Chapter 3: Preparing Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Account Guidelines for Managers and Delegates

ACCOUNT/BUDGET GENERAL OPERATING PRINCIPLES for IU SOUTHEAST ACCOUNT MANAGERS / ACCOUNT DELEGATES The Fiscal Year runs from July 1 – June 30. Operating budgets are distributed in June/July. Accounts may not exceed their budgeted amounts within the fiscal year. Account managers will be required to develop a plan to bring the account in balance before the closing of the fiscal year or to carry forward the over- expenditures to the next fiscal year. Allocated funds do not carry forward to the next fiscal year. Unused funds are forfeited. Allocated funds should be spent to or close to zero. Every department has an organization code (contact Melissa Hill in Accounting Services, #2359). Examples: Student Affairs (SSER), Athletics (ATHL). A budget binder or file should be established for each account. All budget documents should be kept for the current fiscal year within the budget binder or file. Receipts/documentation must be kept for all expenditures. All budget documentation must be kept on file for seven years. Use of funds must conform to IU Financial Policies found on web site: http://www.indiana.edu/%7Epolicies/ The Financial Information System (FIS) is used for account transactions and account monitoring. Passwords and access are needed (contact IT or Accounting Services). If FIS training is needed, contact Melissa Hill in Accounting Services (#2359). Monthly operating statements should be printed from FIS (available first of month—notification comes by email) and account transactions should be reconciled by the account manager or delegate on a monthly basis at minimum. Each expenditure must be accounted for with receipts or other appropriate documentation. -

Preparing a Short-Term Cash Flow Forecast

Preparing a short-term What is a short-term cash How does a short-term cash flow forecast and why is it flow forecast differ from a cash flow forecast important? budget or business plan? 27 April 2020 The COVID-19 crisis has brought the importance of cash flow A short-term cash flow forecast is a forecast of the The income statement or profit and loss account forecasting and management into sharp focus for businesses. cash you have, the cash you expect to receive and in a budget or business plan includes non-cash the cash you expect to pay out of your business over accounting items such as depreciation and accruals This document explores the importance of forecasting, explains a certain period, typically 13 weeks. Fundamentally, for various expenses. The forecast cash flow how it differs from a budget or business plan and offers it’s about having good enough information to give statement contained in these plans is derived from practical tips for preparing a short-term cash flow forecast. you time and money to make the right business the forecast income statement and balance sheet decisions. on an indirect basis and shows the broad categories You can also access this information in podcast form here. of where cash is generated and where cash is spent. Forecasts are important because: They are produced on a monthly or quarterly basis. • They provide visibility of your future cash position In contrast, a short-term cash flow forecast: and highlight if and when your cash position is going to be tight. -

Illustrative IFRS Financial Statements 2019 – Investment Funds

Illustrative IFRS financial statements 2019 Investment funds Stay informed. Visit inform.pw c.com Illustrative IFRS financial statements 2019 – Investment funds Illustrative IFRS financial statements 2019 – Investment funds This publication provides an illustrative set of financial statements, prepared in accordance with International Financial Reporting Standards (IFRS), for a fictional open-ended investment fund (‘ABC Fund’ or the ‘Fund’). ABC Fund is an existing preparer of IFRS financial statements; IFRS 1, ‘First-time adoption of IFRS’, is not applicable. It does not have any subsidiaries, associates or joint ventures. The Fund’s shares are not traded in a public market. Guidance on financial statements for first-time adopters of IFRS is available at www.pwc.com/ifrs. This publication is based on the requirements of IFRS standards and interpretations for the financial year beginning on 1 January 2019. There are no standards effective for the first time in 2019 that required changes to the disclosures or accounting policies in this publication. However, readers should consider whether any of the standards that are mandatory for the first time for financial years beginning 1 January 2019 could affect their own accounting policies. Appendix XII contains a full list of these standards (including those that have only a disclosure impact) as well as a summary of their key requirements. In compiling the illustrative disclosures, we have updated the guidance included in Appendix VIII to address IFRIC 23 ‘Uncertainty over income tax treatments’ which is applicable for financial years beginning on or after 1 January 2019. Commentary boxes are included throughout the publication to provide additional information where necessary. -

Chapter 5 Consolidation Following Acquisition Consolidation Following

Consolidation Following Acquisition Chapter 5 • The procedures used to prepare a consolidated balance sheet as of the date of acquisition were introduced in the preceding chapter, that is, Consolidation Chapter 4. Following Acquisition • More than a consolidated balance sheet, however, is needed to provide a comprehensive picture of the consolidated entity’s activities following acquisition. McGraw-Hill/Irwin Copyright © 2005 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Consolidation Following Acquisition Consolidation Following Acquisition • The purpose of this chapter is to present the procedures used in the preparation of a • As with a single company, the set of basic consolidated balance sheet, income statement, financial statements for a consolidated entity and retained earnings statement subsequent consists of a balance sheet, an income to the date of combination. statement, a statement of changes in retained earnings, and a statement of cash flows. • The preparation of a consolidated statement of cash flows is discussed in Chapter 10. 5-3 5-4 Consolidation Following Acquisition Consolidation Following Acquisition • This chapter first deals with the important concepts of consolidated net income and consolidated retained earnings. • Finally, the remainder of the chapter deals with the specific procedures used to • Thereafter, the chapter presents a description prepare consolidated financial statements of the workpaper format used to facilitate the subsequent to the date of combination. preparation of a full set of consolidated financial statements. 5-5 5-6 1 Consolidation Following Acquisition Consolidation Following Acquisition • The discussion in the chapter focuses on procedures for consolidation when the parent company accounts for its investment in • Regardless of the method used by the parent subsidiary stock using the equity method. -

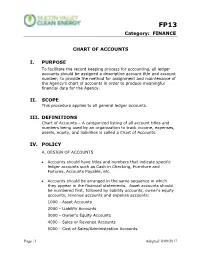

G&A101 Chart of Accounts

FP13 Category: FINANCE CHART OF ACCOUNTS I. PURPOSE To facilitate the record keeping process for accounting, all ledger accounts should be assigned a descriptive account title and account number; to provide the method for assignment and maintenance of the Agency’s chart of accounts in order to produce meaningful financial data for the Agency. II. SCOPE This procedure applies to all general ledger accounts. III. DEFINITIONS Chart of Accounts – A categorized listing of all account titles and numbers being used by an organization to track income, expenses, assets, equity, and liabilities is called a Chart of Accounts. IV. POLICY A. DESIGN OF ACCOUNTS • Accounts should have titles and numbers that indicate specific ledger accounts such as Cash in Checking, Furniture and Fixtures, Accounts Payable, etc. • Accounts should be arranged in the same sequence in which they appear in the financial statements. Asset accounts should be numbered first, followed by liability accounts, owner’s equity accounts, revenue accounts and expense accounts: 1000 - Asset Accounts 2000 - Liability Accounts 3000 - Owner’s Equity Accounts 4000 - Sales or Revenue Accounts 5000 - Cost of Sales/Administration Accounts Page | 1 Adopted: 8/09/2017 FP13 Category: FINANCE 6000 - Debt Service Accounts 8000 - Other Accounts B. DESCRIPTION OF ACCOUNTS • Each account should be given a short title description that is brief but will allow the reader to quickly ascertain the purpose of the account. • For training and consistent transaction coding, as well as to help other non-accounting managers understand why something is recorded as it is, each account should be defined. Definitions should be concise and meaningful. -

Absorption Costing - Overview

Absorption Costing - Overview 1. Overview of Absorption costing and Variable Costing 2. Review how costs for Manufacturing are transferred to the product 3. Job Order Vs. Process Costing 4. Overhead Application - Under applied Overhead - Over applied overhead 5. Problems with Absorption Costing 6. Concluding Comments Absorption Costing The focus of this class is on how to allocate manufacturing costs to the product. - Direct Materials - Direct Labor - Overhead Absorption costing is a process of tracing the variable costs of production and the fixed costs of production to the product. Variable Costing traces only the variable costs of production to the product and the fixed costs of production are treated as period expenses. Absorption Costing There are three different types of Absorption Costing Systems: - Job Order Costing - Process Costing - ABC Costing In Job Order Costing costs are assigned to the product in Batches or lots. - Printing - Furniture manufacturing - Bicycle Manufacturing In Process Costing, costs are systematically assigned to the product, since there are no discreet batches to assign costs. - Oil Distilling - Soda Manufacturing ABC Costing assigns cost from cost centers to the product - Best in a multi product firm, where there are different volumes Absorption Costing A simplified view of Production: Introduce Raw Manufacture Store finished Sell Finished Materials Product goods Goods 1. Direct materials 1. Direct labor 1. Production process are purchased applied to completed 2. Direct materials product 2. Goods are shipped are placed into 2. Overhead costs for sale production are incurred Absorption Costing How do we account for the production process? 1. Direct materials are purchased and recorded as an asset. -

Cash Flow Statement Introduction Introd. Contd

Cash Flow Statement Chapter 4 Introduction Management and other interested external parties have always recognized the need for a cash flow statement but it was never required until the FASB (Financial Accounting Standards Board) issued Statement # 95 “Statement of Cash Flows” in 1988. This statement required that: - businesses include a statement of cash flow as part of their financial reporting. Introd. Contd. Under GAAP, most businesses use accrual basis of accounting. This method requires that revenue is recorded when earned and expenses recorded when incurred. Now, revenue may include credit sales that have yet to be collected in cash and expenses that have yet to be paid. Thus under accrual accounting net income will generally not equal net cash flow from operations. 1 Need for the CF statement? Fact is, not all revenue that is earned is received in cash or received immediately, and not all expenses incurred is paid. So a cash flow statement reconciles the accrual income statement to net cash collected or paid. Cash is critical to any hospitality business. A hotel or restaurant’s success or failure will be determined by, among other things, how the flow of cash is utilized by management. Purpose of Cash Flow statement • To use information about the past sources of cash to predict the hotel or restaurant’s ability to generate positive cash flows in the future. • To establish the hotel or restaurant’s ability to pay its bills – ability to meet its obligations. Purpose – contd. • To ascertain whether the business’ cash is coming from operations mostly or from other sources instead. -

Cash Advance Admin User Guide

Concur Expense: Cash Advance Admin User Guide Last Revised: August 27 2021 Applies to these SAP Concur solutions: Expense Professional/Premium edition Standard edition Travel Professional/Premium edition Standard edition Invoice Professional/Premium edition Standard edition Request Professional/Premium edition Standard edition Table of Contents Section 1: Permissions ................................................................................................ 1 Section 2: Overview .................................................................................................... 1 Typical Cash Advance Process ...................................................................................... 1 Receiving Email Notifications of a Cash Advance Pending Issuance ................................... 2 Cash Advances Using a Company Card.......................................................................... 2 Imported Transactions of Type Cash Advance ........................................................... 3 Directly Issued and Auto-Issuance Cash Advances ......................................................... 3 Section 3: Cash Advance Admin Tool ........................................................................... 3 Section 4: Procedures ................................................................................................. 4 Accessing Cash Advance Admin.................................................................................... 4 Searching for Employees ............................................................................................ -

Chapter 5 Questions Multiple Choice 1

Chapter 5 Question Review 1 Chapter 5 Questions Multiple Choice 1. At the beginning of the year, Paradise Co. had an inventory of $200,000. During the year, the company purchased goods costing $900,000. Paradise Co reported ending inventory of $300,000 at the end of the year. Their cost of goods sold is a. $1,000,000 b. $800,000 c. $1,400,000 d. $400,000 2. Under the perpetual inventory system, in addition to making the entry to record a sale, a company would a. debit Inventory and credit Cost of Goods Sold. b. debit Cost of Goods Sold and credit Purchases. c. debit Cost of Goods sold and credit Inventory. d. make no additional entry until the end of the period. 3. Gross profit equals the difference between net sales and a. operating expenses. b. cost of goods sold. c. net income. d. cost of goods sold plus operating expenses. 4. Income from operations appears on a. both a multiple-step and a single-step income statement. b. neither a multiple-step nor a single-step income statement. c. a single-step income statement. d. a multiple-step income statement. 5. The entry for a buyer to record the return of goods under a perpetual inventory system assuming the purchase was made on account would include a a. debit to inventory b. debit to purchase returns and allowances c. credit to accounts payable d. debit to accounts payable 6. Under the perpetual system, cash freight costs incurred by the buyer for the transporting of goods is recorded in which account? a. -

Consolidated Financial Statements 2019

CONSOLIDATED FINANCIAL STATEMENTS 2019 Contents Consolidated Financial Statements The Board of Directors' and CEO's Report 1 14 Property, plant and equipment 41 Independent Auditor's report 7 15 Right of use assets 43 Consolidated Statement of Income 11 16 Goodwill 44 Consolidated Statement of Comprehensive Income 12 17 Intangible assets 46 Consolidated Statement of Financial Position 13 18 Investments in associates 47 Consolidated Statement of Changes in Equity 14 19 Trade receivables, other receivables and Consolidated Statement of Cash Flows 15 prepayments 48 Notes to the Consolidated Financial Statements 16 20 Deferred income tax 49 1 General information 16 21 Inventories 51 2 Summary of significant accounting policies 17 22 Equity 52 3 Critical accounting estimates and 23 Borrowings and lease liabilities 56 assumptions 31 24 Provisions 61 4 Business combinations 32 25 Post-employment benefits 62 5 Non-IFRS measurement 34 26 Financial instruments and risks 62 6 Segment information 35 27 Trade and other payables 68 7 Revenues 37 28 Contingencies 69 8 Expenses by nature 38 29 Related party transactions and information on 9 Net finance costs 38 remuneration 70 10 Staff costs 38 30 Subsequent events 71 11 Fees to Auditors 39 31 Subsidiaries 72 12 Income tax 39 32 Quarterly results (unaudited) 73 13 Earnings per share 40 33 Definitions and abbreviations 75 The Board of Directors' and CEO's Report Marel is a leading global provider of advanced utilization levels the interest and finance cost is processing equipment, systems, software and expected to decrease as the new facility includes services to the poultry, meat and fish industries with more favorable terms. -

Reading and Understanding Nonprofit Financial Statements

Reading and Understanding Nonprofit Financial Statements What does it mean to be a nonprofit? • A nonprofit is an organization that uses surplus revenues to achieve its goals rather than distributing them as profit or dividends. • The mission of the organization is the main goal, however profits are key to the growth and longevity of the organization. Your Role in Financial Oversight • Ensure that resources are used to accomplish the mission • Ensure financial health and that contributions are used in accordance with donor intent • Review financial statements • Compare financial statements to budget • Engage independent auditors Cash Basis vs. Accrual Basis • Cash Basis ▫ Revenues and expenses are not recognized until money is exchanged. • Accrual Basis ▫ Revenues and expenses are recognized when an obligation is made. Unaudited vs. Audited • Unaudited ▫ Usually Cash Basis ▫ Prepared internally or through a bookkeeper/accountant ▫ Prepared more frequently (Quarterly or Monthly) • Audited ▫ Accrual Basis ▫ Prepared by a CPA ▫ Prepared yearly ▫ Have an Auditor’s Opinion Financial Statements • Statement of Activities = Income Statement = Profit (Loss) ▫ Measures the revenues against the expenses ▫ Revenues – Expenses = Change in Net Assets = Profit (Loss) • Statement of Financial Position = Balance Sheet ▫ Measures the assets against the liabilities and net assets ▫ Assets = Liabilities + Net Assets • Statement of Cash Flows ▫ Measures the changes in cash Statement of Activities (Unaudited Cash Basis) • Revenues ▫ Service revenues ▫ Contributions -

VALUE IFRS Plc Illustrative IFRS Consolidated Financial Statements December 2019

VALUE IFRS Plc Illustrative IFRS consolidated financial statements December 2019 This publication presents the sample annual financial reports of a fictional listed company, VALUE IFRS Plc. It illustrates the financial reporting requirements that would apply to such a company under International Financial Reporting Standards as issued at 31 May 2019. Supporting commentary is also provided. For the purposes of this publication, VALUE IFRS Plc is listed on a fictive Stock Exchange and is the parent entity in a consolidated entity. VALUE IFRS Plc 2019 is for illustrative purposes only and should be used in conjunction with the relevant financial reporting standards and any other reporting pronouncements and legislation applicable in specific jurisdictions. Global Accounting Consulting Services PricewaterhouseCoopers LLP This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. About PwC At PwC, our purpose is to build trust in society and solve important problems. We're a network of firms in 158 countries with more than 250,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com © 2019 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. VALUE IFRS Plc Illustrative IFRS consolidated financial statements December