HOLBA-Insights-Report-Jun-20.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Trades' Directory. 811

1841.] TRADES' DIRECTORY. 811 SILK &VEL YET MANFRS.-continued. l\Iay William, 132 Bishops~ate without DentJ.30,31,32 Crawfordst.Portmansq Brandon William, 23 Spital square *Nalders, Spall & Co. 41 Cheapside Devy M. 73 Lower Grosvenor street, & Bridges & Camp bell, 19 Friday street N eill & Langlands, 45 Friday street 120 George street, Edinburgh Bridgett Joseph & Co.63 Alderman bury Perry T. W. & Co. 20 Steward st. Spitalfi *Donnon Wm.3.5Garden row, London rd British, IJ-ish, ~· Colonial Silk Go. 10~ Place & Wood, 10 Cateaton street Duthoit & Harris, 77 Bishopsgate within King's arms yard Powell John & Daniel, 1 Milk !'treet t Edgington \Yilliam, 37 Piccadilly Brocklehurst Jno. & Th. 32 & 331\-Iilk st t Price T. Divett, 19 Wilson st. Finsbury Elliot Miss Margt. Anne, 43 Pall mall Brooks Nathaniel, 25 Spital square Ratliffs & Co. 78\Vood st. Cheapside E~·les,Evans,Hands&.Wells,5Ludgatest Brown .Archbd. & Co.ltl Friday st.Chpsi Rawlinson Geo. & Co. 34 King st. City *Garnham Wm. Henry, 30 Red Lion sq *Brown James U. & Co. 3,5 Wood street Reid John & Co. 21 Spital square George & Lambert, 192 Regent street *Brunskill Chas.& Wm.5 Paternostr.rw Relph & Witham, 6 Mitre court, Milk st Green Saml. 7 Lit. Aygyll st.llegent st Brunt Josiah, & Co.12 Milk st. Cheapsi Remington, Mills & Co. 30 Milk street Griffiths & Crick, 1 Chandos street Bullock Wm. & Co. 11 Paternoster row tRobinsonJas.&Wm.3&4Milkst.Chepsid +Hall Hichanl, 29 St. John street Buttre~s J. J. & Son, 36Stewardst.Spital RobinsonJ. & T. 21 to 23 Fort st. Spitalfi *Hamer & Jones, 59 Blackfriars road Buttress John, 15 Spital square Salter J. -

HOLBA-Insights-Report-Jul-20.Pdf

HEART OF LONDON JULY AREA PERFORMANCE HEART OF LONDON AREA PERFORMANCE CONTENTS JULY 2020 EDITION INTRODUCTION 02 Welcome to our area performance report. This monthly summary provides trends in footfall, spending SUMMARY ANALYSIS 03 and much more, in the Heart of London area. Focusing on Leicester Square, Piccadilly Circus, Haymarket, Piccadilly and FOOTFALL TRENDS 04 St James’s, find out exactly how our area has performed FOOTFALL OVERVIEW 05 throughout the month. HOURLY FOOTFALL 06 The report is available exclusively to members, and explores REGIONAL FOOTFALL 07 changes in trends that impact the performance of our area, allowing your business to plan with confidence and make the COVID-19 AND FOOTFALL 08 most of being in the heart of London. YOUR FEEDBACK IS IMPORTANT TO US PROPERTY & INVESTMENT 09 PLEASE CLICK ON THE BUTTON INVESTMENT 10 TO REQUEST NEW DATA OR ANALYSIS PROPERTY PERFORMANCE 11 LEASE AVAILABILITY 12 EVENTS & ACTIVITY 13 IMPACT CALENDAR 14 GLOSSARY 15 See our Glossary for more detail on data sources and definitions. 2 HEART OF LONDON AREA PERFORMANCE SUMMARY ANALYSIS – JULY 2020 Rainfall (mm) 2020 2019 500K 25 YEAR ON YEAR FOOTFALL 450K -72% Footfall in the current month compared to the same month last year 400K 20 350K 300K 15 MONTH ON MONTH FOOTFALL 250K +97% Footfall in the current month compared Footfall 200K 10 to the previous month Rainfall (mm) Rainfall 150K 100K 5 YEAR TO DATE FOOTFALL 50K -58% Footfall in the current year to date K 0 compared to the same period last year M T W T F S S M T W T F S S M T W T F S S M T W T F S S 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 1 2 Week 28 Week 29 Week 30 Week 31 July trend summary • Like-for-like footfall in the Heart of London area was down 72% in July 2020 compared to the same month last year. -

Timeline: 2-14 Baker Street Date Event Notes

Timeline: 2-14 Baker Street Parties: British Land, McAleer & Rushe. Bank of Ireland, NAMA, Portman Estate Topic: 2-14 Baker Street - in London which was subject to a loan from Bank of Ireland Timeline: Date Event Notes August Several media articles report on This was the second reported purchase by and agreement between British Land and McAleer & Rushe from British Land – the September McAleer & Rushe for the sale (by BL) previous deal was for the Swiss Centre in 2005 of 2-14 Baker Street. Leicester Square. Guide price for the 2-14 Baker Street property was UK£47.5m with British Land offering it as a potential 150,000 sq. ft development opportunity. 5th 2-14 Baker Street purchased by Travers Smith acted for McAleer & Rushe October McAleer & Rushe by British Land for Group on the acquisition. 2005 UK£57.2m. The existing building tenants: Purchase funded with a Bank of Offices let on a lease expiring in December Ireland loan. 2009. Retail accommodation let under four separate leases all expiring by December 2009 The property comprised 94,000 sq. ft. held on a 98 year headlease from the Portman Estate. 16th Planning Application submitted to Planning application filed by Gerald Eve, December Westminster City Council listing Chartered Surveyors and Property Consultants 2008 Owners pf 2-14 Baker Street as: Contact person: James Owens 1. Portman Estate (freeholder) [email protected] 2. Mourant & Co Trustees Ltd and Mourant Property Trustees Ltd Baker Street Unit Trust is owned by McAleer & as Trustees of the Baker Street Rushe with a Jersey address. -

COMMERCIAL DIRECTORY. Albrecht Henry Jas. & Co. East India

292 COMMERCIAL DIRECTORY. [1841. Albrecht Henry Jas. & Co. east india merchts. 14 Eastcheap Alexander Wm. Southwm·k Arms P.H. 151 Tooley street AlbrecLt John, colonial broker, 48 Fenchurch street Alexander Wm. John, barrister, 3 King's bench walk,Templtt Albri~ht Eliz. (1\Ira.),stationer, 36 Bridge ho. pl. N ewing.cau Alexanure Auguste, for. booksel. 37 Gt. Russell st. Bloomsb Alcock Anthony,glass & chinaman, 6 Charles st. Westminster Alexandre Edme, artificial florist, 20 King's rd. Bedford row Alcock Edward, grocer, 361 Rotherhithe Aley James, Fathe1· Red Cap P.H. Camberwell green Alcock John, rag merchant, 12 Addle hill, Doctors' Commons Aley Thomas, watchmaker, 18 Park side, Knight~bridge Alcock Wm. printers' joiner, 2! White Lion st. N orton folgate Aley William, poulterer, 2 Queen's buildings, Knights bridge Alcock Rutherford, physician, 13 Park place, St. James's Altord Charles, lighterman, 12 Bennett's hill, Due. corn. Alder Edward, coffee rooms, 208 Sloane st. Knightsbridge Alford, Fitzherbert & Co. cloth factors, 10 Ironmonger lane Alder John, Golden Horse P. H. Glasshouse yd. Aldersgt. st AI ford J ames, cooper& oil bag ma. 8 Bennett's hill, Doe. corn. Alderman Wm.Hen.Lm·dNelsonP.H.ll!Bishopsgt.without Alford Jenkins, Colonel lVardle P.H. 138 Tooley street Alders Jas. engraver & chaser, 3 Thorney st. Bloomsbury sq Alford Robert,engraver, & copperplate, letterpress & gold Aldersey Joseph Stephens, attomey, 8 Gower st. Bedford sq printer, 13 Bridge street, Southwark Aldersey Richard Baker, who. stationer, 11 Cloaklane1 City Altord Thomas,coachmaker,Cumber land st. N ewingtonbutts Alderson Geo. D. & Co. lead mercs. 2 Blenl1eim st. -

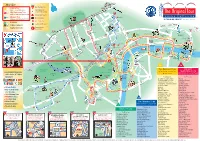

A4 Web Map 26-1-12:Layout 1

King’s Cross Start St Pancras MAP KEY Eurostar Main Starting Point Euston Original Tour 1 St Pancras T1 English commentary/live guides Interchange Point City Sightseeing Tour (colour denotes route) Start T2 W o Language commentaries plus Kids Club REGENT’S PARK Euston Rd b 3 u Underground Station r n P Madame Tussauds l Museum Tour Russell Sq TM T4 Main Line Station Gower St Language commentaries plus Kids Club q l S “A TOUR DE FORCE!” The Times, London To t el ★ River Cruise Piers ss Gt Portland St tenham Ct Rd Ru Baker St T3 Loop Line Gt Portland St B S s e o Liverpool St Location of Attraction Marylebone Rd P re M d u ark C o fo t Telecom n r h Stansted Station Connector t d a T5 Portla a m Museum Tower g P Express u l p of London e to S Aldgate East Original London t n e nd Pl t Capital Connector R London Wall ga T6 t o Holborn s Visitor Centre S w p i o Aldgate Marylebone High St British h Ho t l is und S Museum el Bank of sdi igh s B tch H Gloucester Pl s England te Baker St u ga Marylebone Broadcasting House R St Holborn ld d t ford A R a Ox e re New K n i Royal Courts St Paul’s Cathedral n o G g of Justice b Mansion House Swiss RE Tower s e w l Tottenham (The Gherkin) y a Court Rd M r y a Lud gat i St St e H n M d t ill r e o xfo Fle Fenchurch St Monument r ld O i C e O C an n s Jam h on St Tower Hill t h Blackfriars S a r d es St i e Oxford Circus n Aldwyc Temple l a s Edgware Rd Tower Hil g r n Reg Paddington P d ve s St The Monument me G A ha per T y Covent Garden Start x St ent Up r e d t r Hamleys u C en s fo N km Norfolk -

Aldwych-House-Brochure.Pdf

Executive summary • An iconic flagship in the heart of Midtown • This imposing building invested with period grandeur, has been brought to life in an exciting and modern manner • A powerful and dramatic entrance hall with 9 storey atrium creates a backdrop to this efficient and modern office • A total of 142,696 sq ft of new lettings have taken place leaving just 31,164 sq ft available • A space to dwell… 4,209 – 31,164 SQ FT 4 | ALDWYCHHOUSE.COM ALDWYCHHOUSE.COM | 5 Aldwych House • MoreySmith designed reception • Full height (9 storey) central atrium fusing a modern which provides a light, modern, interior with imposing spacious circulation area 1920s architecture • Floors are served by a newly refurbished lightwell on the west side and a dramatically lit internal Aldwych House totals 174,000 atrium to the east from lower sq ft over lower ground to 8th ground to 3rd floor floors with a 65m frontage • An extensive timber roof terrace onto historic Aldwych around a glazed roof area • Showers, cycle storage and a drying room are located in the basement with easy access from the rear of the building • The ROKA restaurant is on the ground floor 6 | ALDWYCHHOUSE.COM ALDWYCHHOUSE.COM | 7 8 | ALDWYCHHOUSE.COM Floorplate Typical upper floor c. 18,000 sq ft Typical upper floor CGI with sample fit-out 10 | ALDWYCHHOUSE.COM ALDWYCHHOUSE.COM | 11 Floorplate Typical upper floor with suite fit-out 12 | ALDWYCHHOUSE.COM ALDWYCHHOUSE.COM | 13 SOHO TOTTENHAM COURT ROAD MIDTOWN | LONDON Aldwych House, now transformed as part of the dynamic re-generation of this vibrant eclectic midtown destination, stands tall and COVENT GARDEN commanding on the north of the double crescent of Aldwych. -

The Heart of the Empire

The heart of the Empire A self-guided walk along the Strand ww.discoverin w gbrita in.o the stories of our rg lands discovered th cape rough w s alks 2 Contents Introduction 4 Route map 5 Practical information 6 Commentary 8 Credits 30 © The Royal Geographical Society with the Institute of British Geographers, London, 2015 Discovering Britain is a project of the Royal Geographical Society (with IBG) The digital and print maps used for Discovering Britain are licensed to the RGS-IBG from Ordnance Survey Cover image: Detail of South Africa House © Mike jackson RGS-IBG Discovering Britain 3 The heart of the Empire Discover London’s Strand and its imperial connections At its height, Britain’s Empire covered one-quarter of the Earth’s land area and one-third of the world’s population. It was the largest Empire in history. If the Empire’s beating heart was London, then The Strand was one of its major arteries. This mile- long street beside the River Thames was home to some of the Empire’s administrative, legal and commercial functions. The days of Empire are long gone but its legacy remains in the landscape. A walk down this modern London street is a fascinating journey through Britain’s imperial history. This walk was created in 2012 by Mike Jackson and Gary Gray, both Fellows of the Royal Geographical Society (with IBG). It was originally part of a series that explored how our towns and cities have been shaped for many centuries by some of the 206 participating nations in the 2012 Olympic and Paralympic Games. -

London 252 High Holborn

rosewood london 252 high holborn. london. wc1v 7en. united kingdom t +44 2o7 781 8888 rosewoodhotels.com/london london map concierge tips sir john soane’s museum 13 Lincoln's Inn Fields WC2A 3BP Walk: 4min One of London’s most historic museums, featuring a quirky range of antiques and works of art, all collected by the renowned architect Sir John Soane. the old curiosity shop 13-14 Portsmouth Street WC2A 2ES Walk: 2min London’s oldest shop, built in the sixteenth century, inspired Charles Dickens’ novel The Old Curiosity Shop. lamb’s conduit street WC1N 3NG Walk: 7min Avoid the crowds and head out to Lamb’s Conduit Street - a quaint thoroughfare that's fast becoming renowned for its array of eclectic boutiques. hatton garden EC1N Walk: 9min London’s most famous quarter for jewellery and the diamond trade since Medieval times - nearly 300 of the businesses in Hatton Garden are in the jewellery industry and over 55 shops represent the largest cluster of jewellery retailers in the UK. dairy art centre 7a Wakefield Street WC1N 1PG Walk: 12min A private initiative founded by art collectors Frank Cohen and Nicolai Frahm, the centre’s focus is drawing together exhibitions based on the collections of the founders as well as inviting guest curators to create unique pop-up shows. Redhill St 1 Brick Lane 16 National Gallery Augustus St Goswell Rd Walk: 45min Drive: 11min Tube: 20min Walk: 20min Drive: 6min Tube: 11min Harringtonn St New N Rd Pentonville Rd Wharf Rd Crondall St Provost St Cre Murray Grove mer St Stanhope St Amwell St 2 Buckingham -

A History of the French in London Liberty, Equality, Opportunity

A history of the French in London liberty, equality, opportunity Edited by Debra Kelly and Martyn Cornick A history of the French in London liberty, equality, opportunity A history of the French in London liberty, equality, opportunity Edited by Debra Kelly and Martyn Cornick LONDON INSTITUTE OF HISTORICAL RESEARCH Published by UNIVERSITY OF LONDON SCHOOL OF ADVANCED STUDY INSTITUTE OF HISTORICAL RESEARCH Senate House, Malet Street, London WC1E 7HU First published in print in 2013. This book is published under a Creative Commons Attribution- NonCommercial-NoDerivatives 4.0 International (CC BY- NCND 4.0) license. More information regarding CC licenses is available at https://creativecommons.org/licenses/ Available to download free at http://www.humanities-digital-library.org ISBN 978 1 909646 48 3 (PDF edition) ISBN 978 1 905165 86 5 (hardback edition) Contents List of contributors vii List of figures xv List of tables xxi List of maps xxiii Acknowledgements xxv Introduction The French in London: a study in time and space 1 Martyn Cornick 1. A special case? London’s French Protestants 13 Elizabeth Randall 2. Montagu House, Bloomsbury: a French household in London, 1673–1733 43 Paul Boucher and Tessa Murdoch 3. The novelty of the French émigrés in London in the 1790s 69 Kirsty Carpenter Note on French Catholics in London after 1789 91 4. Courts in exile: Bourbons, Bonapartes and Orléans in London, from George III to Edward VII 99 Philip Mansel 5. The French in London during the 1830s: multidimensional occupancy 129 Máire Cross 6. Introductory exposition: French republicans and communists in exile to 1848 155 Fabrice Bensimon 7. -

London in One Day Itinerary

Thursday's post for London Love was Part 1 of 2 of 'London in One Day' where I gave you a short list of essentials to make your day out run as smoothly and comfortably as possible, along with information to purchase your Tube and London Eye tickets . Now that we've got all that taken care off we're off on a busy day filled with many of London's best landmarks and attractions. *Please note that all times listed on here are approximate and will be based on things like how fast you walk, possible train delays, or unexpected crowds. I've done my best to estimate these based on my experiences in London to show you as much as possible in one day (albeit a fairly long, but definitely enjoyable, day). (9:00 a.m. - 10:00 a.m.) WESTMINSTER & WHITEHALL ©2014 One Trip at a Time |www.onetripatatime.com| Yep it's an early start but you've got places to go and things to see! You won't be sorry you got up bright and early especially when you exit Westminster Station and look up and there it is... Big Ben ! Unarguably London's best known landmark and where our tour begins. Take some selfies or have your travel companions take your photo with Big Ben and then save them for later when you have free WiFi (at lunch) to post on all your social network sites. Don't worry that lunch is a few hours off because with time zone differences people back home probably aren't awake to see them yet anyway. -

Aldwych Key Features

61 ALDWYCH KEY FEATURES 4 PROMINENT POSITION ON CORNER OF ALDWYCH AND KINGSWAY HOLBORN, STRAND AND COVENT GARDEN ARE ALL WITHIN 5 MINUTES’ WALK APPROXIMATELY 7,500 – 45,000 SQ FT OF FULLY REFURBISHED OFFICE ACCOMMODATION AVAILABLE 2,800 SQ FT ROOF TERRACE ON 9TH FLOOR DUAL ENTRANCES TO THE BUILDING OFF ALDWYCH AND KINGSWAY TEMPLE 61 ALDWYCH 14 KINGSWAY 6 HOLBORN COVENT GARDEN FARRINGDON 14 4 CHANCERY LANE N LOCAL AMENITIESSmitheld Market C NEWMAN’S ROW 15 HOLBORN H A 12 N C E OCCUPIERS R 13 FARRINGDON STREET 7 Y 1 British American Tobacco 9 Fladgates TOTTENHAM COURT ROAD L A 2 BUPA 10 PWC KINGSWAY N 3 11 Tate & Lyle D R U R Y L N E LSE 6 4 Mitsubishi 12 ACCA 11 5 Shell 13 Law Society E 9 N 6 Google 14 Reed D 7 Mishcon De Reya 15 WSP E E V L 8 Coutts 16 Covington and Burlington L A S 10 Y T LINCOLN’S INN FIELDS 13 R GREAT QUEEN ST U 3 C A R E Y S T RESTAURANTS B S Covent E 1 Roka 8 The Delauney T Garden F 2 The Savoy 9 Rules A CHARING CROSS RD Market 61 8 H 3 STK 10 Coopers S ALDWYCH 1 4 L’Ate l i e r 11 Fields Bar & Kitchen 11 5 The Ivy 12 Mirror Room and Holborn 16 N D 6 Dining Room 5 8 L D W Y C H A Radio Rooftop Bar 4 2 A R 13 8 L O N G A C R E 3 S T 7 Balthazar Chicken Shop & Hubbard 4 and Bell at The Hoxton COVENT GARDEN 7 LEISURE & CULTURE 6 3 1 National Gallery 6 Royal Festival Hall 1 2 7 Theatre Royal National Theatre ST MARTIN’S LN 3 Aldwych Theatre 8 Royal Courts of Justice LEICESTER 5 4 Royal Opera House 9 Trafalgar Square 5 Somerset House BLACKFRIARS SQUARE 9 2 TEMPLE BLACKFRIARS BRIDGE T 2 E N K M N B A STRAND M E 5 I A R WATERLOO BRIDGE O T STAY CONNECTED 1 C 8 12 I V CHARING CROSS STATION OXO Tower WALKING TIME 9 Holborn 6 mins Temple 8 mins Trafalgar Square Covent Garden 9 mins 10 NORTHUMBERLAND AVE Leicester Square 12 mins EMBANKMENT 7 Charing Cross 12 mins Embankment 12 mins Chancery Lane 13 mins Tottenham Court Road 15 mins 6 London Eye WATERLOO RD THE LOCATION The building benefits from an excellent location on the corner of Aldwych and Kingsway, which links High Holborn to the north and Strand to the south. -

LEICESTER SQUARE / LONDON WC2 a Rare Freehold Opportunity to Develop a Landmark Site in the Heart of London’S West End

LSQ LEICESTER SQUARE / LONDON WC2 A rare freehold opportunity to develop a landmark site in the heart of London’s West End www.lsq-site.com Computer generated image www.lsq-site.com LSQ www.lsq-site.com CENTRE SOHO CENTRAL SHAFTESBURY PICCADILLY THE NATIONAL TRAFALGAR CHARING CORINTHIA HORSE GUARDS THE POINT ST GILES AVENUE CIRCUS W HOTEL GALLERY SQUARE CROSS HOTEL PARADE LONDON EYE STATION THE SAVOY OVERVIEW LSQ LSQ, London WC2 is offered for sale on the instructions of J Gershinson FRICS and S Davidson MRICS of Allsop LLP as Joint Fixed Charge Receivers and Tamarin Ltd / Real Estate Resolutions Ltd. • Freehold site of 0.47 acres fronting Leicester Square in the heart of London’s West End. • Planning consent for a 227,000 sq ft (GIA) mixed use scheme - a 245 bedroom hotel, 33 residential apartments, a roof-top restaurant, restaurants / retail opening out on to the square and a state of the art cinema. • Far reaching views of London’s impressive skyline. • Benefitting from the extensive remodelling and upgrading of Leicester Square which will provide one of London’s finest public realm environments. • Existing tenant income with vacant possession obtainable to suit the purchaser’s timeframe. • Potential for a range of alternative uses on site to match the purchaser’s vision, subject to the necessary consents. • Unconditional offers are invited for the freehold interest. www.lsq-site.com ANGEL KING’S CROSS EUSTON E G FARRINGDON Not to scale and for identification purposes only. LIVERPOOL STREET S G M I A U N N P N B R P E A 40 O Inn N S A O O E R D Smithfield E SH P T E U LD DI W T O B N R T B O H E O N E L T H E S E Market V N Goodge L R E MOORGATE T A T Gardens R .