Report on Financial Privacy, Law Enforcement and Terrorism

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

("DSCC") Files This Complaint Seeking an Immediate Investigation by the 7

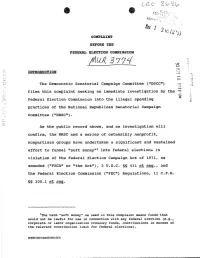

COMPLAINT BEFORE THE FEDERAL ELECTION CBHMISSIOAl INTRODUCTXON - 1 The Democratic Senatorial Campaign Committee ("DSCC") 7-_. J _j. c files this complaint seeking an immediate investigation by the 7 c; a > Federal Election Commission into the illegal spending A* practices of the National Republican Senatorial Campaign Committee (WRSCIt). As the public record shows, and an investigation will confirm, the NRSC and a series of ostensibly nonprofit, nonpartisan groups have undertaken a significant and sustained effort to funnel "soft money101 into federal elections in violation of the Federal Election Campaign Act of 1971, as amended or "the Act"), 2 U.S.C. 5s 431 et seq., and the Federal Election Commission (peFECt)Regulations, 11 C.F.R. 85 100.1 & sea. 'The term "aoft money" as ueed in this Complaint means funds,that would not be lawful for use in connection with any federal election (e.g., corporate or labor organization treasury funds, contributions in excess of the relevant contribution limit for federal elections). THE FACTS IN TBIS CABE On November 24, 1992, the state of Georgia held a unique runoff election for the office of United States Senator. Georgia law provided for a runoff if no candidate in the regularly scheduled November 3 general election received in excess of 50 percent of the vote. The 1992 runoff in Georg a was a hotly contested race between the Democratic incumbent Wyche Fowler, and his Republican opponent, Paul Coverdell. The Republicans presented this election as a %ust-win81 election. Exhibit 1. The Republicans were so intent on victory that Senator Dole announced he was willing to give up his seat on the Senate Agriculture Committee for Coverdell, if necessary. -

Box Number: M 17 (Otw./R?C<O R 15

This document is from the collections at the Dole Archives, University of Kansas http://dolearchives.ku.edu Robert J. Dole Institute of Politics REMOVAL NOTICE Removed from: S\>QQClt\es, j'Ot1Lt Mc..C.luv\Uj I ( 1 'f<-f Accession: Box Number: m17 (otw./r?C<O r 15 z,cr ~ fftt«r Rt (Jub/t'c CV1 Removed to: Oversized Photographs Box I (Circle one) Oversized Publications Box Campaign Material Box Oversized Newsprint Box Personal Effects Box Mem~rabilia Btm- _:£__ Oversized Flats [Posters, Handbills, etc] Box Political Cartoons Box -- Textiles Box Photograph Collection Box \ ,,,,,,,.... 4" Size: X , 2 5 >< • 7J Format: Pi v'\ Description: Ret k~v\o.>1 Dat~: rn4 > ol ""'~\ t ~', Subject Terms (ifanyJ. Restrictions: none Remarks: Place one copy with removed item Place one copy in original folder File one copy in file Page 1 of 188 This document is from the collections at the Dole Archives, University of Kansas http://dolearchives.ku.edu Robert J. Dole Institute of Politics REMOVAL NOTICE Date: from: ~pe (!c_~J Jt:'~C. e rf)c C..lun ji l'7°1 Accession: Box Number: B 0 ~ \ t ro 'I"' l'l • l 5 6L/ /;;Ff So'"":t-h.v\V"'\ 'R-e._plA l; co-"' ~~~~ Removed to: Oversized Photographs Box C.O~t-('U"UL.. ( C ircle one) Oversized Publications Box Campaign Material Box Oversized Newsprint Box Personal Effects Box Memorabilia -:tJ1f X Oversized Flats [Posters, Handbills, etc] Box __ Political Cartoons Box Textiles Box Photograph Collection Box Restrictions: none Remarks: Place one copy with removed item Place one copy in original folder File one copy in file Page 2 of 188 This document is from the collections at the Dole Archives, University of Kansas http://dolearchives.ku.edu WH"A T , S .INN AT ENGL ..ISH MANOR AND LA.KE .RA.BUN .INNS ..IN 1 994 FOR THOSE OF YOU #HO HAVEN'T BEEN OUR t;UESTS IN THE PAST OR HAVEN'T VISITED US RECENTLY, ENt;LISH ANO I #OULO LIKE TO ACQUAINT YOU ANO BRINE; YOU UP TO DATE. -

Appendix File 1987 Pilot Study (1987.Pn)

Page 1 of 189 Version 01 Codebook ------------------- CODEBOOK APPENDIX FILE 1987 PILOT STUDY (1987.PN) USER NOTE: This file has been converted to electronic format via OCR scanning. As as result, the user is advised that some errors in character recognition may have resulted within the text. >> OPEN-END RESPONSES FOR THE 1987 PILOT WAVES 1 AND 2 N.B. 1. The first part of this section is a memo by John Zaller, "Cognitive Responses to Survey Questions" which documents and discusses the coding scheme for the cognitive experiments on the Pilot Study. Those who plan to use these data should, without fail, read this memo. 2. The Zaller memo is followed by the open-end master codes: a) direction of response b) emotional intensity and elaboration of thought c) Frame of reference and content code 3. Numerous variables refer to PF 10. PF 10 is a function key used by CATI interviewers in recording comments of respondents. These side comments have been coded for this study. 4. In Wave 2 variables, respondents who were interviewed in Wave 1 but not re-interviewed in Wave 2 have had data variables padded with O's. This is not explicitly stated in the variable documentation. COGNITIVE RESPONSES TO SURVEY QUESTIONS The 1987 Pilot study carried a series of questions designed to elicit information about what is on people's minds as they respond to survey questions. The basic method was to ask individuals a standard policy question and then to use open-ended probes tofind out what exactly the individual thought about that issue. -

Georgia's Perfect Spots

GEORGIA’S PERFECT SPOTS Receive your power from one of the MEAG Power Acworth East Point Monticello Adel Elberton Moultrie communities listed here and you receive a host Albany Ellaville Newnan of advantages – local decision-making, local rate- Barnesville Fairburn Norcross setting and local service. And because these Blakely Fitzgerald Oxford Brinson Forsyth Palmetto hometowns have MEAG Power as their wholesale Buford Fort Valley Quitman power supplier, you gain the advantages of MEAG Cairo Grantville Sandersville Calhoun Griffin Sylvania Power’s 99.996% reliability and 68% carbon-free Camilla Hogansville Sylvester delivered energy portfolio. Better yet, because these Cartersville Jackson Thomaston are public power communities, utility revenue is College Park LaFayette Thomasville Commerce LaGrange Washington reinvested in the community. The result: a vibrant Covington Lawrenceville West Point spot to be. And how perfect is that! Crisp County Mansfield Whigham Doerun Marietta Douglas Monroe Municipal Electric Authority of Georgia 1-800-333-MEAG www.meagpower.org FIND YOUR SPARK Fuel your passion, ignite your creative spark. At KSU, we give you the inspiration you need to engineer your own solutions. From top-tier research in state-of-the-art facilities to gaining insights to solve real-world engineering problems, we support students every step of the way. When you come to KSU, you don’t just find your spark. You find your wings. Learn more at FIND.KENNESAW.EDU JANUARY 2021 • VOLUME 36 • NUMBER 5 TABLE OF CONTENTS COVER STORY 2021 Georgians of the Year: COVID Heroes 18 BY SUSAN PERCY Frontline workers fi ghting the pandemic and its effects. FEATURES 28 Hall of Fame BY KENNA SIMMONS AND PATTY RASMUSSEN Ann Cramer and James Cox Kennedy are the 2021 inductees. -

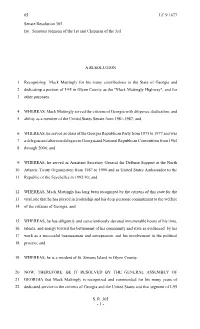

Senate Resolution 305 By: Senators Johnson of the 1St and Chapman of the 3Rd

05 LC 9 1677 Senate Resolution 305 By: Senators Johnson of the 1st and Chapman of the 3rd A RESOLUTION 1 Recognizing Mack Mattingly for his many contributions to the State of Georgia and 2 dedicating a portion of I-95 in Glynn County as the "Mack Mattingly Highway"; and for 3 other purposes. 4 WHEREAS, Mack Mattingly served the citizens of Georgia with diligence, dedication, and 5 ability as a member of the United States Senate from 1981-1987; and 6 WHEREAS, he served as chair of the Georgia Republican Party from 1975 to 1977 and was 7 a delegate and alternate delegate to Georgia and National Republican Conventions from 1964 8 through 2004; and 9 WHEREAS, he served as Assistant Secretary General for Defense Support at the North 10 Atlantic Treaty Organization from 1987 to 1990 and as United States Ambassador to the 11 Republic of the Seychelles in 1992-93; and 12 WHEREAS, Mack Mattingly has long been recognized by the citizens of this state for the 13 vital role that he has played in leadership and his deep personal commitment to the welfare 14 of the citizens of Georgia; and 15 WHEREAS, he has diligently and conscientiously devoted innumerable hours of his time, 16 talents, and energy toward the betterment of his community and state as evidenced by his 17 work as a successful businessman and entrepreneur and his involvement in the political 18 process; and 19 WHEREAS, he is a resident of St. Simons Island in Glynn County. 20 NOW, THEREFORE, BE IT RESOLVED BY THE GENERAL ASSEMBLY OF 21 GEORGIA that Mack Mattingly is recognized and commended for his many years of 22 dedicated service to the citizens of Georgia and the United States and that segment of I-95 S. -

TR Category of the White House Central Files Subject File at the Gerald R

Digitized from the TR category of the White House Central Files Subject File at the Gerald R. Ford Presidential Library Page One TRIPS OF 'mE ~.rnEm 1975 ~TlJ.ESS : -'~''''''''''''''"!''W'''''01ua:=-==:::NG==r'''''''V-AC''''A~TIONS AND \'JE!~K-F1mS: TRIP ----Dl'."STINATION: DATE: STATLiTE HOURS STATUTE HOURS EXPLANATION: !llifu. MJLES : AlrTAY: MIlES : ~ ,.r~_,> 1. Grand Junction and Vail, Jan 1-2 1,867 19 Note: Going portion shown in 1974 travel Records. Colorado Wed. Jan. 1: Skied late morning until early afternoon. Worked in residence. Watched some football on T.V. Thurs. Jan 2: Returned to Washington D.C. 2. Queenstown, Maryland Jan. 19 5 Surr. Jan 19: Guest of honor at a gathering of the Chowder and Marching Soviety (Formed by Freshmen GOP members who ) came to Congress in the late 1940's) at the home of Senator Charles E. Potter. Tour of the 48 acre estate by Sen. Potter. 3· Atlanta, Georgia Feb. 3-4 1,130 26 Mon. Feb. 3: Dobbins AFB - Atlanta, Ga: Greeted by Governor George Busbee and others. Hyatt Regency Hotel: Attended White House Conference in the Phoenix Room. Working dinner with Governors, Selected Mayors, and Legislators. RON. Tues. Feb. 4: Working breakfast with regional representative in the Tudor Room. Remarks. Marriott Hotel: Attended (OIC) Opportunities Industrialization Centers 11th. Annual Conven tion luncheon in the Grand Ballroom. Remarks. Hyatt Regency Hotel: Regional Press Conference in the Phoenix Room. (Note: Due to inclement weather, the Press Charter was diver ted to New York (JFK).RON returnil1g to Washington Feb. 5th. ) 4. Camp David, Maryland Feb. -

Fall 2010 0.Pdf

The Yale Historical Review Fall 2010 An Undergraduate Publication Lebkc[??iik[) The 20th Century Issue Churchill in the First World War The Richard Nixon Memorial Library Berlin’s Holocaust Memorial The Rise of Republicanism in Georgia The Yale Historical Review An Undergraduate Publication Donors Founding Patrons In Memory of David J. Magoon Stauer Derek Wang Zixiang Zhao Founding Contributors Joe and Marlene Toot Yale Center for British Art Yale Club of Hartford Contributors Greg Weiss Editorial Board For information regarding submissions, advertise- ments, subscriptions, and contributions, or to provide feedback, please contact us at Editor-in-Chief [email protected] or write to us at Layne Johnson, SM ‘12 Managing Editor Yale Historical Review Kate Liebman, BK ‘13 Yale University PO 204204 Senior Essay Editor New Haven, CT 06520 Joe Geylin, SM ‘11 or visit our website at www.yalehistoricalreview.org Junior Seminar Editors Jessica Moldovan, SY ‘11 COVER: “Winston Churchill : premier ministre de Josh Tannen, SY ‘11 Grande-Bretagne” from ARTstor’s “World War I and At-Large Editor II Posters and Postcards (University of Minnesota Jack Bisceglia, PC ‘12 Libraries)” Collection. ID Number: msp03528 Directed Studies Editor Source Image and original data from University of Thomas Meyerson, BK ‘11 Minnesota Libraries: http://www.lib.umn.edu/ Outside Editor Elinor Monahan, JE ‘13 The photographs from “A Moment in Yale’s History” Brendan Ross, BK ‘13 are courtesy of the Vorys Archive. Freshman Paper Editor The Yale Historical Review is published by Yale Noah Gray, MC ‘13 College students. Yale University is not responsible for Design Editor its contents. -

MALE SPEAKER: Let Me Welcome You to This Session of the Series of Reflections On

MALE SPEAKER: Let me welcome you to this session of the series of Reflections on Georgia Politics. We’ve had some wonderful sessions so far and continue to provide these for you, and we certainly have one in store today. I’m hopeful that there may be some other people who are out there, circling around looking for parking. That was certainly true when I came in, that there was not that much parking available. But we are glad to have you today. Also, keep in mind the schedule. The next program will be one week from today here at the same place. The Georgia political figure who will be under discussion at that time will be Griffin Bell. We certainly look forward to that. Today we have former Senator Mack Mattingly with us. Our gracious host, Bob Short, will lead us into a discussion here. We’re delighted to have Bob always. He does a tremendous job for us. Senator Mattingly, we’re so happy to have you as well. MACK MATTINGLY: Thanks. MALE SPEAKER: Turning it over to you, Bob. BOB SHORT: Thank you very much. Thank you, Senator, for being with us today. This is a series of Reflections on Georgia Politics, so we want you to think and reflect with us during that period when you were coming up from Newton County in the Republican Party, from being a – as far as I’m concerned – the kingpin of Republicans in Georgia. And we want to start off, if we may, by asking you to give a little bit about yourself. -

U.S. Senate Republican Leader Bob Dole Georgia State Convention Saturday, May 20, 1989 Atlanta, Georgia

This document is from the collections at the Dole Archives, University of Kansas http://dolearchives.ku.edu U.S. SENATE REPUBLICAN LEADER BOB DOLE GEORGIA STATE CONVENTION SATURDAY, MAY 20, 1989 ATLANTA, GEORGIA Page 1 of 95 This document is from the collections at the Dole Archives, University of Kansas OSCAR, THANK YOUhttp://dolearchives.ku.edu VERY MUCH FOR THAT KIND INTRODUCTION. I ALSO WANT TO THANK YOU FOR ALL THE GOOD WORK YOU DID FOR ME AND ELIZABETH DURING THE PRESIDENTIAL CAMPAIGN . WE'RE GRATEFUL. \ I I KNOW THESE ARE EXCITING TIMES FOR GEORGIA REPUBLICANS; AND I AM VERY PLEASED TO BE A PART OF IT HERE TODAY. YOU HAVE SOME IMPORTANT DECISIONS TO MAKE THIS WEEKEND, INCLUDING THE SELECTION OF A NEW STATE CHAIRMAN. -2- Page 2 of 95 This document is from the collections at the Dole Archives, University of Kansas SO LET ME TAKEhttp://dolearchives.ku.edu THIS OPPORTUNl1Y TO SALUTE THE WORK OF A GOOD MAN, YOUR SOON-TO-BE FORMER CHAIRMAN JOHN STUCKEY. UNDER -HIS LEADERSHIP, THE GEORGIA REPUBLICAN PAR1Y HAS MADE HISTORIC GAINS ACROSS-THE-BOARD. THANKS TO YOU,- JOHN,THE PAR1Y IS ON THE MOVE AND THE FUTURE LOOKS BRIGHT, INDEED. > -3- Page 3 of 95 This document is from the collections at the Dole Archives, University of Kansas GEORGIAhttp://dolearchives.ku.edu SUCCESS STORY NO DOUBT ABOUT IT, THE DAYS OF THE "SOLID SOUTH" ARE OVER FOR THE DEMOCRATS. IT'S "SOLID" ALL RIGHT -- FOR RONALD REAGAN AND GEORGE BUSH. WHAT WE HAVE TO DO NOW IS MAKE IT JUST AS "SOLID" FOR REPUBLICAN CANDIDATES AT EVERY LEVEL OF GOVERNMENT -- IN GEORGIA AND IN EVERY OTHER SOUTHERN STATE. -

Notes to Pages 2–16

Abbreviations and Short Citations CINS Cumberland Island National Seashore, St. Marys, Ga. CPSU Cooperative Park Studies Unit DSC Denver Service Center of the National Park Service, Denver Ga. Archives Georgia Archives, Atlanta NA National Archives, College Park, Md. NPS National Park Service SERO Southeast Regional Office of the National Park Service, Atlanta Thornton Morris Papers Thornton Morris Papers, Morris Law Firm, Atlanta UGa University of Georgia, Athens Introduction 1. The concept of “biography of place” is a useful means by which historical geographers focus on place as a complex entity formed by diverse processes that dynamically changes through time. An early example of this term’s use can be found in Marwyn S. Samuels, 1979, “The Biography of Landscape,” in Ordinary Places, ed. Donald W. Meinig (New York: Oxford Univ. Press), 51–88. Later works include William Wyckoff, 1988, The Developer’s Frontier: The Making of the West- ern New York Landscape (New Haven: Yale Univ. Press), and Gay M. Gomez, 1998, A Wetland Biography: Seasons on Louisiana’s Chenier Plain (Austin: Univ. of Texas Press). 2. A voluminous literature exists on the national park system and its man- agement. Classic overviews include Ronald A. Foresta, 1984, America’s National Parks and Their Keepers (Washington, D.C.: Resources for the Future); Alfred Runte, 1987, National Parks: The American Experience, 2d ed. (Lincoln: Univ. of Nebraska Press); Richard West Sellars, 1997, Preserving Nature in the National Parks: A History (New Haven: Yale Univ. Press); and Conrad L. Wirth, 1980, Parks, Politics, and People (Norman: Univ. of Oklahoma Press). More specific works on managing preexisting land uses, private holdings, and park threats include John C. -

President's Daily Diary Collection (Box 78A) at the Gerald R

Scanned from the President's Daily Diary Collection (Box 78A) at the Gerald R. Ford Presidential Library THE WHITE HOUSE THE DAILY DIARY OF PRESIDENT GERALD R. FORD PLACE DAY BEGAN DATE (Mo., Day, Yr.) THE WHITE HOUSE NOVEMBER 14, 1975 '- WASHINGTON, D.C. TIME DAY 7:24 a.m. FRIDAY -PHONE TIME ." "0 ~" '., ACTIVITY ii: " II '"II In Out .. '" 7:24 The President had breakfast with Senator Barry Goldwater (R-Arizona). 8:05 The President went to the doctor's office. 8:07 The President went to the Oval Office. 8:19 8:22 R The President talked with Mayor Richard J. Daley (D-Chicago, Illinois) • 8:47 The President went to the South Grounds of the White House. The President greeted members of the U.S. Olympic Ski team. For a list of attendees, see APPENDIX "A." 8:48 8:55 The President flew by helicopter from the South Grounds to Andrews AFB, Maryland. For a list of passengers, see APPENDIX "B." 9:02 9:44 The President flew by the "Spirit of '76" from Andrews AFB to Raleigh-Durham Airport, Raleigh, North Carolina. For a list of passengers, see APPENDIX "C." 9:44 The President was greeted by Governor James E. Holshouser (R-North Carolina). 9:55 10:14 The President motored from the Raleigh-Durham Airport to the McDougald Gymnasium, North Carolina Central University, Durham, North Carolina. The President was greeted by: Albert H. Whiting, Chancellor of North Carolina Central University William C. Friday, President of the University of North Carolina School System 10:16 The Presidential party went to the holding room. -

~Ior 2003-/5- I

McKenria Long RECEIVED Adante *r Alrlrirlcw* FEC MAIL SanDie9° & euJ ^™§ OPERATIONS CENTER SanFrandsco Los Angeles 303 Peachtree Street, NE • Suite 5300 • Atlanta,$8>#8 \\y A IP 09 Washington. D.C. Tel: 404.527.4000 • Fax: 404.527.4198 Philadelphia www.mckennalong.com Brussel$ 6. SCOTT RAFSHOON EMAIL ADDRESS (404) 527-4952 [email protected] April 14,2003 ^ 3 g cr aH5rp? Federal Election Commission J ^ ^^ ^"> ^ /v °"9 / ^ m r^B{5n Office of General Counsel /l/lD J {jlVS** I *\ ^ g*=*° 999EStreetNW ~iO^# ftR^ 2003-/5^^tV-> / ^ - -I * © Washington, DC 20463 Re: Advisory Opinion Request Dear Commissioners: On behalf of Denise Majette, a Member of the United States House of Representatives, and the Committee to Re-Elect Congresswoman Denise Majette (the "Committee"), we respectfully request an advisory opinion from the Federal Election Commission pursuant to 2 U.S.C. § 437f of the Federal Election Campaign Act of 1971, as amended (the "Act"). A civil lawsuit was brought against Representative Majette by supporters of her opponent in Georgia's 2002 primary election. As a direct result of that lawsuit, Representative Majette has incurred significant legal expenses. To defray those legal expenses, Representative Majette wishes to establish a Legal Expense Fund, as more specifically detailed below. We respectfully ask that you confirm that funds raised and spent by Representative Majette under the circumstances described in this letter, for the purpose of defraying the costs associated with defending against the described litigation, are not "contributions" or "expenditures" as defined in the Act, and are thus not subject to the provisions of the Act.