Does a Candlestick Strategy Have Its Value in the VIX Future Market?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Estimating 90-Day Market Volatility with VIX and VXV

Estimating 90-Day Market Volatility with VIX and VXV Larissa J. Adamiec, Corresponding Author, Benedictine University, USA Russell Rhoads, Tabb Group, USA ABSTRACT The CBOE Volatility Index (VIX) has historically been a consistent indicator of 30-day or 1-month (21-day actual) realized market volatility. In addition, the Chicago Board Options Exchange also quotes the CBOE 3-Month Volatility Index (VXV) which indicates the 3-month realized market volatility. This study demonstrates both VIX and VXV are still reliable indicators of their respective realized market volatility periods. Both of the indexes consistently overstate realized volatility, indicating market participants often perceive volatility to be much higher than volatility actually is. The overstatement of expected volatility leads to an indicator which is consistently higher. Perceived volatility in the long-run is often lower than volatility in the short-run which is why VXV is often lower than VIX (VIX is usually lower than VXV). However, the accuracy of the VXV is roughly 35% as compared with the accuracy of the VIX at 60.1%. By combining the two indicators to create a third indicator we were able to provide a much better estimate of 64-Day Realized volatility, with an accuracy rate 41%. Due to options often being over-priced, historical volatility is often higher than both realized volatility or the volatility index, either the VIX or the VXV. Even though the historical volatility is higher we find the estimated historical volatility to be more easily estimated than realized volatility. Using the same time period from January 2, 2008 through December 31, 2016 we find the VIX estimates the 21-Day Historical Volatility with 83.70% accuracy. -

A Statistical Analysis of the Predictive Power of Japanese Candlesticks Mohamed Jamaloodeen Georgia Gwinnett College, [email protected]

Journal of International & Interdisciplinary Business Research Volume 5 Article 5 June 2018 A Statistical Analysis of the Predictive Power of Japanese Candlesticks Mohamed Jamaloodeen Georgia Gwinnett College, [email protected] Adrian Heinz Georgia Gwinnett College, [email protected] Lissa Pollacia Georgia Gwinnett College, [email protected] Follow this and additional works at: https://scholars.fhsu.edu/jiibr Part of the Finance and Financial Management Commons Recommended Citation Jamaloodeen, Mohamed; Heinz, Adrian; and Pollacia, Lissa (2018) "A Statistical Analysis of the Predictive Power of Japanese Candlesticks," Journal of International & Interdisciplinary Business Research: Vol. 5 , Article 5. Available at: https://scholars.fhsu.edu/jiibr/vol5/iss1/5 This Article is brought to you for free and open access by FHSU Scholars Repository. It has been accepted for inclusion in Journal of International & Interdisciplinary Business Research by an authorized editor of FHSU Scholars Repository. Jamaloodeen et al.: Analysis of Predictive Power of Japanese Candlesticks A STATISTICAL ANALYSIS OF THE PREDICTIVE POWER OF JAPANESE CANDLESTICKS Mohamed Jamaloodeen, Georgia Gwinnett College Adrian Heinz, Georgia Gwinnett College Lissa Pollacia, Georgia Gwinnett College Japanese Candlesticks is a technique for plotting past price action of a specific underlying such as a stock, index or commodity using open, high, low and close prices. These candlesticks create patterns believed to forecast future price movement. Although the candles’ popularity has increased rapidly over the last decade, there is still little statistical evidence about their effectiveness over a large number of occurrences. In this work, we analyze the predictive power of the Shooting Star and Hammer patterns using over six decades of historical data of the S&P 500 index. -

Copyrighted Material

Index 12b-1 fee, 68–69 combining with Western analysis, 3M, 157 122–123 continuation day, 116 ABC of Stock Speculation, 157 doji, 115 accrual accounting, 18 dragonfl y doji, 116–117 accumulated depreciation, 46–47 engulfi ng pattern, 120, 121 accumulation phase, 158 gravestone doji, 116, 117, 118 accumulation/distribution line, hammer, 119 146–147 hanging man, 119 Adaptive Market Hypothesis, 155 harami, 119, 120 Altria, 29, 127, 185–186 indicators 120 Amazon.com, 151 long, 116, 117, 118 amortization, 47, 49 long-legged doji, 118 annual report, 44–46 lower shadow, 115 ascending triangle, 137–138, 140 marubozu, 116 at the money, 192 real body, 114–115 AT&T, 185–186 segments illustrated, 114 shadows, 114 back-end sales load, 67–68 short,116, 117 balance sheet, 46–50 spinning top, 118–119 balanced mutual funds, 70–71 squeeze alert, 121, 122, 123 basket of stocks, 63 tails, 114 blue chip companies, 34 three black crows, 122, 123 Boeing, 134–135 three white soldiers, 122, 123 book value, 169 trend-based, 117–118 breadth, 82–83, 97 upper shadow, 115 breakaway gap, 144 wicks, 114 break-even rate, 16–17 capital assets, 48, 49 breakout, 83–84, 105–106 capitalization-based funds, 71 Buffett, Warren, 152 capitalization-weighted average, 157 bull and bear markets,COPYRIGHTED 81, 174–175 Caterpillar, MATERIAL 52–54, 55, 57, 58, 59, 131 Bureau of Labor Statistics (BLS), 15 CBOE Volatility Index (VIX), 170, 171 Buy-and-hold strategy, 32, 204–205 Chaikin Money Flow (CMF), 146 buy to open/sell to open, 96 channel, 131–132 charting calendar spreads, 200–201 -

Asset Allocation POINT WHAT DOES a LOW VIX TELL US June 2017 ABOUT the MARKET? Timely Intelligence and Analysis for Our Clients

PRICE Asset Allocation POINT WHAT DOES A LOW VIX TELL US June 2017 ABOUT THE MARKET? Timely intelligence and analysis for our clients. KEY POINTS . The financial press has been paying considerable attention lately to the Chicago Board Options Exchange Volatility Index (VIX), with many financial pundits citing recent low readings on the VIX as evidence of investor complacency and rising equity risk. Robert Harlow, CFA, CAIA . Quantitative Analyst Media coverage often implies that a low current VIX is a strong signal of expected Asset Allocation future volatility and will be followed by a sell-off in U.S. equities and other risk-seeking assets. Historical evidence shows that, over the near term, investors typically overestimate the next 30-day volatility of the S&P 500 Index. Further, when the VIX has been low, U.S. equities have outperformed U.S. bonds on average over the next 12 months, regardless of the change in the VIX over that horizon. Without a meaningful and prolonged catalyst, we do not believe a low level of the VIX David Clewell, CFA alone implies investor complacency or an immediate danger of a risk-off event. Research Analyst Asset Allocation BACKGROUND There has been much discussion in the financial press recently about the danger of investor complacency—with a low VIX frequently cited as compelling evidence that equity investors have grown too relaxed about potential risks. The problem is that it is difficult to determine whether markets are truly complacent or not; we can’t survey all investors and, even if we could, how many investors would admit that they were complacent? Instead, we take a mental shortcut and presume that something we can measure is a good proxy for the thing we actually care about. -

Candlestick—The Main Mistake of Economy Research in High Frequency Markets

International Journal of Financial Studies Article Candlestick—The Main Mistake of Economy Research in High Frequency Markets Michał Dominik Stasiak Department of Investment and Real Estate, Poznan University of Economics and Business, al. Niepodleglosci 10, 61-875 Poznan, Poland; [email protected] Received: 4 August 2020; Accepted: 1 October 2020; Published: 10 October 2020 Abstract: One of the key problems of researching the high-frequency financial markets is the proper data format. Application of the candlestick representation (or its derivatives such as daily prices, etc.), which is vastly used in economic research, can lead to faulty research results. Yet, this fact is consistently ignored in most economic studies. The following article gives examples of possible consequences of using candlestick representation in modelling and statistical analysis of the financial markets. Emphasis should be placed on the problem of research results being detached from the investing practice, which makes most of the results inapplicable from the investor’s point of view. The article also presents the concept of a binary-temporal representation, which is an alternative to the candlestick representation. Using binary-temporal representation allows for more precise and credible research and for the results to be applied in investment practice. Keywords: high frequency econometric; technical analysis; investment decision support; candlestick representation; binary-temporal representation JEL Classification: C01; C53; C90 1. Introduction While researching any subject literature, often one can notice that some popular methods in scientific research are copied and used without second thought by further researchers. Nowadays, the vast majority of papers pertaining to the analysis of course trajectory on financial markets and connected prediction possibilities use historical data in the form of a candlestick representation (or its derivatives such as daily opening prices, usually called daily prices, etc.) (Burgess 2010; Kirkpatrick and Dahlquist 2010; Schlossberg 2012). -

Japanese Candlestick Patterns

Presents Japanese Candlestick Patterns www.ForexMasterMethod.com www.ForexMasterMethod.com RISK DISCLOSURE STATEMENT / DISCLAIMER AGREEMENT Trading any financial market involves risk. This course and all and any of its contents are neither a solicitation nor an offer to Buy/Sell any financial market. The contents of this course are for general information and educational purposes only (contents shall also mean the website http://www.forexmastermethod.com or any website the content is hosted on, and any email correspondence or newsletters or postings related to such website). Every effort has been made to accurately represent this product and its potential. There is no guarantee that you will earn any money using the techniques, ideas and software in these materials. Examples in these materials are not to be interpreted as a promise or guarantee of earnings. Earning potential is entirely dependent on the person using our product, ideas and techniques. We do not purport this to be a “get rich scheme.” Although every attempt has been made to assure accuracy, we do not give any express or implied warranty as to its accuracy. We do not accept any liability for error or omission. Examples are provided for illustrative purposes only and should not be construed as investment advice or strategy. No representation is being made that any account or trader will or is likely to achieve profits or losses similar to those discussed in this report. Past performance is not indicative of future results. By purchasing the content, subscribing to our mailing list or using the website or contents of the website or materials provided herewith, you will be deemed to have accepted these terms and conditions in full as appear also on our site, as do our full earnings disclaimer and privacy policy and CFTC disclaimer and rule 4.41 to be read herewith. -

Futures & Options on the VIX® Index

Futures & Options on the VIX® Index Turn Volatility to Your Advantage U.S. Futures and Options The Cboe Volatility Index® (VIX® Index) is a leading measure of market expectations of near-term volatility conveyed by S&P 500 Index® (SPX) option prices. Since its introduction in 1993, the VIX® Index has been considered by many to be the world’s premier barometer of investor sentiment and market volatility. To learn more, visit cboe.com/VIX. VIX Futures and Options Strategies VIX futures and options have unique characteristics and behave differently than other financial-based commodity or equity products. Understanding these traits and their implications is important. VIX options and futures enable investors to trade volatility independent of the direction or the level of stock prices. Whether an investor’s outlook on the market is bullish, bearish or somewhere in-between, VIX futures and options can provide the ability to diversify a portfolio as well as hedge, mitigate or capitalize on broad market volatility. Portfolio Hedging One of the biggest risks to an equity portfolio is a broad market decline. The VIX Index has had a historically strong inverse relationship with the S&P 500® Index. Consequently, a long exposure to volatility may offset an adverse impact of falling stock prices. Market participants should consider the time frame and characteristics associated with VIX futures and options to determine the utility of such a hedge. Risk Premium Yield Over long periods, index options have tended to price in slightly more uncertainty than the market ultimately realizes. Specifically, the expected volatility implied by SPX option prices tends to trade at a premium relative to subsequent realized volatility in the S&P 500 Index. -

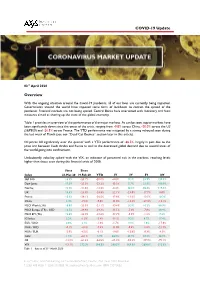

COVID-19 Update Overview

COVID-19 Update 03rd April 2020 Overview With the ongoing situation around the Covid-19 pandemic, all of our lives are currently being impacted. Governments around the world have imposed some form of lockdown to contain the spread of the pandemic. Financial markets are not being spared. Central Banks have intervened with monetary and fiscal measures aimed at shoring up the state of the global economy. Table 1 provides an overview of the performance of the major markets. As can be seen, equity markets have been significantly down since the onset of the crisis, ranging from -9.8% across China, -20.0% across the US (S&P500) and -26.5% across France. The YTD performance was mitigated by a strong rebound seen during the last week of March (see our “Dead Cat Bounce” section later in this article). Oil prices fell significantly over the quarter with a YTD performance of -66.5%, largely in part due to the price war between Saudi Arabia and Russia as well as the decreased global demand due to several areas of the world going into confinement. Undoubtedly volatility spiked with the VIX, an indicator of perceived risk in the markets, reaching levels higher than those seen during the financial crisis of 2008. Since Since Index 23-Mar-20 19-Feb-20 YTD 1Y 3Y 5Y 10Y S&P 500 15.5% -23.7% -20.0% -8.8% 9.1% 23.9% 120.3% Dow Jones 17.9% -25.3% -23.2% -15.5% 5.7% 21.9% 100.9% Nasdaq 12.2% -21.6% -14.2% -0.4% 30.2% 55.6% 219.4% UK 13.6% -23.9% -24.8% -22.1% -23.0% -17.7% 0.0% France 12.3% -28.1% -26.5% -17.8% -13.6% -13.5% 10.3% China 3.4% -7.6% -9.8% -11.0% -

The DB Currency Volatility Index (CVIX): a Benchmark for Volatility

Global Foreign Excahnge Deutsche Bank@ October 2007 Deutsche Bank Guide To Currency Indices Global Markets Saravelos Global Hzead Global Head FX StrategyBilal Jason Rashid James Torquil George Hafeez Batt Hoosenally Malcolm Wheatley Editor Contributors George Saravelos Mirza Baig Jason Batt Bilal Hafeez FX Strategy EM FX Strategy Global Head Global Head FX Index Products FX Strategy Rashid Hoosenally Caio Natividade James Malcolm Global Head FX Derivatives Strategy EM FX Strategy Global Risk Strategy Deutsche Bank@ Guide to Currency Indices October 2007 Table of Contents Introduction............................................................................................................................. 3 Overview ................................................................................................................................ 4 The Deutsche Bank Menu of Currency Indices...................................................................... 7 Currency Markets: Money Left on the Table?........................................................................ 9 Tactical Currency Indices DB G10 Trade-Weighted Indices: From Theory to Practice.................................................. 18 DB EM Asia Policy Baskets .................................................................................................. 22 The Emerging Asia Reserves, Liquidity and Yield (EARLY) Index......................................... 26 The DB Currency Volatility Index (CVIX): A Benchmark for Volatility ................................... -

Development and Analysis of a Trading Algorithm Using Candlestick Patterns

COMP 4971C – Independent Study (Summer 2016) DEVELOPMENT AND ANALYSIS OF A TRADING ALGORITHM USING CANDLESTICK PATTERNS By MUTHUKUMAR, Sivaraam Year 4, Dual Degree in Technology and Management (MEGBA) [email protected] 11th August 2016 Supervised by: Dr David Rossiter Department of Computer Science and Engineering Development and Analysis of a Trading Algorithm using Candlestick Patterns Table of Contents ABSTRACT .................................................................................................................................. 3 INTRODUCTION ......................................................................................................................... 3 Assumptions .......................................................................................................................... 3 PROCESS FLOW .......................................................................................................................... 4 GETTING DATA ........................................................................................................................... 5 Assumptions .......................................................................................................................... 5 COLOUR CODING THE CANDLESTICK CHART ............................................................................. 5 Assumptions .......................................................................................................................... 6 Colour coding algorithm ....................................................................................................... -

VIX Futures As a Market Timing Indicator

Journal of Risk and Financial Management Article VIX Futures as a Market Timing Indicator Athanasios P. Fassas 1 and Nikolas Hourvouliades 2,* 1 Department of Accounting and Finance, University of Thessaly, Larissa 41110, Greece 2 Department of Business Studies, American College of Thessaloniki, Thessaloniki 55535, Greece * Correspondence: [email protected]; Tel.: +30-2310-398385 Received: 10 June 2019; Accepted: 28 June 2019; Published: 1 July 2019 Abstract: Our work relates to the literature supporting that the VIX also mirrors investor sentiment and, thus, contains useful information regarding future S&P500 returns. The objective of this empirical analysis is to verify if the shape of the volatility futures term structure has signaling effects regarding future equity price movements, as several investors believe. Our findings generally support the hypothesis that the VIX term structure can be employed as a contrarian market timing indicator. The empirical analysis of this study has important practical implications for financial market practitioners, as it shows that they can use the VIX futures term structure not only as a proxy of market expectations on forward volatility, but also as a stock market timing tool. Keywords: VIX futures; volatility term structure; future equity returns; S&P500 1. Introduction A fundamental principle of finance is the positive expected return-risk trade-off. In this paper, we examine the dynamic dependencies between future equity returns and the term structure of VIX futures, i.e., the curve that connects daily settlement prices of individual VIX futures contracts to maturities across time. This study extends the VIX futures-related literature by testing the market timing ability of the VIX futures term structure regarding future stock movements. -

Candlestick Patterns

INTRODUCTION TO CANDLESTICK PATTERNS Learning to Read Basic Candlestick Patterns www.thinkmarkets.com CANDLESTICKS TECHNICAL ANALYSIS Contents Risk Warning ..................................................................................................................................... 2 What are Candlesticks? ...................................................................................................................... 3 Why do Candlesticks Work? ............................................................................................................. 5 What are Candlesticks? ...................................................................................................................... 6 Doji .................................................................................................................................................... 6 Hammer.............................................................................................................................................. 7 Hanging Man ..................................................................................................................................... 8 Shooting Star ...................................................................................................................................... 8 Checkmate.......................................................................................................................................... 9 Evening Star ....................................................................................................................................