Annu Al Report 2001

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Market Cap Close ADV 1598 67Th Pctl 745,214,477.91 $ 23.96

Market Cap Close ADV 1598 67th Pctl $ 745,214,477.91 $ 23.96 225,966.94 801 33rd Pctl $ 199,581,478.89 $ 10.09 53,054.83 2399 Ticker_ Listing_ Effective_ Revised Symbol Security_Name Exchange Date Mkt Cap Close ADV Stratum Stratum AAC AAC Holdings, Inc. N 20160906 M M M M-M-M M-M-M AAMC Altisource Asset Management Corp A 20160906 L M L L-M-L L-M-L AAN Aarons Inc N 20160906 H H H H-H-H H-H-H AAV Advantage Oil & Gas Ltd N 20160906 H L M H-L-M H-M-M AB Alliance Bernstein Holding L P N 20160906 H M M H-M-M H-M-M ABG Asbury Automotive Group Inc N 20160906 H H H H-H-H H-H-H ABM ABM Industries Inc. N 20160906 H H H H-H-H H-H-H AC Associated Capital Group, Inc. N 20160906 H H L H-H-L H-H-L ACCO ACCO Brand Corp. N 20160906 H L H H-L-H H-L-H ACU Acme United A 20160906 L M L L-M-L L-M-L ACY AeroCentury Corp A 20160906 L L L L-L-L L-L-L ADK Adcare Health System A 20160906 L L L L-L-L L-L-L ADPT Adeptus Health Inc. N 20160906 M H H M-H-H M-H-H AE Adams Res Energy Inc A 20160906 L H L L-H-L L-H-L AEL American Equity Inv Life Hldg Co N 20160906 H M H H-M-H H-M-H AF Astoria Financial Corporation N 20160906 H M H H-M-H H-M-H AGM Fed Agricul Mtg Clc Non Voting N 20160906 M H M M-H-M M-H-M AGM A Fed Agricultural Mtg Cla Voting N 20160906 L H L L-H-L L-H-L AGRO Adecoagro S A N 20160906 H L H H-L-H H-L-H AGX Argan Inc N 20160906 M H M M-H-M M-H-M AHC A H Belo Corp N 20160906 L L L L-L-L L-L-L AHL ASPEN Insurance Holding Limited N 20160906 H H H H-H-H H-H-H AHS AMN Healthcare Services Inc. -

NASDAQ Stock Market

Nasdaq Stock Market Friday, December 28, 2018 Name Symbol Close 1st Constitution Bancorp FCCY 19.75 1st Source SRCE 40.25 2U TWOU 48.31 21st Century Fox Cl A FOXA 47.97 21st Century Fox Cl B FOX 47.62 21Vianet Group ADR VNET 8.63 51job ADR JOBS 61.7 111 ADR YI 6.05 360 Finance ADR QFIN 15.74 1347 Property Insurance Holdings PIH 4.05 1-800-FLOWERS.COM Cl A FLWS 11.92 AAON AAON 34.85 Abiomed ABMD 318.17 Acacia Communications ACIA 37.69 Acacia Research - Acacia ACTG 3 Technologies Acadia Healthcare ACHC 25.56 ACADIA Pharmaceuticals ACAD 15.65 Acceleron Pharma XLRN 44.13 Access National ANCX 21.31 Accuray ARAY 3.45 AcelRx Pharmaceuticals ACRX 2.34 Aceto ACET 0.82 Achaogen AKAO 1.31 Achillion Pharmaceuticals ACHN 1.48 AC Immune ACIU 9.78 ACI Worldwide ACIW 27.25 Aclaris Therapeutics ACRS 7.31 ACM Research Cl A ACMR 10.47 Acorda Therapeutics ACOR 14.98 Activision Blizzard ATVI 46.8 Adamas Pharmaceuticals ADMS 8.45 Adaptimmune Therapeutics ADR ADAP 5.15 Addus HomeCare ADUS 67.27 ADDvantage Technologies Group AEY 1.43 Adobe ADBE 223.13 Adtran ADTN 10.82 Aduro Biotech ADRO 2.65 Advanced Emissions Solutions ADES 10.07 Advanced Energy Industries AEIS 42.71 Advanced Micro Devices AMD 17.82 Advaxis ADXS 0.19 Adverum Biotechnologies ADVM 3.2 Aegion AEGN 16.24 Aeglea BioTherapeutics AGLE 7.67 Aemetis AMTX 0.57 Aerie Pharmaceuticals AERI 35.52 AeroVironment AVAV 67.57 Aevi Genomic Medicine GNMX 0.67 Affimed AFMD 3.11 Agile Therapeutics AGRX 0.61 Agilysys AGYS 14.59 Agios Pharmaceuticals AGIO 45.3 AGNC Investment AGNC 17.73 AgroFresh Solutions AGFS 3.85 -

Market Cap Close ADV

Market Cap Close ADV 1598 67th Pctl $745,214,477.91 $23.96 225,966.94 801 33rd Pctl $199,581,478.89 $10.09 53,054.83 2399 Listing_ Revised Ticker_Symbol Security_Name Exchange Effective_Date Mkt Cap Close ADV Stratum Stratum AAC AAC Holdings, Inc. N 20160906 M M M M-M-M M-M-M Altisource Asset Management AAMC Corp A 20160906 L M L L-M-L L-M-L AAN Aarons Inc N 20160906 H H H H-H-H H-H-H AAV Advantage Oil & Gas Ltd N 20160906 H L M H-L-M H-M-M AB Alliance Bernstein Holding L P N 20160906 H M M H-M-M H-M-M ABG Asbury Automotive Group Inc N 20160906 H H H H-H-H H-H-H ABM ABM Industries Inc. N 20160906 H H H H-H-H H-H-H AC Associated Capital Group, Inc. N 20160906 H H L H-H-L H-H-L ACCO ACCO Brand Corp. N 20160906 H L H H-L-H H-L-H ACU Acme United A 20160906 L M L L-M-L L-M-L ACY AeroCentury Corp A 20160906 L L L L-L-L L-L-L ADK Adcare Health System A 20160906 L L L L-L-L L-L-L ADPT Adeptus Health Inc. N 20160906 M H H M-H-H M-H-H AE Adams Res Energy Inc A 20160906 L H L L-H-L L-H-L American Equity Inv Life Hldg AEL Co N 20160906 H M H H-M-H H-M-H AF Astoria Financial Corporation N 20160906 H M H H-M-H H-M-H AGM Fed Agricul Mtg Clc Non Voting N 20160906 M H M M-H-M M-H-M AGM A Fed Agricultural Mtg Cla Voting N 20160906 L H L L-H-L L-H-L AGRO Adecoagro S A N 20160906 H L H H-L-H H-L-H AGX Argan Inc N 20160906 M H M M-H-M M-H-M AHC A H Belo Corp N 20160906 L L L L-L-L L-L-L ASPEN Insurance Holding AHL Limited N 20160906 H H H H-H-H H-H-H AHS AMN Healthcare Services Inc. -

Foreign Private Issuers Lists, 1996

u.s. Securities and Exchange Commission FOREIGN COMPANIES REGISTERED AND REPORTING WITH THE u.S. SECURITIES AND EXCHANGE COMMISSION DECEMBER 31 , 1996 Office of International Corporate Finance Division of Corporation Finance REPORTING FOREIGN ISSUERS AS OF DECEMBER 31, 1996 SUMMARY"INFORMATION REPORTING COUNTRY COMPANIES CANADA 374 UNITED KINGDOM 81 ISRAEL 71 MEXICO 30 NETHERLANDS 29 AUSTRALIA 26 BERMUDA 22 CHILE 22 JAPAN 21 FRANCE 18 ITALY 13 ARGENTINA 12 BRITISH VIRGIN ISLANDS 11 IRELAND 11 SWEDEN 10 INDONESIA 9 GERMANY 8 LUXEMBOURG 8 SPAIN 8 NETHERLANDS ANTILLES 7 NORWAY 7 BAHAMAS 6 SOUTH AFRICA 6 CHINA 5 FINLAND 5 HONG KONG 5 LIBERIA 5 BRAZIL 4 CAYMAN ISLANDS 4 COLOMBIA 4 DENMARK 4 KOREA 4 NEW ZEALAND 4 VENEZUELA 4 PERU 3 PORTUGAL 3 SINGAPORE 3 BELGIUM 2 PANAMA 2 PHILIPPINES 2 BELIZE 1 BOTSWANA 1 GHANA 1 PAPUA NEW Gl.!lNEA 1 RUSSIA 1 SWITZERLAND 1 TAIWAN 1 ZAMBIA 1 TOTAL 881 p MARKET SUMMARY BY COUNTRY NASDAQ NASDAQ COUNTRY NYSE AMEX NMS Small Cap OTC COMBINED ARGENTINA 10 0 1 0 1 12 26 AUSTRALIA 9 0 7 3 7 BAHAMAS 1 0 2 0 3 6 BELGIUM 0 0 2 0 0 2 BELIZE 0 0 1 0 0 1 BERMUDA 9 3 7 1 2 22 BOTSWANA 0 0 0 0 1 1 4 BRAZIL 2 0 1 0 1 BRIT. V.1. 0 0 8 1 2 11 CANADA 61 39 94 57 123 374 CAYMAN ISLANDS 0 2 2 0 0 4 CHILE 19 0 1 0 2 22 CHINA 5 0 0 0 0 5 COLOMBIA 2 0 0 0 2 4 DENMARK 3 0 1 0 0 4 FINLAND 3 '0 0 1 1 5 FRANCE 9 0 6 0 3 18 GERMANY 5 0 1 0 2 8 GHANA 1 0 0 0 0 1 HONG KONG 1 0 0 0 4 5 0 4 9 I INDONESIA 4 0 1 IRELAND 5 0 3 1 2 11 ISRAEL 4 5 45 11 6 71 ITALY 11 0 2 0 0 13 JAPAN 11 0 7 1 2 21 KOREA 3 0 0 0 1 4 LIBERIA 2 2 0 0 1 5 LUXEMBOURG 3 0 5 0 0 8 MEXICO 25 2 0 0 3 30 NETH. -

Alphabetical Listing by Company Name

FOREIGN COMPANIES REGISTERED AND REPORTING WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION December 31, 2015 Alphabetical Listing by Company Name COMPANY COUNTRY MARKET 21 Vianet Group Inc. Cayman Islands Global Market 37 Capital Inc. Canada OTC 500.com Ltd. Cayman Islands NYSE 51Job, Inc. Cayman Islands Global Market 58.com Inc. Cayman Islands NYSE ABB Ltd. Switzerland NYSE Abbey National Treasury Services plc United Kingdom NYSE - Debt Abengoa S.A. Spain Global Market Abengoa Yield Ltd. United Kingdom Global Market Acasti Pharma Inc. Canada Capital Market Acorn International, Inc. Cayman Islands NYSE Actions Semiconductor Co. Ltd. Cayman Islands Global Market Adaptimmune Ltd. United Kingdom Global Market Adecoagro S.A. Luxembourg NYSE Adira Energy Ltd. Canada OTC Advanced Accelerator Applications SA France Global Market Advanced Semiconductor Engineering, Inc. Taiwan NYSE Advantage Oil & Gas Ltd. Canada NYSE Advantest Corp. Japan NYSE Aegean Marine Petroleum Network Inc. Marshall Islands NYSE AEGON N.V. Netherlands NYSE AerCap Holdings N.V. Netherlands NYSE Aeterna Zentaris Inc. Canada Capital Market Affimed N.V. Netherlands Global Market Agave Silver Corp. Canada OTC Agnico Eagle Mines Ltd. Canada NYSE Agria Corp. Cayman Islands NYSE Agrium Inc. Canada NYSE AirMedia Group Inc. Cayman Islands Global Market Aixtron SE Germany Global Market Alamos Gold Inc. Canada NYSE Alcatel-Lucent France NYSE Alcobra Ltd. Israel Global Market Alexandra Capital Corp. Canada OTC Alexco Resource Corp. Canada NYSE MKT Algae Dynamics Corp. Canada OTC Algonquin Power & Utilities Corp. Canada OTC Alianza Minerals Ltd. Canada OTC Alibaba Group Holding Ltd. Cayman Islands NYSE Allot Communications Ltd. Israel Global Market Almaden Minerals Ltd. -

NOVA MEASURING INSTRUMENTS LTD. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 20-F o REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) or (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 OR o TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR o SHELL COMPANY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission File Number 000-30668 NOVA MEASURING INSTRUMENTS LTD. (Exact name of Registrant as specified in its charter) Nova Measuring Instruments Ltd. Israel (Translation of Registrant’s name into English) (Jurisdiction of incorporation or organization) Weizmann Science Park, Einstein St., Building 22, 2nd Floor, Ness-Ziona, Israel (Address of principal executive offices) Dror David, +972-73-2295833, +972-8-9407776, P.O.B 266, Rehovot 7610201, Israel (Name, Telephone, E-mail and/or Facsimile number and Address of the Registrant’s Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Ordinary Shares, nominal value NIS 0.01 per share The NASDAQ Global Select Market Securities registered or to be registered pursuant to Section 12(g) of the Act: None Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 27,351,431 ordinary shares, NIS 0.01 nominal (par) value per share, as of December 31, 2016. -

Ticker Name Sector Subgroup Market Cap Price P/E Gryld ESLT ELBIT SYSTEMS LTD Aerospace/Defense Aerospace/Defense-Equip 1872732

Ticker Name Sector Subgroup Market Cap Price P/E GrYld ESLT ELBIT SYSTEMS LTD Aerospace/Defense Aerospace/Defense-Equip 1872732000 43.72 10.16 3.29 TATT TAT TECHNOLOGIES LTD Aerospace/Defense Aerospace/Defense-Equip 44163170 5.01 N/A N/A DELTY DELTA GALIL INDUSTRIES-ADR Apparel Apparel Manufacturers 132338700 5.65 N/A 6.01 CGEN COMPUGEN LTD Biotechnology Medical-Biomedical/Gene 142664900 4.16 N/A N/A PNTR POINTER TELOCATION LTD Commercial Services Commercial Services 19191250 4.01 11.46 N/A LAXAF LAXAI PHARMA LTD Commercial Services Research&Development 570408.8 0.01 N/A N/A BPHX BLUEPHOENIX SOLUTIONS LTD Computers Computer Services 15623440 0.63 N/A N/A JCDA JACADA LTD Computers Computer Services 9037805 2.25 N/A N/A TISA TOP IMAGE SYSTEMS LTD Computers Computers-Integrated Sys 17851280 2.00 18.18 N/A ELTK ELTEK LTD Electronics Circuit Boards 6940612 1.05 N/A N/A ELRNF ELRON ELECTRONIC INDS LTD Electronics Electronic Compo-Misc 122792500 4.14 N/A N/A RADA RADA ELECTRONIC INDS LTD Electronics Electronic Compo-Misc 19954930 2.25 12.50 N/A ORBK ORBOTECH LTD Electronics Electronic Measur Instr 444145500 10.31 7.26 N/A CAMT CAMTEK LTD Electronics Electronic Measur Instr 56486220 1.98 6.83 N/A ITRN ITURAN LOCATION AND CONTROL Electronics Electronic Secur Devices 258956200 12.35 N/A 8.10 MAGS MAGAL SECURITY SYS LTD Electronics Electronic Secur Devices 37967580 2.40 N/A N/A OTIV ON TRACK INNOVATIONS LTD Electronics Identification Sys/Dev 45468330 1.46 N/A N/A BSI ALON HOLDINGS BLUE SQ-ADR Food Food-Retail 342303500 5.19 N/A N/A WILC G. -

ONTO INNOVATION INC. (Exact Name of Registrant As Specified in Its Charter)

2019 Annual Report + 2020 Proxy DEAR SHAREHOLDERS The semiconductor industry plays an increasingly larger role in many of today’s most exciting megatrends. Technological breakthroughs are happening all around us as machine learning is being facilitated by high-power computing combined with high-bandwidth memory. Massive amounts of data are being generated and uploaded to data centers with cloud computing consuming additional processors and memory. In parallel, the anticipated 5G communication channels are increasing data transfer speeds to satisfy the needs of infrastructure, industrial, commercial and consumer systems that will all require more processing power, memory, and wireless (RF systems. The increasing complexity and smaller sizes of all these devices requires inclusive, factory-wide manufacturing controls to achieve higher yields and the long-term reliability that is needed today. With this exciting backdrop, this past June, Nanometrics and Rudolph Technologies announced our intention to merge as equal companies. We recognized that our complementary technologies and teams would accelerate our ability to serve our markets as well as expand our opportunities with strategic customers. Our customers now require a more collaborative and inventive supply chain to maintain their rapid pace of innovation. As our name suggests, Onto Innovation is advancing manufacturing innovation by providing comprehensive solutions to emerging process challenges across the semiconductor value chain. Complementary Products: Throughout the Entire Semiconductor -

Biolinerx Ltd. (Exact Name of Registrant As Specified in Its Charter) (Translation of Registrant’S Name Into English)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F (Mark One) o REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ⌧ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2012 OR o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR o SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report For the transition period from __________ to __________ Commission file number _______________ BioLineRx Ltd. (Exact name of Registrant as specified in its charter) (Translation of Registrant’s name into English) Israel (Jurisdiction of incorporation or organization) P.O. Box 45158 19 Hartum Street Jerusalem 91450, Israel (Address of principal executive offices) Philip Serlin +972 (2) 548-9100 +972 (2) 548-9101 (facsimile) [email protected] P.O. Box 45158 19 Hartum Street Jerusalem 9777518, Israel (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered American Depositary Shares, each representing 10 ordinary shares, par value NIS 0.01 per share Nasdaq Capital Market Ordinary shares, par value NIS 0.01 per share Nasdaq Capital Market* *Not for trading; only in connection with the registration of American Depositary Shares. Securities registered or to be registered pursuant to Section 12(g) of the Act. -

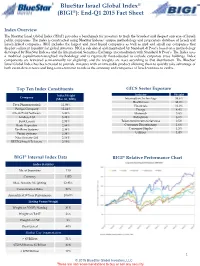

Bluestar Israel Global Index® (BIGI®): End-Q1 2015 Fact Sheet

BlueStar Israel Global Index® (BIGI®): End-Q1 2015 Fact Sheet Index Overview The BlueStar Israel Global Index (’BIGI’) provides a benchmark for investors to track the broadest and deepest universe of Israeli public companies. The index is constructed using BlueStar Indexes’ unique methodology and proprietary database of Israeli and Israeli-linked companies. BIGI includes the largest and most liquid companies as well as mid and small cap companies that display sufficient liquidity for global investors. BIGI is calculated and maintained by Standard & Poor’s based on a methodology developed by BlueStar Indexes and the International Securities Exchange in consultation with Standard & Poor’s. The Index uses a modified capitalization-weighted methodology and is rigorously float-adjusted to exclude corporate cross holdings. Index components are reviewed semi-annually for eligibility, and the weights are reset according to that distribution. The BlueStar Israel Global Index has been created to provide investors with an investable product allowing them to quickly take advantage of both event-driven news and long-term economic trends as the economy and companies of Israel continue to evolve. Top Ten Index Constituents GICS Sector Exposure Index Weight Industry Weight Company (Mar. 31, 2015) Information Technology 33.6% Health Care 32.0% Teva Pharmaceutical 12.93% Financials 16.0% Perrigo Company 12.44% Energy 4.4% Check Point Software 6.42% Materials 3.8% Amdocs Ltd 5.25% Industrials 3.2% Bank Leumi 2.95% Telecommunications Services 2.5% Bank Hapoalim 2.84% Consumer Discretionary 1.6% VeriFone Systems 2.36% Consumer Staples 1.5% Verint Systems 2.34% Utilities 1.4% Nice Systems Ltd 2.16% BEZEQ Israeli Telecom. -

Nova Measuring Instruments Ltd. (NVMI)

April 16, 2019 INITIATING COVERAGE Innovating the Future of Metrology; Initiating Coverage with a Buy Nova Measuring Instruments Ltd. (NVMI) BUY Stock Rating $33.00 We are initiating coverage of Nova Measuring Instruments (NVMI) with a Buy rating Price Target and Price Target of $33, based on 18x our CY20 NG EPS (ex SBC) estimate. Nova is a pure-play wafer fabrication equipment (WFE) vendor participating exclusively in the Process Control optical and materials metrology market. Nova is one of three participants in the thin- film metrology market, which is one of the fastest growing process control segments N. Quinn Bolton, CFA with a ~20% 2014-2018 CAGR. We are positive on Nova’s growth potential in the long run reflecting the company’s leadership position in integrated OCD, growth prospects (212) 705-0322 [email protected] for the company’s unique and innovative XPS technology for materials metrology and Charles Shi, Ph.D. the anticipated market introduction of two new technologies with at least one expected toA metrologybegin generating pure play revenue in 2019. (415) 262-4868 [email protected] . Nova is a pure-play WFE vendor solely focused on the optical Michelle Waller thin film metrology segment of process control, one of the fastest growing process control segments with a ~20% 2014-2018 CAGR. Similar to the deposition, etch and (212) 705-0295 CMP equipment markets, optical thin film metrology is benefiting from the adoption of [email protected] multipleThe leader patterning in integrated in advanced OCD logic and the increasing layer counts in 3D NAND. Since its founding in 1993, Nova has been an innovator of integrated metrology solutions and has established the market leadership position, including in CMP. -

NOVA MEASURING INSTRUMENTS LTD. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) or (g) OF THE SECURITIES EXCHANGE ACT OF 1934 ☐ OR ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 ☒ For the fiscal year ended December 31, 2018 OR TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 ☐ OR SHELL COMPANY REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 ☐ Commission File Number 000-30668 NOVA MEASURING INSTRUMENTS LTD. (Exact name of Registrant as specified in its charter) Nova Measuring Instruments Ltd. Israel (Translation of Registrant’s name into English) (Jurisdiction of incorporation or organization) Weizmann Science Park, Einstein St., Building 22, 2nd Floor, Ness-Ziona, Israel (Address of principal executive offices) Dror David, +972-73-2295833, +972-8-9407776, P.O.B 266, Rehovot 7610201, Israel (Name, Telephone, E-mail and/or Facsimile number and Address of the Registrant’s Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Ordinary Shares, nominal value NIS 0.01 per share The Nasdaq Global Select Market Securities registered or to be registered pursuant to Section 12(g) of the Act: None Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 27,917,505 ordinary shares, NIS 0.01 nominal (par) value per share, as of December 31, 2018.