A Bridge to a Greener Greece a Realistic Assessment of CCS Potential

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Verification of Vulnerable Zones Identified Under the Nitrate Directive \ and Sensitive Areas Identified Under the Urban Waste W

CONTENTS 1 INTRODUCTION 1 1.1 THE URBAN WASTEWATER TREATMENT DIRECTIVE (91/271/EEC) 1 1.2 THE NITRATES DIRECTIVE (91/676/EEC) 3 1.3 APPROACH AND METHODOLOGY 4 2 THE OFFICIAL GREEK DESIGNATION PROCESS 9 2.1 OVERVIEW OF THE CURRENT SITUATION IN GREECE 9 2.2 OFFICIAL DESIGNATION OF SENSITIVE AREAS 10 2.3 OFFICIAL DESIGNATION OF VULNERABLE ZONES 14 1 INTRODUCTION This report is a review of the areas designated as Sensitive Areas in conformity with the Urban Waste Water Treatment Directive 91/271/EEC and Vulnerable Zones in conformity with the Nitrates Directive 91/676/EEC in Greece. The review also includes suggestions for further areas that should be designated within the scope of these two Directives. Although the two Directives have different objectives, the areas designated as sensitive or vulnerable are reviewed simultaneously because of the similarities in the designation process. The investigations will focus upon: • Checking that those waters that should be identified according to either Directive have been; • in the case of the Nitrates Directive, assessing whether vulnerable zones have been designated correctly and comprehensively. The identification of vulnerable zones and sensitive areas in relation to the Nitrates Directive and Urban Waste Water Treatment Directive is carried out according to both common and specific criteria, as these are specified in the two Directives. 1.1 THE URBAN WASTEWATER TREATMENT DIRECTIVE (91/271/EEC) The Directive concerns the collection, treatment and discharge of urban wastewater as well as biodegradable wastewater from certain industrial sectors. The designation of sensitive areas is required by the Directive since, depending on the sensitivity of the receptor, treatment of a different level is necessary prior to discharge. -

For Municipal Solid Waste Management in Greece

Journal of Open Innovation: Technology, Market, and Complexity Article Description and Economic Evaluation of a “Zero-Waste Mortar-Producing Process” for Municipal Solid Waste Management in Greece Alexandros Sikalidis 1,2 and Christina Emmanouil 3,* 1 Amsterdam Business School, Accounting Section, University of Amsterdam, 1012 WX Amsterdam, The Netherlands 2 Faculty of Economics, Business and Legal Studies, International Hellenic University, 57001 Thessaloniki, Greece 3 School of Spatial Planning and Development, Aristotle University of Thessaloniki, 54124 Thessaloniki, Greece * Correspondence: [email protected]; Tel.: +30-2310-995638 Received: 2 July 2019; Accepted: 19 July 2019; Published: 23 July 2019 Abstract: The constant increase of municipal solid wastes (MSW) as well as their daily management pose a major challenge to European countries. A significant percentage of MSW originates from household activities. In this study we calculate the costs of setting up and running a zero-waste mortar-producing (ZWMP) process utilizing MSW in Northern Greece. The process is based on a thermal co-processing of properly dried and processed MSW with raw materials (limestone, clay materials, silicates and iron oxides) needed for the production of clinker and consequently of mortar in accordance with the Greek Patent 1003333, which has been proven to be an environmentally friendly process. According to our estimations, the amount of MSW generated in Central Macedonia, Western Macedonia and Eastern Macedonia and Thrace regions, which is conservatively estimated at 1,270,000 t/y for the year 2020 if recycling schemes in Greece are not greatly ameliorated, may sustain six ZWMP plants while offering considerable environmental benefits. This work can be applied to many cities and areas, especially when their population generates MSW at the level of 200,000 t/y, hence requiring one ZWMP plant for processing. -

Registration Certificate

1 The following information has been supplied by the Greek Aliens Bureau: It is obligatory for all EU nationals to apply for a “Registration Certificate” (Veveosi Engrafis - Βεβαίωση Εγγραφής) after they have spent 3 months in Greece (Directive 2004/38/EC).This requirement also applies to UK nationals during the transition period. This certificate is open- dated. You only need to renew it if your circumstances change e.g. if you had registered as unemployed and you have now found employment. Below we outline some of the required documents for the most common cases. Please refer to the local Police Authorities for information on the regulations for freelancers, domestic employment and students. You should submit your application and required documents at your local Aliens Police (Tmima Allodapon – Τμήμα Αλλοδαπών, for addresses, contact telephone and opening hours see end); if you live outside Athens go to the local police station closest to your residence. In all cases, original documents and photocopies are required. You should approach the Greek Authorities for detailed information on the documents required or further clarification. Please note that some authorities work by appointment and will request that you book an appointment in advance. Required documents in the case of a working person: 1. Valid passport. 2. Two (2) photos. 3. Applicant’s proof of address [a document containing both the applicant’s name and address e.g. photocopy of the house lease, public utility bill (DEH, OTE, EYDAP) or statement from Tax Office (Tax Return)]. If unavailable please see the requirements for hospitality. 4. Photocopy of employment contract. -

1 from City-State to Region-State

The Athenian Experiment: Building an Imagined Political Community in Ancient Attica, 508-490 B.C. Greg Anderson http://www.press.umich.edu/titleDetailDesc.do?id=17798 The University of Michigan Press 1 FROM CITY-STATE TO REGION-STATE What exactly do we mean when we say that Attica in the classical period was politically “incorporated” or “uniµed”? If, for the purposes of analysis, we unpack the idea of the polis, we can distinguish three essential levels or sources of political unity in the Attic peninsula. First and most fundamental, the reach of Athenian state institutions ex- tended to the territorial limits of Attica, and this apparatus was recognized as the ultimate locus of political authority for the entire region. Second, all free, native-born, adult males in Attica were eligible to become citizens of Athens, entitling them—even obliging them—to participate in the civil, military, and religious life of the polis. From / on, enrollment took place locally in one of town and village units, or demes, scattered throughout the peninsula and was administered by one’s fellow demesmen. Third, despite the unusually large size of the polis, citizens appear to have been bound to one another by a pow- erful and at times distinctly chauvinistic form of collective consciousness or identity. Each citizen was encouraged to imagine himself a member of a sin- gle, extended, undifferentiated community of “Athenians,” sharing with his fellows a common history, culture, and destiny that set them apart from all other such communities. For most modern authorities, these distinctions will seem artiµcial and per- haps anachronistic, since it is widely felt that, unlike the nation-states of our own times, the Greek polis in general and the Athenian instance in particular 13 The Athenian Experiment: Building an Imagined Political Community in Ancient Attica, 508-490 B.C. -

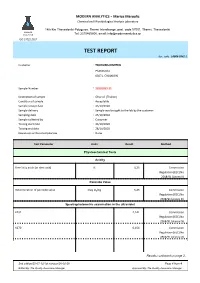

TEST REPORT Doc

MODERN ANALYTICS - Marios Maroulis Chemical and Microbiological Analysis Laboratory 14th Km Thessaloniki-Polygyros, Thermi Interchange, post. code 57001, Thermi, Thessaloniki MODERN ANALYTICS Tel: 2310465600, email: [email protected] ISO 17025:2017 TEST REPORT doc. code : LAB06-03#2-1 Customer : TSIKOURIS DIMITRIS PSAKOUDIA 63071, CHALKIDIKI Sample Number : 20201023-21 Description of sample : Olive oil [Thallon] Condition of sample : Acceptable Sample receipt date : 23/10/2020 Sample delivery : Sample was brought to the lab by the customer Sampling date : 23/10/2020 Sample collected by : Customer Testing start date : 23/10/2020 Testing end date : 26/10/2020 Deviations or Non-Compliances : None Test Parameter Units Result Method Physicochemical Tests Acidity Free fatty acids (as oleic acid) % 0,23 Commission Regulation (EEC) No 2568/91 (Annex II) Peroxide Value Determination of peroxide value meq O₂/Kg 6,46 Commission Regulation (EEC) No 2568/91 (Annex III) Spectrophotometric examination in the ultraviolet Κ232 2,141 Commission Regulation (EEC) No 2568/91 (Annex IX) Κ270 0,154 Commission Regulation (EEC) No 2568/91 (Annex IX) Results continued on page 2... 2nd edition/25-07-12/1st revision/20-02-20 Page 1 from 4 Edited By: The Quality Assurance Manager Approved By: The Quality Assurance Manager MODERN ANALYTICS - Marios Maroulis Chemical and Microbiological Analysis Laboratory 14th Km Thessaloniki-Polygyros, Thermi Interchange, post. code 57001, Thermi, Thessaloniki MODERN ANALYTICS Tel: 2310465600, email: [email protected] -

Generation 2.0 for Rights, Equality & Diversity

Generation 2.0 for Rights, Equality & Diversity Intercultural Mediation, Interpreting and Consultation Services in Decentralised Administration Immigration Office Athens A (IO A) January 2014 - now On 1st January 2014, the One Stop Shop was launched and all the services issuing and renewing residence permits for immigrants in Greece were moved from the municipalities to Decentralised Administrations. Namely, the 66 Attica municipalities were shared between 4 Immigration Offices of the Attic Decentralised Administration. a) Immigration Office for Athens A with territorial jurisdiction over residents of the Municipality of Athens, Address: Salaminias 2 & Petrou Ralli, Athens 118 55 b) Immigration Office for Central Athens and West Attica, with territorial jurisdiction over residents of the following Municipalities; i) Central Athens: Filadelfeia-Chalkidona, Galatsi, Zografou, Kaisariani, Vyronas, Ilioupoli, Dafni-Ymittos, ii) West Athens: Aigaleo Peristeri, Petroupoli, Chaidari, Agia Varvara, Ilion, Agioi Anargyroi- Kamatero, and iii) West Attica: Aspropyrgos, Eleusis (Eleusis-Magoula) Mandra- Eidyllia (Mandra - Vilia - Oinoi - Erythres), Megara (Megara-Nea Peramos), Fyli (Ano Liosia - Fyli - Zefyri). Address: Salaminias 2 & Petrou Ralli, Athens 118 55 c) Immigration Office for North Athens and East Attica with territorial jurisdiction over residents of the following Municipalities; i) North Athens: Penteli, Kifisia-Nea Erythraia, Metamorfosi, Lykovrysi-Pefki, Amarousio, Fiothei-Psychiko, Papagou- Cholargos, Irakleio, Nea Ionia, Vrilissia, -

Technical Report Skouries Project Greece

Technical Report Skouries Project Greece Centered on Latitude 40° 29’and Longitude 23°42’ Effective Date: January 01, 2018 Prepared by: Eldorado Gold Corporation 1188 Bentall 5 - 550 Burrard Street Vancouver, BC V6C 2B5 Qualified Person Company Mr. Richard Alexander, P.Eng. Eldorado Gold Corporation Dr. Stephen Juras, P.Geo. Eldorado Gold Corporation Mr. Paul Skayman, FAusIMM Eldorado Gold Corporation Mr. Colm Keogh, P.Eng. Eldorado Gold Corporation Mr. John Nilsson, P.Eng. Nilsson Mine Services Ltd. S KOURIES P ROJECT, G REECE T ECHNICAL R EPORT TABLE OF CONTENTS SECTION • 1 SUMMARY ................................................................................................................ 1-1 1.1 Introduction ................................................................................................... 1-1 1.2 Property Description ..................................................................................... 1-2 1.3 Permitting ..................................................................................................... 1-2 1.4 History........................................................................................................... 1-3 1.5 Deposit Geology ........................................................................................... 1-4 1.6 Metallurgical Testwork .................................................................................. 1-4 1.7 Mineral Resources ........................................................................................ 1-5 1.8 Mineral Reserves ......................................................................................... -

11A, Othonos Hounta, 19002 - Paiania, Attikis, Hellas Telephone +30 6944290651 Fax +30 211 3657950 E-Mail [email protected]

N IKOS G OURAROS CURRICULUM VITAE J UNE 2004 PERSONAL INFORMATION Name GOURAROS NIKOS Address 11A, Othonos Hounta, 19002 - Paiania, Attikis, Hellas Telephone +30 6944290651 Fax +30 211 3657950 E-mail [email protected] Nationality Greek Date of birth 10/12/1970 WORK EXPERIENCE • Dates (from – to) February 1999 – Today (June 2004) • Name and address of employer Lambrakis Press Organization, Sector of Informatics and New Technologies • Type of business or sector Publishing, Newspapers, Magazines, Electronic Publications • Occupation or position held Director of Archives • Main activities and responsibilities Management : a . Cataloguing, Digitization, Digital Library Development of the Group’s content from 1922 to date (The largest digitization project in Greece), b. exploitation of the digitized content, c. development of 3 software packages for the creation, management and electronic publishing of digital archives of newspapers ( e-preserve newspapers), magazines (e-preserve magazines), and assets (e-preserve assets: documents, photos, manuscripts, maps, icons, video, sound) d. proposal preparations for research programs • Dates (from – to) September 1998, February 1999 • Name and address of employer Lambrakis Press Organisation • Type of business or sector Publishing, Newspapers, Magazines, Electronic Publications • Occupation or position held Head of Design • Main activities and responsibilities Responsible for the design of the Digital Archival Library Page 1 - Curriculum vitae of Gouraros, Nikos – June 2004 FREELANCE WORK • Dates (from – to) September 1998 – Today (January 2004) [freelance work] • Name and address of employer Center of Neo-Hellenic Studies • Type of business or sector Non-Profit Organisation, for the promotion of Modern Greek Literature and Culture, both in Greece and abroad. The Cavafy Archive • Occupation or position held Head Advisor for the Electronic Publications, Head of Digital Library Design (The first Digital Library for the Hellenic Literature) • Main activities and responsibilities Project Management consultant for a. -

The Cognitive Benefits of Learning Native Language

Short Communication Open Access J Neurol Neurosurg Volume 10 Issue 3 - March 2019 DOI: 10.19080/OAJNN.2019.10.555788 Copyright © All rights are reserved by Genc Struga The Cognitive Benefits of Learning Native Language Genc Struga1* and Thomas Bak2 1Department of Neuroscience, University Hospital Mother Teresa, Albania 2Department of Psychology, Psychology and Language Sciences University of Edinburgh, UK Submission: February 05, 2019; Published: March 26, 2019 *Corresponding author: Genc Struga, Department of Neuroscience, University Hospital Mother Teresa, Albania Abstract Background The cognitive benefits of learning native language and bilingualism project focuses on Arvanites, a bilingual population in Greece that speak theAvantika, ability a for dialect further of learningAlbanian and language acquisition still spokenof other in languages. vast areas of Greece. It is classified as a minority and an endagered language and is considered in risk of extinction. The project aims to examine possible cognitive benefits of bilingualism in native speakers of Avantika, including Method We aim to achieve statistically important number of Arvanites equal Bilingual and monolingual to be interview using a up to date questionnaire and TEA or TEA like cognitive screening. This is a cross-sectional population study including bilingual and monolingual speakers orwithout 15% ofexclusion population. criteria and with respects to gender equality, stratified random sampling responders in the areas where Arvanite population traditionally lived achieving -

Civil Affairs Handbook on Greece

Preliminary Draft CIVIL AFFAIRS HANDBOOK on GREECE feQfiJtion Thirteen on fcSSLJC HJI4LTH 4ND S 4 N 1 T £ T I 0 N THE MILITARY GOVERNMENT DIVISION OFFICE OF THE PROVOST MARSHAL GENERAL Preliminary Draft INTRODUCTION Purposes of the Civil Affairs Handbook. International Law places upon an occupying power the obligation and responsibility for establishing government and maintaining civil order in the areas occupied. The basic purposes of civil affairs officers are thus (l) to as- sist the Commanding General of the combat units by quickly establishing those orderly conditions which will contribute most effectively to the conduct of military operations, (2) to reduce to a minimum the human suffering and the material damage resulting from disorder and (3) to create the conditions which will make it possible for civilian agencies to function effectively. The preparation of Civil Affairs Handbooks is a part of the effort of the War Department to carry out this obligation as efficiently and humanely as is possible. The Handbooks do not deal with planning or policy. They are rather ready reference source books of the basic factual information needed for planning and policy making. Public Health and Sanitation in Greece. As a result of the various occupations, Greece presents some extremely difficult problems in health and sanitation. The material in this section was largely prepared by the MILBANK MEMORIAL FUND and the MEDICAL INTELLI- GENCE BRANCH OF THE OFFICE OF THE SURGEON GENERAL. If additional data on current conditions can be obtained, it willJse incorporated in the final draft of the handbook for Greece as a whole. -

14.7.2010 Official Journal of the European Union C 190/37

14.7.2010 EN Official Journal of the European Union C 190/37 Publication of an application pursuant to Article 6(2) of Council Regulation (EC) No 510/2006 on the protection of geographical indications and designations of origin for agricultural products and foodstuffs (2010/C 190/08) This publication confers the right to object to the application pursuant to Article 7 of Council Regulation (EC) No 510/2006 ( 1). Statements of objection must reach the Commission within six months from the date of this publication. SUMMARY COUNCIL REGULATION (EC) No 510/2006 ‘ΠΡΑΣΙΝΕΣ ΕΛΙΕΣ ΧΑΛΚΙΔΙΚΗΣ’ (PRASINES ELIES CHALKIDIKIS) EC No: EL-PDO-0005-0539-27.03.2006 PDO ( X ) PGI ( ) This summary sets out the main features of the product specifications for information purposes. 1. Responsible department in the Member State: Name: Υπουργείο Αγροτικής Ανάπτυξης και Τροφίμων., Δ/νση Βιολογικής Γεωργίας,Τμήμα ΠΟΠ — ΠΓΕ — Ιδιότυπων και Παραδοσιακών Προϊόντων (Ministry of Rural Development and Food, Organic Farming Department, PDO/PGI/Special and Traditional Products Section) Address: Αχαρνών 29/Acharnon 29 104 39 Αθήνα/Athens ΕΛΛΑΔΑ/GREECE Tel. +30 2102125152 Fax — E-mail: [email protected] 2. Group: Name: Κοινοπραξία Ενώσεων Αγροτικών Συνεταιρισμών Πολυγύρου και Χαλκιδικής (Association of Unions of Farmers’ Cooperatives of Polygyros and Chalkidiki), with the trade name ‘Βιοκαλλιεργητική Χαλκιδικής’ (Viokallieryitiki Chalkidikis) Address: Κωνσταντινουπόλεως 13/Konstantinoupoleos 13 631 00 Πολύγυρος/Polygyros ΕΛΛΑΔΑ/GREECE Tel. +30 2371023076 Fax — E-mail: [email protected] Composition: Producers/processors ( X ) Other ( ) 3. Type of product: Class 1.6 — Fruit, vegetables and cereals, fresh or processed 4. Specification: (summary of requirements under Article 4(2) of Regulation (EC) No 510/2006) 4.1. -

Visa & Residence Permit Guide for Students

Ministry of Interior & Administrative Reconstruction Ministry of Foreign Affairs Directorate General for Citizenship & C GEN. DIRECTORATE FOR EUROPEAN AFFAIRS Immigration Policy C4 Directorate Justice, Home Affairs & Directorate for Immigration Policy Schengen Email: [email protected] Email: [email protected] www.ypes.gr www.mfa.gr Visa & Residence Permit guide for students 1 Index 1. EU/EEA Nationals 2. Non EU/EEA Nationals 2.a Mobility of Non EU/EEA Students - Moving between EU countries during my short-term visit – less than three months - Moving between EU countries during my long-term stay – more than three months 2.b Short courses in Greek Universities, not exceeding three months. 2.c Admission for studies in Greek Universities or for participation in exchange programs, under bilateral agreements or in projects funded by the European Union i.e “ERASMUS + (placement)” program for long-term stay (more than three months). - Studies in Greek universities (undergraduate, master and doctoral level - Participation in exchange programs, under interstate agreements, in cooperation projects funded by the European Union including «ERASMUS+ placement program» 3. Refusal of a National Visa (type D)/Rights of the applicant. 4. Right to appeal against the decision of the Consular Authority 5. Annex I - Application form for National Visa (sample) Annex II - Application form for Residence Permit Annex III - Refusal Form Annex IV - Photo specifications for a national visa application Annex V - Aliens and Immigration Departments Contacts 2 1. Students EU/EEA Nationals You will not require a visa for studies to enter Greece if you possess a valid passport from an EU Member State, Iceland, Liechtenstein, Norway or Switzerland.