Molson Coors Brewing Company 2015 Third Quarter Earnings

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Elyxir Price List

Effective: 6/3/2015 Product List COORS 1198 COORS LT 1/4 KEG 1111111111 1199 COORS LT 1/2 KEG 1111111111 BLUEMOON ID Product Name Unit UPC COORS N/A ID Product Name Unit UPC 3800 BLUEMOON BELGIAN WHITE 4/6/12 LNNR 7199009511 1906 COORS N/A 2/12/12 CN 7199077008 3802 BLUEMOON BELGIAN WHITE 2/12/12 LNN 7199009516 1950 COORS N/A 4/6/12 LNNR 7199077005 3805 BLUEMOON BELGIAN WHITE 15/22 NR 7199009513 3806 BLUEMOON BELGIAN WHITE 2/12/12 CN 7199009506 KEYSTONE 3807 BLUEMOON BELGIAN WHITE 1/6 KEG 1111111111 ID Product Name Unit UPC KEYSTONE ICE 2/12/12 CN 3809 BLUEMOON BELGIAN WHITE 1/2 KEG 1111111111 2206 7199047702 KEYSTONE ICE 30/12 CN 3816 BLUEMOON BELGIAN WHITE 6/4/16 CN 7199009545 2225 7199047714 3839 BLUEMOON WHITE IPA 1/2 KEG KILLIANS RED 3841 BLUEMOON WHITE IPA 4/6/12 LNNR 7199009561 ID Product Name Unit UPC KILLIAN'S RED 4/6/12 LNNR 3847 BLUEMOON WHITE IPA 1/6 KEG 3550 7199070002 3894 BLUEMOON CINNAMON HORCHATA 4/6/12 LNNR 7199009584 MOLSON COORS BANQUET ID Product Name Unit UPC MOLSON CANADIAN 2/12/12 LNNR ID Product Name Unit UPC 3722 6821303117 1000 COORS BANQUET 4/6/12 CAN 7199000007 KEYSTONE LT 1006 COORS BANQUET 2/12/12 CAN 7199000047 ID Product Name Unit UPC 1015 COORS BANQUET 18/12 CAN 7199010020 2106 KEYSTONE LT 2/12/12 CAN 7199048004 1022 COORS BANQUET 20/12 CN 7199017017 2125 KEYSTONE LT 30/12 CAN 7199048019 1025 COORS BANQUET 30/12 CAN 7199010033 2133 KEYSTONE LT 12/24OZ CAN 7199048024 1029 COORS BANQUET 4/6/16 CAN 7199010002 BLUEMOON SEASONAL 1033 COORS BANQUET 12/24OZ CAN 7199010071 ID Product Name Unit UPC 1050 COORS -

Molson Coors Beverage Company

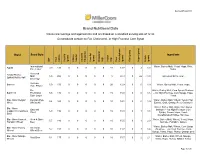

Revised 04/12/2021 Molson Coors Beverage Company Nutritional, Ingredient and Fermentation Source Data – Brands Sold in the U.S. Only Values are average and approximate and are based on a standard regulatory serving size. Our products contain no Fat, Cholesterol, or High Fructose Corn Syrup Where corn syrup is used as an adjunct to aid fermentation, it is consumed by yeast during that process and is not present in the final product Brand Brand Style Ingredients and Fermenation Sources Serving Size ABV Total Calories Total Fat (grams) Calories from Fat Saturated (grams) Fat Trans Fat (grams) Cholesterol (mg) Sodium (mg) Total Carbohydrates (grams) Fiber(grams) Sugars (grams) Protein (grams) German- Barmen 12 oz 5.0 156 0 0 0 0 0 20 12.9 0 0 1.9 Water, Barley Malt, Yeast, Hops Style Pilsner Pre- Water, Barley Malt, Corn Syrup Batch 19 Prohibition 12 oz 5.5 174 0 0 0 0 0 15 15.0 0 0 1.6 (Dextrose)*, Hops, Yeast Style Lager Blue Moon Belgian Belgian-Style Water, Barley Malt, Wheat, Yeast, Hop 12 oz 5.4 168 0 0 0 0 0 10 14.1 0 0 1.9 White Wheat Ale Extract, Oats, Orange Peel, Coriander Blue Moon Harvest Herb & Spice Water, Barley Malt, Wheat, Yeast, Hops, 12 oz 5.7 180 0 0 0 0 0 10 15.5 0 1 2.0 Pumpkin Wheat Beer Sucrose, Pumpkin, Spices Water, Barley Malt, Wheat, Corn Syrup Blue Moon Honey American 12 oz 5.2 153 0 0 0 0 0 10 11.7 0 3 1.4 (Dextrose)*, Yeast, Hops, Honey, Orange Wheat Wheat Beer peel Water, Barley Malt, Wheat, Oats, Corn Blue Moon Iced Blonde Ale 12 oz 5.4 185 0 0 0 0 0 10 17.2 TBD 5.00 3.0 Syrup (Dextrose)*, Decaffeinated Coffee, -

Sabmiller and Molson Coors to Combine U.S. Operations in Joint Venture

SABMILLER AND MOLSON COORS TO COMBINE U.S. OPERATIONS IN JOINT VENTURE • Combination of complementary assets will create a stronger, more competitive U.S. brewer with an enhanced brand portfolio • Greater scale and resources will allow additional investment in brands, product innovation and sales execution • Consumers and retailers will benefit from greater choice and access to brands • Distributors will benefit from a superior core brand portfolio, simplified systems, lower operating costs and improved chain account programs • $500 million of annual cost synergies will enhance financial performance • SABMiller and Molson Coors with 50%/50% voting interest and 58%/42% economic interest 9 October 2007 (London and Denver) -- SABMiller plc (SAB.L) and Molson Coors Brewing Company (NYSE: TAP; TSX) today announced that they have signed a letter of intent to combine the U.S. and Puerto Rico operations of their respective subsidiaries, Miller and Coors, in a joint venture to create a stronger, brand-led U.S. brewer with the scale, resources and distribution platform to compete more effectively in the increasingly competitive U.S. marketplace. The new company, which will be called MillerCoors, will have annual pro forma combined beer sales of 69 million U.S. barrels (81 million hectoliters) and net revenues of approximately $6.6 billion. Pro forma combined EBITDA will be approximately $842 million1. SABMiller and Molson Coors expect the transaction to generate approximately $500 million in annual cost synergies to be delivered in full by the third full financial year of combined operations. The transaction is expected to be earnings accretive to both companies in the second full financial year of combined operations. -

Domestically Brewed Beers

Menu_0710rev_Pub500Menu.New6.07.qxd 7/8/10 3:33 PM Page 1 { PUB 500 WORLD BEER CRUISE } Welcome! The Pub continues its cruise around the world to bring you the finest beers from every corner of the globe. When you sign up to sail, all you have to do is drink one of each beer listed on our cruise menu (not all in one sitting of course). When you finish the cruise, you will be awarded a World Beer Cruise Fleece Jacket ($90 value). Ask your server or bartender how to sign up and set sail. BEER SELECTIONS ARE SUBJECT TO AVAILABILITY AND THE ADMIRAL’S WHIM. { DOMESTICALLY BREWED BEERS } { INTERNATIONALLY BREWED BEERS } CALIFORNIA Chico AUSTRALIA Sydney Sierra Nevada Pale Ale (1) Foster’s Lager (43) San Francisco BELGIUM Leuven Stella Artois (44) Anchor Steam (78) CANADA London, ONT COLORADO Breckenridge Labatt Blue Pilsner (45) Breckenridge Oatmeal Stout (2) Molson Canadian (46) Denver Saint John, NB { HEARTY FARE } Blue Moon Belgian White (3) Moosehead Lager (47) Killian’s Irish Red (4) CHINA Qingdal Golden Tsingtao (48) Coors Light (5) CZECH REPUBLIC Pilsen Coors (28) Pilsner Urquell (49) MASSACHUSETTS Boston DENMARK Copenhagen Samuel Adams (6) Carlsberg (50) Samuel Adams Light (7) ENGLAND Hereford Strongbow Cider (30) MINNESOTA New Ulm Grain Belt Nordeast (22) London Bass Pale Ale (51) Grain Belt Premium (8) Grain Belt Premium Light (9) Newcastle Rag Top Amber (10) Newcastle Brown Ale (52) Schell’s Rotating Specialty (11) GERMANY Bremen Schell’s Firebrick Lager (12) Beck’s (53) Schell’s Deer Brand (13) St. Pauli Girl Lager (54) Schell’s Pilsner (14) Munich Schell’s Seasonal (15) Hacker-Pschorr (55) Schell’s Dark (19) Warstein Schell’s Light (20) Warsteiner Premium Verum (56) Schell’s Stout (21) HOLLAND Amsterdam St. -

BROWN JUG CURBSIDE BEER SELECTION Beer Import NA HEINEKEN 00 NON ALCOHOLIC 6B $ 10.29 Belgian LINDEMANS FRAMBOISE 25.4OZ $

BROWN JUG CURBSIDE BEER SELECTION FOUR LOKO WATERMELON 23.5OZ $ 2.99 JOOSE B-BERRY 23OZ $ 4.00 Beer Import NA JOOSE MAS MANGO $ 4.00 HEINEKEN 00 NON ALCOHOLIC 6B $ 10.29 JOOSE SCREWDRIVER 23.5Z $ 4.00 MIKES BLACK CHERRY 23.5Z $ 2.99 Belgian MIKES HARD MANGO PUNCH 6B $ 10.49 LINDEMANS FRAMBOISE 25.4OZ $ 10.99 MIKES HARDER BLACK CHERRY 16Z $ 1.99 STELLA ARTOIS 12B $ 17.99 MIKES HARDER BLK CHERRY 23.5Z $ 2.99 STELLA ARTOIS 12C $ 17.99 MIKES HARDER COLLECTIBLES 16Z $ 1.99 STELLA ARTOIS 6B $ 9.99 MIKES HARDER CRANBERRY 23Z $ 2.99 MIKES HARDER CRANLEM 16Z C $ 1.99 Canadian MIKES HARDER LEMONADE 16Z C $ 1.99 MOLSON CANADIAN 12B $ 14.99 MIKES HARDER LEMONADE 23Z $ 2.99 MOLSON ICE 12B $ 14.99 MIKES HARDER MANGO 23.5Z $ 2.99 MOOSEHEAD 12B $ 17.99 MIKES HARDER SEASONAL 23.5Z $ 2.99 UNIBROUE L FIN D MONDE $ 8.49 MIKES LEMONADE 6B $ 10.49 MIKES MXD LONG ISLAND 16OZ $ 4.00 Cider MIKES PARTY PACK 12B $ 18.99 ACE GUAVA CIDER 6C $ 11.99 MIKES RASPBERRY LEMONADE 6B $ 10.49 ACE PINEAPPLE CIDER 6B $ 11.99 MIKES STRAW PINEAPPLE 23.5Z $ 2.99 AK CIDERWORKS BACKCOUNTRY 6C $ 12.99 MIKES STRAWBERRY LEMONADE 16Z $ 1.99 AK CIDERWORKS NORTHWIND 6C $ 12.99 MIKES STRAWBERRY LEMONADE 6B $ 10.49 ANGRY ORCHARD CRISP APPLE 16Z $ 2.00 MIKES VARIETY 16OZ 8C $ 14.99 ANGRY ORCHARD CRISP APPLE 6B $ 10.99 MIKES VARIETY PACK 12C $ 18.99 ANGRY ORCHARD GREEN APPLE 6B $ 10.99 NATTY RUSH HURRICAN PUNCH 25OZ $ 4.00 DOUBLE SHOVEL APPALANCHE 4C $ 12.49 SEAGRAMS WILD BERRY SINGLE $ 1.49 DOUBLE SHOVEL FORGET ME HOP 4C $ 12.49 SMIRNOFF ICE 6B $ 10.49 INCLINE PRICKLY PEAR 19.2OZ $ 4.49 -

FORM 10-K Molson Coors Beverage Company

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 _______________________________________________________________ FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ______ to ______ . Commission File Number: 1-14829 Molson Coors Beverage Company (Exact name of registrant as specified in its charter) Delaware (State or other jurisdiction of incorporation or organization) 1801 California Street, Suite 4600, Denver, Colorado, USA 1555 Notre Dame Street East, Montréal, Québec, Canada (Address of principal executive offices) 84-0178360 (I.R.S. Employer Identification No.) 80202 H2L 2R5 (Zip Code) 303-927-2337 (Colorado) 514-521-1786 (Québec) (Registrant's telephone number, including area code) _______________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading symbols Name of each exchange on which registered Class A Common Stock, $0.01 par value TAP.A New York Stock Exchange Class B Common Stock, $0.01 par value TAP New York Stock Exchange 1.25% Senior Notes due 2024 TAP New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. -

Molson Coors Beverage Annual Report 2020

Molson Coors Beverage Annual Report 2020 Form 10-K (NYSE:TAP) Published: February 12th, 2020 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 _______________________________________________________________ FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ______ to ______ . Commission File Number: 1-14829 Molson Coors Beverage Company (Exact name of registrant as specified in its charter) Delaware (State or other jurisdiction of incorporation or organization) 1801 California Street, Suite 4600, Denver, Colorado, USA 1555 Notre Dame Street East, Montréal, Québec, Canada (Address of principal executive offices) 84-0178360 (I.R.S. Employer Identification No.) 80202 H2L 2R5 (Zip Code) 303-927-2337 (Colorado) 514-521-1786 (Québec) (Registrant's telephone number, including area code) _______________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading symbols Name of each exchange on which registered Class A Common Stock, $0.01 par value TAP.A New York Stock Exchange Class B Common Stock, $0.01 par value TAP New York Stock Exchange 1.25% Senior Notes due 2024 TAP New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Y es ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. -

Brand Nutritional Data Values Are Average and Approximate and Are Based on a Standard Serving Size of 12 Oz

Revised 05/28/2019 Brand Nutritional Data Values are average and approximate and are based on a standard serving size of 12 oz. Our products contain no Fat, Cholesterol, or High Fructose Corn Syrup Brand Brand Style Ingredients ABV Total Calories Fat Total (grams) Calories Fat from Saturated Fat (grams) Trans Fat (grams) Cholesterol (mg) Sodium (mg) Total Carbohydrates (grams) Fiber (grams) Sugars (grams) Protein (grams) International Water, Barley Malt, Yeast, Hops, Rice, Aguila 3.9 126 0 0 0 0 0 10 13.7 0 2 1.0 Pale Lager Sugar Flavored Arnold Palmer Malt 5.0 206 0 0 0 0 0 5 28.3 0 26 < 1.0 Ingredient list to come Spiked Half & Half Beverage German- Barmen 5.0 156 0 0 0 0 0 20 12.9 0 0 1.9 Water, Barley Malt, Yeast, Hops Style Pilsner Pre- Water, Barley Malt, Corn Syrup (Dextrose Batch 19 Prohibition 5.5 174 0 0 0 0 0 15 15.0 0 0 1.6 – not High-Fructose Corn Syrup), Hops, Style Lager Yeast Blue Moon Belgian Belgian-Style Water, Barley Malt, Wheat, Yeast, Hop 5.4 168 0 0 0 0 0 10 14.1 0 0 1.9 White Wheat Ale Extract, Oats, Orange Peel, Coriander Water, Barley Malt, Oats, Corn Syrup Blue Moon Oatmeal (Maltose – not High-Fructose Corn Cappuccino Oatmeal 5.9 196 0 0 0 0 0 10 18.8 0 1 1.8 Stout Syrup), Cocoa, Hops, Yeast, Stout Decaffeinated Coffee, Sucrose Blue Moon Harvest Herb & Spice Water, Barley Malt, Wheat, Yeast, Hops, 5.7 180 0 0 0 0 0 10 15.5 0 1 2.0 Pumpkin Wheat Beer Sucrose, Pumpkin, Spices Water, Barley Malt, Wheat, Corn Syrup Blue Moon Honey American 5.2 153 0 0 0 0 0 10 11.7 0 3 1.4 (Dextrose – not High-Fructose Corn Wheat -

Vysoká Škola Hotelová V Praze 8, Spol. S R. O

Vysoká škola hotelová v Praze 8, spol. s r. o. Hana Vágnerová Pivovarnictví v ČR a ve světě - trendy a inovace Diplomová práce 2013 Pivovarnictví v ČR a ve světě - trendy a inovace Diplomová práce Bc. Hana Vágnerová Vysoká škola hotelová v Praze 8, spol. s r. o. katedra hotelnictví Studijní obor: Management hotelnictví a lázeňství Vedoucí diplomové práce: Ing. Dana Johnová Datum odevzdání diplomové práce: 2013-05-07 Datum obhajoby diplomové práce: E-mail: [email protected] Praha 2013 Master´s Dissertation World and Czech Brewing - trends and inovations Bc. Hana Vágnerová The Institute of Hospitality Management in Prague 8, Ltd. Department of Hotel Management Major: Hospitality and Spa Management Thesis Advisor: Ing. Dana Johnová Date of Submission: 2013-05-07 Date of Thesis Defense: E-mail: [email protected] Praha 2013 Čestné prohlášení P r o h l a š u j i, že jsem diplomovou práci na téma Pivovarnictví v ČR a ve světě - trendy a inovace zpracovala samostatně a veškerou použitou literaturu a další podkladové materiály, které jsem použila, uvádím v seznamu použitých zdrojů a že svázaná a elektronická podoba práce je shodná. V souladu s § 47b zákona č. 111/1998 Sb., o vysokých školách v platném znění souhlasím se zveřejněním své diplomové práce, a to v nezkrácené formě, v elektronické podobě ve veřejně přístupné databázi Vysoké školy hotelové v Praze 8, spol. s r. o. Hana Vágnerová V Praze dne 7. května 2013 Abstrakt Vágnerová Hana. Pivovarnictví v ČR a ve světě - trendy a inovace. Diplomová práce. Vysoká škola hotelová v Praze 8, spol. -

The Beverage Company Beer List

The Beverage Company Beer List Dogfish Head 90 Minute Ipa Michelob Ultra 20 Pk Btls Magic Hat Jinx 6pk Michelob Light 20pk Btls Kronenbourg 1664 4/6 Budweiser 220z Btl Beers Of The World Bud 16oz Single Delirium Tremors Bud Light 16oz Saison Dupont Icehouse 22oz Btl Delirium Nocturnum Icehouse 30pk Bud 120z Btl Budweiser Select 24oz 15pk Bud Ice 12oz Btl High Life 24oz Btl Bud Select 12oz Btl Lite 6‐Pack/16 Oz Busch 12oz Btl Bud Light Lime Alum 6/4 Busch Light 12oz Btl Budweiser Chelada 4pk Michelob Light 12oz Btl Odouls Amber 12pk Michelob Ultra Btl Lite 24pk 16oz Harley Cans Michelob Ultra Amber Blatz 24pk Btl Zima Hard Punch Odouls Amber 1/2bbl Lite Easy Chill 16oz Plastic Bud Light Lime 4pk Alum Steel Reserve 12pk Can Bud Light 6/4 Alum Btl Coors Light 18pk 16oz Bud 16oz Aulm.Btl 4pk Coors Winterfest 6pk Bud Light 24pk Pet Coors Light Nfl Mini Keg Budweiser 16oz Aluminum 15pk Old Style 1/2 Bbl Bud Light 16oz Aluminum 15pk Coors Light Btl Busch 1/4 Bbl Lite 18pk Btl Busch Light 1/4 Bbl Killians Single Michelob Ultra 18pk Btl Rock Green Light 12pk Btl Michelob Light 18pk Btl Bud Light 12oz Btl Michelob Ultra 1/6 Bbl Michelob Celebrate Gift Pk Michelob Ultra 1/2 Bbl Icehouse 4/6 Btl Michelob Light 1/2 Bbl Icehouse 6pk Btl Michelob Light 1/6 Bbl Budweiser Select 16oz 15pk Alu Michelob Amber Bock 1/6 Bbl Coors Light 18pk 16oz Plastic Green Light 6pk Michelob Amber Budweiser 24 Pk Plastic Btl Coors Light 1/4 Bbl Lite 16oz Pet High Life 18pk Btl Genuine Draft 12pk Btl Bud Light 7oz Christmas Btl High Life 1/2 Bbl Bud Light 7oz Christmas -

Drink Menu Great Beer

GOOD FOOD GREAT BEER in London’s Downtown DRINK MENU Purveyors of over 100 of the finest beers and ciders and representing 29 countries worldwide. Cheers! We hope you enjoy. BEER CANADA TYPE SIZE ALC % COST GERMANY TYPE SIZE ALC % COST Molson Canadian Lager 341 5.0 $5.00 Beck’s Pale Lager 500 5.0 $8.72 Molson Canadian 67 Lager 341 5.0 $5.00 DAB Pale Lager 440 5.0 $5.53 Coors Light Lager 341 4.0 $5.00 Lowenbrau Pale Lager 473 5.2 $7.61 Miller Genuine Lager 355 4.7 $5.30 Erdinger Dunkel Dark Ale 500 5.6 $9.03 Moosehead Lager 473 5.0 $6.77 Erdinger Weissbier Wheat 500 5.3 $9.03 Mad Jack Lager 473 5.0 $6.60 Molson Export Pale Ale 341 5.0 $5.00 IRELAND Sleeman Clear Lager 355 5.0 $5.00 Kilkenny Brown Ale 500 4.3 $8.10 Sleeman Cream Ale 355 5.0 $5.49 Smithwick’s Brown Ale 500 4.5 $7.26 Sleeman Honey Brown Lager 355 5.2 $5.49 Guinness Blonde Lager 473 5.0 $7.08 Sapporo Lager 500 5.0 $6.84 Guinness Hop House 13 Lager 500 5.0 $7.96 Harp Pale Lager 500 5.0 $6.73 ASIA Guinness Stout 440 4.2 $7.08 Tsingtao Pale Lager 500 4.5 $6.99 Tiger Pale Lager 500 5.0 $6.99 ITALY Sinha Stout 330 8.8 $8.85 Peroni Pale Lager 500 5.1 $7.52 Singha Pale Lager 330 5.0 $6.82 MEXICO BELGIUM Corona Extra Pale Lager 330 4.6 $6.46 Chimay Blue Cap Ale 330 9.0 $10.10 Dos Equis Pale Lager 473 4.5 $7.92 Chimay White Cap Ale 330 8.0 $9.03 Sol Pale Lager 330 4.5 $6.15 Fruli Ale 330 4.1 $8.73 Modelo Especial Pilsner 330 4.5 $6.46 Leffe Blonde Ale 330 6.6 $7.61 Leffe Brune Ale 330 6.5 $7.61 PORTUGAL Rochefort 8 Ale 330 9.2 $9.03 Sagres Pale Lager 330 5.1 $5.27 CARIBBEAN SCANDINAVIA -

Millercoors Reports Lower Third Quarter Underlying Net Income

MILLERCOORS REPORTS LOWER THIRD QUARTER UNDERLYING NET INCOME BUT HIGHER NET REVENUE PER BARREL Coors Light and Miller Lite Gain Market Share of Premium Light Segment in the Third Quarter November 5, 2015 (London and Denver) – SABMiller plc (LN:SAB; OTC:SABMRY) and Molson Coors Brewing Company (NYSE: TAP; TSX: TPX) reported that third quarter MillerCoors underlying net income declined 8.6 percent to $344.4 million versus the same period in the prior year, driven by lower volume and increased marketing investment, partially offset by lower cost of sales, positive sales mix and net pricing growth. For the second consecutive quarter, Coors Light and Miller Lite both gained market share of the Premium Light segment, with Miller Lite delivering volume growth. Combined, Coors Light and Miller Lite delivered their best quarterly performance in three years. “As we relentlessly pursue total portfolio growth, job number one is taking share and growing our American Light Lagers. This past quarter, we took a step in this direction by taking segment share with both Coors Light and Miller Lite,” said Gavin Hattersley, MillerCoors Chief Executive Officer. “We have a lot of work ahead of us to address our economy segment performance, but all other segments across our portfolio are in good shape as we close out the year. Net income was down this quarter due to lower volume, partially due to bringing distributor inventories down as anticipated coming out of peak-selling season, and increased media investments across our brands.” Third Quarter Highlights Unless otherwise indicated, all amounts are in U.S. dollars and calculated in accordance with accounting principles generally accepted in the U.S.