Abstract David Ricardo's Macroeconomics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Anwar Shaikh and Isabella Weber the U.S.-China Trade Balance and The

Anwar Shaikh and Isabella Weber The U.S.-China Trade Balance and the Theory of Free Trade: Debunking the Currency Manipulation Argument May 2018; revised December 2019 Working Paper 05/2018 Department of Economics The New School for Social Research The views expressed herein are those of the author(s) and do not necessarily reflect the views of the New School for Social Research. © 2018 by Anwar Shaikh and Isabella Weber. All rights reserved. Short sections of text may be quoted without explicit permission provided that full credit is given to the source. Anwar Shaikh The New School for Social Research Department of Economics Isabella Weber* University of Massachusetts Amherst Department of Economics The U.S.-China Trade Imbalance and the Theory of Free Trade: Debunking the Currency Manipulation Argument Abstract The U.S.-China trade imbalance is commonly attributed to a Chinese policy of currency manipulation. However, empirical studies failed to reach consensus on the degree and kind of RMB misalignment. We argue that this is not a consequence of poor measurement but of theory. At the most abstract level the conventional principle of comparative cost advantage suggests real exchange rates will adjust so as to balance trade. Therefore, the persistence of trade imbalances tends to be interpreted as arising from currency manipulation facilitated by foreign exchange interventions. By way of contrast, the absolute cost theory provided by Smith and Harrod theory explains trade imbalances as the outcome of free trade among nations that have unequal real costs. We argue that a disparity in real costs is the root cause of the U.S.-China trade imbalance. -

Descendants of John Pelly

Descendants of John Pelly Charles E. G. Pease Pennyghael Isle of Mull Descendants of John Pelly 1-John Pelly was born on 9 Jun 1711 and died on 22 Nov 1762 at age 51. John married Elizabeth Hinde, daughter of Henry Hinde. Elizabeth was born in 1717 and died on 6 Nov 1761 at age 44. They had two children: Henry Hinde and John. 2-Capt. Henry Hinde Pelly was born on 6 Jun 1744 in West Ham, London and died on 23 Feb 1818 at age 73. Henry married Sally Hitchen Blake,1 daughter of Capt. John Blake, on 13 Jul 1776. Sally was born in 1744 and died on 15 May 1824 at age 80. They had four children: John Henry, William, Charles, and Francis. 3-Sir John Henry Pelly 1st Bt. was born on 31 Mar 1777 in West Ham, London and died on 13 Aug 1852 in Upton Manor, Plaistow, Essex at age 75. General Notes: Sir John Henry Pelly, 1st Bt. was a Younger Brother of Trinity House in 1803. He was Deputy Governor of the Hudson Bay Company between 1812 and 1822. He was Captain of the Honourable East India Company Service. He was a Member of Court Bank of England between 1822 and 1852. He was Governor of the Hudson Bay Company between 1822 and 1852. He held the office of Elder Brother of Trinity House in 1823. He was Deputy Master of Trinity Master in 1834. He was created 1st Baronet Pelly, of Upton, Essex [U.K.] on 12 August 1840. Noted events in his life were: • He worked as a Director of the Bank of England in Threadneedle Street, London. -

Part 1. During Inflation: Preferences, Investment, Risk*

Part 1. During Inflation: Preferences, Investment, Risk* Leonid A. Shapiro Abstract. Producers cannot avoid being misled in their decisions even when they know inflation is taking place; effects of inflation are neither proportional to its extent nor to its magnitude — they resemble an infinite sum of disorienting impulses from perspective of entrepreneurs — and so slight inflation can, too, like greater inflation, force relations of market prices and profits to deviate significantly from such relations which would exist if intervention was indeed absent. This causes manufacture of products contrary to actual preferences of consumers and, too, real availability of capital goods. Harmful effects of intervention are themselves not linear and so minimizing it without eliminating it does not guarantee that harm arising from this intervention is minimal and thus analysis suggests that during every burst of inflation — slight or great — possibility of significant decrease of welfare cannot itself be rejected a priori. §1 Introduction Is increase of roundaboutness of production or lengthening of investment chains — and corresponding necessary decrease of quantity of first-order goods produced or manufacture of different first-order goods — proportional to increase of quantity of money or its substitutes, and supply of loanable funds, by way of credit expansion or coercive intervention, namely, inflation? Following Cantillon (1755), Craig (1821), Say (1821), Gossen (1854), Menger (1871; 1888), Hayek (1931; 1932), Hulsmann (1998), Hutt (1939; 1956), Mises (1912; 1949), Rothbard (1962a; 1962b), Garrison (2001): 1. Producers cannot avoid involvement in business cycles when inflation occurs. This remains true when they know that inflation is taking place and what it causes. -

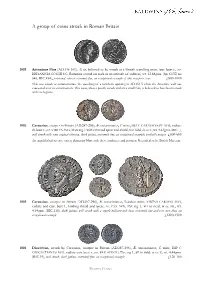

A Group of Coins Struck in Roman Britain

A group of coins struck in Roman Britain 1001 Antoninus Pius (AD.138-161), Æ as, believed to be struck at a British travelling mint, laur. bust r., rev. BRITANNIA COS III S C, Britannia seated on rock in an attitude of sadness, wt. 12.68gms. (Sp. COE no 646; RIC.934), patinated, almost extremely fine, an exceptional example of this very poor issue £800-1000 This was struck to commemorate the quashing of a northern uprising in AD.154-5 when the Antonine wall was evacuated after its construction. This issue, always poorly struck and on a small flan, is believed to have been struck with the legions. 1002 Carausius, usurper in Britain (AD.287-296), Æ antoninianus, C mint, IMP C CARAVSIVS PF AVG, radiate dr. bust r., rev. VIRTVS AVG, Mars stg. l. with reversed spear and shield, S in field,in ex. C, wt. 4.63gms. (RIC.-), well struck with some original silvering, dark patina, extremely fine, an exceptional example, probably unique £600-800 An unpublished reverse variety depicting Mars with these attributes and position. Recorded at the British Museum. 1003 Carausius, usurper in Britain (AD.287-296), Æ antoninianus, London mint, VIRTVS CARAVSI AVG, radiate and cuir. bust l., holding shield and spear, rev. PAX AVG, Pax stg. l., FO in field, in ex. ML, wt. 4.14gms. (RIC.116), dark patina, well struck with a superb military-style bust, extremely fine and very rare thus, an exceptional example £1200-1500 1004 Diocletian, struck by Carausius, usurper in Britain (AD.287-296), Æ antoninianus, C mint, IMP C DIOCLETIANVS AVG, radiate cuir. -

The Unsolved Problem of Economic Crisis As a Turning Point of Marxs

The Unsolved Problem of Economic Crisis as a Turning Point of Marx’s Critique of Political Economy, 1844-45 Timm Graßmann Abstract: With the continuing publication of the complete works of Karl Marx and Friedrich Engels (Marx-Engels-Gesamtausgabe, MEGA), a bulk of new material concerning Marx’s studies of economic crises has been made available-with further releases expected to follow. These publications have revealed Marx’s enormous efforts to examine in detail every economic cri- sis through which he lived. The most prominent examples are the three Books of Crisis( Kris- enhefte), which he compiled in 1857-58 amidst the first truly global economic crisis. This paper sets out to, first, provide an overview of new MEGA-texts regarding Marx’s studies of contemporaneous 19th century revulsions. In the main part, a closer look will be taken at the origin of Marx’s crisis studies in the 1840s. A comparison between his notes on James Mill’s Elements of Political Economy, written in the Paris Notebooks( 1844), and his excerpts from John Stuart Mill’s Essays on Some Unsettled Questions of Political Economy, taken in his Manchester Notebooks( 1845), reveals Marx’s changing stance on classical political econo- my’s ‘general glut controversy,’ i.e., the debate over the( im)possibility of overproduction cri- ses in commodity-producing societies. In between his stays in Paris and Manchester, Marx took extensive notes on the works of Simonde de Sismondi in his Brussels Notebooks (1845), which played a major role in his break from anthropological-essentialist thinking. JEL classification numbers: B 00, B 51, E 32. -

The Bank of England and the Bank Act of 1844 Laurent Le Maux

Central banking and finance: the Bank of England and the Bank Act of 1844 Laurent Le Maux To cite this version: Laurent Le Maux. Central banking and finance: the Bank of England and the Bank Act of1844. Revue Economique, Presses de Sciences Po, 2018. hal-02854521 HAL Id: hal-02854521 https://hal.archives-ouvertes.fr/hal-02854521 Submitted on 8 Jun 2020 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Central banking and finance: the Bank of England and the Bank Act of 1844 Laurent LE MAUX* May 2020 The literature on the Bank of England Charter Act of 1844 commonly adopts the interpretation that it was a crucial step in the construction of central banking in Great Britain and the analytical framework that contrasts rules and discretion. Through examination of the monetary writings of the period and the Bank of England’s interest rate policy, and also through the systematic analysis of the financial aspect of the 1844 Act, the paper shows that such an interpretation remains fragile. Hence the present paper rests on the articulation between monetary history and the history of economic analysis and also on the institutional approach to money and banking so as to assess the consequences of the 1844 Act for the liquidity market and the relations between the central bank and finance. -

Ancient, Islamic, British and World Coins Historical Medals and Banknotes

Ancient, Islamic, British and World Coins Historical Medals and Banknotes To be sold by auction at: Sotheby’s, in the Upper Grosvenor Gallery The Aeolian Hall, Bloomfield Place New Bond Street London W1 Day of Sale: Thursday 29 November 2007 10.00 am and 2.00 pm Public viewing: 45 Maddox Street, London W1S 2PE Friday 23 November 10.00 am to 4.30 pm Monday 26 November 10.00 am to 4.30 pm Tuesday 27 November 10.00 am to 4.30 pm Wednesday 28 November See below Or by previous appointment. Please note that viewing arrangements on Wednesday 28 November will be by appointment only, owing to restricted facilities. For convenience and comfort we strongly recommend that clients wishing to view multiple or bulky lots should plan to do so before 28 November. Catalogue no. 30 Price £10 Enquiries: James Morton, Tom Eden, Paul Wood or Stephen Lloyd Cover illustrations: Lot 172 (front); ex Lot 412 (back); Lot 745 (detail, inside front and back covers) in association with 45 Maddox Street, London W1S 2PE Tel.: +44 (0)20 7493 5344 Fax: +44 (0)20 7495 6325 Email: [email protected] Website: www.mortonandeden.com This auction is conducted by Morton & Eden Ltd. in accordance with our Conditions of Business printed at the back of this catalogue. All questions and comments relating to the operation of this sale or to its content should be addressed to Morton & Eden Ltd. and not to Sotheby’s. Important Information for Buyers All lots are offered subject to Morton & Eden Ltd.’s Conditions of Business and to reserves. -

British Financial Experience, 1790-1830 283

BRITISH FINANCIAL EXPERIENCE 1790-1830 NORMAN J. SILBERLING HE monetary and financial events which attended brought down to 1837 in the History of Prices,1 with the Tthe military operations carried on by Great Britain assistance of Mr. M. L. Merac, who likewise derived and her continental allies against the armies of France, practically all of his figures from the Price Current. The between 1793 and 1815, have acquired at this time a table of prices as given in this volume includes the high special interest. The wars of the Napoleonic era pre- and low quotations at four periods within each year: sent, in their political and economic aspects, numerous (1) about the middle of January, (2) the last days of points of similarity to, as well as interesting points of March and first days of April, (3) about the middle of contrast with, the great war of the past five years. An July, and (4) about the middle of November. There examination of some of the financial experiences of are many gaps in the data, especially in the quotations England during and immediately following this earlier for the first and last periods during the earlier years. period may be useful, not only in setting forth historical This series was continued in the subsequent volumes of parallels and contrasts, but in furnishing valuable the History of Prices. In the early sixties, Professor lessons for our own time. Jevons conceived the plan of casting these materials It is proposed to consider in this paper, certain as- into the form of an index number, in order that the pects of the financial history of England for a period general trend of prices might be ascertained. -

Caribbeana : Being Miscellaneous Papers Relating to the History, Genealogy, Topography, and Antiquities of the British West Indi

WBHHBJMi H llllliii USUI mm Hi mm mm I §§§ H ^^mmMB 97 172 REYNOLDS HISTORICAL GENEALOGY COLLECTION ALLEN COUNTY PUBLIC LIBRARY 3 1833 01072 5171 Digitized by the Internet Archive in 2012 http://archive.org/details/caribbeanabeingmv6oliv CARIBBEANA Miscellaneous papers relating to the history , genealogy, topography, and antiquities of the British West Indies Edited by Vere Langford Oliver /. E QABIBBEAgA; "being miscellaneous papers relating 67 to the history, genealogy, topography., and ,16 antiquities of the British West Indies— v u l- 6; Jan. 1909-Oct. 1919. London, Mitchell, Hughes and Clarkec 1909-1 9u , 6v„ illus. plates, ports 27cq (. quarterly. \ , Edited by Vere Langford Oliver. "The registers of St. Thomas Middle Island, St. Kitts. edited "by Vere Langford Oliver. n London, l?15 issuedCas suppl. to voloIV. feMf I C nor IC1T 5O-562 ( *t ) Clajttom Eobert Claxton of Bristol, merchant. Will dated 22 Jan. 1812. To my wife Eachael my lionse and furniture in Park Str. and £1000 a year. To my son Butler Thompson C. the portraits of my late mother and of her 2 a husband Dr. Geo. Thompson. My houses in Basseterre S l Kitts to be sold. To my sons Chi\, Kob., Wm. and Philip Prothero at 21 £3000 each. To my dans. Eliz. ami Margt. £4000 each. (Short abstract.) P. 6 Feb. 1818. ((53, Heathfiold.) 1707-8. Census of St. Kitts. Parish of Trinity, Palmetto Point :—Frans Claxton, ago 32 — 1 man, 3 women, 2 boys, 26 slaves. (Ante, III., 139.) 1716, May 22. Depositions taken at the house at Basseterre, St. Kitts, of Mr. -

February 75 Vol. TY 1 ISSN 0305 - 8247

Bulletin of the Conference of • Socialist • Economists February 75 Vol. TY 1 ISSN 0305 - 8247 For contents see back cover A Itoh 1 THE FORMATION OF MARX'S THEORY OF CRISIS Makoto Itoh I TWO TYPES OF CRISIS THEORY Marx's theory of crisis in "Capital" forms a focus of his systematic critique of Classical economics in which capitalist economy is regarded as the ultimate natural order of human society. Unlike the Classical school, Marx's theory treats the law of motion of capitalistic production scientifically with its historical forms and mechanisms. Without such a systematic theory, we cannot clarify the logical necessity of cyclical crises which reveal the contradictory nature of capitalist economy in all its complex interrelations. In dealing with such complex phenomena, the level and the empirical basis of abstraction is particularly important. The crisis theory in "Capital" was dev- eloped in order to prove the inevitability of cyclical crises at the level of basic principle. And it was formed on the empirical basis of the most typical cyclical crises at the middle of the 19th century, the most suitable historical basis of abstracting the principle of crisis.. If we take as the basis of abstraction the whole history of crises, including the immature crises in the mercantilistic age, we will only recognize either too diverse concrete factors (often not exclusively economic factors, such as wars) affecting the courses and phases of crises, or too abstract formal common factors, in order to prove not the mere possibility but the logical necessity of cyclical crises. Professor Uno's systematic division of levels of research in Marxian Economics into Principle, Stages Theory, and Analysis is essential here. -

British Coins

______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________ ______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________ BRITISH COINS 567 Eadgar (959-975), cut Halfpenny, from small cross Penny of moneyer Heriger, 0.68g (S 1129), slight crack, toned, very fine; Aethelred II (978-1016), Penny, last small cross type, Bath mint, Aegelric, 1.15g (N 777; S 1154), large fragment missing at mint reading, good fine. (2) £200-300 with old collector’s tickets of pre-war vintage 568 Aethelred II (978-1016), Pennies (2), Bath mint, long -

No More Credit Excesses

naslovnica 11/14_naslovnica 11-2013 23/10/14 11:13 Page 1 THE JOURNAL FOR MONEY AND BANKING LJUBLJANA, VOLUME 63, No. 11, NOVEMBER 2014 SPECIAL ISSUE Bančni LEARNING FROM HISTORY – NO MORE vestnik CREDIT EXCESSES VSEBINA/CONTENT EDITORIAL Boštjan Jazbec: Banking sector recapitalisation, corporate sector leverage and ways out in Slovenia 1 ECONOMIC ACTIVITY, BUSINESS CYCLES AND CREDIT GROWTH Bernhard Winkler: Flow-of-funds perspective on unconventional monetary policy 2 Daria Zakharova and co-authors: Reviving credit growth for strong and sustainable recovery 11 Marko Simoneti: Quantitative easing and non-bank debt financing in Slovenia 22 REHABILITATION OF BANKS AND COMPANIES IN CREDIT STAGNATION CONDITIONS Robert Priester: Structural changes in European banking and influence on banking business models 31 Tina Žumer: Sectoral indebtedness and balance sheet repair in euro area 35 Marko Košak: In search for sustainable funding structure of commercial banks 43 Ivan Ribnikar: Banks’ capital and their funding 52 Timotej Jagrič and Rasto Ovin: Positioning Slovenian banking sector in EU 59 Božo Jašovič and Matej Tomec: Financial instability, government intervention and credit growth 64 Bojan Ivanc: Concept of business restructuring and sustainable funding of Slovenian companies 74 BEST PRACTICE CASES Carmelina Carluzzo and Milen Kassabov: CEE banking: Switching to sustainable track 78 Gvido Jemenšek: Potential for restructuring and new business models for banks 83 Janko Medja and co-authors: Transforming NLB, Slovenian market leader 91 Lars Nyberg: Bank Assets Management Company – Experiences so far 101 CONCLUDING REMARKS Emil Lah: Monetary policy paradoxes and banking crisis 113 STATISTICAL APPENDIX 120 kolofon 2014_Layout 1 23/10/14 11:38 Page 1 Uredniški odbor: mag.