Leading Multinationals from Taiwan Increase Their Foreign Assets Despite the Global Crisis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Reply Brief of Petitioners

No. 06-937 In the Supreme Court of the United States QUANTA COMPUTER, INC., QUANTA COMPUTER USA, INC., Q-LITY COMPUTER, INC., COMPAL ELECTRONICS, INC., BIZCOM ELECTRONICS, INC., SCEPTRE TECHNOLOGIES, INC., FIRST INTERNATIONAL COMPUTER, INC. AND FIRST INTERNATIONAL COMPUTER OF AMERICA, INC., PETITIONERS, V. LG ELECTRONICS, INC., RESPONDENT. ON PETITION FOR A WRIT OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR THE FEDERAL CIRCUIT REPLY BRIEF OF PETITIONERS TERRENCE D. GARNETT MAUREEN E. MAHONEY VINCENT K. YIP Counsel of Record PETER WIED J. SCOTT BALLENGER PAUL, HASTINGS, JANOFSKY ANNE W. ROBINSON & WALKER LLP LATHAM & WATKINS LLP 515 SOUTH FLOWER STREET 555 11TH STREET N.W. 25TH FLOOR SUITE 1000 LOS ANGELES, CA 90071 WASHINGTON, D.C. 20004 (213) 683-6000 (202) 637-2200 Counsel for Quanta Computer, Counsel for Petitioners Inc., Quanta Computer USA, Inc., Q-Lity Computer, Inc. Additional Counsel Listed on Inside Cover MAXWELL A. FOX WILLIAM J. ANTHONY, JR. PAUL, HASTINGS, JANOFSKY ERIC L. WESENBERG & WALKER LLP KAI TSENG 34 F ARK MORI BUILDING MATTHEW J. HULT P.O. BOX 577 ROWENA Y. YOUNG 12-32 AKASAKA 1-CHOME ORRICK, HERRINGTON MINATO-KU, TOKYO 107-6034 & SUTCLIFFE LLP JAPAN 1000 MARSH ROAD 813 6229 6100 MENLO PARK, CA 94025 Counsel for Quanta (650) 614-7400 Computer, Inc., Quanta Counsel for Compal Electronics, Computer USA, Inc., Q-Lity Inc., Bizcom Electronics, Inc., Computer, Inc. Sceptre Technologies, Inc. RONALD S. LEMIEUX PAUL, HASTINGS, JANOFSKY & WALKER LLP 5 PALO ALTO SQUARE 6TH FLOOR PALO ALTO, CA 94306 Counsel for First International Computer, Inc. and First International Computer of America, Inc. -

Global Capital, the State, and Chinese Workers: the Foxconn Experience

MCX38410.1177/0097700 447164412447164Pun and ChanModern China © 2012 SAGE Publications Reprints and permission: sagepub.com/journalsPermissions.nav Articles Modern China 38(4) 383 –410 Global Capital, the State, © 2012 SAGE Publications Reprints and permission: and Chinese Workers: sagepub.com/journalsPermissions.nav DOI: 10.1177/0097700412447164 The Foxconn Experience http://mcx.sagepub.com Pun Ngai1 and Jenny Chan2 Abstract In 2010, a startling 18 young migrant workers attempted suicide at Foxconn Technology Group production facilities in China. This article looks into the development of the Foxconn Corporation to understand the advent of capi- tal expansion and its impact on frontline workers’ lives in China. It also pro- vides an account of how the state facilitates Foxconn’s production expansion as a form of monopoly capital. Foxconn stands out as a new phenomenon of capital expansion because of the incomparable speed and scale of its capital accumulation in all regions of China. This article explores how the workers at Foxconn, the world’s largest electronics manufacturer, have been subjected to work pressure and desperation that might lead to suicides on the one hand but also open up daily and collective resistance on the other hand. Keywords global capital, Chinese state, student workers, rural migrant workers, Foxconn Technology Group When Time magazine nominated workers in China as the runners-up for the 2009 Person of the Year, the editor commented that Chinese workers have brightened the future of humanity by “leading the world to economic 1Hong Kong Polytechnic University, Kowloon, Hong Kong 2Royal Holloway, University of London, Surrey, UK Corresponding Author: Pun Ngai, Department of Applied Social Sciences, Hong Kong Polytechnic University, Kowloon, Hong Kong Email: [email protected] 384 Modern China 38(4) recovery” (Time, Dec. -

USD XINT M EM HL Taiwan NTR USD Index

Created on 30 th April 2020 XINT M EM HL Taiwan NTR USD Index USD The XINT M EM HL Taiwan NTR USD Index covers the highly liquid and liquid segment of the Taiwanese equity market. The index membership comprises the 89 largest companies by freefloat adjusted market value and represents approximately 85% of the Taiwanese market. INDEX PERFORMANCE - PRICE RETURN USD 130 120 110 100 90 80 70 Dec 2017 Mar 2018 Jun 2018 Sep 2018 Dec 2018 Mar 2019 Jun 2019 Sep 2019 Dec 2019 Mar 2020 Index Return % annualised Standard Deviation % annualised Maximum Drawdown 3M -7.33 3M 36.87 From 14 Jan 2020 6M 1.07 6M 27.83 To 19 Mar 2020 1Y 11.14 1Y 22.27 Return -29.23% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com TOP 10 Largest Constituents FFMV million Weight Industry Sector Taiwan Semiconductor Man Co Ltd 37.57% 252,160 37.57% Technology Hon Hai Precision Industry Co Ltd 4.81% 32,296 4.81% Industrial Goods & Services MediaTek Inc 3.14% 21,069 3.14% Technology Chunghwa Telecom Co Ltd 2.08% 13,992 2.08% Telecommunications Largan Precision Co Ltd 2.07% 13,900 2.07% Personal & Household Goods Formosa Plastics Corp 1.96% 13,167 1.96% Chemicals CTBC Financial Holding Co Ltd 1.86% 12,453 1.86% Banks Nan Ya Plastics Corp 1.71% 11,472 1.71% Chemicals Uni-President Enterprises Corp 1.68% 11,284 1.68% Food & Beverage Mega Financial Holding Co Ltd 1.64% 11,009 1.64% Banks Total 392,803 58.52% This information has been prepared by Index Intelligence GmbH (“IIG”). -

Representative Legal Matters Mark W.C

Representative Legal Matters Mark W.C. Tu Represented KKR in relation to its proposed buyout of Yageo Corporation. Represented Advanced Semiconductor Engineering Inc. in its acquisition of 100 percent shares of PowerASE Technology by way of tender offer and merger. Represented Morgan Stanley, the financial advisor to Polaris Securities Corporation, in relation to its share swap with Yuanta Financial Holding Company. Represented MediaTek Inc. for acquisition of 100 percent of outstanding shares of Ralink Technology Corporation by way of a share swap. Represented Chimei Optoelectronics Corporation in relation to its merger with Innolux Corporation. Represented Morgan Stanley, the financial advisor to Taiwan International Securities Corporation (TISC), in relation to the sale of all issued and outstanding shares of TISC to Capital Securities Corporation by way of a tender offer followed by a merger. Represented E.Sun Commercial Bank in its general business and asset assumption from Chu Nan Co-operative Credit Association. Represented Prime View International Co., Ltd. in relation to its acquisition of E. Ink Corporation by way of a share exchange. Represented Morgan Stanley Private Equity in its acquisition of a stake in CTCI Corporation. Representing WIN Semiconductors Corporation in relation to its issuance of global depositary receipts. Represented E.Sun Financial Holding Company. in relation to its issuance of global depositary receipts. Represented Cathay Financial Holding Company in relation to its issuance of European convertible bonds. Represented Chunghwa Telecom Co., Ltd. in relation to its Form 20-F filing submitted to the U.S. Securities and Exchange Commission. Represented Pegatron Corporation in relation to its issuance of European convertible bonds. -

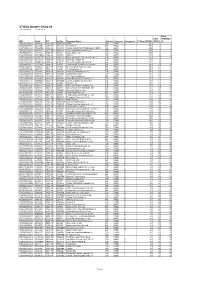

STOXX Greater China 80 Last Updated: 01.08.2017

STOXX Greater China 80 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.9 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 3 3 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 51.5 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 5 5 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 6 6 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 7 9 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 8 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 9 8 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 10 10 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 11 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 12 11 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 13 13 TW0003008009 6451668 3008.TW TW05PJ LARGAN Precision TW TWD Y 19.7 14 15 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 17 19 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. -

Formosa Plastics Corporation Financial Statements December 31, 2017 and 2016

1 Stock Code:1301 (English Translation of Financial Statements and Report Originally Issued in Chinese) FORMOSA PLASTICS CORPORATION FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 (With Independent Auditors’ Report Thereon) Address:No.100, Shuiguan Rd., Renwu Dist., Kaohsiung City 814, Taiwan (R.O.C.) Telephone:(07)371-1411;(02)2712-2211 The independent auditors’ report and the accompanying financial statements are the English translation of the Chinese version prepared and used in the Republic of China. If there is any conflict between, or any difference in the interpretation of, the English and Chinese language independent auditors’ report and financial statements, the Chinese version shall prevail. 2 Table of Contents Contents Page 1. Cover Page 1 2. Table of Contents 2 3. Independent Auditors’ Report 3 4. Balance Sheets 4 5. Statements of Comprehensive Income 5 6. Statements of Changes in Equity 6 7. Statements of Cash Flows 7 8. Notes to Financial Statements (1) Company history 8 (2) Approval date and procedures of the financial statements 8 (3) Application of new standards, amendments and interpretations 8~13 (4) Summary of significant accounting policies 13~25 (5) Critical accounting judgments and key sources of estimation uncertainly 26 (6) Significant account disclosures 26~55 (7) Related-party transactions 55~61 (8) Pledged properties 61 (9) Significant commitments and contingencies 61~62 (10) Losses due to major disasters 62 (11) Subsequent events 62 (12) Other 62 (13) Other disclosures (a) Information on significant transactions 63~68 (b) Information on investees 69 (c) Information on investment in mainland China 69 (14) Segment information 69 3 KPMG 〵⻍䋑11049⥌纏騟5媯7贫68垜(〵⻍101㣐垜) Telephone ꨶ鑨 + 886 (2) 8101 6666 68F., TAIPEI 101 TOWER, No. -

Compal Electronics, Inc. and Subsidiaries

1 Stock Code:2324 COMPAL ELECTRONICS, INC. AND SUBSIDIARIES Consolidated Financial Statements With Independent Auditors’ Review Report For the Nine Months Ended September 30, 2019 and 2018 Address: No.581 & 581-1, Ruiguang Rd., Neihu District, Taipei, Taiwan Telephone: (02)8797-8588 2 Table of contents Contents Page 1. Cover Page 1 2. Table of Contents 2 3. Independent Auditors’ Review Report 3 4. Consolidated Balance Sheets 4 5. Consolidated Statements of Comprehensive Income 5 6. Consolidated Statements of Changes in Equity 6 7. Consolidated Statements of Cash Flows 7 8. Notes to the Consolidated Financial Statements (1) Company history 8 (2) Approval date and procedures of the consolidated financial statements 8 (3) New standards, amendments and interpretations adopted 8~11 (4) Summary of significant accounting policies 11~21 (5) Significant accounting assumptions and judgments, and major sources 21 of estimation uncertainty (6) Explanation of significant accounts 21~63 (7) Related-party transactions 63~65 (8) Pledged assets 65 (9) Commitments and contingencies 66 (10) Losses due to major disasters 66 (11) Subsequent events 66 (12) Other 66~67 (13) Other disclosures (a) Information on significant transactions 67, 69~79 (b) Information on investees 68, 80~85 (c) Information on investment in Mainland China 68, 86~88 (14) Segment information 68 3 Independent Auditors’ Review Report To COMPAL ELECTRONICS, INC.: Introduction We have reviewed the accompanying consolidated balance sheets of COMPAL ELECTRONICS, INC. (the “Company”) and its subsidiaries (the “Group”) as of September 30, 2019 and 2018, and the related consolidated statements of comprehensive income for the three months and nine months then ended, as well as the changes in equity and cash flows for the nine months then ended, and notes to the consolidated financial statements, including a summary of significant accounting policies. -

Taiwan's Top 50 Corporates

Title Page 1 TAIWAN RATINGS CORP. | TAIWAN'S TOP 50 CORPORATES We provide: A variety of Chinese and English rating credit Our address: https://rrs.taiwanratings.com.tw rating information. Real-time credit rating news. Credit rating results and credit reports on rated corporations and financial institutions. Commentaries and house views on various industrial sectors. Rating definitions and criteria. Rating performance and default information. S&P commentaries on the Greater China region. Multi-media broadcast services. Topics and content from Investor outreach meetings. RRS contains comprehensive research and analysis on both local and international corporations as well as the markets in which they operate. The site has significant reference value for market practitioners and academic institutions who wish to have an insight on the default probability of Taiwanese corporations. (as of June 30, 2015) Chinese English Rating News 3,440 3,406 Rating Reports 2,006 2,145 TRC Local Analysis 462 458 S&P Greater China Region Analysis 76 77 Contact Us Iris Chu; (886) 2 8722-5870; [email protected] TAIWAN RATINGS CORP. | TAIWAN'S TOP 50 CORPORATESJenny Wu (886) 2 872-5873; [email protected] We warmly welcome you to our latest study of Taiwan's top 50 corporates, covering the island's largest corporations by revenue in 2014. Our survey of Taiwan's top corporates includes an assessment of the 14 industry sectors in which these companies operate, to inform our views on which sectors are most vulnerable to the current global (especially for China) economic environment, as well as the rising strength of China's domestic supply chain. -

This Version of Au Optronics Corp's Form 20-F, As

NOTE: THIS VERSION OF AU OPTRONICS CORP’S FORM 20-F, AS FILED WITH THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION (“SEC”) ON HTML FORMAT ON MAY 3, 2011, HAS BEEN CONVERTED FROM HTML BACK TO MICROSOFT WORD. PLEASE VISIT THE SEC’S WEBSITE AT www.sec.gov FOR THE FILED VERSION OF AU OPTRONICS CORP’S FORM 2O-F, INCLUDING THE EXHIBITS. WorldReginfo - b24d0578-faa5-4ed6-8a00-edfe430d82e2 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F (Mark One) REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2010 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ________________ to ________________ OR SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report ________________ Commission file number: 001-31335 (Exact name of Registrant as specified in its charter) AU OPTRONICS CORP. TAIWAN, REPUBLIC OF CHINA (Translation of Registrant’s name into English) (Jurisdiction of incorporation or organization) 1 LI-HSIN ROAD 2 HSINCHU SCIENCE PARK HSINCHU, TAIWAN REPUBLIC OF CHINA (Address of principal executive offices) Andy Yang 1 Li-Hsin Road 2 Hsinchu Science Park Hsinchu, Taiwan Republic of China Telephone No.: +886-3-500-8800 Facsimile No.: +886-3-564-3370 Email: [email protected] (Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act. -

Compal Electronics, Inc. and Subsidiaries

1 Stock Code:2324 COMPAL ELECTRONICS, INC. AND SUBSIDIARIES Consolidated Financial Statements With Independent Auditors’ Review Report For the Three Months Ended March 31, 2020 and 2019 Address: No.581 & 581-1, Ruiguang Rd., Neihu District, Taipei, Taiwan Telephone: (02)8797-8588 2 Table of contents Contents Page 1. Cover Page 1 2. Table of Contents 2 3. Independent Auditors’ Review Report 3 4. Consolidated Balance Sheets 4 5. Consolidated Statements of Comprehensive Income 5 6. Consolidated Statements of Changes in Equity 6 7. Consolidated Statements of Cash Flows 7 8. Notes to the Consolidated Financial Statements (1) Company history 8 (2) Approval date and procedures of the consolidated financial 8 statements (3) New standards, amendments and interpretations adopted 8~9 (4) Summary of significant accounting policies 9~16 (5) Significant accounting assumptions and judgments, and major 16~17 sources of estimation uncertainty (6) Explanation of significant accounts 17~56 (7) Related-party transactions 56~58 (8) Pledged assets 59 (9) Commitments and contingencies 59 (10) Losses due to major disasters 59 (11) Subsequent events 59 (12) Other 60 (13) Other disclosures (a) Information on significant transactions 60~61, 62~72 (b) Information on investees 61, 73~78 (c) Information on investment in mainland China 61, 79~81 (d) Major shareholders 61 (14) Segment information 61 3 Independent Auditors’ Review Report To COMPAL ELECTRONICS, INC.: Introduction We have reviewed the accompanying consolidated balance sheets of COMPAL ELECTRONICS, INC. and its subsidiaries (the “Group”) as of March 31, 2020 and 2019, and the related consolidated statements of comprehensive income, changes in equity and cash flows for the three months ended March 31, 2020 and 2019, and notes to the consolidated financial statements, including a summary of significant accounting policies. -

“UROP Has Long Represented the Opportunity to Discover, Innovate and Create New Knowledge. the EECS Superurop Promises MIT Un

“UROP has long represented the opportunity to discover, innovate and create new knowledge. The EECS SuperUROP promises MIT undergraduates an even more intensive and sustained intellectual SuperUROP experience working with our faculty. We expect EECS majors will welcome this new opportunity with enthusiasm.” — Julie B. Norman Senior Associate Dean for Undergraduate Education Director, Office of Undergraduate Advising and Academic Programming 2012– 2013 I am thrilled to celebrate the launch of the new Advanced Undergraduate Research Program in EECS, now officially known as SuperUROP. This collaboration between EECS and the MIT UROP office evolved out of the 2012 EECS strategic plan, which included strong participation from faculty, students, and staff. The program responded to my vision for creating a high caliber undergraduate research program that would produce publication- worthy results. The Undergraduate Student Advisory Group in EECS (USAGE) strongly influenced the overall structure of the program. The SuperUROP program will provide a jump-start on graduate school, act as a startup accelerator, and be an industry-training bootcamp—all rolled “Our engineering students want a into one. The response from students has been extremely positive. We have 86 students participating this inaugural year, and expect that number will deeper understanding of the topics increase in the future. they care about, and they want to apply SuperUROP students engage in a year-long research experience and participate in a course titled “Preparation for Undergraduate Research,” which covers a range of subjects, from selecting projects and research this knowledge in a way that will lead topics in EECS to entrepreneurship and ethics in engineering. -

Albert Shih ASSOCIATE

Albert Shih ASSOCIATE Litigation Palo Alto [email protected] 650-849-3022 FOCUS AREAS EXPERIENCE Albert Shih is an associate in the Palo Alto office of Wilson Sonsini Goodrich & Rosati, Litigation where his practice focuses on intellectual property litigation and counseling. He has litigated Patent Litigation more than 25 patent cases before federal district courts, the International Trade Commission, and Judicial Arbitration and Mediation Services, including a $31 million judgment obtained for his client in the field of telecommunication protocol. He also regularly advises clients on company intellectual property strategy, technology transactions, licensing negotiation, FRAND-rate setting for standard-essential patents, and patent prosecution matters. Prior to law school, Albert was a design engineer at Intel, where he taught courses at Intel University on chipset design. His field experience and knowledge allow him to understand and appreciate the unique business and technical perspective associated with leaders and innovators in the field of mobile telecommunication protocol, baseband processor, liquid crystal display, semiconductor fabrication, digital signal processors, digital receivers and tuners, image sensors, Internet security software, and various digital and analog circuit designs. Educated in Taiwan and Singapore in his early years, Albert is fluent in Mandarin Chinese. CREDENTIALS Education J.D., Loyola Law School, Los Angeles B.S., Electrical Engineering, University of Michigan, Ann Arbor Associations and Memberships Member, American Bar Association, Intellectual Property Section Member, American Intellectual Property Law Association Member, Asia Pacific Intellectual Property Association Member, International Trade Commission Trial Lawyer Association Honors Named to the 2015-2018 editions of the "Rising Stars" list published by Northern California Super Lawyers Admissions State Bar of California U.S.