Skew Index: Descriptive Analysis, Explanatory Power and Short- Term Forecast

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Estimating 90-Day Market Volatility with VIX and VXV

Estimating 90-Day Market Volatility with VIX and VXV Larissa J. Adamiec, Corresponding Author, Benedictine University, USA Russell Rhoads, Tabb Group, USA ABSTRACT The CBOE Volatility Index (VIX) has historically been a consistent indicator of 30-day or 1-month (21-day actual) realized market volatility. In addition, the Chicago Board Options Exchange also quotes the CBOE 3-Month Volatility Index (VXV) which indicates the 3-month realized market volatility. This study demonstrates both VIX and VXV are still reliable indicators of their respective realized market volatility periods. Both of the indexes consistently overstate realized volatility, indicating market participants often perceive volatility to be much higher than volatility actually is. The overstatement of expected volatility leads to an indicator which is consistently higher. Perceived volatility in the long-run is often lower than volatility in the short-run which is why VXV is often lower than VIX (VIX is usually lower than VXV). However, the accuracy of the VXV is roughly 35% as compared with the accuracy of the VIX at 60.1%. By combining the two indicators to create a third indicator we were able to provide a much better estimate of 64-Day Realized volatility, with an accuracy rate 41%. Due to options often being over-priced, historical volatility is often higher than both realized volatility or the volatility index, either the VIX or the VXV. Even though the historical volatility is higher we find the estimated historical volatility to be more easily estimated than realized volatility. Using the same time period from January 2, 2008 through December 31, 2016 we find the VIX estimates the 21-Day Historical Volatility with 83.70% accuracy. -

Copyrighted Material

Index 12b-1 fee, 68–69 combining with Western analysis, 3M, 157 122–123 continuation day, 116 ABC of Stock Speculation, 157 doji, 115 accrual accounting, 18 dragonfl y doji, 116–117 accumulated depreciation, 46–47 engulfi ng pattern, 120, 121 accumulation phase, 158 gravestone doji, 116, 117, 118 accumulation/distribution line, hammer, 119 146–147 hanging man, 119 Adaptive Market Hypothesis, 155 harami, 119, 120 Altria, 29, 127, 185–186 indicators 120 Amazon.com, 151 long, 116, 117, 118 amortization, 47, 49 long-legged doji, 118 annual report, 44–46 lower shadow, 115 ascending triangle, 137–138, 140 marubozu, 116 at the money, 192 real body, 114–115 AT&T, 185–186 segments illustrated, 114 shadows, 114 back-end sales load, 67–68 short,116, 117 balance sheet, 46–50 spinning top, 118–119 balanced mutual funds, 70–71 squeeze alert, 121, 122, 123 basket of stocks, 63 tails, 114 blue chip companies, 34 three black crows, 122, 123 Boeing, 134–135 three white soldiers, 122, 123 book value, 169 trend-based, 117–118 breadth, 82–83, 97 upper shadow, 115 breakaway gap, 144 wicks, 114 break-even rate, 16–17 capital assets, 48, 49 breakout, 83–84, 105–106 capitalization-based funds, 71 Buffett, Warren, 152 capitalization-weighted average, 157 bull and bear markets,COPYRIGHTED 81, 174–175 Caterpillar, MATERIAL 52–54, 55, 57, 58, 59, 131 Bureau of Labor Statistics (BLS), 15 CBOE Volatility Index (VIX), 170, 171 Buy-and-hold strategy, 32, 204–205 Chaikin Money Flow (CMF), 146 buy to open/sell to open, 96 channel, 131–132 charting calendar spreads, 200–201 -

Asset Allocation POINT WHAT DOES a LOW VIX TELL US June 2017 ABOUT the MARKET? Timely Intelligence and Analysis for Our Clients

PRICE Asset Allocation POINT WHAT DOES A LOW VIX TELL US June 2017 ABOUT THE MARKET? Timely intelligence and analysis for our clients. KEY POINTS . The financial press has been paying considerable attention lately to the Chicago Board Options Exchange Volatility Index (VIX), with many financial pundits citing recent low readings on the VIX as evidence of investor complacency and rising equity risk. Robert Harlow, CFA, CAIA . Quantitative Analyst Media coverage often implies that a low current VIX is a strong signal of expected Asset Allocation future volatility and will be followed by a sell-off in U.S. equities and other risk-seeking assets. Historical evidence shows that, over the near term, investors typically overestimate the next 30-day volatility of the S&P 500 Index. Further, when the VIX has been low, U.S. equities have outperformed U.S. bonds on average over the next 12 months, regardless of the change in the VIX over that horizon. Without a meaningful and prolonged catalyst, we do not believe a low level of the VIX David Clewell, CFA alone implies investor complacency or an immediate danger of a risk-off event. Research Analyst Asset Allocation BACKGROUND There has been much discussion in the financial press recently about the danger of investor complacency—with a low VIX frequently cited as compelling evidence that equity investors have grown too relaxed about potential risks. The problem is that it is difficult to determine whether markets are truly complacent or not; we can’t survey all investors and, even if we could, how many investors would admit that they were complacent? Instead, we take a mental shortcut and presume that something we can measure is a good proxy for the thing we actually care about. -

Futures & Options on the VIX® Index

Futures & Options on the VIX® Index Turn Volatility to Your Advantage U.S. Futures and Options The Cboe Volatility Index® (VIX® Index) is a leading measure of market expectations of near-term volatility conveyed by S&P 500 Index® (SPX) option prices. Since its introduction in 1993, the VIX® Index has been considered by many to be the world’s premier barometer of investor sentiment and market volatility. To learn more, visit cboe.com/VIX. VIX Futures and Options Strategies VIX futures and options have unique characteristics and behave differently than other financial-based commodity or equity products. Understanding these traits and their implications is important. VIX options and futures enable investors to trade volatility independent of the direction or the level of stock prices. Whether an investor’s outlook on the market is bullish, bearish or somewhere in-between, VIX futures and options can provide the ability to diversify a portfolio as well as hedge, mitigate or capitalize on broad market volatility. Portfolio Hedging One of the biggest risks to an equity portfolio is a broad market decline. The VIX Index has had a historically strong inverse relationship with the S&P 500® Index. Consequently, a long exposure to volatility may offset an adverse impact of falling stock prices. Market participants should consider the time frame and characteristics associated with VIX futures and options to determine the utility of such a hedge. Risk Premium Yield Over long periods, index options have tended to price in slightly more uncertainty than the market ultimately realizes. Specifically, the expected volatility implied by SPX option prices tends to trade at a premium relative to subsequent realized volatility in the S&P 500 Index. -

COVID-19 Update Overview

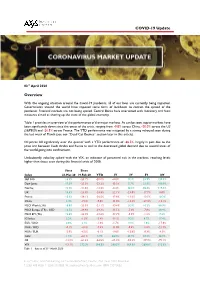

COVID-19 Update 03rd April 2020 Overview With the ongoing situation around the Covid-19 pandemic, all of our lives are currently being impacted. Governments around the world have imposed some form of lockdown to contain the spread of the pandemic. Financial markets are not being spared. Central Banks have intervened with monetary and fiscal measures aimed at shoring up the state of the global economy. Table 1 provides an overview of the performance of the major markets. As can be seen, equity markets have been significantly down since the onset of the crisis, ranging from -9.8% across China, -20.0% across the US (S&P500) and -26.5% across France. The YTD performance was mitigated by a strong rebound seen during the last week of March (see our “Dead Cat Bounce” section later in this article). Oil prices fell significantly over the quarter with a YTD performance of -66.5%, largely in part due to the price war between Saudi Arabia and Russia as well as the decreased global demand due to several areas of the world going into confinement. Undoubtedly volatility spiked with the VIX, an indicator of perceived risk in the markets, reaching levels higher than those seen during the financial crisis of 2008. Since Since Index 23-Mar-20 19-Feb-20 YTD 1Y 3Y 5Y 10Y S&P 500 15.5% -23.7% -20.0% -8.8% 9.1% 23.9% 120.3% Dow Jones 17.9% -25.3% -23.2% -15.5% 5.7% 21.9% 100.9% Nasdaq 12.2% -21.6% -14.2% -0.4% 30.2% 55.6% 219.4% UK 13.6% -23.9% -24.8% -22.1% -23.0% -17.7% 0.0% France 12.3% -28.1% -26.5% -17.8% -13.6% -13.5% 10.3% China 3.4% -7.6% -9.8% -11.0% -

The DB Currency Volatility Index (CVIX): a Benchmark for Volatility

Global Foreign Excahnge Deutsche Bank@ October 2007 Deutsche Bank Guide To Currency Indices Global Markets Saravelos Global Hzead Global Head FX StrategyBilal Jason Rashid James Torquil George Hafeez Batt Hoosenally Malcolm Wheatley Editor Contributors George Saravelos Mirza Baig Jason Batt Bilal Hafeez FX Strategy EM FX Strategy Global Head Global Head FX Index Products FX Strategy Rashid Hoosenally Caio Natividade James Malcolm Global Head FX Derivatives Strategy EM FX Strategy Global Risk Strategy Deutsche Bank@ Guide to Currency Indices October 2007 Table of Contents Introduction............................................................................................................................. 3 Overview ................................................................................................................................ 4 The Deutsche Bank Menu of Currency Indices...................................................................... 7 Currency Markets: Money Left on the Table?........................................................................ 9 Tactical Currency Indices DB G10 Trade-Weighted Indices: From Theory to Practice.................................................. 18 DB EM Asia Policy Baskets .................................................................................................. 22 The Emerging Asia Reserves, Liquidity and Yield (EARLY) Index......................................... 26 The DB Currency Volatility Index (CVIX): A Benchmark for Volatility ................................... -

VIX Futures As a Market Timing Indicator

Journal of Risk and Financial Management Article VIX Futures as a Market Timing Indicator Athanasios P. Fassas 1 and Nikolas Hourvouliades 2,* 1 Department of Accounting and Finance, University of Thessaly, Larissa 41110, Greece 2 Department of Business Studies, American College of Thessaloniki, Thessaloniki 55535, Greece * Correspondence: [email protected]; Tel.: +30-2310-398385 Received: 10 June 2019; Accepted: 28 June 2019; Published: 1 July 2019 Abstract: Our work relates to the literature supporting that the VIX also mirrors investor sentiment and, thus, contains useful information regarding future S&P500 returns. The objective of this empirical analysis is to verify if the shape of the volatility futures term structure has signaling effects regarding future equity price movements, as several investors believe. Our findings generally support the hypothesis that the VIX term structure can be employed as a contrarian market timing indicator. The empirical analysis of this study has important practical implications for financial market practitioners, as it shows that they can use the VIX futures term structure not only as a proxy of market expectations on forward volatility, but also as a stock market timing tool. Keywords: VIX futures; volatility term structure; future equity returns; S&P500 1. Introduction A fundamental principle of finance is the positive expected return-risk trade-off. In this paper, we examine the dynamic dependencies between future equity returns and the term structure of VIX futures, i.e., the curve that connects daily settlement prices of individual VIX futures contracts to maturities across time. This study extends the VIX futures-related literature by testing the market timing ability of the VIX futures term structure regarding future stock movements. -

An Introduction to the VIX Index and Volatility Instruments Alexander Ryvkin Pace University

Pace University DigitalCommons@Pace Honors College Theses Pforzheimer Honors College 2019 Volatility Products and their Uses: An Introduction to the VIX Index and Volatility Instruments Alexander Ryvkin Pace University Follow this and additional works at: https://digitalcommons.pace.edu/honorscollege_theses Part of the Business Commons Recommended Citation Ryvkin, Alexander, "Volatility Products and their Uses: An Introduction to the VIX Index and Volatility Instruments" (2019). Honors College Theses. 230. https://digitalcommons.pace.edu/honorscollege_theses/230 This Thesis is brought to you for free and open access by the Pforzheimer Honors College at DigitalCommons@Pace. It has been accepted for inclusion in Honors College Theses by an authorized administrator of DigitalCommons@Pace. For more information, please contact [email protected]. Volatility Products and Their Uses 1 Volatility Products and their Uses An Introduction to the VIX Index and Volatility Instruments Pace University, Lubin School of Business Pforzheimer Honors College Majoring in Finance Presenting May 9th, 2019 Graduating May 18th, 2019 Examiner: Andrew Coggins By Alexander Ryvkin Volatility Products and Their Uses 2 Volatility Products and Their Uses 3 Abstract Volatility instruments are complex investment products that can be used to hedge or speculate based on changes in market sentiment and fluctuations in the S&P 500. These products offer a unique approach to protecting one’s portfolio and making strategic bets on future market volatility. However, lack of understanding of these products can be potentially dangerous as they can change dramatically in value within extremely short time-frames. Investors must be wary of using these products improperly; failure to adequately assess the risk of using volatility products can deliver devastating losses to one’s portfolio. -

A Linear Process Approach to Short-Term Trading Using the VIX Index As a Sentiment Indicator

Preprints (www.preprints.org) | NOT PEER-REVIEWED | Posted: 29 July 2021 Article A Linear Process Approach to Short-term Trading Using the VIX Index as a Sentiment Indicator Yawo Mamoua Kobara 1,‡ , Cemre Pehlivanoglu 2,‡* and Okechukwu Joshua Okigbo 3,‡ 1 Western University; [email protected] 2 Cidel Financial Services; [email protected] 3 WorldQuant University; [email protected] * Correspondence: [email protected] ‡ These authors contributed equally to this work. 1 Abstract: One of the key challenges of stock trading is the stock prices follow a random walk 2 process, which is a special case of a stochastic process, and are highly sensitive to new information. 3 A random walk process is difficult to predict in the short-term. Many linear process models that 4 are being used to predict financial time series are structural models that provide an important 5 decision boundary, albeit not adequately considering the correlation or causal effect of market 6 sentiment on stock prices. This research seeks to increase the predictive capability of linear process 7 models using the SPDR S&P 500 ETF (SPY) and the CBOE Volatility (VIX) Index as a proxy for 8 market sentiment. Three econometric models are considered to forecast SPY prices: (i) Auto 9 Regressive Integrated Moving Average (ARIMA), (ii) Generalized Auto Regressive Conditional 10 Heteroskedasticity (GARCH), and (iii) Vector Autoregression (VAR). These models are integrated 11 into two technical indicators, Bollinger Bands and Moving Average Convergence Divergence 12 (MACD), focusing on forecast performance. The profitability of various algorithmic trading 13 strategies are compared based on a combination of these two indicators. -

Bloomberg Commodity Outlook

Learn more about Bloomberg Indices Broad Market Outlook 1 Energy 3 Bloomberg Commodity Outlook – June 2019 Edition Metals 7 Agriculture 11 Bloomberg Commodity Index (BCOM) DATA PERFORMANCE: 17 Overview, Commodity TR, Prices, Volatility The Receding Tide CURVE ANALYSIS: 21 Contango/Backwardation, Roll Yields, - Lower broad-commodity prices help fill some macroeconomic gaps Forwards/Forecasts - Commodity tide is receding with bond yields MARKET FLOWS: 24 Open Interest, Volume, - Crude oil is the greatest risk to macro performance COT, ETFs - Base metals to join receding macroeconomic tide; gold supported PERFORMANCE 27 - Stormy weather may be lightning strike for agriculture bulls Note ‐ Click on graphics to get to the Bloomberg terminal Data and outlook as of May 31 Mike McGlone – BI Senior Commodity Strategist BI COMD (the commodity dashboard) Crude Oil and Copper's Primary Risks trade deal. Our graphic depicts the Bloomberg Are on Receding Macro Tide Commodity Spot Index's vulnerability at the downward- sloping 60-month average, as the same measure of the Performance: May -3.4%, 2019 +2.3%, Spot +3.4%. VIX Volatility Index turns higher. (Returns are total return (TR) unless noted) BCOM Risks Downturn With Yields, Bottoming VIX (Bloomberg Intelligence) -- The decreasing likelihood of a definitive U.S.-China trade accord, and V-shaped bottoms in crude oil and stocks, will pressure broad commodities as the macroeconomic tide recedes, in our view. Declining Treasury yields have been a leading indicator this year, continuing 4Q's risk-off trend. Commodities appear to be teetering on their last, wobbly pillar (stock- market volatility), with declining crude oil -- the greater risk, in our view -- dashing hopes. -

VIX and VIX Etns

VIX and VIX ETNs What They’re All About and How to Trade this Exciting Market Dan, The Trading God [email protected] http://tradinggods.net Ridgeline Media Group, LLC. 70 SW Century Drive Suite 100-148 Bend, Oregon 97702 VIX and VIX ETNs What They’re All About and How to Trade This Exciting Market Table of Contents Chapter 1: VIX Overview - What it is and how it Works Chapter 2: Three Ways to Trade VIX Chapter 3: Four VIX Trading Strategies Chapter 4: VIX Trader Chapter 5: VIX Resources Chapter 1: VIX Overview - What it is and how it Works: VIX is the Chicago Board Options Exchange (CBOE) Volatility Index and it shows the market expectation of 30 day volatility. The VIX Index is updated on a continuous basis and offers a picture of the expected market volatility in the S&P 500 during the next 30 days. The VIX Index was first introduced in 1993 and a second version was introduced in 2003 and is still in use today. VIX is also commonly known as the “fear index,” since volatility and the VIX index tend to rise during times that the S&P 500 is falling. Therefore, the VIX Index is said to measure the amount of fear or complacency in the market. Many analysts suggest that VIX is a predictive measure of market risk and future market action since this index is traded by some of the most professional traders in the world. However, there is also a large school of thought that suggests that VIX is a trailing indicator and so not suitable for attempts at market timing. -

January 2021 to Five Prior Years, We Highlight the Following

Spotlight: January Market Metrics SIFMA Insights January Market Metrics and Trends A Look at Monthly Volatility and Equity and Options Volumes February 2021 Monthly Metrics • Volatility (VIX): January average 24.91 (-14.8% to 2020), peak 37.21 on January 27 • S&P 500 (Price): January average 3,793.75 (+17.9% to 2020), peak 3,855.36 on January 27 • Equity ADV (billion shares): January average 15.6 (+42.6% to 2020), peak 24.5 on January 27 • Options ADV (million contracts): January average 43.5 (+49.8% to 2020), peak 59.3 on January 27 Monthly Trend Highlights • January VIX the highest since 2016; was on a weekly downward trend until the last week of the month when the WallStreetBets short squeeze trades began • Analyzing the inverse relationship in price movements in GME/AMC and the S&P 500; on January 27, the S&P 500 daily price change was -2.6, versus GME +134.8 and AMC +301.2% SIFMA Insights Page | 1 Spotlight: January Market Metrics Spotlight: January Market Metrics To say 2021 came out of the gates strong would be an understatement. On average in January, markets (in terms of S&P 500 price) were up 17.9% to the 2020 average, on top of a 10.5% Y/Y rise in 2020. Volumes continued to climb in January: multi-listed options +49.8% to the 2020 average (+52.5% Y/Y in 2020); and equities +42.6% to the 2020 average in January (+55.4% Y/Y in 2020). These higher than historical volume levels come as volatility began to settle at the start of the year, with the January average -14.8% to the 2020 average (the VIX increased +90.1% Y/Y in 2020 on average).