Central Electricity Regulatory Commission New Delhi

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Village Panchayats in Tamil Nadu District Code District Name

List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 1 Kanchipuram 1 Kanchipuram 1 Angambakkam 2 Ariaperumbakkam 3 Arpakkam 4 Asoor 5 Avalur 6 Ayyengarkulam 7 Damal 8 Elayanarvelur 9 Kalakattoor 10 Kalur 11 Kambarajapuram 12 Karuppadithattadai 13 Kavanthandalam 14 Keelambi 15 Kilar 16 Keelkadirpur 17 Keelperamanallur 18 Kolivakkam 19 Konerikuppam 20 Kuram 21 Magaral 22 Melkadirpur 23 Melottivakkam 24 Musaravakkam 25 Muthavedu 26 Muttavakkam 27 Narapakkam 28 Nathapettai 29 Olakkolapattu 30 Orikkai 31 Perumbakkam 32 Punjarasanthangal 33 Putheri 34 Sirukaveripakkam 35 Sirunaiperugal 36 Thammanur 37 Thenambakkam 38 Thimmasamudram 39 Thilruparuthikundram 40 Thirupukuzhi List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 41 Valathottam 42 Vippedu 43 Vishar 2 Walajabad 1 Agaram 2 Alapakkam 3 Ariyambakkam 4 Athivakkam 5 Attuputhur 6 Aymicheri 7 Ayyampettai 8 Devariyambakkam 9 Ekanampettai 10 Enadur 11 Govindavadi 12 Illuppapattu 13 Injambakkam 14 Kaliyanoor 15 Karai 16 Karur 17 Kattavakkam 18 Keelottivakkam 19 Kithiripettai 20 Kottavakkam 21 Kunnavakkam 22 Kuthirambakkam 23 Marutham 24 Muthyalpettai 25 Nathanallur 26 Nayakkenpettai 27 Nayakkenkuppam 28 Olaiyur 29 Paduneli 30 Palaiyaseevaram 31 Paranthur 32 Podavur 33 Poosivakkam 34 Pullalur 35 Puliyambakkam 36 Purisai List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 37 -

Summer Research Internship Programme at GRD Centre For

Summer research internship programme at GRD Centre for Materials Research, through PSG Centre for Non-Formal & Continuing Education, PSG College of Technology, Coimbatore - 641 004 Genesis: National Advisory Committee About the College Shri. L. Gopalakrishnan, PSG & Sons Charities, Coimbatore Dr. R. Rudramoorthy, PSG CT, Coimbatore PSG College of Technology established in 1951, is one of the many educational institutions nurtured by PSG & Sons Dr. A. Kandaswamy, PSG CT, Coimbatore Charities Trust. The college is Government Aided, Autonomous, ISO 9001 certified and affiliated to Anna University. Equipped Dr. P. C. Angelo, PSG CT, Coimbatore with the latest facilities and excellent infrastructure, the college offers a total of 48 full time and part time programs in Science, Dr. R. Sreenivasan, PSG CT, Coimbatore Engineering and Management at undergraduate, post graduate and doctoral levels. The institution has a strong alumni base, most Dr. G. Amarendra, IGCAR, Kalpakkam of them occupying coveted positions in many educational, industrial and research organizations all over the world. The mission Dr. Anuradha Ashok, PSG IAS, Coimbatore of the College is to provide world-class engineering education, foster research and development, evolve innovative applications of technology, encourage entrepreneurship and ultimately mould young men and women capable of assuming leadership of the Dr. M. Arivanandhan, Anna University, Chennai society for the betterment of the country. Mr. S. Arul (Co-coordinator), PSG PTC, Coimbatore Dr. J. Arunshankar, PSG CT, Coimbatore About the research centre: Mr. Avinash Padmappa, Optis India, Bengaluru Dr. R. Balasundaraprabhu, PSG CT, Coimbatore GRD Centre for Materials Research aims to carry out research on materials for advanced technology. -

Download Author Version (PDF)

RSC Advances This is an Accepted Manuscript, which has been through the Royal Society of Chemistry peer review process and has been accepted for publication. Accepted Manuscripts are published online shortly after acceptance, before technical editing, formatting and proof reading. Using this free service, authors can make their results available to the community, in citable form, before we publish the edited article. This Accepted Manuscript will be replaced by the edited, formatted and paginated article as soon as this is available. You can find more information about Accepted Manuscripts in the Information for Authors. Please note that technical editing may introduce minor changes to the text and/or graphics, which may alter content. The journal’s standard Terms & Conditions and the Ethical guidelines still apply. In no event shall the Royal Society of Chemistry be held responsible for any errors or omissions in this Accepted Manuscript or any consequences arising from the use of any information it contains. www.rsc.org/advances Page 1 of 24 RSC Advances Experimental and Theoretical Studies on Extraction behavior of Di -n-Alkyl Phosphine Oxides towards Actinides Dhrubajyoti Das 1, E. Veerashekhar Goud 1, Suresh Annam 1, S. Jayalakshmi 2, Gopinadhanpillai Gopakumar 2, C.V.S. Brahmmananda Rao 2, N. Sivaraman 2, Akella Sivaramakrishna 1, * and Kari Vijayakrishna 1, * 1 Organic Chemistry Division, School of Advanced Sciences, VIT University, Vellore-632014, Tamil Nadu, India. Manuscript 2 Chemistry Group, Indira Gandhi Centre for Atomic Research (IGCAR), Kalpakkam-603102, Tamil Nadu, India. Accepted Corresponding Author: Dr. Kari Vijayakrishna Address: Organic Chemistry Division, School of Advanced Sciences, VIT University, Vellore 632014, Tamil Nadu, India. -

Chengalpattu District

DISTRICT DISASTER MANAGEMENT PLAN 2020 CHENGALPATTU DISTRICT District Disaster Management Authority Chengalpattu District, Tamil Nadu DISTRICT DISASTER MANAGEMENT PLAN 2020 DISTRICT DISASTER MANAGEMENT AUTHORITY CHENGALPATTU DISTRICT TAMIL NADU PREFACE Endowed with all the graces of nature’s beauty and abundance, the newly created district of Chengalpattu is a vibrant administrative entity on the North eastern part of the state of Tamil Nadu. In spite of the district’s top-notch status in terms of high educational, human development index and humungous industrial productivity, given its geography, climate and certain other socio-political attributes, the district administration and its people have to co-exist with the probabilities of hazards like floods, cyclone, Tsunami, drought, heat wave, lightning and chemical, biological, radiological and nuclear emergencies. The Disastrous events in the recent past like the Tsunami of 2004, the catastrophic floods of year 2015, the cyclone of year 2016 and most recently the COVID-19 pandemic, will serve as a testament to the district’s vulnerability to such hazards. How the society responds to such vagaries of nature decides the magnitude and intensity of the destruction that may entail hazardous events. It is against this back drop, the roll of the District Disaster Management Authority can be ideally understood. The change in perspective from a relief- based approach to a more holistic disaster management approach has already begun to gain currency among the policy makers due to its substantial success in efficient handling of recent disasters across the globe. The need of the hour, therefore, is a comprehensive disaster management plan which is participative and people-friendly with the component of inter- departmental co-ordination at its crux. -

Details for KALPAKKAM

ANNEXURE-I Reply to AD, KMG, NPCIL email dated 12/07/2021 with regard to MAPS arrangement for Selection interview for ET-2020 during Aug.9 th to 21, 2021 to publish in the Recruitment Portal is as follows: SNo Information sought Response 1 ‘Place of Reporting’ for Selection Interview DAE OFFICERS HOSTEL, (If a candidate wishes to arrive on their DAE TOWNSHIP,KALPAKKAM 603 102 own) CHENGALPATTU DIST., TAMIL NADU. 1.a. Complete Address including location hyperlink DAE OFFICERS HOSTEL, of 'Place of Reporting' DAE TOWNSHIP,KALPAKKAM 603 102 CHENGALPATTU DIST., TAMIL NADU. Location hyper link is given below. 1.b. Name, designation, email address, mobile and 1. N. SRINIVASAN, MANAGER(HR), landline telephone numbers of the Contact MADRAS ATOMIC POWER official/s STATION,KALPAKKAM. MOBILE NO: 9489046185 Email id: [email protected] 2. R. NEHRU SAH,SR. ASSISTANT.GR.1(HR) MADRAS ATOMIC POWER STATION, KALPAKKAM. MOBILE NO: 9445397562 Email id: [email protected] 1.c. A small write up on ‘How to Reach the Kalpakkam is situated about 70 Kms. Interview Venue’ by Rail/Road/Air/Taxi/ from Chennai Domestic Airport and 73 Others from various parts of Country Kms. from Purachi Thalaivar including available modes of public M.G.Ramachandran Central Railway transport from nearby Railway Station/ Station Egmore Railway Station. (Journey time approximately 2½ hours), Airport/ Bus Depot to reach 'Place of 30 kms from Chengalpattu7. Reporting' To reach Kalpakkam - Board Kalpakkam Bus(No.188 and ECR –Pondicherry Bus) plying from Koyambedu Bus Terminus alight at Pudupattinam/Kalpakkam or hire a taxi from Airport/Railway station. -

Site-Specific Analysis of Cancer Incidence and Related Sociological Parameters in a ‘Radiation Hot Spot’, Along the West Coast of Tamil Nadu, India

International Journal of Health Sciences and Research www.ijhsr.org ISSN: 2249-9571 Original Research Article Site-Specific Analysis of Cancer Incidence and Related Sociological Parameters in a ‘Radiation Hot Spot’, along the West Coast of Tamil Nadu, India Aneesh D1, Kanagappan, M2, Godwin Wesley S3 1Research Scholar, 2Associate Professor, 3Professor Emeritus, Department of Zoology and Research Centre, Scott Christian College (Autonomous), Nagercoil - 629 003, Kanniyakumari District, Tamil Nadu Corresponding Author: Aneesh D ABSTRACT Background: Manavalakurichi, along the west coast of Tamil Nadu, India is well known for its natural radioactivity due to deposition of monazite sand and considered as high background natural radiation area (HBNRA). The incidence of cancer in relation to background radiation and parameters such as occupation, habits (tobacco chewing, smoking, drinking) and gender was preliminarily assessed. Although residing in a HBNRA has been reported to lead to an increase in the frequency of chromosomal aberrations in lymphocytes, the carcinogenic effect has not yet been established. The present study aims to evaluate the impact of background radiation in residents of HBNRA. Materials and Methods: A cross-sectional study was conducted considering 938 and 778 residents from HBNRA and low background natural radiation area (LBNRA), respectively using as health assessment survey questionnaire. Result: The incidence of cancer was 1.49% in HBNRA and 1.43% in LBNRA. Regression analysis of the total population of both areas revealed that radiation dose is not significantly related to incidence of cancer (R2 = 0.010, p=0.411). Pearson chi-square analysis of data showed that a higher proportion (age >18 years) has relationship between cancer and tobacco usage [HBNRA: χ2 (1, N=364) = 7.098, p = 0.009, LBNRA: χ2 (1, N=322) = 5.544, p = 0.024]. -

Cmi-Brochure-2015.Pdf

Chennai Mathematical Institute National Undergraduate and Postgraduate Programmes in Mathematical Sciences Information Brochure, 2015{2016 3-Year B.Sc. (Honours) Programme in Mathematics and Computer Science 3-Year B.Sc. (Honours) Programme in Mathematics and Physics 2-Year M.Sc. Programme in Mathematics 2-Year M.Sc. Programme in Computer Science 2-Year M.Sc. Programme in Applications of Mathematics Ph.D. Programme in Mathematics Ph.D. Programme in Computer Science Ph.D. Programme in Physics Contact Address Chennai Mathematical Institute H1, SIPCOT IT Park, Siruseri Kelambakkam 600 130, India Phone: (044) 6748 0900, (044) 2747 0226{0229, (044) 3298 3441/3442 Fax: (044) 2747 0225 E-mail: [email protected] WWW: http://www.cmi.ac.in/admissions The Chennai Mathematical Institute Chennai Mathematical Institute (CMI), a university under Section 3 of the UGC Act 1956, is recognized both within the country and abroad as one of the important centres in India for research and teaching in mathematical sciences. CMI is set up under a Trust and is managed by a Governing Council made up of eminent academic personalities. The teaching programmes are overseen by the Academic Council, consisting of senior faculty from CMI and other leading institutions across India. The members of the Governing Council and Academic Council are listed on the front and back inside covers. Research at CMI The Institute is headed by Professor Rajeeva L. Karandikar, an inter- nationally renowned mathematician. CMI was founded in 1989 by Pro- fessor C. S. Seshadri, f.r.s., who is presently Director-Emeritus. The Institute has a talented group of faculty members who have strong aca- demic ties with reputed institutions in India and abroad. -

Address of Canara Bank Wings Identified for Concurrent/ Continuous Audit by External Chartered Accountants for the Period 01St July 2021 to 30Th June 2022

ADDRESS OF CANARA BANK WINGS IDENTIFIED FOR CONCURRENT/ CONTINUOUS AUDIT BY EXTERNAL CHARTERED ACCOUNTANTS FOR THE PERIOD 01ST JULY 2021 TO 30TH JUNE 2022 S no DP Branch Name Circle Address City Pin code State Dist. 1. 6987 CPC - FT Manipal Integrated Treasury Wing, Manipal 576104 Karnataka Udupi HO Annex, II Floor, 2. 6805 CPC –FT Mumbai Canara Bank Bldgs, 8th Mumbai 400051 Maharashtra Mumbai Suburban Floor, C-14, G-Block, MCA Club, Bandra-Kurla Complex, ADDRESS OF CANARA BANK LARGE CORPORATE BRANCHES IDENTIFIED FOR CONCURRENT/ CONTINUOUS AUDIT BY EXTERNAL CHARTERED ACCOUNTANTS FOR THE PERIOD 01ST JULY 2021 TO 30TH JUNE 2022 S no DP Branch Name Circle Address City Pin code State Dist. 3. 4891 CHANDIGARH LARGE Chandigarh SCO 117-119, Sector-17C, Chandigarh 160017 Chandigarh-UT Chandigarh CORPORATE BRANCH Chandigarh 4. 2636 BENGALURU LARGE Bengaluru #18, Ramanashree Arcade, Bengaluru 560001 Karnataka Bengaluru Urban CORPORATE BRANCH III Floor, M G Road, 5. 1942 NEW DELHI Delhi II Floor, 9, World Trade Delhi 110002 NCT of Delhi-UT New Delhi CONNAUGHT PLACE Tower, Barakambha Lane, LARGE CORPORATE BRANCH 6. 19531 LARGE CORPORATE Kolkata ILLACO HOUSE, 1, Kolkata 700001 West Bengal Kolkata BRANCH KOLKATA BRABOURNE ROAD, BRABOURNE ROAD LARGE CORPORATE BRANCH, Page 1 of 45 ADDRESS OF CANARA BANK RETAIL ASSET HUBs IDENTIFIED FOR CONCURRENT/ CONTINUOUS AUDIT BY EXTERNAL CHARTERED ACCOUNTANTS FOR THE PERIOD 01ST JULY 2021 TO 30TH JUNE 2022 S no DP Branch Name Circle Address City Pin code State Dist. 7. 2284 RAH ANANTHAPUR Vijayawada Near Clock Tower, I Floor, Anantapur 515001 Andhra Pradesh Anantapur Canara Bank Branch Main-II, 8. -

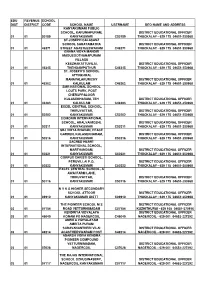

Deo &Ceo Address List

EDU REVENUE SCHOOL DIST DISTRICT CODE SCHOOL NAME USERNAME DEO NAME AND ADDRESS KANYAKUMARI PUBLIC SCHOOL, KARUNIAPURAM, DISTRICT EDUCATIONAL OFFICER 01 01 50189 KANYAKUMARI C50189 THUCKALAY - 629 175 04651-250968 ST.JOSEPH CALASANZ SCHOOL SAHAYAMATHA DISTRICT EDUCATIONAL OFFICER 01 01 46271 STREET AGASTEESWARAM C46271 THUCKALAY - 629 175 04651-250968 GNANA VIDYA MANDIR MADUSOOTHANAPURAM VILLAGE KEEZHAKATTUVILAI, DISTRICT EDUCATIONAL OFFICER 01 01 46345 THENGAMPUTHUR C46345 THUCKALAY - 629 175 04651-250968 ST. JOSEPH'S SCHOOL ATTINKARAI, MANAVALAKURICHY DISTRICT EDUCATIONAL OFFICER 01 01 46362 KALKULAM C46362 THUCKALAY - 629 175 04651-250968 SMR NATIONAL SCHOOL LOUTS PARK, POST CHERUPPALOOR KULASEKHARAM, TEH DISTRICT EDUCATIONAL OFFICER 01 01 46383 KALKULAM C46383 THUCKALAY - 629 175 04651-250968 EXCEL CENTRAL SCHOOL, THIRUVATTAR, DISTRICT EDUCATIONAL OFFICER 01 01 50202 KANYAKUMARI C50202 THUCKALAY - 629 175 04651-250968 COMORIN INTERNATIONAL SCHOOL, ARALVAIMOZHI, DISTRICT EDUCATIONAL OFFICER 01 01 50211 KANYAKUMARI C50211 THUCKALAY - 629 175 04651-250968 SBJ VIDYA BHAVAN, PEACE GARDEN, KULASEKHARAM, DISTRICT EDUCATIONAL OFFICER 01 01 50216 KANYAKUMARI C50216 THUCKALAY - 629 175 04651-250968 SACRED HEART INTERNATIONAL SCHOOL, MARTHANDAM, DISTRICT EDUCATIONAL OFFICER 01 01 50221 KANYAKUMARI C50221 THUCKALAY - 629 175 04651-250968 CORPUS CHRISTI SCHOOL, PERUVILLAI P.O, DISTRICT EDUCATIONAL OFFICER 01 01 50222 KANYAKUMARI C50222 THUCKALAY - 629 175 04651-250968 EXCEL CENTRAL SCHOOL, A AWAI FARM LANE, THIRUVATTAR, DISTRICT EDUCATIONAL OFFICER -

Officials from the State of Tamil Nadu Trained by NIDM During the Year 209-10 to 2014-15

Officials from the state of Tamil Nadu trained by NIDM during the year 209-10 to 2014-15 S.No. Name Designation & Address City & State Department 1 Shri G. Sivakumar Superintending National Highways 260 / N Jawaharlal Nehru Salai, Chennai, Tamil Engineer, Roads & Jaynagar - Arumbakkam, Chennai - 600166, Tamil Nadu Bridges Nadu, Ph. : 044-24751123 (O), 044-26154947 (R), 9443345414 (M) 2 Dr. N. Cithirai Regional Joint Director Animal Husbandry Department, Government of Tamil Chennai, Tamil (AH), Animal husbandry Nadu, Chennai, Tamil Nadu, Ph. : 044-27665287 (O), Nadu 044-23612710 (R), 9445001133 (M) 3 Shri Maheswar Dayal SSP, Police Superintending of Police, Nagapattinam District, Tamil Nagapattinam, Nadu, Ph. : 04365-242888 (O), 04365-248777 (R), Tamil Nadu 9868959868 (M), 04365-242999 (Fax), Email : [email protected] 4 Dr. P. Gunasekaran Joint Director, Animal Animal Husbandary, Thiruvaruru, Tamil Nadu, Ph. : Thiruvarur, Tamil husbandary 04366-205946 (O), 9445001125 (M), 04366-205946 Nadu (Fax) 5 Shri S. Rajendran Dy. Director of Department of Agriculture, O/o Joint Director of Ramanakapuram, Agriculture, Agriculture Agriculture, Ramanakapuram (Disa), Tamil Nadu, Ph. : Tamil Nadu 04567-230387 (O), 04566-225389 (R), 9894387255 (M) 6 Shri R. Nanda Kumar Dy. Director of Statistics, Department of Economics & Statistics, DMS Chennai, Tamil Economics & Statistics Compound, Thenampet, Chennai - 600006, Tamil Nadu Nadu, Ph. : 044-24327001 (O), 044-22230032 (R), 9865548578 (M), 044-24341929 (Fax), Email : [email protected] 7 Shri U. Perumal Executive Engineer, Corporation of Chennai, Rippon Building, Chennai - Chennai, Tamil Municipal Corporation 600003, Ph. : 044-25361225 (O), 044-65687366 (R), Nadu 9444009009 (M), Email : [email protected] National Institute of Disaster Management (NIDM) Trainee Database is available at http://nidm.gov.in/trainee2.asp 58 Officials from the state of Tamil Nadu trained by NIDM during the year 209-10 to 2014-15 8 Shri M. -

2004 Indian Ocean Tsunami on the Madras Nuclear Power Plant, India

Transactions of the Korean Nuclear Society Spring Meeting Chuncheon, Korea, May 25-26 2006 2004 Indian Ocean Tsunami on the Madras Nuclear Power Plant, India Sobeom Jin,a Sungjin Hong,b Fumihiko Imamura,c a Korea Institute of Nuclear Safety, P.O.Box 114, Yusong, Daejon, 305-600,[email protected] b SKK University, 330, Cheoncheon-dong, Jangan-gu, Suwon, Gyeonggi-do, 440-746 c Disaster Control Research Center, Tohoku Univ., Aoba 6-6-11-1106, Sendai, 980-8579, Japan 1. Introduction the traveling water screen in the seawater pump house due to heavy ingress of debris caused by the tsunami. In On December 26 00:58(UTC), 06:28 (Local time, Further, the cooling of the reactor of MAPS Unit-2 and India), a great earthquake occurred off the coast of north different loads were achieved by using the firewater Sumatra, Indonesia. The magnitude of this earthquake system. Though the offsite power remained available was 9.0 and it was the fourth largest earthquake in the throughout the event, emergency diesel generators were world since 1900. The tsunami, 2004 Indian Ocean started and kept running as a precautionary measure. tsunami, accompanied with this earthquake propagated The plant declared an emergency alert at 10:25 on in the entire Indian Ocean, and caused significant December 26, which was lifted at 21:43 on December damage. The tsunami attacked not only the coast of 27. Indonesia and Thailand, close to the source of The tsunami did not affect the activities in MAPS earthquake, but also the coast of India, Sri Lanka, and Unit-1, which was under shutdown. -

Chennai Mathematical Institute - 01-27-2014 by Asia Pacific Mathematics Newsletter - Gonit Sora

Chennai Mathematical Institute - 01-27-2014 by Asia Pacific Mathematics Newsletter - Gonit Sora - https://gonitsora.com Chennai Mathematical Institute by Asia Pacific Mathematics Newsletter - Monday, January 27, 2014 https://gonitsora.com/chennai-mathematical-institute/ The Chennai Mathematical Institute (CMI) is one of the important centres in India for research in and teaching of mathematical sciences. The Institute is recognised as a University by the Indian government and awards bachelors, masters and doctoral degrees. History CMI began as a research institute in 1989 which carried out only a PhD programme. In 1998, the institute ventured into teaching, with an undergraduate course for Mathematics and Computer Science. An undergraduate course in Physics was added a few years later. Parallel to this, CMI began its Masters programmes in Mathematics and Computer Science. A new Masters course in Applications of Mathematics was started in 2010. The institute was founded by C S Seshadri, an internationally renowned algebraic geometer. The present Director is Rajeeva Karandikar, who is an expert in probability theory and statistics. The institute has a talented group of about 30 permanent faculty members who have strong academic ties with reputed institutions in India and abroad. The institute also attracts a regular stream of academic visitors, both from India and abroad. Research The main areas of research in Mathematics pursued at the Institute are algebra, analysis, differential equations, geometry, probability, statistics and topology. In Computer Science, the main areas of research are formal methods in the specification and verification of software systems, design and analysis of algorithms, computational complexity theory and computer security.