HLL Infra Tech Services Limited: Ratings Reaffirmed Summary Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Sector Undertaking (Services)

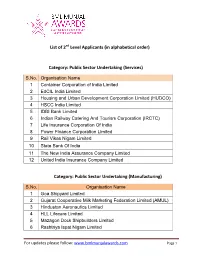

List of 2nd Level Applicants (in alphabetical order) Category: Public Sector Undertaking (Services) S.No. Organisation Name 1 Container Corporation of India Limited 2 EdCIL India Limited 3 Housing and Urban Development Corporation Limited (HUDCO) 4 HSCC India Limited 5 IDBI Bank Limited 6 Indian Railway Catering And Tourism Corporation (IRCTC) 7 Life Insurance Corporation Of India 8 Power Finance Corporation Limited 9 Rail Vikas Nigam Limited 10 State Bank Of India 11 The New India Assurance Company Limited 12 United India Insurance Company Limited Category: Public Sector Undertaking (Manufacturing) S.No. Organisation Name 1 Goa Shipyard Limited 2 Gujarat Cooperative Milk Marketing Federation Limited (AMUL) 3 Hindustan Aeronautics Limited 4 HLL Lifecare Limited 5 Mazagon Dock Shipbuilders Limited 6 Rashtriya Ispat Nigam Limited For updates please follow: www.bmlmunjalawards.com Page 1 List of 2nd Level Applicants (in alphabetical order) Category: Private Sector (Services) S.No. Organisation Name 1 Adani Ports and Special Economic Zone Limited 2 Aditya Birla Financial Services Limited 3 Aspire Systems India Private Limited 4 Axis Bank 5 Bajaj Allianz General Insurance Company Limited 6 Bata India Limited 7 Bausch & Lomb India Private Limited 8 Bharat Hotels Limited 9 Bharti Realty Holdings Limited 10 Boeing International Corporation India Private Limited 11 Cyient Limited 12 DTDC Express Limited 13 ECOS (India) Mobility & Hospitality Private Limited 14 Feedback Infra Private Limited 15 Ferns & Petals Private Limited 16 Gmmco Limited 17 -

Tender Document

TENDER DOCUMENT SUPPLY, INSTALLATION, COMMISIONING & MAINTENANCE OF MEDICAL GAS PIPELINE SYSTEM ON TURNKEY BASIS AT DR. SUSHILATIWARI STATE HOSPITAL, HALDWANI IN THE STATE OF UTTARAKHAND. e-Tendering Hi-CARE DIVISION HLL Lifecare Limited (A Government of India Enterprise) Central Marketing Office, HLL Bhavan, #26/4, Tambaram-Velachery Main Road, Pallikaranai, Chennai – 600 100, Tamilnadu, India Ph: 044-29813732/34 SEPTEMBER 2020 1 INDEX Section Topic PageNo. I Notice inviting Tender (NIT) 3 II Instructions To The Bidders (ITB) 11 III General Conditions of Contract (GCC) 24 IV Special Conditions Of Contract (SCC) 37 V List Of Requirements 40 VI Technical Specifications 42 VII Quality Control Requirements 73 VIII Qualification Criteria 74 IX Tender Form for Technical Bid 75 IX A Proforma ‘A’ I & A II 77 IX B Tender form for price bid 78 X Price Schedules (A & B) 79 XI Bank Guarantee Form for Performance Security /CAMC 89 Security XII Manufacturer’s/ Distributor’s Authorization Form 90 XIII Contract Form ’A’ 94 XIV Contract Form ‘B’ 98 XV Proforma of Consignee Receipt Certificate 100 XVI Proforma of Final Acceptance Certificate by the Consignee 101 XVII Consignee Address 103 2 HLL LIFECARE LIMITED (A Government of India Enterprise) Hicare Division, Central MarketingOffice, HLL Bhavan, No26/4, Tambaram-Velachery Main Road, Pallikaranai, Chennai-600 100, Tamilnadu, India Ph: +91-44-2981 3732/34 SECTION I NOTICE INVITING TENDER (NIT) IFBNo:HLL/CMO/HCD/UK-MGPS/STH/2020-21 08-09-2020 HLL Lifecare Limited (HLL), a Government of India Enterprise, invites online bids from eligible, competent and experienced parties who are capable of executing the following item/work meeting the requirements as per ourtender. -

Internal Audit

Annexure-1 Oraganisations who recognised CMAs for Internal Audit/Concurrent Audit S.No. Name of Organisations Central PSU 1 Airports Authority of India 2 Andaman and Nicobar Islands Integrated Development Corporation Limited 3 Andrew Yule & Company Limited 4 Artificial Limbs Manufacturing Corporation of India Limited 5 Biecco Lawrie Limited 6 Bharat Coking Coal Limited 7 Bharat Heavy Electricals Limited 8 Bharat Wagon Engineering Co. Ltd 9 BharatBroadband Network Limited 10 Bharat Sanchar Nigam Limited 11 Brahmaputra Valley Fertilizer Corporation Limited 12 Braithwaite & Co. Limited 13 Bharat Dynamic Limited 14 Burn Standard Co. Ltd 15 Central Cottage Industries of India Ltd. 16 Central Coalfields Limited 17 Central Electronics Limited 18 Central Mine Planning & Design Institute Limited 19 CENTRAL COTTAGE INDUSTRIES CORPORATION OF INDIA LIMITED 20 Coal India Limited 21 Container Corporation of India 22 Dedicated Freight Corridor Corporation of India Limited 23 Durgapur Chemicals Limited 24 Eastern Coalfields Limited 25 Fertilisers and Chemicals Travancore Limited (FACT Ltd.) 26 Ferro Scrap Nigam Ltd 27 Garden Reach Shipbuliders & Engineers Limited 28 GOA SHIPYARD LIMITED 29 Heavy Engineering Corporation Limited 30 Hindustan Aeronautics Limited 31 HIL (INDIA) LIMITED formerly known as Hindustan Insecticides Limited 32 Hindustan Newsprint Limited 33 Handicrafts & Handlooms Exports Corporations of India Ltd. 34 HLL Lifecare Ltd 34 HMT Ltd. 35 HMT MACHINE TOOLS LIMITED 36 IFCI Infrastructure Development Limited India-Infrastructure-Finance-Company-Limited -

Government of India Ministry of Micro, Small and Medium Enterprises

GOVERNMENT OF INDIA MINISTRY OF MICRO, SMALL AND MEDIUM ENTERPRISES LOK SABHA UNSTARRED QUESTION NO. 4232 TO BE ANSWERED ON 07.01.2019 PUBLIC PROCUREMENT POLICY 4232. SHRI ADHALRAO PATIL SHIVAJIRAO: SHRI SHRIRANG APPA BARNE: SHRI KUNWAR PUSHPENDRA SINGH CHANDEL: DR. SHRIKANT EKNATH SHINDE: SHRI ANANDRAO ADSUL: SHRI VINAYAK BHAURAO RAUT: Will the Minister of MICRO, SMALL AND MEDIUM ENTERPRISES be pleased to state: (a) the details of the total annual procurement of goods and services by each Public Sector Enterprise (PSE) in the year 2014-15, 2015-16, 2016-17 and 2017-18; (b) the quantity of calculated value of goods and services procured under Public Procurement Policy Order, 2012 during the said period in each PSE; (c) the status of procurement under this policy from MSMEs owned by SC/ST and non-SC/STs during the said period by each PSE; (d) whether the public procurement policy is not being complied with by many Government departments/PSEs; and (e) if so, the details thereof and the reasons therefor along with corrective steps taken/being taken by the Government in this regard? ANSWER MINISTER OF STATE (INDEPENDENT CHARGE) FOR MICRO, SMALL AND MEDIUM ENTERPRISES (SHRI GIRIRAJ SINGH) (a) to (e): The details of annual procurement of goods & services by the Central Public Sector Enterprise (CPSE) as per information provided by Department of Public Enterprises (DPE) are as under: Year No. of Total Procurement Procurement from MSEs CPSEs Procurement From MSEs owned by SC/ST (Rs. in Crore) (Rs. in Crore) Entrepreneur (Rs. in Crore) 2014-15 133 131766.86 15300.57 59.37 2015-16 132 279167.15 12566.15 50.11 2016-17 142 245785.31 25329.44 400.87 2017-18 169 280785.49 24226.51 442.52 Ministry of MSME has taken several measures for effective implementation of the Public Procurement Policy. -

Year : 2015-16

LIST OF RTI Nodal Officers Year : 2015-16 Sr.No Ministry/Department/Organisation Nodal Officer Contact Address Phone No/Fax/ Email Name/Designation 1 Cabinet Secretariat Shri Sunil Mishra Rashtrapati Bhawan Director & CPIO New Delhi 1 Cabinet Secretariat 110001 23018467 2 Department of Atomic Energy Shri P Ramakrishnan Central Office, Western Chief Administrator Anushaktinagar, 1 Atomic Energy Education Society Mumbai - 400 094 02225565049 [email protected] Dr. Pankaj Tandon Niyamak Bhavan, Scientific Officer F Anushaktinagar, 2 Atomic Energy Regulatory Board Mumbai- 400 094 25990659 [email protected] Shri M.B. Verma Atomic Minerals Atomic Minerals Directorate for Additional Director (Op 1-10-153/156, AMD 3 Exploration and Research Hyderabad - 500 016 04027766472 [email protected] Dr. P.M. Satya Sai Head, Commissioning 04427480044 Scientific Officer (H) Nuclear Recycle Group 4427480252 4 BARC Facilities, Kalpakkam Kalpakkam, [email protected] Shri Sanjay Pradhan TNRPO, NRB, BARC, 02525244299 Chief Superitendent Ghivali Post, Palghar 2525244158 5 Bhabha Atomic Resarch Centre (Tarapur) Pin 401502 [email protected] Shri. B. P. Joshi Central Complex, 3rd 02225505330 Chief Administrative Trombay, 2225505151 6 Bhabha Atomic Research Centre Mumbai - 400 085 [email protected] Smt. K. Malathi BHAVINI 04427480915 Bharatiya Nabhikiya Vidhyut Nigam Ltd. Senior Manager (HR) Kalpakkam - 603 102 4427480640 7 (BHAVINI) Kancheepuram Dist. [email protected] Shri M.C. Dinakaran BRIT, Project House, 02225573534 Board of Radiation and Isotope General Manager (PIO) Anushakti Nagar 2225562161 8 Technology Mumbai- 400 094. [email protected] Deputy Secretary Anushakti Bhavan 22839961 Deputy Secretary CSM Marg, 22048476 9 Department of Atomic Energy Mumbai-400001 [email protected] Shri V.K. -

ANSWERED ON:28.07.2017 Disinvestment Strategy Senthilnathan Shri PR

GOVERNMENT OF INDIA FINANCE LOK SABHA UNSTARRED QUESTION NO:2080 ANSWERED ON:28.07.2017 Disinvestment Strategy Senthilnathan Shri PR. Will the Minister of FINANCE be pleased to state: (a) whether the Government has chalked out any strategy to disinvest the Government's shares in certain loss making PSUs and also to acquire certain PSUs by the profit making PSUs and if so, the details thereof; (b) whether the Union Government has devised new initiatives and policies for the development of Nava Ratna and Mini Ratna Companies in the country; and (c) if so, the details thereof and the performance and loss of the companies of the last two years? Answer THE MINISTER OF STATE IN THE MINISTRY OF FINANCE (SHRI ARJUN RAM MEGHWAL) (a): Disinvestment in Central Public Sector Enterprises (CPSEs) is undertaken as per the extant disinvestment policy of the Government which , inter alia, envisages:- (i) Disinvestment through minority stake sale in listed CPSEs to achieve minimum public shareholding norms of 25 per cent. While pursuing disinvestment of CPSEs, the Government will retain majority shareholding, i.e. at least 51% and management control of the Public Sector Undertakings. (ii) Strategic disinvestment by way of sale of substantial portion of Government shareholding in identified CPSEs upto 50 per cent or more, along with transfer of management control. (b) & (c): The Government has already delegated financial and operational powers to the Boards of Navratna and Miniratna Central Public Sector Enterprises (CPSEs) in the areas of capital expenditure, investment in joint ventures/subsidiaries, human resources management, entering into technology joint ventures or strategic alliances, etc. -

The Cognate Group Is Effective from 26.03.2018, That Is the Date of Its Uploading on PESB’S Website

The Cognate Group is effective from 26.03.2018, that is the date of its uploading on PESB’s website APPENDIX – II CENTRAL PUBLIC SECTOR ENTERPRISES UNDER DIFFERENT SECTORS/COGNATE GROUPS AS ON 31.3.2017 S. No. Sector / Cognate Group / CPSE AGRICULTURE AGRO BASED INDUSTRIES 1 ANDAMAN & NICOBAR ISL. FOREST & PLANT.DEV.CORP.LTD 2 NATIONAL SEEDS CORPN. LTD. MINING AND EXPLORATION COAL 3 BHARAT COKING COAL LTD. 4 CENTRAL COALFIELDS LTD. 5 COAL INDIA LTD. 6 EASTERN COALFIELDS LTD. 7 MAHANADI COALFIELDLS LTD. 8 NORTHERN COALFIELDS LTD. 9 SOUTH EASTERN COALFIELDS LTD. 10 WESTERN COALFIELDS LTD. MINING AND EXPLORATION CRUDE OIL 11 BHARAT PETRO RESOURCES LTD. 12 OIL & NATURAL GAS CORPORATION LTD. 13 OIL INDIA LTD. 14 ONGC VIDESH LTD. MINING AND EXPLORATION OTHER MINERALS & METALS 15 FCI ARAVALI GYPSUM & MINERALS (INDIA) LTD. 16 HINDUSTAN COPPER LTD. 17 INDIAN RARE EARTHS LTD. 18 KIOCL LTD. 19 MOIL LTD. 20 NATIONAL ALUMINIUM COMPANY LTD. 21 NMDC Ltd. 22 ORISSA MINERAL DEVELOPMENT COMPANY LTD. 23 THE BISRA STONE LIME COMPANY LTD. 24 URANIUM CORPORATION OF INDIA LTD. The Cognate Group is effective from 26.03.2018, that is the date of its uploading on PESB’s website MANUFACTURING, PROCESSING AND GENERATION STEEL 25 FERRO SCRAP NIGAM LTD. 26 MISHRA DHATU NIGAM LTD. 27 RASHTRIYA ISPAT NIGAM LTD. 28 STEEL AUTHORITY OF INDIA LTD. MANUFACTURING, PROCESSING AND GENERATION PETROLEUM (REFINERY & MARKETING) 29 BHARAT PETROLEUM CORPN. LTD. 30 CHENNAI PETROLEUM CORPORATION LTD. 31 HINDUSTAN PETROLEUM CORPN. LTD. 32 INDIAN OIL CORPORATION LTD. 33 MANGALORE REFINERY & PETROCHEMICALS LTD. 34 NUMALIGARH REFINERY LTD. MANUFACTURING, PROCESSING AND GENERATION FERTILIZERS 35 BRAHMAPUTRA VALLEY FERTILIZER CORPN. -

OM for Online Workshop on Mou 2021-22 to Be Held on 02.07

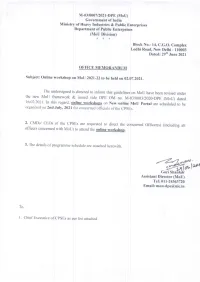

M-03/0007/2021-DPE (MoU) Government of India Ministry of Heavy Industries & Public Enterprises Department of Public Enterprises (MoU Division) * * * Block No.- 1 4 , C.G.O. Complex Lodhi Road, New Delhi - 110003 Dated: 29"" June 2021 OFFICE MEMORANDUM Subject: Online workshop on MoU 2021-22 t o be h e l d on 02.07.2021. The undersigned is directed to inform that guidelines o n MoU h a v e b e e n revised u n d e r t h e new MoU framework & issued vide DPE OM n o . M-03/0003/2020-DPE (MoU) dated 16.02.2021. I n t h i s regard, online workshops on New online MoU Portal a r e scheduled to b e organized on 2nd J u l y , 2021 f o r concerned officials of t h e CPSEs. 2. CMDs/ CEOs of t h e CPSEs a r e requested to d i r e c t t h e concerned O f f i c e r ( s ) ( including all officers concerned with MoU) to attend t h e online workshop. 3 . T h e d e t a i l s of programme schedule a r e attached herewith. Go ae: Fa). oto |2™ Gori Shankar Assistant Director (MoU) Tel: 011-24363720 Email: [email protected] To, 1 . C h i e f Executive of CPSEs as p e r list attached Department of Public Enterprises MoU 2021-22 Schedule of Online Workshop on New online MoU portal Venue: Conference Room No. -

SN Company 1 Cochin Shipyard Limited 2 India Tourism

SN Company 1 Cochin Shipyard Limited 2 India Tourism Development Corporation Limited 3 Mishra Dhatu Nigam Limited 4 Bharat Dynamics Limited 5 Bharat Electronics Limited 6 NMDC Limited 7 Bharat Heavy Electricals Limited 8 Chennai Petroleum Corporation Limited 9 Security Printing and Minting Corporation of India Limited 10 State Trading Corporation of India Limited 11 Central Coalfields Limited 12 Satluj Jal Vidyut Nigam Limited 13 RITES Limited 14 Hindustan Petroleum Corporation Limited 15 MMTC Limited 16 Goa Shipyard Limited 17 Garden Reach Shipbuilders & Engineers Limited 18 Rashtriya Ispat Nigam Limited 19 Engineers India Limited 20 South Eastern Coalfields Limited 21 Container Corporation of India Limited 22 NTPC Limited 23 Hindustan Aeronautics Limited 24 Central Warehousing Corporation 25 National Aluminium Company Limited 26 Steel Authority of India Limited 27 Numaligarh Refinery Limited 28 Western Coalfields Limited 29 Allahabad Bank 30 Mahanagar Telephone Nigam Limited 31 Hindustan Paper Corporation Limited 32 HLL Lifecare Limited 33 Bank of Baroda 34 Hindustan Newsprint Limited 35 Ircon International Limited 36 Coal India Limited 37 Dredging Corporation of India Limited 38 Andhra Bank 39 Indian Oil Corporation Limited 40 Rashtriya Chemicals & Fertilizers Limited 41 Bharat Sanchar Nigam Limited 42 Tehri Hydro Development Corporation Limited 43 Ennore Ports Limited 44 Balmer Lawrie & Company Limited 45 MSTC Limited 46 National Fertilizers Limited 47 Hindustan Copper Limited 48 Mangalore Refinery & Petrochemicals Limited 49 Housing -

Defence Psus, OFB Ramp up Their Resources to Fight COVID-19 Pandemic

Ministry of Defence Defence PSUs, OFB ramp up their resources to fight COVID-19 pandemic Posted On: 18 APR 2020 10:20AM by PIB Delhi Defence Public Sector Undertakings (DPSUs) and Ordnance Factory Board (OFB) have played their part in assisting civilian administration in fight against COVID-19 pandemic. These vital institutions of Department of Defence Production (DDP), Ministry of Defence have channelised all their resources, technical knowhow and manpower to help the nation mitigate the deadly virus. Following are some of the fruits of the efforts put in by scientists and personnel of DPSUs and OFB: Hindustan Aeronautics Limited (HAL) Bengaluru, a Defence PSU has set up isolation ward facility with three beds in Intensive Care Unit and 30 beds in wards. In addition, a building having 30 rooms was readied. In all, 93 persons can be accommodated at HAL facility. HAL has manufactured and distributed 25 PPEs to Doctors in various Hospitals in Bangalore which are authorised to treat Covid-19 patients. It has also manufactured 160 aerosol boxes which have been distributed to various Government Hospitals in Bengaluru, Mysore, Mumbai, Pune, Uttar Pradesh, Telangana, Andhra Pradesh and Tamil Nadu. Bharat Electronic Limited (BEL)has come forward on the directions of Ministry of Health and Family Welfare (MoH&FW to manufacture and supply 30,000 ventilators within two months for ICUs in the country. The design of these ventilators was originally developed by DRDO, which was improved upon by M/s Skanray, Mysore, with whom BEL has collaborated. BEL is likely to start manufacturing of ventilators between April20-24,2020. -

Eligible Members for GB

BDR-0001 BDR-0006 Kalyana Pattina Souharda Sahakari Ni., Gramina Mahila Multipurpose Souharda Cooperative Ltd. No.9-1-65, Mohana Market Complex, 1st Floor, K.P.T.C.L Road, Prawarda Campus, Near Sri Beerlingeshwara Temple, Bidar - 585401 Sastapura,, Basavakalyana - 585327 Bidar Bidar Ph: 08482-220559, 8050270731 Ph: 08482-232710, 9902410464 BDR-0008 BDR-0009 Pragathi Pattina Souharda Sahakari Ni., Kailasanatha Pattina Souharda Sahakari Ni., Mahalaxmi Plaza Complex, Gunj Bhalki, Bhalki - 585328 1st Cross, kailash Layout, Behind kailash Motors Show Room, Bidar Mannahalli Road, Bidar - 585403 Ph: 99452 76068, 9535925456 Bidar Ph: 7353143437, 8762500348 BDR-0010 BDR-0011 Chitaguppa Pattina Souharda Sahakari Ni., Sri Basaveshwara Souharda Pattina Sahakari Ni., Basavaraja Chouka, Main Road, Chitaguppa, Chitaguppa - Chitaguppa, Near Neharu Chouk, Main Road, Chitaguppa - 585412 585412 Bidar Bidar Ph: 08483 277407, 9611219850 Ph: 93432 05421, BDR-0014 BDR-0021 Pandith Deena Dayal Upadhyaya Pattin Souharda Sahakari Ni., Srinidhi Pattina Souharda Sahakari Ni., Plot No.50, APMC Yard, Humnabad - 585330 Amara Gangu Complex, 1st Floor, Opp. Siddarooda Mata, Bidar Mannalli Road, Bidar - 585403 Ph: 08483-270300, 9880918047 Bidar Ph: 08482-224655, 9739422310 BDR-0023 BDR-0025 Srinidhi Pattina Souharda Sahakari Ni. Adarsha Souharda Pattina Sahakari Ni. Near Basaveshwar Hospital, Main Road,, Basavakalyana - 585327 Masiya Complex, Najarat Colony, Near Karnataka College, Bidar Hydrabad Road, Bidar - 585401 Ph: 08481-295055, 9591668822 Bidar Ph: 9845893970, 8722091227 BDR-0026 BDR-0029 Jana Seva Souharda Sahakari Ni., Sri Sai Pattina Souharda Sahakari Ni. # 49, KHB Colony, Noubad, Bidar - 585402 Near Kranti Ganesh,Near Basava Mantap, Bidar - 585401 Bidar Bidar Ph: 9242163152, 9686743441 Ph: 9035101596, 9731500152/ 8904529104 BDR-0038 BDR-0039 Muktha Vividoddesha Souharda Sahakari Ni., Channabasava Pattina Souharda Sahakari Ni. -

HLL Lifecare

20, AVENUE APPIA – CH-1211 GENEVA 27 – SWITZERLAND – TEL CENTRAL +41 22 791 2111 – FAX CENTRAL +41 22 791 3111 – WWW.WHO.INT Prequalification Team Inspection services WHO PUBLIC INSPECTION REPORT (WHOPIR) Finished Product Manufacturer Part 1 General information Manufacturers details Company information Name of HLL Lifecare Limited manufacturer Corporate address HLL Lifecare Limited of manufacturer Thiruvananthapuram, Kerala, India Inspected site Address of Kanagala 591 225, inspected Dist. Belgaum, manufacturing Karnataka, India site if different from that given GPS coordinates: 16.31640 N, 74.42620E. above DUNS Number: 725552330 Unit / block / UniPill block workshop number Manufacturing KTK/28/258/93 license number, (delete if not applicable) Inspection details Dates of inspection 16-19 January 2017 Type of Initial GMP inspection inspection Introduction Brief summary of HLL Lifecare Limited, UniPill block Kanagala, is a tablets manufacturing unit at the manufacturing Belgaum district, Karnataka, India. activities General HLL Lifecare Limited (HLL) is a public sector enterprise under the Ministry of Health information about and Welfare. HLL has seven manufacturing units – Peroorkada Factory, Trivandrum the company and (PFT), Akkulam Factory Trivandrum (AFT), Kanagala Factory Belgaum (KFB), site Kakkanad Factory Cochin (KFC), Irapuram Factory Cochin (IFC), Manesar Factory Gurgaon (MFG) and Pharma Factory Indore (PFI). The management of the company belongs to the government of India (financial support WHOPIR: HLL Lifecare Limited, India This inspection report is the property of the WHO Contact: [email protected] Page 1 of 11 20, AVENUE APPIA – CH-1211 GENEVA 27 – SWITZERLAND – TEL CENTRAL +41 22 791 2111 – FAX CENTRAL +41 22 791 3111 – WWW.WHO.INT whereas personnel are recruited by the Unit Head).