Comprehensive Version

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Solar Energy: State of the Art

Downloaded from orbit.dtu.dk on: Sep 27, 2021 Solar energy: state of the art Furbo, Simon; Shah, Louise Jivan; Jordan, Ulrike Publication date: 2003 Document Version Publisher's PDF, also known as Version of record Link back to DTU Orbit Citation (APA): Furbo, S., Shah, L. J., & Jordan, U. (2003). Solar energy: state of the art. BYG Sagsrapport No. SR 03-14 General rights Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights. Users may download and print one copy of any publication from the public portal for the purpose of private study or research. You may not further distribute the material or use it for any profit-making activity or commercial gain You may freely distribute the URL identifying the publication in the public portal If you believe that this document breaches copyright please contact us providing details, and we will remove access to the work immediately and investigate your claim. Editors: Simon Furbo Louise Jivan Shah Ulrike Jordan Solar Energy State of the art DANMARKS TEKNISKE UNIVERSITET Internal Report BYG·DTU SR-03-14 2003 ISSN 1601 - 8605 Solar Energy State of the art Editors: Simon Furbo Louise Jivan Shah Ulrike Jordan Department of Civil Engineering DTU-bygning 118 2800 Kgs. Lyngby http://www.byg.dtu.dk 2003 PREFACE In June 2003 the Ph.D. course Solar Heating was carried out at Department of Civil Engineering, Technical University of Denmark. -

A Comprehensive Review of Thermal Energy Storage

sustainability Review A Comprehensive Review of Thermal Energy Storage Ioan Sarbu * ID and Calin Sebarchievici Department of Building Services Engineering, Polytechnic University of Timisoara, Piata Victoriei, No. 2A, 300006 Timisoara, Romania; [email protected] * Correspondence: [email protected]; Tel.: +40-256-403-991; Fax: +40-256-403-987 Received: 7 December 2017; Accepted: 10 January 2018; Published: 14 January 2018 Abstract: Thermal energy storage (TES) is a technology that stocks thermal energy by heating or cooling a storage medium so that the stored energy can be used at a later time for heating and cooling applications and power generation. TES systems are used particularly in buildings and in industrial processes. This paper is focused on TES technologies that provide a way of valorizing solar heat and reducing the energy demand of buildings. The principles of several energy storage methods and calculation of storage capacities are described. Sensible heat storage technologies, including water tank, underground, and packed-bed storage methods, are briefly reviewed. Additionally, latent-heat storage systems associated with phase-change materials for use in solar heating/cooling of buildings, solar water heating, heat-pump systems, and concentrating solar power plants as well as thermo-chemical storage are discussed. Finally, cool thermal energy storage is also briefly reviewed and outstanding information on the performance and costs of TES systems are included. Keywords: storage system; phase-change materials; chemical storage; cold storage; performance 1. Introduction Recent projections predict that the primary energy consumption will rise by 48% in 2040 [1]. On the other hand, the depletion of fossil resources in addition to their negative impact on the environment has accelerated the shift toward sustainable energy sources. -

Solar Combisystems

Method and comparison of advanced storage concepts A Report of IEA Solar Heating and Cooling programme - Task 32 “Advanced storage concepts for solar and low energy buildings” Report A4 of Subtask A December 2007 Jean-Christophe Hadorn Thomas Letz Michel Haller Method and comparison of advanced storage concepts Jean-Christophe Hadorn, BASE Consultants SA, Geneva, Switzerland Thomas Letz INES Education, Le Bourget du Lac, France Contribution on method: Michel Haller Institute of Thermal Engineering Div. Solar Energy and Thermal Building Simulation Graz University of Technology Inffeldgasse 25 B, A-8010 Graz A technical report of Subtask A BASE CONSULTANTS SA 8 rue du Nant CP 6268 CH - 1211 Genève INES - Education Parc Technologique de Savoie Technolac 50 avenue du Léman BP 258 F - 73 375 LE BOURGET DU LAC Cedex 3 Executive Summary This report presents the criteria that Task 32 has used to evaluate and compare several storage concepts part of a solar combisystem and a comparison of storage solutions in a system. Criteria have been selected based on relevance and simplicity. When values can not be assessed for storage techniques to new to be fully developped, we used more qualitative data. Comparing systems is always a very hard task. Boundary conditions and all paramaters must be comparable. This is very difficult to achieve when 9 analysts work around the world on similar systems but with different storage units. This report is an attempt of a comparison. Main generic results that we can draw with some confidency from the inter comparison of systems are: - The drain back principle increases thermal performances because it does not use of a heat exchanger in the solar loop and increases therefore the efficiency of the solar collector. -

Building Envelope and Thermal Storage

Energies 2012, 5, 3972-3985; doi:10.3390/en5103972 OPEN ACCESS energies ISSN 1996-1073 www.mdpi.com/journal/energies Article Residential Solar-Based Seasonal Thermal Storage Systems in Cold Climates: Building Envelope and Thermal Storage Alexandre Hugo 1 and Radu Zmeureanu 2,* 1 Halsall Associates, 2300 Yonge Street, Suite 2300 Toronto, Ontario M4P 1E4, Canada; E-Mail: [email protected] 2 Department of Building, Civil and Environmental Engineering, Faculty of Engineering and Computer Science, Concordia University, Montréal, Québec H3G 1M8, Canada * Author to whom correspondence should be addressed; E-Mail: [email protected]; Tel.: +1-514-848-2424 (ext. 3203); Fax: +1-514-848-7965. Received: 21 August 2012; in revised form: 26 September 2012 / Accepted: 8 October 2012 / Published: 16 October 2012 Abstract: The reduction of electricity use for heating and domestic hot water in cold climates can be achieved by: (1) reducing the heating loads through the improvement of the thermal performance of house envelopes, and (2) using solar energy through a residential solar-based thermal storage system. First, this paper presents the life cycle energy and cost analysis of a typical one-storey detached house, located in Montreal, Canada. Simulation of annual energy use is performed using the TRNSYS software. Second, several design alternatives with improved thermal resistance for walls, ceiling and windows, increased overall air tightness, and increased window-to-wall ratio of South facing windows are evaluated with respect to the life cycle energy use, life cycle emissions and life cycle cost. The solution that minimizes the energy demand is chosen as a reference house for the study of long-term thermal storage. -

Reference System, Germany Solar Combisystem for Multi-Family House INFO Sheet a 10

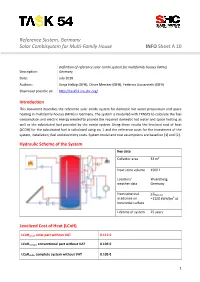

Reference System, Germany Solar Combisystem for Multi-Family House INFO Sheet A 10 Definition of reference solar combi system for multifamily houses (MFH), Description: Germany Date: July 2018 Authors: Sonja Helbig (ISFH), Oliver Mercker (ISFH), Federico Giovannetti (ISFH) Download possible at: http://task54.iea-shc.org/ Introduction This document describes the reference solar combi system for domestic hot water preparation and space heating in multifamily houses (MFH) in Germany. The system is modelled with TRNSYS to calculate the fuel consumption and electric energy needed to provide the required domestic hot water and space heating as well as the substituted fuel provided by the combi system. Using these results the levelized cost of heat (LCOH) for the substituted fuel is calculated using eq. 1 and the reference costs for the investment of the system, installation, fuel and electricity costs. System model and cost assumptions are based on [1] and [2]. Hydraulic Scheme of the System Key data Collector area 33 m² Heat store volume 1500 l Location/ Wuerzburg, weather data Germany Hemispherical Ghem,hor irradiance on =1120 kWh/(m2 a) horizontal surface Lifetime of system 25 years Levelized Cost of Heat (LCoH) LCoHsol,fin solar part without VAT 0.112 € LCoHconv,fin conventional part without VAT 0.103 € LCoHov,fin complete system without VAT 0.105 € 1 Reference System, Germany Solar Combisystem for Multi-Family House INFO Sheet A 10 Details of the System Location Wuerzburg, Germany Type of system Combisystem Weather data TRY 2 - hemispherical -

Solar Combisystems

INDUSTRY NEWSLETTER An yearly update for industrial companies Nr. 3 January 2003 IEA SHC - TASK 26 Solar Combisystems (Source: Wagner &Co, Germany) CONTENTS Task 26 is completed............................................................................................................................... 2 The Altener Combisystems Project........................................................................................................ 8 Dissemination activities within the ALTENER Project „Solar Combisystems“..................................... 9 Drainback technology ........................................................................................................................... 11 The FSC procedure, a powerful design tool.......................................................................................... 14 Promising market development for solar combisystems....................................................................... 18 SHC-TASK 26 Participants................................................................................................................... 20 SHC-TASK 26 Industry Participants ................................................................................................... 24 Neither the experts nor IEA SH&C can assume any liability for information provided in this Newsletter. Edited by Jean-Marc Suter and Irene Bergmann http://www.iea-shc.org 2 Task 26 is completed By Operating Agent Werner Weiss, AEE INTEC, Arbeitsgemeinschaft ERNEUERBARE ENERGIE, Institute for Sustainable Technologies, -

Analysis of System Improvements in Solar Thermal and Air Source Heat

Analysis of system improvements in solar thermal and air source heat pump combisystems Stefano Poppi, Chris Bales, Andreas Heinz, Franz Hengel, David Chèze, Igor Mojic, Catia Cialani To cite this version: Stefano Poppi, Chris Bales, Andreas Heinz, Franz Hengel, David Chèze, et al.. Analysis of system improvements in solar thermal and air source heat pump combisystems. Applied Energy, Elsevier, 2016, 173 (1), pp.606-623. 10.1016/j.apenergy.2016.04.048. cea-01310230 HAL Id: cea-01310230 https://hal-cea.archives-ouvertes.fr/cea-01310230 Submitted on 2 May 2016 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Analysis of system improvements in solar thermal and air source heat pump combisystems. Stefano Poppi*1,2, Chris Bales1, Andreas Heinz4, Franz Hengel4, David Chèze6, Igor Mojic5, Catia Cialani3 1Solar Energy Research Center (SERC), Dalarna University College, S-79188 Falun, Sweden 2Department of Energy Technology, KTH, SE-100 44 Stockholm, Sweden 3Department of Economics, Dalarna University College, S-79188 Falun, Sweden 4Institute of Thermal Engineering, Graz University of Technology, Inffeldgasse 25b, A-8010 Graz, Austria 5Institut für Solartechnik SPF, University of Applied Sciences HSR, Oberseestr. 10, 8640 Rapperswil, Switzerland 6CEA, LITEN, Department of Solar Technologies, F-73375 Le Bourget du Lac, France *Corresponding author. -

Combisol Publishable Report.Pdf

Solar Combisystems Promotion and Standardisation Final report Created by: Philippe Papillon Staff member of CEA-INES Contributions from Jan Erik Nielsen (PlanEnergi), Xavier Cholin, Thomas Letz (INES Education), Alexander Thür, Gabrielle Kuhness (AEE INTEC) Chris Bales (SERC) Philippe Papillon, Mickael Albaric (CEA-INES) Barbara Mette, Jens Ullmann, Harald Drueck (ITW) (2010) Date 12/20/2010 Version Final Revision 2 The sole responsibility for the content of this publication lies with the authors. It does not necessarily reflect the opinion of the European Union. Neither the EACI nor the European Commission are responsible for any use that may be made of the information contained therein. CONTENTS Symbol list ............................................................................................................................... 5 Table list .................................................................................................................................. 6 Figure list................................................................................................................................. 6 Introduction ............................................................................................................................. 9 1 Potential of solar combisystems ....................................................................................... 10 2 Typical solar combisystem................................................................................................ 14 2.1 Different hydraulic schemes...................................................................................................14 -

Idronics 6: Solar Thermal Combisystems

Idronics#6 Feat_rev2.indd 1 5/4/10 2:57:56 PM CaleffiCaleffi North North America, America, Inc. Inc. 98503883 South W. Milwaukee 54th Street Rd Franklin,Milwaukee, WI 53132 Wisconsin 53208 T:T: 414.421.1000414.238.2360 F: F: 414.421.2878 414.238.2366 Dear Hydronic Professional, Dear Hydronic Professional, Welcome to the 6th edition of idronics, Caleffi ’s semi-annual design journal Welcomefor hydronic to theprofessionals. 2nd edition of idronics – Caleffi’s semi-annual design journal for hydronic professionals. The global recession has slowed nearly all industries over the past year. TheHowever, 1st edition despite of idronicsdeclines was in construction, released in January solar water 2007 heater and distributed shipments to over 80,000in the US people increased in North 50% America. during 2008.It focused on the topic hydraulic separation. From the feedback received, it’s evident we attained our goal of explaining the benefits andAs more proper and application more HVAC of professionalsthis modern design become technique familiar forwith hydronic solar water systems. heating, many recognize opportunities to extend solar thermal technology A Technical Journal Iffor you combined haven’t domesticyet received hot a water copy andof idronics space heating#1, you applications.can do so by Thissending is a in the attachedtrend our reader parent response Caleffi SpA card, identifi or by ed registering several years online ago at in www.caleffi.us Europe, and is. The from publicationnow a topic willof growing be mailed interest to you here free inof North charge. America. You can For also this download reason, the Caleffi Hydronic Solutions completesolar “combisystems” journal as a PDF was fileselected from our as theWeb topic site. -

Solar & Hydronic Heating

TECHNICAL FEATURE This article was published in ASHRAE Journal, February 2012. Copyright 2012 American Society of Heating, Refrigerating and Air-Conditioning Engineers, Inc. Posted at www.ashrae.org. This article may not be copied and/or distributed electronically or in paper form without permission of ASHRAE. For more information about ASHRAE Journal, visit www.ashrae.org. A B Photo 1a (left): Small commercial solar combisystem. Photo 1b (right): Residential solar combisystem. Integrating Solar & Hydronic Heating In Residential and Small Commercial Systems By Bristol Stickney uses, not just a single water tank. In a combisystem, it is typical for a large his article and the following companion article, “Advantages group of collectors to provide heat for space heating, water heating, and other Tof Integrated Control in Solar Combisystems,” share our field uses such as boiler preheat, pools, spas, ice melt, and heat storage. The piping experience in the solar heating industry for those seeking better involved in these systems can seem complex, and the control systems for- ways to apply solar thermal technology in their heating system de- midable. But the technology has ma- tured and the energy savings can be signs. This article discusses applications where hot water produced significant, so solar heating should not be overlooked. by solar collectors can be easily allocated to multiple uses with a The information presented here is es- simple piping configuration and straightforward control strategies. sentially a report from the field, draw- ing upon the experience of more than The detailed control of these systems is more thoroughly described 100 solar-heated combisystems in- stalled and operating over the past five in the companion article. -

A Methodology for Optimizing Solar Thermal Combisystems: from Data Collection to Multi- Objective Optimization

________________________________________________________________________________________________ A Methodology for Optimizing Solar Thermal Combisystems: From Data Collection to Multi- Objective Optimization Anthony Rey, Radu Zmeureanu Centre for Net-Zero Energy Buildings Studies, Department of Building, Civil and Environmental Engineering, Gina Cody School of Engineering and Computer Science, Concordia University, Montreal, Quebec, Canada analysis of a solar combisystem was performed in (Kaçan Abstract and Ulgen, 2014) based on an experimental setup built in This paper presents a methodology for optimizing solar Turkey. Tank volume was found to be one of the most thermal combisystems from data collection to multi- important parameters to reduce the energy use. objective optimization, which is applied to an existing Experimental data from a solar thermal combisystem, residential solar thermal combisystem installed in installed in Ireland, were used to calibrate a TRNSYS Massachusetts, USA. This solar combisystem, installed in model in (Clarke et al., 2014). The effect of solar an occupied house, is composed of two distinct arrays of combisystem components on the overall system exergy 2 flat-plate collectors of 15.8 m connected to a thermal efficiency was assessed in (Kaçan, 2015). The optimum storage tank of 617 litres, and provides for domestic hot overall exergy efficiency of 11.95% was obtained. The water and space heating. The methodology comprises: (i) lack of uncertainty analysis associated with building presentation of the solar combisystem, (ii) outliers performance simulations was reported in (Attia et al., detection and uncertainty analysis of measurements, (iii) 2013). model validation, (iv) trend data analysis, and (v) multi- Only a few studies have focused on the optimization of objective optimization. -

Solar Update

S LAR UPDATE NEWSLETTER OF THE INTERNATIONAL ENERGY AGENCY SOLAR HEATING AND COOLING PROGRAMME • NO. 35 DECEMBER 2000 Solar Combisystems for a Sustainable Energy Future ince December 1998, 25 experts and 11 solar industries Denmark, Germany and Switzerland, the demand for solar com- from 9 countries have been collaborating to further devel- bisystems is increasing rapidly (see figure 1). Sop and optimize solar combisystems for detached single- family houses, groups of single-family houses and multi-family houses. This project, which is part of the Solar Heating and What is a Combisystem? Cooling Programme, is working to standardize the classification Solar combisystems are solar heating systems for combined and evaluation of solar combisystems with the overall objective domestic hot water preparation and space heating. They are sim- of developing recommendations for the international standard- ilar to solar water heaters in that they use solar energy and trans- ization of combisystem test procedures. port the produced heat to a storage device. The major difference is that the installed collector area is generally larger for com- bisystems, as there are two heat loads to meet. Also, a combisys- Why Solar Space Heating? tem uses at least two energy sources to supply hot water and Throughout the world, hundreds of thousands of domestic solar heating—a solar collector and an auxiliary energy source. The hot water systems are demonstrating the possibilities of this auxiliary energy source could be biomass, gas, oil or electricity. renewable energy source. Due to the success of these hot water The key design challenge is how to integrate the different systems, more builders are turning to solar energy for space requirements of the heating source and the heating loads into a heating.