2016 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

Ftse4good UK 50

2 FTSE Russell Publications 19 August 2021 FTSE4Good UK 50 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.81 UNITED GlaxoSmithKline 5.08 UNITED Rentokil Initial 0.67 UNITED KINGDOM KINGDOM KINGDOM Anglo American 2.56 UNITED Halma 0.74 UNITED Rio Tinto 4.68 UNITED KINGDOM KINGDOM KINGDOM Antofagasta 0.36 UNITED HSBC Hldgs 6.17 UNITED Royal Dutch Shell A 4.3 UNITED KINGDOM KINGDOM KINGDOM Associated British Foods 0.56 UNITED InterContinental Hotels Group 0.64 UNITED Royal Dutch Shell B 3.75 UNITED KINGDOM KINGDOM KINGDOM AstraZeneca 8.25 UNITED International Consolidated Airlines 0.47 UNITED Schroders 0.28 UNITED KINGDOM Group KINGDOM KINGDOM Aviva 1.15 UNITED Intertek Group 0.65 UNITED Segro 0.95 UNITED KINGDOM KINGDOM KINGDOM Barclays 2.1 UNITED Legal & General Group 1.1 UNITED Smith & Nephew 0.99 UNITED KINGDOM KINGDOM KINGDOM BHP Group Plc 3.2 UNITED Lloyds Banking Group 2.39 UNITED Smurfit Kappa Group 0.74 UNITED KINGDOM KINGDOM KINGDOM BT Group 1.23 UNITED London Stock Exchange Group 2.09 UNITED Spirax-Sarco Engineering 0.72 UNITED KINGDOM KINGDOM KINGDOM Burberry Group 0.6 UNITED Mondi 0.67 UNITED SSE 1.13 UNITED KINGDOM KINGDOM KINGDOM Coca-Cola HBC AG 0.37 UNITED National Grid 2.37 UNITED Standard Chartered 0.85 UNITED KINGDOM KINGDOM KINGDOM Compass Group 1.96 UNITED Natwest Group 0.77 UNITED Tesco 1.23 UNITED KINGDOM KINGDOM KINGDOM CRH 2.08 UNITED Next 0.72 UNITED Unilever 7.99 UNITED KINGDOM KINGDOM -

Constituents & Weights

2 FTSE Russell Publications 19 August 2021 FTSE 100 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.59 UNITED GlaxoSmithKline 3.7 UNITED RELX 1.88 UNITED KINGDOM KINGDOM KINGDOM Admiral Group 0.35 UNITED Glencore 1.97 UNITED Rentokil Initial 0.49 UNITED KINGDOM KINGDOM KINGDOM Anglo American 1.86 UNITED Halma 0.54 UNITED Rightmove 0.29 UNITED KINGDOM KINGDOM KINGDOM Antofagasta 0.26 UNITED Hargreaves Lansdown 0.32 UNITED Rio Tinto 3.41 UNITED KINGDOM KINGDOM KINGDOM Ashtead Group 1.26 UNITED Hikma Pharmaceuticals 0.22 UNITED Rolls-Royce Holdings 0.39 UNITED KINGDOM KINGDOM KINGDOM Associated British Foods 0.41 UNITED HSBC Hldgs 4.5 UNITED Royal Dutch Shell A 3.13 UNITED KINGDOM KINGDOM KINGDOM AstraZeneca 6.02 UNITED Imperial Brands 0.77 UNITED Royal Dutch Shell B 2.74 UNITED KINGDOM KINGDOM KINGDOM Auto Trader Group 0.32 UNITED Informa 0.4 UNITED Royal Mail 0.28 UNITED KINGDOM KINGDOM KINGDOM Avast 0.14 UNITED InterContinental Hotels Group 0.46 UNITED Sage Group 0.39 UNITED KINGDOM KINGDOM KINGDOM Aveva Group 0.23 UNITED Intermediate Capital Group 0.31 UNITED Sainsbury (J) 0.24 UNITED KINGDOM KINGDOM KINGDOM Aviva 0.84 UNITED International Consolidated Airlines 0.34 UNITED Schroders 0.21 UNITED KINGDOM Group KINGDOM KINGDOM B&M European Value Retail 0.27 UNITED Intertek Group 0.47 UNITED Scottish Mortgage Inv Tst 1 UNITED KINGDOM KINGDOM KINGDOM BAE Systems 0.89 UNITED ITV 0.25 UNITED Segro 0.69 UNITED KINGDOM -

The R&CO Risk-Based UK Index Provides an Alternative to Market

The R&CO Risk-Based UK Index provides an alternative to market-cap weighting with a risk-based approach to index construction. The strategy seeks to equalize risk contribution of index constituents and to maximize risk diversification while avoiding excessive turnover and portfolio concentration. The approach seeks to provide lower volatility, reduced maximum drawdown and higher Sharpe ratio compared with market capitalization indices over the long-term. Rothschild & Co Risk-Based UK TR GBP (Total) 6,871.0 Rothschild & Co Risk-Based UK NR GBP (Total) 6,857.9 MSCI United Kingdom GR LCL (Total) 2,016.9 24.54 24.49 16.45 21.38 27.6621.38 9,000 -9.25 -9.28 -8.76 -22.15 -22.15 -28.46 7,000 13.57 13.55 11.79 5.86 5.86 6.57 4.99 4.95 19.24 5,000 25.62 25.62 14.62 11.83 11.82 -2.16 23.25 23.25 20.09 3,000 2.38 2.37 0.54 22.86 22.86 11.49 1,000 26.58 26.58 18.47 17.96 17.95 10.24 26.70 26.70 18.76 -1,000 4.32 -1.794.30 -7.08 -7.08 -23.37 2002 2004 2006 2008 2010 2012 2014 2016 2018 17.30 12.2217.29 2.27 2.27 -11.78 Risk-Based UK TR GBP 3,217.01 -7.52 -5.20 -8.83 5.06 3.99 5.17 9.76 10.05 Risk-Based UK NR GBP 3,210.90 -7.53 -5.21 -8.84 5.01 3.95 5.14 9.74 10.04 MSCI United Kingdom GR LCL 14,679.63 -9.10 -9.77 -12.11 -3.48 0.57 2.79 5.88 3.55 Risk-Based UK TR GBP 10.83 10.06 9.96 -0.06 0.24 0.01 0.84 0.87 0.86 78.38 74.41 74.33 68.28 69.49 70.67 Risk-Based UK NR GBP 10.83 10.06 9.96 -0.06 0.24 0.01 0.84 0.87 0.86 78.40 74.43 74.35 68.23 69.46 70.66 MSCI United Kingdom GR LCL 13.87 11.57 11.25 -0.33 -0.05 0.20 1.00 1.00 1.00 100.00 100.00 100.00 100.00 -

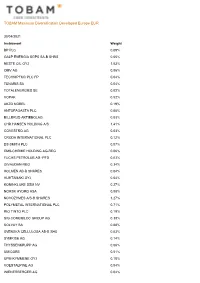

TOBAM Maximum Diversification Developed Europe EUR

TOBAM Maximum Diversification Developed Europe EUR 30/04/2021 Instrument Weight BP PLC 0.09% GALP ENERGIA SGPS SA-B SHRS 0.05% NESTE OIL OYJ 1.03% OMV AG 0.06% TECHNIPFMC PLC FP 0.04% TENARIS SA 0.04% TOTALENERGIES SE 0.02% VOPAK 0.52% AKZO NOBEL 0.19% ANTOFAGASTA PLC 0.05% BILLERUD AKTIEBOLAG 0.03% CHR HANSEN HOLDING A/S 1.41% COVESTRO AG 0.03% CRODA INTERNATIONAL PLC 0.12% DS SMITH PLC 0.07% EMS-CHEMIE HOLDING AG-REG 0.06% FUCHS PETROLUB AG -PFD 0.03% GIVAUDAN-REG 0.34% HOLMEN AB-B SHARES 0.04% HUHTAMAKI OYJ 0.04% KONINKLIJKE DSM NV 0.27% NORSK HYDRO ASA 0.08% NOVOZYMES A/S-B SHARES 1.27% POLYMETAL INTERNATIONAL PLC 0.71% RIO TINTO PLC 0.19% SIG COMBIBLOC GROUP AG 0.38% SOLVAY SA 0.08% SVENSKA CELLULOSA AB-B SHS 0.03% SYMRISE AG 0.14% THYSSENKRUPP AG 0.06% UMICORE 0.51% UPM-KYMMENE OYJ 0.18% VOESTALPINE AG 0.04% WIENERBERGER AG 0.04% TOBAM Maximum Diversification Developed Europe EUR 30/04/2021 Instrument Weight YARA INTERNATIONAL ASA 0.08% A P MOLLER - MAERSK A/S - A 0.06% A P MOLLER - MAERSK A/S - B 0.08% ACS ACTIVIDADES CONS Y SERV 0.07% ADDTECH AB-B SHARES 0.03% ADP 0.04% AENA SA 0.11% ALSTOM 0.17% ANDRITZ AG 0.03% ATLANTIA SPA 0.08% BELIMO HOLDING AG-REG 0.04% BUCHER INDUSTRIES AG-REG 0.04% BUNZL PLC 0.10% DEUTSCHE LUFTHANSA-REG 0.05% DIPLOMA PLC 0.04% DSV PANALPINA A/S 0.45% EASYJET PLC 0.20% ELIS SA 0.03% EPIROC AB-A 0.10% EPIROC AB-B 0.06% FERROVIAL SA 0.05% FLUGHAFEN ZURICH AG-REG 0.03% GEA GROUP AG 0.06% GEBERIT AG-REG 0.21% HAYS PLC 0.03% HOMESERVE PLC 0.04% HOWDEN JOINERY GROUP PLC 0.06% IMCD GROUP NV 0.07% IMI PLC 0.05% -

Chapter 5. Project Environmental Impact 63 5.1

E1188 TRANSLATION FROM RUSSIAN Preparation stage for the Project on Fire Management in High Conservation Value Forests of the Amur-Sikhote-Alin Ecoregion Grant GEF PPG TF051241 Public Disclosure Authorized Public Disclosure Authorized F I N A L R E P O R T Project on Fire Management in High Conservation Value Forests of the Amur- Sikhote-Alin Ecoregion Environmental Impact Assessment Public Disclosure Authorized EIA Leader D.Biol. B.A. Voronov Public Disclosure Authorized Khabarovsk – February 2005 2 Summary Report: 125 pages, figures 4, tables 12, references 70, supplements 2 AMUR-SIKHOTE-ALIN ECOREGION, HIGH CONSERVATION VALUE FORESTS, MODEL TERRITORIES, RESERVES, FOREST FIRE MANAGEMNT, CONSERVATION, BIODIVERSITY Analysis and assessment of Project on Fire Management in High Conservation Value Forests of the Amur-Sikhote-Alin Ecoregion Goals: assessment of Project environmental impact and contribution to the implementation of the program on forest fire prevention, elimination and control in the Amur-Sikhote-Alin ecoregion. Present-day situation, trends and opportunities for developing a fire prevention, elimination and control system were in the focus of attention. Existing data and materials have been studied to reveal forest fire impact on environment as well as Project environmental impact. Project under consideration is aimed at improving current fire management system and strengthening protection of ecoregion forests from degradation, which make it extremely socially and ecologically valuable and important. 3 List of Specialists Senior researcher, C.Biol.Sc. A.L. Antonov (Chapter 3) Senior researcher, D.Biol. B.A. Voronov (Introduction, Chapters 2,5,6) Senior researcher, C.Agr.Sc. A.K. Danilin (Chapter 4) Senior researcher, C.Biol.Sc. -

Newell, J. 2004. the Russian Far East

Industrial pollution in the Komsomolsky, Solnechny, and Amursky regions, and in the city of Khabarovsk and its Table 3.1 suburbs, is excessive. Atmospheric pollution has been increas- Protected areas in Khabarovsk Krai ing for decades, with large quantities of methyl mercaptan in Amursk, formaldehyde, sulfur dioxide, phenols, lead, and Type and name Size (ha) Raion Established benzopyrene in Khabarovsk and Komsomolsk-on-Amur, and Zapovedniks dust prevalent in Solnechny, Urgal, Chegdomyn, Komso- molsk-on-Amur, and Khabarovsk. Dzhugdzhursky 860,000 Ayano-Maysky 1990 Between 1990 and 1999, industries in Komsomolsky and Bureinsky 359,000 Verkhne-Bureinsky 1987 Amursky Raions were the worst polluters of the Amur River. Botchinsky 267,400 Sovetsko-Gavansky 1994 High concentrations of heavy metals, copper (38–49 mpc), Bolonsky 103,600 Amursky, Nanaisky 1997 KHABAROVSK zinc (22 mpc), and chloroprene (2 mpc) were found. Indus- trial and agricultural facilities that treat 40 percent or less of Komsomolsky 61,200 Komsomolsky 1963 their wastewater (some treat none) create a water defi cit for Bolshekhekhtsirsky 44,900 Khabarovsky 1963 people and industry, despite the seeming abundance of water. The problem is exacerbated because of: Federal Zakazniks Ⅲ Pollution and low water levels in smaller rivers, particular- Badzhalsky 275,000 Solnechny 1973 ly near industrial centers (e.g., Solnechny and the Silinka River, where heavy metal levels exceed 130 mpc). Oldzhikhansky 159,700 Poliny Osipenko 1969 Ⅲ A loss of soil fertility. Tumninsky 143,100 Vaninsky 1967 Ⅲ Fires and logging, which impair the forests. Udylsky 100,400 Ulchsky 1988 Ⅲ Intensive development and quarrying of mineral resourc- Khekhtsirsky 56,000 Khabarovsky 1959 es, primarily construction materials. -

FTSE Publications

2 FTSE Russell Publications FTSE 100 Semi Annual Equally 19 August 2021 Weighted Net Tax Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.95 UNITED Fresnillo 0.86 UNITED Prudential 0.92 UNITED KINGDOM KINGDOM KINGDOM Admiral Group 1.06 UNITED GlaxoSmithKline 1.08 UNITED Reckitt Benckiser Group 1.02 UNITED KINGDOM KINGDOM KINGDOM Anglo American 0.91 UNITED Glencore 0.94 UNITED RELX 1.05 UNITED KINGDOM KINGDOM KINGDOM Antofagasta 0.91 UNITED Halma 1.05 UNITED Rentokil Initial 1.04 UNITED KINGDOM KINGDOM KINGDOM Ashtead Group 1.04 UNITED Hargreaves Lansdown 0.98 UNITED Rightmove 1.09 UNITED KINGDOM KINGDOM KINGDOM Associated British Foods 0.96 UNITED Hikma Pharmaceuticals 1.03 UNITED Rio Tinto 0.96 UNITED KINGDOM KINGDOM KINGDOM AstraZeneca 1.11 UNITED HSBC Hldgs 0.94 UNITED Rolls-Royce Holdings 0.9 UNITED KINGDOM KINGDOM KINGDOM Auto Trader Group 1.15 UNITED Imperial Brands 0.98 UNITED Royal Dutch Shell A 0.56 UNITED KINGDOM KINGDOM KINGDOM Avast 1.07 UNITED Informa 0.94 UNITED Royal Dutch Shell B 0.49 UNITED KINGDOM KINGDOM KINGDOM Aveva Group 1.08 UNITED InterContinental Hotels Group 0.97 UNITED Royal Mail 0.99 UNITED KINGDOM KINGDOM KINGDOM Aviva 1 UNITED Intermediate Capital Group 0.99 UNITED Sage Group 1.06 UNITED KINGDOM KINGDOM KINGDOM B&M European Value Retail 1.04 UNITED International Consolidated Airlines 0.85 UNITED Sainsbury (J) 1.03 UNITED KINGDOM Group KINGDOM KINGDOM BAE Systems 1 UNITED Intertek -

20 Years of Sustainable Development

20 YEARS OF SUSTAINABLE DEVELOPMENT Polymetal International plc Sustainability Report 2017 THE GROUP CEO’S STATEMENT OVERVIEW Action expresses priorities OVERVIEW HEALTH AND SAFETY Welcome to our Sustainability Report, which marks Polymetal’s 20th year of conducting business responsibly: Welcome to our At a glance 06 Safety risks management 48 two decades in which we have achieved tremendous Where we operate 08 Safety performance 50 success. We currently employ around 12,000 people at eight Sustainability Business model 10 operations covering three countries and seven time zones. Our approach 12 COMMUNITIES Of our employees, 20% are under 30, and more than 500 come from families who have worked at Polymetal for years. Report 2017 How we manage sustainability 14 Community engagement 55 Materiality 17 Social investment 56 Altogether we have produced almost 16.6 Moz of gold, and over 350 Moz of silver. We have discovered 20 mineral ENVIRONMENT Stakeholder engagement 18 Impact assessment 58 deposits, performed 2,200 km of exploration drilling, and Sustainable development goals 20 developed over 550 km underground. Our current licensed Our performance 21 ECONOMIC area is the size of 1,000,000 football pitches. We were the first company in the former Soviet Union to use pressure Financial assistance 63 ENVIRONMENT oxidation technology (POX) for extracting gold from refractory Local employment 63 concentrates, and the first in post-Soviet states to establish Water 26 Supply chain 63 When our environment and society an in-house engineering and design centre. Waste 27 R&D 64 ABOUT THIS REPORT flourish, our business can flourish. Our achievements spread beyond Polymetal to the benefit Polymetal International’s Sustainability Report 2017 covers Energy and carbon 29 Markets served 64 of the wider community. -

Subject of the Russian Federation)

How to use the Atlas The Atlas has two map sections The Main Section shows the location of Russia’s intact forest landscapes. The Thematic Section shows their tree species composition in two different ways. The legend is placed at the beginning of each set of maps. If you are looking for an area near a town or village Go to the Index on page 153 and find the alphabetical list of settlements by English name. The Cyrillic name is also given along with the map page number and coordinates (latitude and longitude) where it can be found. Capitals of regions and districts (raiony) are listed along with many other settlements, but only in the vicinity of intact forest landscapes. The reader should not expect to see a city like Moscow listed. Villages that are insufficiently known or very small are not listed and appear on the map only as nameless dots. If you are looking for an administrative region Go to the Index on page 185 and find the list of administrative regions. The numbers refer to the map on the inside back cover. Having found the region on this map, the reader will know which index map to use to search further. If you are looking for the big picture Go to the overview map on page 35. This map shows all of Russia’s Intact Forest Landscapes, along with the borders and Roman numerals of the five index maps. If you are looking for a certain part of Russia Find the appropriate index map. These show the borders of the detailed maps for different parts of the country. -

Specifics of Cultural Space of the Khabarovsk Territory

Journal of Siberian Federal University. Humanities & Social Sciences 2021 14(6): 918–926 DOI: 10.17516/1997–1370–0770 УДК 008: 304.2+379.81 Specifics of Cultural Space of the Khabarovsk Territory Lidiya V. Sheremet’eva* Khabarovsk State Institute of Culture Khabarovsk, Russian Federation Received 26.03.2021, received in revised form 16.04.2021, accepted 21.05.2021 Abstract. The paper focuses on various activities of cultural institutions operating in the territory of the region. The methodological basis of the research is L. V. Nikiforova’s cultural expertise based on systematisation of the categories of «places» of cultural space. The paper is a preparatory stage of cultural expertise, which aims to thoroughly analyse the network of cultural institutions in general and to identify potential art- spaces for further detailed study. It provides a detailed analysis of the network of cultural institutions in Khabarovsk and an overview of the categories of cultural institutions in the administrative centers of all districts in the Khabarovsk territory. The source base of the study is the data obtained from the analysis of websites of cultural institutions, social networks, as well as the respondents’ personal surveys. Cultural institutions representing different forms of cultural activity have been roughly divided into ten groups. The result of the research is a perspective to identify institutions the activities of which can be evaluated in terms of belonging to the art-space format. Keywords: culture, society, region, cultural space, art-space, Khabarovsk, Khabarovsk Territory, research activities, cultural expertise, cultural institutions. Research area: 24.00.00 – сulturology. Citation: Sheremet’eva, L.V.