This Is Part of Our Round Table on Against the Troika: Crisis and Austerity in the Eurozone

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Exchange Rate: Economic Policy Tool Or Market Price?

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Research Papers in Economics UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT THE EXCHANGE RATE: ECONOMIC POLICY TOOL OR MARKET PRICE? Heiner Flassbeck No. 157 November 2001 DISCUSSION PAPERS THE EXCHANGE RATE: ECONOMIC POLICY TOOL OR MARKET PRICE? Heiner Flassbeck No. 157 November 2001 I am grateful to Yilmaz Akyüz, Wolfgang Filc and Jörg Mayer for their helpful comments on the first draft. UNCTAD/OSG/DP/157 - ii - The opinions expressed in this paper are those of the author and do not necessarily reflect the views of UNCTAD. The designations and terminology employed are also those of the author. UNCTAD Discussion Papers are read anonymously by at least one referee, whose comments are taken into account before publication. Comments on this paper are invited and may be addressed to the author, c/o the Editorial Assistant*, Macroeconomic and Development Policies, GDS, United Nations Conference on Trade and Development (UNCTAD), Palais des Nations, CH-1211 Geneva 10, Switzerland. Copies of Discussion Papers may also be obtained from this address. New Discussion Papers are available on the website at: http://www.unctad.org/en/pub/pubframe.htm * Tel. 022–907.5733; Fax 907.0274; E-mail: [email protected] JEL classification: F310, F410 and F420. - iii - Contents Page Preface 1 Abstract 1 I. INTRODUCTION 2 II. CAPITAL ACCOUNT OR CURRENT ACCOUNT CRISES? 5 III. FLEXIBLE PRICES AND FLEXIBLE EXCHANGE RATES 8 IV. INFLEXIBLE PRICES AND FLEXIBLE EXCHANGE RATES 10 V. EXCHANGE RATES AS A BUFFER FOR REAL SHOCKS 15 VI. -

Left-Wing Strategies to Solve the Euro Crisis

LEFT-WING STRATEGIES TO SOLVE THE EURO CRISIS What answers can the left provide to the euro-zone crisis and the world economic crisis? The Left Party has begun analysing this important question in light of the continued growth of euro-scepticism. In order to further the debate, the Rosa Luxemburg Foundation has published a study by the economists Heiner Flassbeck and Costas Lapavitsas on the causes of the crisis and possible solutions. This study is summarised in the following, but can be found in full at: http://www.rosalux.de/publication/39478. HEINER FLASSBECK THE EURO AT A CROSSROADS THE CONCLUSIONS OF THE STUDY BY FLASSBECK AND LAPAVITSAS Let’s use our last chance! The study by Heiner Flassbeck and Costas Lapavitsas, The Systemic Crisis of the Euro – True Causes and Effective Therapies, which has been published by the Rosa Luxemburg Foundation, clearly demonstrates that the common European currency is seriously under threat. This situation has come about because the basic conditions needed for successful monetary union have been disregarded since the very beginning. Consequently, European Economic and Monetary Union (EMU) has been managed according to principles that fail to grasp its complexity, and EMU policy, which is blinded by the ideology of its main actors, has continually focused on fiscal issues. Since the beginning of the European crisis, which occurred at the same time as the world economic crisis, attempts to prevent the dissolution of European monetary union have been marred by serious mistakes. Once again, fiscal issues – in this case, the sovereign debt crisis – have become the focus of policy, and this has hindered the development of a comprehensive and targeted therapy package that could solve the problems currently faced by EMU. -

THE CRISIS BEHIND the CRISIS: the EUROPEAN CRISIS AS a MULTI-DIMENSIONAL SYSTEMIC FAILURE of the EU Faculty of Law, University of Cambridge 31 March-1St April

THE CRISIS BEHIND THE CRISIS: THE EUROPEAN CRISIS AS A MULTI-DIMENSIONAL SYSTEMIC FAILURE OF THE EU Faculty of Law, University of Cambridge 31 March-1st April PROGRAMME WEDNESDAY 30TH MARCH 20:30 Welcome drinks, King’s College Bar THURSDAY 31ST MARCH 09:00 Welcome 09:15 Keynote Speech I: Professor Michelle Everson, Birkbeck University of London 10:45 Coffee 11.00 THE CRISIS AS A CRISIS OF THE EU’S IDENTITY (Chair: Dr Theodore Konstadinides, University of Surrey) Professor Magnus Ryner, King’s College London ‘The International Political Economy or European Authoritarian Neo-Liberalism’ Dr Charalampos Kouroundis, Aristotle University of Thessaloniki ‘The Roots of the European Crisis: A Historical Perspective’ Dr Maria Tzanakopoulou, UCL ‘The EU from Below: Ruptures with the Neo-Liberal Consensus?’ Hent Kalmo, Université de Paris Nanterre ‘Nostalgia for the Future: The Eurocrisis and the End of Self-Fulfilling Europe’ 12:30 Lunch 13:30 THE CRISIS AS A CRISIS OF DEMOCRATIC AND POLITICAL LEGITIMACY (Chair: Dr Davor Jancic, Asser Institute) Elia Alexiou, Université de Paris Nanterre ‘Who's Afraid of the European Demos?: The Uneasy Relationship between European Union and Referenda as a Sign of Identity and Democratic Legitimacy Crisis’ Dr Petr Agha, University of Prague ‘The Empire of Principle’ Jorge Correcher Mira, University of Valencia ‘Ideological Crisis in the EU: Consequences in the Evolution of Crime and Penalty from the Political Economy of Punishment’ 15:00 Coffee 15.15 THE CRISIS AS A NORMATIVE CRISIS OF THE EU ECONOMIC MODEL (Chair: -

The Policy Space Debate

APRIL 2007 Asia Program SPECIAL REPORT No. 136 The Policy Space Debate: Does a JOMO KWAME SUNDARAM Globalized and Multilateral Economy Policy Space? Overcoming Constraints to Pursuing National Development Constrain Development Policies? Strategies EDITED BY BHUMIKA MUCHHALA PAGE 8 ABSTRACT This Special Report asks whether multilateral economic policies constrain the abil- HEINER FLASSBECK Macroeconomic Policy Space ity of developing countries to choose the best mix of economic polices for achieving sustain- and the Global Imbalances able and equitable development. Jomo Kwame Sundaram illustrates the significance of PAGE 17 policy space for national development strategies, and assesses the principal sources of con- straints imposed by international financial institutions (IFIs) on policy space in developing CARLOS CORREA Constraining Policy Space in countries. Heiner Flassbeck contends that intermediate exchange rate regimes and the Intellectual Property development of a multilateral framework for exchange rates would enable developing coun- PAGE 22 tries to better align their monetary policies with their development priorities. Carlos Correa links intellectual property rights (IPR) rules in the global trade regime to equitable development ELAINE ZUCKERMAN by presenting several counter-arguments to the dominant proposition that IPRs are necessary Policy Space and the Gendered Impacts of International to promote knowledge and innovation, and by providing a historical analysis of IPR policy. Financial Institutions Elaine Zuckerman demonstrates -

Syriza's Rise and Fall

Interview: New Masses—13 stathis kouvelakis SYRIZA’S RISE AND FALL Syriza won power in January 2015 as an anti-austerity party—the most advanced political opposition so far to the hardening deflationary poli- cies of the Brussels–Berlin–Frankfurt axis. Six months later, the Tsipras government forced through the harshest austerity package Greece had yet seen. This trajectory was a predictable outcome of the contradiction embod- ied in Syriza’s programme: reject austerity, but keep the euro. Why was Tsipras so incapable of envisaging a course inside the eu but outside the Eurozone, the position of Sweden, Denmark, Poland and half a dozen other European countries? irst, one shouldn’t underestimate the popularity of the euro in the southern-periphery countries—Greece, Spain, Portugal—for whom joining the eu meant accessing political and economic modernity. For Greece, in particular, it meant Fbeing part of the West in a different way to that of the us-imposed post- civil war regime. It seemed a guarantee of the new democratic course: after all, it’s only since 1974 that Greece has known a political regime similar to other Western countries, after decades of authoritarianism, military dictatorship and civil war. The European Community also offered the promise of combining prosperity with a social dimension, supposedly inherent to the project, which sealed the political com- pact that emerged after the fall of the Junta. Joining the euro seemed the logical conclusion of that process. Having the same currency as the most advanced countries has a tremendous power over people’s imagination—carrying in your pocket the same currency as Germans or Dutch, even if you are a low-paid Greek worker or pensioner—which new left review 97 jan feb 2016 45 46 nlr 97 those of us who’d been in favour of exiting the euro since the start of the crisis tended to underestimate. -

1 Crisis & Catharsis in EU Integration Dr. Mai'a K. Davis Cross

Crisis & Catharsis in EU Integration Dr. Mai’a K. Davis Cross Northeastern University [email protected] Abstract This article seeks to explain how and why the EU’s relatively frequent existential crises – complete with ‘end of Europe’ rhetoric – ultimately result in new areas of consensus regarding the EU’s integration project. During the course of these existential crises, member states are able to release underlying societal tensions that might have stood as stumbling blocks to further consensus, and thus achieve a sense of ‘catharsis,’ as evidenced by convergence in attitudes. To illustrate this process, the article examines the case of the Eurozone crisis, and describes how North-South tensions that pre-dated this crisis period were openly aired during the height of the crisis, and created a window of opportunity for leaders to agree to a number of far-reaching policies in the economic and financial area. Keywords: narratives, crisis, integration, social construction Introduction The evolving European order, which centers on the process of European Union (EU) integration, is characterized by both incremental change and critical junctures of crisis. This article focuses on the latter, and aims to provide an agenda for future research into European crises. Even a casual look at the history of the EU since its inception in 1957 shows that at numerous periods through its development, the EU (or EEC/EC in its previous incarnations) has been portrayed as being in severe crisis, even on the verge of dissolution. I examine why these 1 predictions, particularly those of existential threat (episodes in which it seems the “end of Europe” is at hand), have continually been proven false. -

Heiner Flassbeck: Exchange Rate Management in Developing

Heiner Flassbeck Acting Director UNCTAD Heiner Flassbeck Exchange Rate Management in Developing Countries: The Need for a Multilateral Solution in a Globalized Economy The discussion about adequate ex- to reconcile with the expectation of change rate systems for developing neoclassical general equilibrium mod- countries takes a new turn. Whereas, els where poor economies with a low in the 1990s the official doctrine of endowment of capital receive the the Washington-based finance insti- scarce resource from rich countries tutions has been the corner solution with an abundant endowment of capi- idea, developing countries either ab- tal. The fact that the most successful solutely fix their exchange rate against countries in the South have violated an international anchor currency of that “law” puzzles many orthodox ob- float freely, after the Asian crises the servers and leads them to argue that international economics community holding United States treasuries is a favored the return to floating. But waste of resources as this money only a few countries accepted this ad- could have been used much more ef- vice. Most of the countries affected ficiently by investing it in fixed capi- by the storm of the financial crises in tal or by using it for more imports of Asia and in Latin America decided to investment goods. use the opportunity of a low valua- For policymakers in developing tion of their currencies and the swing countries, the fact that exchange rate from current account deficit to sur- movements directly influence the plus to unilaterally fix their exchange overall competitiveness of a country rate or – at least – to frequently inter- and have the potential to directly im- vene in the currency market to avoid prove the overall trade performance the rapid return of their currencies to of the majority of their firms and the pre-crisis levels. -

Explaining the Euro Crisis: Current Account Imbalances, Credit Booms and Economic Policy in Different Economic Paradigms

Explaining the Euro Crisis: Current Account Imbalances, Credit Booms and Economic Policy in Different Economic Paradigms Engelbert Stockhammer, Collin Constantine and Severin Reissl November 2016 Post Keynesian Economics Study Group Working Paper 1617 This paper may be downloaded free of charge from www.postkeynesian.net © Engelbert Stockhammer, Collin Constantine and Severin Reissl Users may download and/or print one copy to facilitate their private study or for non-commercial research and may forward the link to others for similar purposes. Users may not engage in further distribution of this material or use it for any profit-making activities or any other form of commercial gain. Explaining the Euro crisis: Current Account Imbalances, Credit Booms and Economic Policy in Different Economic Paradigms Abstract: The paper proposes a post-Keynesian analysis of the Eurozone crisis and contrasts interpretations inspired by New Keynesian, New Classical, and Marxist theories. The origin of the crisis is the emergence of a debt-driven and an export-driven growth model, which resulted in a rapid increase in private debt ratios and current account imbalances. The reason the crisis escalated in southern Europe, but not in other parts of the world, lies in the unique dysfunctional economic policy regime of the Euro area. European fiscal rules and the Troika impose fiscal austerity on countries in crisis and the separation of fiscal and monetary spaces has made countries vulnerable to sovereign debt crises and forced them to comply. We analyse the role different paradigms attribute to current account imbalances, fiscal policy and monetary policy. Remarkably, opposing views on the relative importance of cost and demand developments in explaining current account imbalances can be found in both heterodox and orthodox economics. -

The Global Dilemma and the European Paradox Prof. Dr. Heiner

Cernobbio, April 2019 The Global Dilemma and the European Paradox Prof. Dr. Heiner Flassbeck www.makroskop.eu We are living in extraordinary times: Never in history interest rates were so low Short term rate in the UK flassbeck-economics.de -2% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8% Source: OECD, Deutsche Bundesbank Deutsche OECD, Source: 1) 1956 We Annual yield on 10 on yield Annual 1957 1958 Geneva and Zurich, February Geneva February Zurich, and 2015 1959 1960 are 1961 1962 1963 entering - 1964 year government bonds (monthly basis), minus annual rate of change CPI (monthly basis) (monthly CPI change of rate annual minus basis), (monthly bonds government year 1965 1966 1967 1968 1969 1970 1971 1972 a 1973 1974 recession 1975 1976 1977 1978 Long 1979 1980 1981 - 1982 inGermany rates interest real term 1983 1984 with 1985 1986 1987 1988 1989 zero 1990 1991 1992 1993 interest 1994 1995 1996 flassbeck 1997 1998 1999 2000 - economics.de 2001 rtates 2002 2003 2004 1) 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 We are entering a recession without a revival of investment Investment ratio of private companies in Germany 1) 25 24 23 nominal 22 21 20 19 18 17 16 15 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 1) Bruttoanlageinvestitionen (neue Anlagen) im Verhältnis zur Bruttowertschöpfung der privaten Unternehmen ohne Grundstücks- und Wohnungswesen. Wert für 2018 berechnet mit Hilfe der Bruttoanlageinvestitionen der nichtstaatlichenSektoren ohne Wohnbauten. -

Flassbeck Spiecker.Indd

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Flassbeck, Heiner; Spiecker, Friederike Article — Published Version The euro: A story of misunderstanding Intereconomics Suggested Citation: Flassbeck, Heiner; Spiecker, Friederike (2011) : The euro: A story of misunderstanding, Intereconomics, ISSN 1613-964X, Springer, Heidelberg, Vol. 46, Iss. 4, pp. 180-187, http://dx.doi.org/10.1007/s10272-011-0381-8 This Version is available at: http://hdl.handle.net/10419/68312 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu DOI: 10.1007/s10272-011-0381-8 Invited Paper Heiner Flassbeck* and Friederike Spiecker** The Euro – a Story of Misunderstanding From the very beginning of the European Monetary Union the crucial institutions, the European Commission and the European Central Bank, led by mainstream economic thinking, were not up to their task of controlling the core of the system effectively. -

Eurozone Austerity Policies Will Spark New Crisis in 2013 Costas Lapavitsas, Therealnews, December 11, 2012

Eurozone Austerity Policies Will Spark New Crisis in 2013 Costas Lapavitsas, TheRealNews, December 11, 2012 PAUL JAY, SENIOR EDITOR, TRNN: Welcome to The Real News Network, and welcome to the first edition of The Lapavitsas Report with Costas Lapavitsas, who now joins us from London, where he's a professor in economics at the School of Oriental and African Studies at the University of London. He's a regular columnist for The Guardian newspaper. His most recent book is Crisis in the Eurozone. Thanks for joining us again, Costas. COSTAS LAPAVITSAS, PROF. ECONOMICS, UNIV. OF LONDON: Hello, Paul. It's nice to be here with you. JAY: So we're just a few weeks away from 2013. How does this year look, this coming year? LAPAVITSAS: I'm afraid that it doesn't look very good at all for economies in general and for working people in particular. And I want to stress that. This is shaping up very badly. The main source of concern is of course the eurozone and the continuing crisis in the eurozone. Now, financial markets have gone quiet or quieter in the last few months, couple of months, and people have been lulled into thinking that the eurozone crisis has been resolved. That is not actually true. The reason why financial markets have gone quieter is because in September Mr. Draghi of the European Central Bank intervened and basically said that he was going to buy bonds of countries in trouble freely. And that made speculation against peripheral eurozone country debt unprofitable. So financial markets went quiet, and people began to think that the eurozone crisis might be on its way out. -

Strengthening the Architecture of the International Monetary System

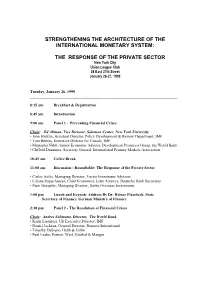

STRENGTHENING THE ARCHITECTURE OF THE INTERNATIONAL MONETARY SYSTEM: THE RESPONSE OF THE PRIVATE SECTOR New York City Union League Club 38 East 37th Street January 26-27, 1999 Tuesday, January 26, 1999 ___________________________________________________________________________ 8:15 am Breakfast & Registration 8:45 am Introduction 9:00 am Panel 1 - Preventing Financial Crises Chair : Ed Altman, Vice Director, Salomon Center, New York University • John Hicklin, Assistant Director, Policy Development & Review Department, IMF • Tom Bernes, Executive Director for Canada, IMF • Mustapha Nabli, Senior Economic Adviser, Development Prospects Group, the World Bank • Clifford Dammers, Secretary General, International Primary Markets Association 10:45 am Coffee Break 11:00 am Discussion - Roundtable: The Response of the Private Sector • Carlos Asilis, Managing Director, Vector Investment Advisors • Liliana Rojas-Suarez, Chief Economist, Latin America, Deutsche Bank Securities • Peter Geraghty, Managing Director, Darby Overseas Investments 1:00 pm Lunch and Keynote Address By Dr. Heiner Flassbeck, State Secretary of Finance, German Ministry of Finance 2:30 pm Panel 2 - The Resolution of Financial Crises Chair: Andres Solimano, Director, The World Bank • Karin Lissakers, US Executive Director, IMF • Daniel Jackson, General Director, Nomura International • Timothy DeSieno, Hebb & Gitlin • Paul Leake, Partner, Weil, Gotshal & Manges 3:30 pm Coffee Break 3:45 pm Discussion - The Response of the Private Sector Chair : Andres Solimano, Director, The World