750,000.00 Marco Rubio) Michigan Curt VanderWall $9,000.00 !1 Location Reported Recipient Amount Michigan Daire Rendon $9,000.00 Michigan Daniela Garcia $9,000.00 Federal Darren Soto $2,700.00 Federal David Brat $12,800.00 Federal David Trott $8,000.00 Michigan David Viviano $22,500.00 Michigan Diana Farrington $9,000.00 Missouri Eric Greitens $100,000.00 Indiana Eric Holcomb $95,000.00 Federal ESAFUND $100,000.00 Michigan FOWB -

County Directory CONTENTS

2020 County Directory CONTENTS EMMET COUNTY OFFICES . 3 FEDERAL OFFICES . 4 STATE OFFICES . 5 57TH CIRCUIT COURT OFFICERS . 6 90TH DISTRICT COURT OFFICERS . 7 7TH DISTRICT PROBATE OFFICERS . 8 LAKEVIEW ACADEMY . 8 COUNTY ELECTED OFFICIALS . 9 COUNTY COMMISSIONERS . 10 COMMISSIONER DISTRICTS . 10 COUNTY APPOINTED OFFICIALS . 11 COUNTY BOARDS AND COMMITTEES . 12-18 CLERKS - TOWNSHIPS/CITIES/VILLAGES . 19 CITY OF HARBOR SPRINGS INFO . 20 CITY OF PETOSKEY INFO . 21 BEAR CREEK TOWNSHIP INFO . 22 BLISS TOWNSHIP INFO . 23 CARP LAKE TOWNSHIP INFO . 24 CENTER TOWNSHIP INFO . 25 CROSS VILLAGE TOWNSHIP INFO . 26 FRIENDSHIP TOWNSHIP INFO . 27 LITTLEFIELD TOWNSHIP INFO . 28 LITTLE TRAVERSE TOWNSHIP INFO . 29 MAPLE RIVER TOWNSHIP INFO . 30 McKINLEY TOWNSHIP INFO . 31 PLEASANTVIEW TOWNSHIP INFO . 32 READMOND TOWNSHIP INFO . 33 RESORT TOWNSHIP INFO . 34 SPRINGVALE TOWNSHIP INFO . 35 WAWATAM TOWNSHIP INFO . 36 WEST TRAVERSE TOWNSHIP INFO . 37 VILLAGE OF ALANSON INFO . 38 VILLAGE OF MACKINAW CITY INFO . 39 VILLAGE OF PELLSTON INFO . 40 - 2 - DIRECTORY - EMMET COUNTY OFFICES County Building / Courthouse in Petoskey ~ Open from 8 a.m. to 5 p.m. M-119 Building in Harbor Springs ~ Open from 8 a.m. to 5 p.m. Veterans Affairs Office ~ Open Tues. thru Fri. from 9 a.m. to 5 p.m. (Mon. by appt.) 9-1-1 OFFICE / CENTRAL DISPATCH 1694 US 131 South, Petoskey (231) 347-3911 AIRPORT (PELLSTON REGIONAL) 1351 US 31 North, Pellston (231) 539-8441 BAY BLUFFS MEDICAL CARE FACILITY 750 E. Main St., Petoskey (231) 526-2161 CAMP PET-O-SE-GA 11000 Camp Petosega Rd., Alanson (231) -

2020 Post-Election Recap and Outlook

2020 Post-Election Recap and Outlook Please click here for complete election results from the Michigan Secretary of State. Summary: As with many other states in the 2020 election, Michigan’s results were closer than expected and resulted in narrow victories for top-of-the ticket Democratic candidates. However, Republicans were able to maintain their legislative majority in the state House of Representatives, and kept several contested Congressional seats. Michigan’s state government remains closely divided, like the federal government in Washington, D.C. Background: Following strong Democratic statewide gains in 2018 and based on polling trends, Democrats were expected to succeed in Michigan in 2020. Presidential candidate Joe Biden saw Michigan – along with Wisconsin and Pennsylvania – as key to rebuilding the traditional Midwestern “blue wall” in the Electoral College. Biden had enjoyed consistent polling leads of between 5 and 10% leading up to the election. Democrats also hoped to “flip” the state House of Representatives to control one of the state legislative bodies for the first time since 2010, and give Governor Whitmer a governing partner. They only needed to flip four seats to do so, and were targeting several strong opportunities in suburban Oakland and Kalamazoo counties with the help of large campaign funds raised. For the U.S. House of Representatives, Democrats were targeting two seats for potential pickups: the third district around Grand Rapids held by outgoing Rep. Justin Amash (now a Libertarian), and the sixth district in Kalamazoo and SW Michigan held by longtime moderate Republican Rep. Fred Upton. On the other hand, first-term U.S. -

Meghan Trainor Is Living Her Best

Community Leaders Look at Risks, Rewards of ELCRA Ballot Proposal Pets in the Workplace Meghan Trainor Is Living Her Best ‘Yaaas,Pop Star on Her Generous Lesbian FansB*tch’ and Tipping Drag Queens with Sam Life Smith’s Money Photo: Hanna Hillier PRIDESOURCE.COM FEBRUARY 20, 2020 | VOL. 2808 | FREE VOL. 2808/09 • FEBRUARY 20, 2020 ISSUE 1141 PRIDE SOURCE MEDIA GROUP 20222 Farmington Rd., Livonia, Michigan 48152 Phone 734.293.7200 Spring Pet Issue PUBLISHERS Susan Horowitz & Jan Stevenson 22 Workplace Pets Create Relaxed Experience EDITORIAL 32 Editor in Chief Susan Horowitz, 734.293.7200 x 102 23 Upcoming Pet Events [email protected] 24 Eastpointe Enacts Stricter Entertainment Editor Animal Welfare Rules Chris Azzopardi, 734.293.7200 x 106 [email protected] News & Feature Editor Eve Kucharski, 734.293.7200 x 105 [email protected] 22 30 News & Feature Writers Michelle Brown, Ellen Knoppow, Jason A. Michael, Drew Howard, Jonathan Thurston CREATIVE Webmaster & MIS Director Kevin Bryant, [email protected] Columnists Charles Alexander, Michelle E. Brown, Mikey Rox, D’Anne Witkowski, Gwendolyn Ann Smith, Dana Rudolph Cartoonists Paul Berg Contributing Photographers Andrew Potter, Andrew Cohen, Roxanne Frith, Tih Penfil ADVERTISING & SALES Director of Sales 07 16 Jan Stevenson, 734.293.7200 x 101 [email protected] NEWS OPINION Sales Representatives 4 Michigan Attorney General Hits Back After Rush 16 Parting Glances Ann Cox, 734.293.7200 x 103 Limbaugh Mocks Buttigieg for Being Gay [email protected] -

Discover Local Shows and Learn How to Start Your

March 11-17, 2020 www.lansingcitypulse.com Locally owned • A newspaper for the rest of us LANSING PODCASTS Discover local shows and learn how to start your own See page 15 2 www.lansingcitypulse.com City Pulse • March 11, 2020 Let your vote be heard! Time is running out! This is the last week of voting! tell us who your favorite democratic candidate is - and nominate your favorite local people, places & businesses! 2020 TOP OF THE TOWN CONTEST finish your nomination ballot before 11:59 PM, Tuesday, march 17 at lansingcitypulse.com top 5 will be revealed april 8th CONTEST City Pulse • March 11, 2020 www.lansingcitypulse.com 3 Favorite Things Summer 2020 Glam rocker Jenna Roark RUHALACENTER.COM and her makeup collection Broadway Summer Camp Auditions! Rock ’n roll vocalist Jenna Roark was born and raised on the stretch of U.S. 127 that runs from Leslie to Jackson, but now calls Lansing proper her home. The flamboy- ant performer fronts Conspicuous Bystanders, a dynamic local four-piece that blends the soul- Hey Yo! Don’t Throw Away Your Shot! AUDTION ! fulness of Amy Winehouse with the raw-riffage of Led Zeppelin, creating a brand-new scorching sound. Last weekend, the group Call (517) 337-0464 to schedule audition played a Bernie Sanders rally at Michigan State University’s New Summer Workshops in Singing/Dance/Acting/ Community Co-op—but the busy group has a lot more in the works, Mental Toughness & Yoga as well. There will be new singles, a forthcoming album, and some Private Lessons Available touring beyond state lines.