Jens Weidmann: Change and Continuity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DEFENDING the WOLF the Useful Contradiction of the Bundesbank Carlo Bastasin

DEFENDING THE WOLF The Useful Contradiction of the Bundesbank Carlo Bastasin SEP Policy Brief No. 1 - 2014 The Deutsche Bundesbank, the German central bank, is commonly regarded as the Euroarea's boogeyman. The pressure imparted by the German monetary authority, for instance, rendered the European Central Bank reluctant to follow the footprints of the Federal Reserve and of other central banks, and engage in non- standard monetary policy measures that might rapidly put an end to the crisis that has been plaguing the euro zone. At several stages, during the current crisis, the ECB has been forced to take actions and prevent severe economic and financial dislocations. Given the institutional vacuum at the area-wide level and the lack of political capacity of the other institutions, the European Central Bank had often to move across the borders of its traditional domain. This has given reason to a slew of criticisms repeatedly and loudly voiced by the Bundesbank. Being also the most vocal policy actor evoking the fiscal risks associated with effecting implicit cross-border transfers via the ECB's balance sheet, the Bundesbank has appeared to have a “non- monetary” hidden agenda or even a “national political” mission. In fact, the Bundesbank has regularly appealed to two fundamental principles of sound economic and monetary policy management that cannot be easily overlooked by anybody concerned that monetary policy may lose its ability to preserve price stability. Should monetary independence be eroded by the increasing tasks devolved to the central banks, wider economic and political consequences might then arise. The first principle is the need to avoid fiscal dominance, not allowing inflation to be determined by the level of fiscal debts; the second is the “principle of responsibility” that sees a contradiction if individual responsibility is blurred by the intervention of joint liability as in the case of a State running unsound fiscal policies and being automatically bailed out by the mutualization of its liabilities. -

How Macron Won It All the French President As Master Kingmaker

How Macron Won It All The French president as master kingmaker. he French did it again. By recalling Christine Lagarde, who has served as managing director of the International Monetary Fund since 2011, from Washington and throwing her into the race to succeed Mario Draghi as By Klaus C. Engelen head of the European Central Bank, French President Emanuel Macron effectively won the real power game in the competition for the top European positions after the May elections for the European Parliament. But since Macron helped nominate, in a big surprise, Ursula von der Leyen, Tthe Brussels-born francophone long-time member of German Chancellor Angela Merkel’s government, to lead the new EU Commission, the disappoint- ment in Germany of not seeing Bundesbank President Jens Weidmann chosen as Draghi’s successor may have been somewhat mitigated. HOW MACRON GOT THE POLE POSITION When the race for the new EU chief executive began, the French presi- dent started questioning the system of Spitzenkandidaten (lead candidates). Macron referred to the Lisbon Treaty, which left the Council in the lead role to select and propose a candidate whom the European Parliament then would have to confirm with an absolute majority. The Council consists of the heads of state or governments of the member countries, together with its president and the president of the Commission. In Macron’s view, the 2014 European election, when the center-right European People’s Party got Jean-Claude Juncker elected Commission president with the help of the Progressive Alliance for Socialist and Democrats, was THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY an aberration to be corrected. -

What Have We Learned? Macroeconomic Policy After the Crisis

What Have We Learned? What Have We Learned? Macroeconomic Policy after the Crisis edited by George Akerlof, Olivier Blanchard, David Romer, and Joseph Stiglitz The MIT Press Cambridge, Massachusetts London, England © 2014 International Monetary Fund and Massachusetts Institute of Technology All rights reserved. No part of this book may be reproduced in any form by any elec- tronic or mechanical means (including photocopying, recording, or information storage and retrieval) without permission in writing from the publisher. Nothing contained in this book should be reported as representing the views of the IMF, its Executive Board, member governments, or any other entity mentioned herein. The views expressed in this book belong solely to the authors. MIT Press books may be purchased at special quantity discounts for business or sales promotional use. For information, please email [email protected]. This book was set in Sabon by Toppan Best-set Premedia Limited, Hong Kong. Printed and bound in the United States of America. Library of Congress Cataloging-in-Publication Data What have we learned ? : macroeconomic policy after the crisis / edited by George Akerlof, Olivier Blanchard, David Romer, and Joseph Stiglitz. pages cm Includes bibliographical references and index. ISBN 978-0-262-02734-2 (hardcover : alk. paper) 1. Monetary policy. 2. Fiscal policy. 3. Financial crises — Government policy. 4. Economic policy. 5. Macroeconomics. I. Akerlof, George A., 1940 – HG230.3.W49 2014 339.5 — dc23 2013037345 10 9 8 7 6 5 4 3 2 1 Contents Introduction: Rethinking Macro Policy II — Getting Granular 1 Olivier Blanchard, Giovanni Dell ’ Ariccia, and Paolo Mauro Part I: Monetary Policy 1 Many Targets, Many Instruments: Where Do We Stand? 31 Janet L. -

8-11 July 2021 Venice - Italy

3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING AND SIDE EVENTS 8-11 July 2021 Venice - Italy 1 CONTENTS 1 ABOUT THE G20 Pag. 3 2 ITALIAN G20 PRESIDENCY Pag. 4 3 2021 G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETINGS Pag. 4 4 3RD G20 FINANCE MINISTERS AND CENTRAL BANK GOVERNORS MEETING Pag. 6 Agenda Participants 5 MEDIA Pag. 13 Accreditation Media opportunities Media centre - Map - Operating hours - Facilities and services - Media liaison officers - Information technology - Interview rooms - Host broadcaster and photographer - Venue access Host city: Venice Reach and move in Venice - Airport - Trains - Public transports - Taxi Accomodation Climate & time zone Accessibility, special requirements and emergency phone numbers 6 COVID-19 PROCEDURE Pag. 26 7 CONTACTS Pag. 26 2 1 ABOUT THE G20 Population Economy Trade 60% of the world population 80 of global GDP 75% of global exports The G20 is the international forum How the G20 works that brings together the world’s major The G20 does not have a permanent economies. Its members account for more secretariat: its agenda and activities are than 80% of world GDP, 75% of global trade established by the rotating Presidencies, in and 60% of the population of the planet. cooperation with the membership. The forum has met every year since 1999 A “Troika”, represented by the country that and includes, since 2008, a yearly Summit, holds the Presidency, its predecessor and with the participation of the respective its successor, works to ensure continuity Heads of State and Government. within the G20. The Troika countries are currently Saudi Arabia, Italy and Indonesia. -

Challenges for Monetary Policy in the Euro Area

Challenges for Monetary Policy in the Euro Area Scientific work for attainment of the academic degree of Bachelor of Science at the Department of Economics at the University of Konstanz Author: Kevin Riedmüller Felchenstraße 3 89584 Ehingen Period of work: from March 1st, 2016 to March 29th, 2016 Supervisor: Prof. Dr. Scholl Konstanz, March 29th, 2016 Konstanzer Online-Publikations-System (KOPS) URL: http://nbn-resolving.de/urn:nbn:de:bsz:352-0-390274 Preface The monetary policy of the European Central Bank is a current and highly debated topic. A lot of economists disagree with the course of the European Central Bank and debate about it in public. This bachelor thesis gives a brief overview of monetary policy during the financial crisis and the discussion about the latest actions of the European Central Bank. Economics students or other interested students can gain a first insight into recent monetary policy by reading this work. First of all, I would like to thank Kerstin and my family for everything. Furthermore, I would like to thank Pablo, Mihaela, Max, Tobias, Edwin and Kasey. At last, I would like to express my gratitude to Prof. Dr. Scholl for great supervision. ii Index 1. Introduction 1 2. The ECB’s monetary policy during the euro area crisis 2 2.1 Overview of monetary policy in the first recession 3 2.2 Overview of monetary policy in the second recession 4 2.3 Why had monetary policy different effects in both recessions? 6 4. The current monetary policy of the ECB 8 4.1 Outright Monetary Transactions 8 4.2 Quantitative Easing 9 5. -

Jens Weidmann : Climate Change and Central Banks

Jens Weidmann: Climate change and central banks Welcome address by Dr Jens Weidmann, President of the Deutsche Bundesbank and Chairman of the Board of Directors of the Bank for International Settlements, at the Deutsche Bundesbank’s second financial market conference, Frankfurt am Main, 29 October 2019. * * * 1 Welcome Ladies and gentlemen, Allow me to bid you a warm welcome to the Deutsche Bundesbank’s second financial market conference, on my own behalf and that of Sabine Mauderer, here at the Gesellschaftshaus in Frankfurt’s green haven, the Palmengarten. Frankfurt’s most charming park, the Palmengarten was created 150 years ago, and a series of events have been scheduled this week to commemorate this anniversary. When Adolphe, Duke of Nassau, was forced to disband his collection of exotic plants housed in Schloss Biebrich in 1866, Heinrich Siesmayer, a Frankfurt garden designer, came up with a clever idea – he set up a stock corporation to buy the plants and build a botanical garden in Frankfurt. City folk snapped up the shares in this company, allowing Siesmayer to buy Duke Adolphe’s green treasures for a price of 60,000 Gulden.1 I suppose you could say that the foundation of Frankfurt’s Palmengarten was an early example of “green finance”, given that it was a privately funded green investment. But there is more to green finance than that, of course. It is a term that also includes accounting for climate risks in the financial sector, or the transition to a greener financial system. If environmental concerns are joined by economic and social sustainability considerations, it is common to use the term “sustainable finance”.2 And that is what today’s conference is all about: sustainable finance. -

Permanent Members of the ESRB General Board

Permanent members of the ESRB General Board Voting Members Non-voting Members Chair of the ESRB General Board Mario Draghi President European Central Bank Sonnemannstraße 20 60314 Frankfurt am Main Germany First Vice-Chair of the ESRB General Board (voting member as Governor of the Bank of England) Mark Carney Governor Bank of England Threadneedle Street London EC2R 8AH United Kingdom Second Vice-Chair of the ESRB General Board (voting member as Chairman of the ESAs Joint Committee) Andrea Enria Chairman European Banking Authority Tower 42 (level 18) 25 Old Broad Street London EC2N 1HQ United Kingdom 1 Permanent members of the ESRB General Board Voting Members Non-voting Members Chair of the Advisory Scientific Committee Richard Portes Professor of Economics London Business School Sussex Place London NW1 4SA United Kingdom Vice-Chair of the Advisory Scientific Committee Javier Suárez CEMFI Casado del Alisal 5 28014 Madrid Spain Vice-Chair of the Advisory Scientific Committee Marco Pagano Department of Economics University of Napoli Federico II Via Cintia Monte S. Angelo 80126 Napoli Italy Chair of the Advisory Technical Committee (voting member as Governor of the Sveriges Riksbank) Stefan Ingves Governor Sveriges Riksbank Brunkebergstorg 11 103 37 Stockholm Sweden 2 Permanent members of the ESRB General Board Voting Members Non-voting Members Austria Ewald Nowotny Helmut Ettl Governor Executive Director Oesterreichische Nationalbank Österreichische Finanzmarktaufsicht (FMA) Otto-Wagner-Platz 3 1090 Vienna Otto-Wagner-Platz 5 Austria 1090 -

Central Bank Activism Duke Law Journal, Vol

Central Bank Activism Duke Law Journal, Vol. 71: __ (forthcoming) Christina Parajon Skinner † ABSTRACT—Today, the Federal Reserve is at a critical juncture in its evolution. Unlike any prior period in U.S. history, the Fed now faces increasing demands to expand its policy objectives to tackle a wide range of social and political problems—including climate change, income and racial inequality, and foreign and small business aid. This Article develops a framework for recognizing, and identifying the problems with, “central bank activism.” It refers to central bank activism as situations in which immediate public policy problems push central banks to aggrandize their power beyond the text and purpose of their legal mandates, which Congress has established. To illustrate, the Article provides in-depth exploration of both contemporary and historic episodes of central bank activism, thus clarifying the indicia of central bank activism and drawing out the lessons that past episodes should teach us going forward. The Article urges that, while activism may be expedient in the near term, there are long-term social costs. Activism undermines the legitimacy of central bank authority, erodes its political independence, and ultimately renders a weaker central bank. In the end, the Article issues an urgent call to resist the allure of activism. And it places front and center the need for vibrant public discourse on the role of a central bank in American political and economic life today. © 2021 Christina Parajon Skinner. Draft 2021-05-27 20:46. † Assistant Professor, The Wharton School of the University of Pennsylvania. This article benefited from feedback provided by workshop or conference participants at The Wharton School, the Federal Reserve Bank of New York . -

The ESRB at 1

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Remsperger, Hermann et al. Proceedings The ESRB at 1 SUERF Studies, No. 2012/4 Provided in Cooperation with: SUERF – The European Money and Finance Forum, Vienna Suggested Citation: Remsperger, Hermann et al. (2012) : The ESRB at 1, SUERF Studies, No. 2012/4, ISBN 978-3-902109-64-4, SUERF - The European Money and Finance Forum, Vienna This Version is available at: http://hdl.handle.net/10419/163503 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu SUERF2012_4.book Page 1 Tuesday, January 8, 2013 11:06 AM The ESRB at 1 SUERF2012_4.book Page 2 Tuesday, January 8, 2013 11:06 AM SUERF2012_4.book Page 3 Tuesday, January 8, 2013 11:06 AM THE ESRB AT 1 Edited by Stefan Gerlach, Ernest Gnan and Jens Ulbrich Chapters by Hermann Remsperger Stephen G. -

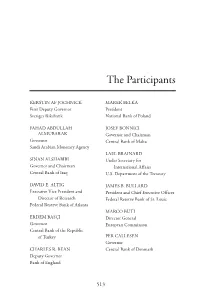

Pdfroster of Attendees

The Participants KERSTIN AF JOCHNICK MAREK BELKA First Deputy Governor President Sveriges Riksbank National Bank of Poland FAHAD ABDULLAH JOSEF BONNICI ALMUBARAK Governor and Chairman Governor Central Bank of Malta Saudi Arabian Monetary Agency LAEL BRAINARD SINAN ALSHABIBI Under Secretary for Governor and Chairman International Affairs Central Bank of Iraq U.S. Department of the Treasury DAVID E. ALTIG JAMES B. BULLARD Executive Vice President and President and Chief Executive Officer Director of Research Federal Reserve Bank of St. Louis Federal Reserve Bank of Atlanta MARCO BUTI ERDEM BASÇI Director General Governor European Commission Central Bank of the Republic of Turkey PER CALLESEN Governor CHARLES R. BEAN Central Bank of Denmark Deputy Governor Bank of England 513 514 The Participants AGUSTÍN CARSTENS DOUGLAS W. ELMENDORF Governor Director Bank of Mexico Congressional Budget Office NORMAN CHAN WILLIAM B. ENGLISH Chief Executive Director of Monetary Affairs Hong Kong Monetary Authority Board of Governors of the Federal Reserve System LUC COENE Governor CHARLES L. EVANS National Bank of Belgium President and Chief Executive Officer Federal Reserve Bank of Chicago JULIA LYNN CORONADO Chief Economist for North America MARTIN FELDSTEIN BNP Paribas President Emeritus, National Bureau of Economic Research CARLOS DA SILVA COSTA Professor, Harvard University Governor Bank of Portugal JACOB A. FRENKEL Chairman CHARLES H. DALLARA JP Morgan Chase International Managing Director Institute of International Finance ARDIAN FULLANI Governor TROY DAVIG Bank of Albania Senior Vice President and Director of Research JOHN GEANAKOPLOS Federal Reserve Bank of Kansas City Professor Yale University PAUL DEBRUCE CEO and Founder, ESTHER L. GEORGE DeBruce Grain Inc. -

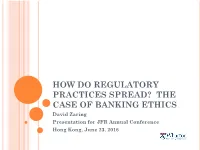

How Do Regulatory Practices Spread?

HOW DO REGULATORY PRACTICES SPREAD? THE CASE OF BANKING ETHICS David Zaring Presentation for JFR Annual Conference Hong Kong, June 23, 2016 GLOBAL BANKING SUPERVISION: SOURCES Comparative law: transplants, etc. Facilitated by regular interactions by banking supervisors International governance: Process: Agencification across borders (Zaring 2016) Substantive: Commitment to six principles (Zaring 2012) 1) a national treatment principle 2) a most favored nation principle 3) a preference for rulemaking over adjudication 4) a subsidiarity principle of enforcement 5) a peer review model of enforcement 6) a network model of institutionalization. WHY ARE SUPERVISORS CALLING FOR ETHICAL BANKING? “Virtue cannot be regulated … Even the strongest supervision cannot guarantee good conduct. Essential will be the rediscovery of core values, and ultimately this is a question of personal responsibility. More than mastering options pricing, company valuation, or accounting, living the right values will be the most important challenge” – Mark Carney, Head of the FSB and Bank of England WHAT IS ETHICAL BANKING? Increasingly characterized as a necessary complement to capital standards But supervisors have never defined what is required by ethical banking with precision. Instead: Christine Lagarde, the French head of the International Monetary Fund (IMF): banks “mired in scandals that violate the most-basic ethical norms.” The Chief Executive of the Hong Kong Monetary Authority: banking industry must “seek to regain the moral and ethical high ground -

Weidmann, Munchau and Target2 Wolfgang Munchau Writes Today About the Letter from Newish Bundesbank President Jens Weidmann to M

Weidmann, Munchau and Target2 Wolfgang Munchau writes today about the letter from newish Bundesbank president Jens Weidmann to Mario Draghi, as discussed here The Bundesbank initially dismissed the Target 2 balance as a matter of statistics. Their argument was: yes, it is recorded in the Bundesbank’s accounts, but the counterparty risk is divided among all members according to their share in the system. But last week, Jens Weidmann, president of the Bundesbank, acknowledged the Target 2 imbalances are indeed important, and an unacceptable risk. The Bundesbank has now joined the united front of German academic opinion. Wolfgang is a fantastic journalist and his FT column is essential reading. But this is a very bad paragraph. It is indeed the case that the Bundesbank has published an analysis of Target2 balances in its monthly report making it clear that the Bundesbank’s credit risk associated with Eurosystem operations was not measured by its Target2 balances (see page 34-35) of this report. That Weidmann now wishes to publicly claim he is concerned about risk associated with the Bundesbank’s Target2 credit does not simply mean that this is a truth that has now been “acknowledged”. I suspect most of us have worked for bosses that say things in public that are just plain wrong and I would guess that the sober Bundesbank officials that approved of the monthly bulletin piece on Target2 are fairly disgusted that Weidmann is adopting an approach in public that they know is ungrounded. As for Wolfgang’s idea that German academics are united behind Hans Werner Sinn in his concern about the Target2 credit (which he consistently and incorrectly labels “Target loans”) I’d note that Ulrich Bindseil and Philipp Johann König appear to have missed the memo that all Germans are supposed to agree with Sinn.