Transforming Canberra's City Centre

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

C T E D G S L R C B a B W S C I a D

Canberra is recognised as one of the world’s most successful examples of planned city development. In sixty years it has grown from a collection of surveyors’ tents to Australia’s largest inland city. Because it has developed so rapidly most of Canberra’s 200,000 citizens were born elsewhere. This book attempts to capture some aspects of life in Canberra — the buildings, the seasons, people at work and play, the countryside — so that residents of the national capital can give an impression of its moods and lifestyle to relatives and friends far away. Designed by ANU Graphic Design/ Stephen Cole Canberra is recognised as one of the world’s most successful examples of planned city development. In sixty years it has grown from a collection of surveyors’ tents to Australia’s largest inland city. Because it has developed so rapidly most of Canberra’s 200,000 citizens were born elsewhere. This book attempts to capture some aspects of life in Canberra — the buildings, the seasons, people at work and play, the countryside — so that residents of the national capital can give an impression of its moods and lifestyle to relatives and friends far away. Designed by ANU Graphic Design/ Stephen Cole This book was published by ANU Press between 1965–1991. This republication is part of the digitisation project being carried out by Scholarly Information Services/Library and ANU Press. This project aims to make past scholarly works published by The Australian National University available to a global audience under its open-access policy. First published in Australia 1978 Printed in Singapore for the Australian National University Press, Canberra by Toppan Printing Co., Singapore ® The Australian National University 1978 This book is copyright. -

Commonwealth of Australia Gazette! Published by the Australian Government Publishing Service

commonwealth of Australia Gazette! Published by the Australian Government Publishing Service No. G 32 Canberra, Tuesday, 16 August 1977 GENERAL CONTENTS AVAILABILrrY. The Gazette may be obtained by mail from: Notice to private advertisers 2 Mail Ordei Sales, Australian Government Publishing Scrvice, Proclamations 2 P.O. Box 84, Canberra, A.C.T. 2600 Legislation 2 or over the counter from Australian Government Pub- Customs 3 lishing Service Bookshops at: Government departments 6 Adelaide: 12 Pirie Street (Telephone 212 3646) Defence force appointments, etc. 16 Brisbane: ShO"'lo]p 42, The Valley rCentre , Fortitud" " e Valley Commonwealth teaching service 20 (Telephone 52 5526) Canberra: 113 London Circuii t (Telephon 547 7211) Bankruptcy Act 20 Hobart: 162 Macquariarie StreeSu t (Telephone 23 7151) Private advertisements 28 Melbourne: 347 Swanston Street (Telephone 66 33010) Tenders invited 31 Perth: 200 St George's Terrace (Telephone 22 4737) Contracts arranged 35 Sydney: 309 Pitt Street (Telephone 211 4755) Special Gazettes Nos S 158, S 159, S 160, S 161 and The Gazette is also available for perusal at official S 162 are attached Post Offices. Commonwealth Acts and Statutory Rules, Australian Commonwealth of Australia Gazette is published section- Capital Territory Ordinances and Regulations, and other ally in accordance with the arrangements set out below: Australian Government publications may also be pur- Public Service issues contain notices concerning admin- chased at these addresses. istrative matters, including examinations, vacancies, transfers and promotions within the Australian Public NOTICES FOR PUBLICATION and related corres- Service. These issues are published weekly at 10.30 a.m. pondence should be addressed to: on Thursday, and are sold at 95c each plus postage or Gazette Office, Australian Government Publishing on subscription of $58,00 (50 issues), $32.00 (25 issues), Service, P.O. -

Figure 5.1 Non-Aboriginal Heritage and Historical Archaeology Site Within the Vicinity of the Russell Extension Project Alignment

Capital Metro Authority Capital Metro Russell Extension Project - Preliminary Environmental Assessment Figure 5.1 Non-Aboriginal heritage and historical archaeology site within the vicinity of the Russell Extension Project alignment Parsons Brinckerhoff | 2207509A-ENV-REP-008 RevB 43 Capital Metro Authority Capital Metro Russell Extension Project - Preliminary Environmental Assessment 5.2.3 Potential impacts Aboriginal heritage The proposed Russell Extension Project alignment has been assessed for its potential to include Aboriginal archaeological and cultural sites. The assessment found that it was unlikely for either archaeological or cultural sites to exist within or in relation to the proposed Russell Extension corridor. The proposed works would therefore not impact upon places of Aboriginal heritage values along this alignment. There are no further requirements for assessment of Aboriginal heritage values for the proposed Russell Extension Project. Adequate environmental management measures would be developed and implemented during the construction of the Project to manage potential impacts to any unexpected Aboriginal heritage item uncovered during construction. Non-Aboriginal heritage and historical archaeology The Project has the potential to have an impact on listed and nominated heritage places and objects along its route. Generally, this would comprise potential impacts on the setting of heritage places and objects, rather than direct impacts on their fabric. These impacts could arise from placing new elements, such as substations, within significant settings of heritage places, or by the stops and shelters or associated infrastructure blocking important views to heritage places along London Circuit, Constitution Avenue or Russell Drive. Overall, the approach taken to the design and development of the Russell Extension Project, based on a detailed understanding of the heritage values of the heritage places along the Project alignment, has contributed positively to an appropriate approach which minimise or avoids heritage impacts. -

Have a Great 2017

HAVE A GREAT 2017 Acknowledgment of country “We acknowledge and celebrate the traditional owners on whose lands we live, work and study – the Ngunnawal people - and pay our respect to the elders past and present” Disclaimer PARSA would like to thank the following individuals for their contribution to the 2017 Postgraduate Survival Guide: • Giraffe Canberra for the design and layout of this publication. • Shikha Sud and Mike Heffron for putting together the content and proofreading this publication. Some of the material in this publication has also been obtained from the ANU website, the Centrelink website, Going to Uni website, Tenancy Advice website, and the Live in Canberra website. Acknowledgements Published by The Australian National University Postgraduate and Research Students’ Association (PARSA). This publication is intended as a guide only. PARSA accepts no responsibility for the accuracy or completeness of the material contained in this publication. We recommend that you exercise your own skill and care, and seek professional advice if necessary, before relying on any such material. PARSA does not provide any warranty or take any responsibility for the accuracy, source or any other aspect of the enclosed website links. The material in this publication has been collected from a variety of sources and does not necessarily reflect the views of PARSA as an organisation. © PARSA 2017 Copyright of material in this publication is owned by PARSA. CONTENTS contents ABOUT PARSA 3 UNI LIFE 42 IMPORTANT DATES 8 Clubs and Societies 42 10 -

20 October 2017 – 18 February 2018

• Things to do in Canberra at the Festival Take advantage of the SFOB Courtesy Bus as it will take people to exciting permanent and travelling exhibitions at many of Canberra’s attractions including the Australian War Memorial, Parliament House and the National Gallery of Australia precinct once play gets under way. National Gallery of Australia 20 October 2017 – 18 February 2018 A levitating man, a genetically engineered baby, towering giants – welcome to humanity amplified. Featuring uncanny figures with painted silicon skin, glass eyes, human hair and cutting-edge digital art, Hyper Real provokes reflection, fascination, fear and joy. From eerily lifelike sculptures to out- of-this-world virtual reality, this major exhibition charts the evolution of hyperrealism into the 21st century. A compelling chronicle of the cycles of life and our constant need for connection, Hyper Real explores the fundamental question: ‘what makes us human?’ The exhibition presents major works from early American pioneers George Segal, John De Andrea and Duane Hanson, celebrated Australian artists Patricia Piccinini, Ron Mueck and Sam Jinks, international masters Maurizio Cattelan (Italy), Berlinde de Bruyckere (Belgium), Evan Penny (Canada), Sun Yuan and Peng Yu (China) and many more. Hyperrealism, paralleling photorealism in painting, began in the 1960s and 70s when a number of sculptors became interested in a form of sculptural realism based on a vivid and lifelike representation of the human figure. From kinetic sculpture to bio art, this exhibition extends our perception of what constitutes the hyperreal. Tickets are on sale now! More details : nga.gov.au Songlines: Tracking the Seven Sisters, 15 September 2017 – 25 February 2018 Immerse yourself in the epic saga of the Seven Sisters in this new Aboriginal-led exhibition. -

Friends' Newsletter 20 / February 2013 Demountable Room and O!Ce with a Kitchen and Toilets, Located Next to the Canberra Discovery Garden

The Opening Festival was all the more special because the new facility for the National Bonsai and Penjing Collection of Australia was opened on the same day. This is a world-class display and if you haven't seen it yet, please make time to do so—you will be amazed. Last week we met with the new General Manager, Jason Brown, who is the new Arboretum representative at our Council meetings. He clearly values the support of the Friends and is working with us on a number of exciting ideas—I will send you reports as they are progressed. We are planning to have an inaugural Friends' Dinner at the Arboretum on Friday, 5 April so please put that date in your diaries—more details available shortly Also, we are working towards having a Friends' Newsletter 20 / February 2013 demountable room and o!ce with a kitchen and toilets, located next to the Canberra Discovery Garden. Dear Friends This will be very useful for meetings and We did it! The absolutely wonderful National Arboretum administration, as well as a place to refresh weary Canberra is now open! Obviously we were part of a very volunteers. Many thanks to the Arboretum Team for large team, including the ACT Government, Arboretum this initiative. Team and contractors, and we've had exciting times We are in discussions with the Arboretum Team collaborating with them and supporting the regarding the nature of the Centenary Gift from the Arboretum's development. Our thanks go to all Friends to the Arboretum—please send any ideas/ involved. -

Answers to Questions on Notice

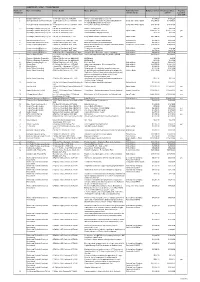

QUESTION NO. NCA01: CONSULTANCIES Number of Name of consultant Contact Details Nature & Purpose Method by which Budgeted amount Actual expenditure Ongoing Consultants contract was let 2003-04 beyond 30 June 2004 1 Bill Guy And Partners 6A Thesiger Ct Deakin ACT 2600 Scrivener Dam Structural assessment $1,874.00 $1,872.20 2 Dorrough Britz & Associates Pty Ltd 12/285 Canberra Avenue Fyshwick ACT Design and Documentation of Landscaping Works for Competitive Written Quote $42,350.00 $17,655.00 2609 Treasury Building Northern Forecourt Dorrough Britz & Associates Pty Ltd 12/285 Canberra Avenue Fyshwick ACT Parkes Place drainage and irrigation Competitive Written Quote $18,452.50 $18,452.50 2609 3 Gutteridge Haskins Davey Pty Ltd PO Box 36 Belconnen ACT 2616 Advice - loading checks $342.00 $341.00 Gutteridge Haskins Davey Pty Ltd PO Box 36 Belconnen 2616 Commonwealth Place Forecourt Open Tender $108,717.40 $108,717.40 yes Gutteridge, Haskins Davey Pty Ltd PO Box 36 Belconnen 2616 Commonwealth Park play structure $126.00 $125.40 Gutteridge, Haskins Davey Pty Ltd PO Box 36 Belconnen ACT 2616 King Edward Terrace Pedestrian works Open Tender $34,200.00 $32,305.90 yes 4 Maunsell Australia Pty Ltd 38 Thesiger Court Deakin ACT 2600 Griffin Legacy - transport assessment Written Quote $5,000.00 $5,000.00 5 Donald Cant Watts Corke (ACT) PO Box 5048 Kingston ACT 2604 National Emergency Services Memorial Written Quote $9,250.00 $9,250.00 6 Young Consulting Engineers PO Box 52 Yarralumla ACT 2600 Design & Documentation of Car park Restoration Works, Competitive -

CBD Design Highlights G

7 Civic Square H CBD Design Highlights G Disliked by modernist purists when T F E this square was built, the gold mosaic columns underneath the twin office NORTHOURNE AVENUE GOU LONSDALE STE LD STREET buildings are now deeply loved. The TORENS STREET bronze statue of Ethos by Tom Bass ELOU ERA STRE 1 University Avenue 4 Monaro Mall is an important work of mid-century ET B AR RY Australian art. DR Once stretching unbroken through At the time Monaro Mall was opened IVE the ANU from the foot of Black in 1963, this mid-century modernist 180 London Circuit Mountain to the central Vernon building by Whitehead and Payne Circle, the innermost block of Architects was the first three-storey, 8 Craft ACT University Avenue contains superb fully enclosed and air-conditioned Craft and Design Centre supports examples of midcentury architecture. shopping centre in Australia. It designers, makers, artists and Stand outside the Reserve Bank and has recently been refurbished as a craftspeople at every stage of their BAR do a twirl. contemporary reinterpretation of its careers. Support local artists and buy RY DRIE 1–21 University Ave original design. COOYO LIMESTONE AVENUE handmade tableware and unique NG STREET Cnr Bunda St + Petrie Plaza jewellery at the Craft ACT shop, 2 Reserve Bank Sculpture and visit their beautiful gallery of 3 T 5 E Frank Hinder Mosaic changing exhibitions. E A hidden treasure inside this excellent R RUDD ST T REET S E Level 1 North Building, 180 London Cct K example of Stripped Classical This is one of those best-kept local R A L C architecture, ‘Four Pieces’ is a 17m secrets: the only way you’ll find this S U C R 9 A wall work designed and sculpted by stunning glass mosaic is by looking Constitution Avenue MORT STEET M AINSLIE AVENUE Gerald and Margo Lewers. -

NPA Bulletin National Parks Association of the A.C.T

NPA Bulletin National Parks Association of the A.C.T. Vol. 23 No. 3 March 1986 NATIONAL PARKS ASSOCIATION OF THE AUSTRALIAN CAPITAL TERRITORY INC. Inaugurated 1 960 Office bearers and Committee Aims and Objects of the Association President: Ross Carlton, 41 Batchelor Street, Torrens, 2607 Promotion of national parks and of measures for the 86 3892 (Hi 68 5366 (W) protection of fauna and flora, scenery and natural Vice-President: Fiona Brand. 11 Dyson Street, Lyneham, features in the Australian Capital Territory and else 2602 47 9538(H) where, and the reservation of specific areas. Secretary: Anne Robertson, PO Box 424, Dickson 2602 Interest in the provision of appropriate outdoor re 72 4534 (W) 82 1 141 (H) creation areas. Treasurer- Syd Comfort, 87 Shackleton Circuit. Mawson Stimulation of interest in, and appreciation and enjoy 2607 86 2578(H) ment of, such natural phenomena by organised field Assistant Secretary: vacant outings, meetings or any other means. Publicity Officer: vacant (contact Secretary) Committee Members: Neville Esau 86 4176 (H) 49 4554 (W) Co-operation with organisations and persons having Kevin Frawley 82 3080 (H) 68 8309 <W) lan Haynes similar interests and objectives. 51 4762(H) MargusKarilaid 48 6149(H) 46 5862 (W) Promotion of. and education for, nature conservation, Kevin Totterdell 814410(H) 63 2837 (W) Phil Gatenby and the planning of land-use to achieve conservation. 41 6284(H) 52 6301 (W) Bulletin Editor: Margus Karilaid, 17 Fairbridge Crescent, Ainslie 2602. 48 6149(H) 46 5862 (W) Outings Convenor: lan -

Newsletter 48

NEWSLETTER Issue 48 September 2020 Dear Friends Just recently, one very cold Tuesday Only a few days ago, ACT sign maker morning, it was heart-warming to see Michael Deren sent me an email the Friends’ logo displayed on the new donating the cost of the wrapping of bus and on the Working Bee trailer the trailer because he said…. ‘It’s a parked up near Adam’s Forest; not to gift from our family for all the mention the Friends hard at work wonderful experiences we have had clearing pink tree guards and making at the NAC’. A wonderful gesture from Adam’s Forest spic and span. He Michael, Lili, Charlie and Ruby. Thank would be very pleased with the ‘tree you very much. Your generous huggers’ as he called us! support is much appreciated. In this edition Discovery Kitchen Garden Update p.7 Message from Callie Earnshaw, Community The Atomic tree p.7 Engagement Officer p.3 Mulching the Silver birches: Working bees part 2 Wattle Day p.4 p.11 STEP news p.6 Trees in Focus: Forest 7, Magnolia p.9 Friends of NAC Newsletter 48, September 2020 1 The Bus got some very special attention recently when local Aboriginal elder of the Ngambri clan, Matilda House performed a smoking ceremony in and around the bus. This ceremony is an ancient aboriginal custom that involves burning and smouldering of various native plants, and in this case, gum leaves. The smoke has cleansing properties and the ability to ward off bad spirits from the people and the land and makes a pathway for a brighter future. -

Archivesact Finding Aid ACT Government Public

fACT Archives ACT 1 ACT Government public art A U S T R A L I A N C A P I T A L T E R R I T O R Y ACT Governm ent public art: fACT 1 ACT Government March 2005 1 Constitution Avenue • Canberra, ACT, 2600 Phone +61 2 6207 5726 • Fax +61 2 6207 5835 Table of Contents EXHIBITIONS .........................30 INTRODUCTION.......................4 TAIKICHI IRIE...........................30 FACT GUIDES SERIES...................4 MAINTENANCE......................32 THE AIM OF THIS FACT GUIDE ...4 ACCESS TO THE RECORDS...........5 PLAQUES, MEMORIALS AND CITING THE RECORDS.................5 TIME CAPSULES....................34 INDEXES AND FINDING AIDS .......6 POLICIES ...................................8 PUBLICATIONS......................36 THE COMMONWEALTH...............8 MONOGRAPHS AND PAMPHLETS ABORIGINAL ART .....................11 ................................................36 THE ACT GOVERNMENT..........12 INFORMATION COMMISSIONED WORKS ...15 MANAGEMENT – CONTROL – REGISTERS ..........................39 SCHOOLS..................................15 PUBLIC LIBRARIES....................19 NATIONAL CAPITAL HOSPITALS & HEALTH CENTRES DEVELOPMENT COMMISSION...39 .................................................19 INDEX .......................................40 GOVERNMENT BUILDINGS, COURTS & POLICE STATIONS ....20 TOWN CENTRES, GROUP CENTRES & LOCAL CENTRES...................20 OPEN PUBLIC PLACES ...............21 STREET ART .............................21 PAINTINGS ...............................21 PRIZES, AWARDS & GRANTS .....................................................23 -

The Top 20 Mid-Century Modern Buildings in Canberra

presents….The Top 20 Mid-Century Modern Buildings in Canberra 20 buildings might seem a lot, but in a city that grew up in the mid-century period that showcases work from some of Australia’s most renowned architects, it is almost impossible to narrow the list to just 20! While many on the list are obvious and iconic, we also wanted to include a few buildings that are lesser known or are at risk of being lost altogether or visually lost in the midst of adjacent developments (*). We are also a little loose on the use of mid-century – some of these buildings even creep into the 1980s – but good architecture is good architecture! Hashtag your pics #canberramodern so we can share in all the fun! And check out canberramodern.com for more info! National Library of Australia, Parkes Place, Parkes - Bunning and Madden, 1968 NB: Happy 50th Birthday! University House, Balmain Crescent, Australian National University, Acton - Brian Lewis, 1954 NB: the interiors of this building are fab including custom design furniture by Fred Ward - a walk around the rest of ANU will also not disappoint, mid-century gems are everywhere! *Churchill House, Northbourne Ave, Braddon - Robin Boyd, 1971 Housing Co-operatives: Urambi Village, Crozier Cct, Kambah and Wybalena Grove, Cook - Michael Dysart, 1974 *Callam Offices, Callam Street, Woden - John Andrews, 1977-81 (also check out his residences at the University of Canberra and his Cameron Offices in Belconnen) *Giralang Primary School, Atalumba Close, Giralang - Enrico Taglietti, 1976 (there are so many Taglietti